Market Overview

| Study Period | 2021 - 2031 |

|---|---|

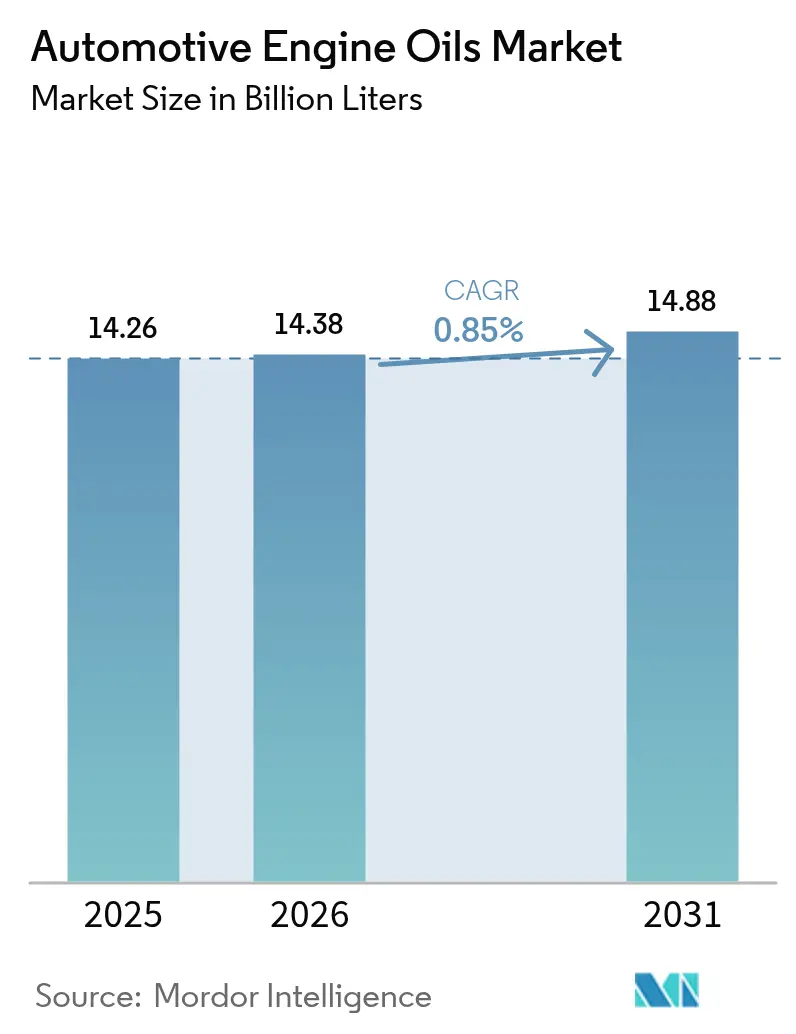

| Market Volume (2026) | 14.38 Billion liters |

| Market Volume (2031) | 14.88 Billion liters |

| Growth Rate (2026 - 2031) | 0.85% CAGR |

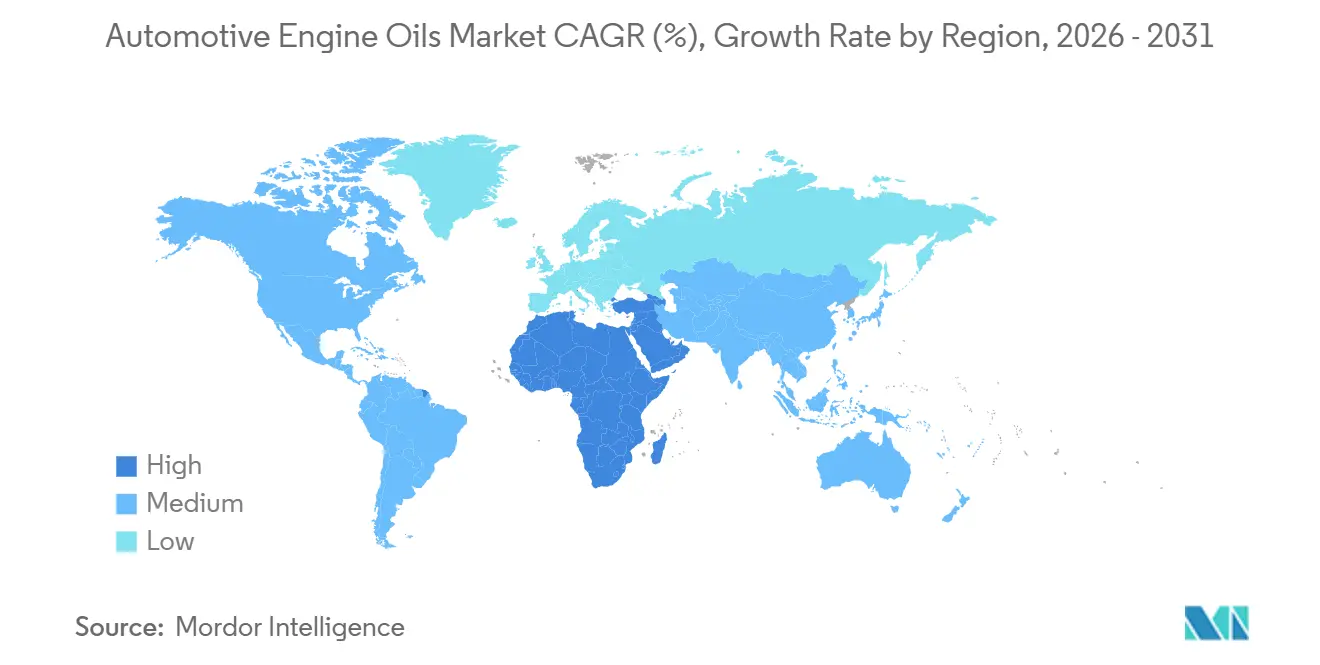

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Engine Oils Market Analysis by Mordor Intelligence

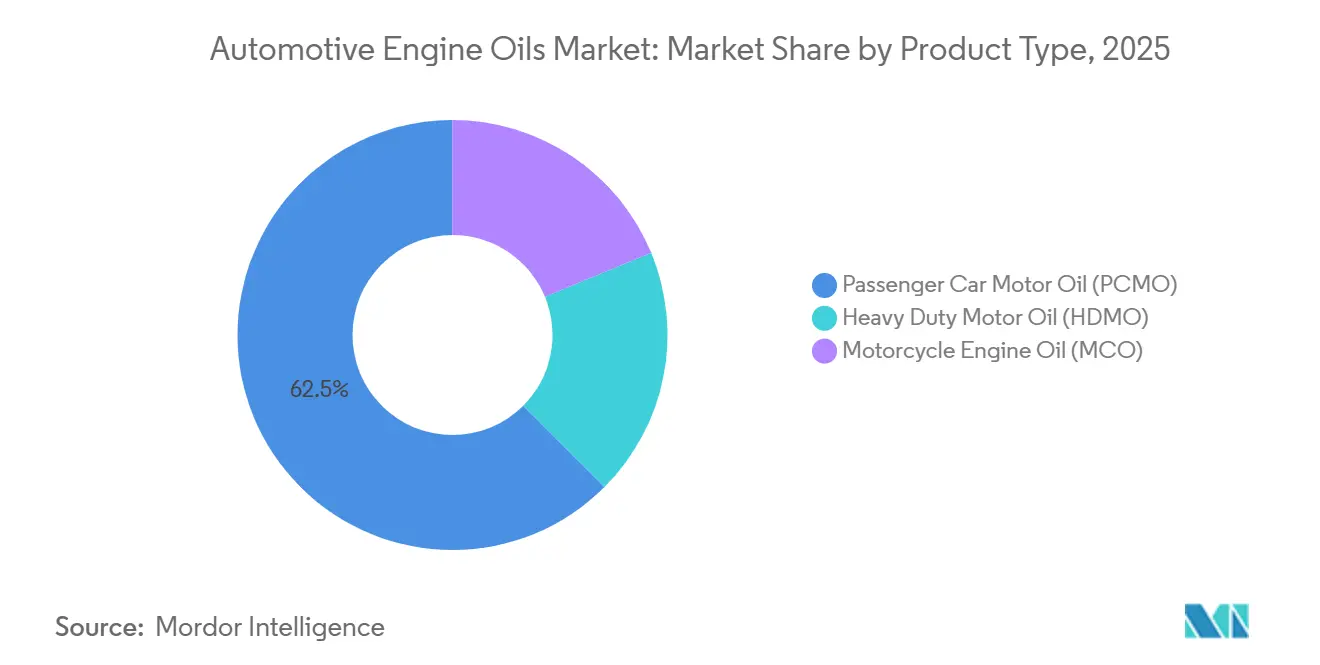

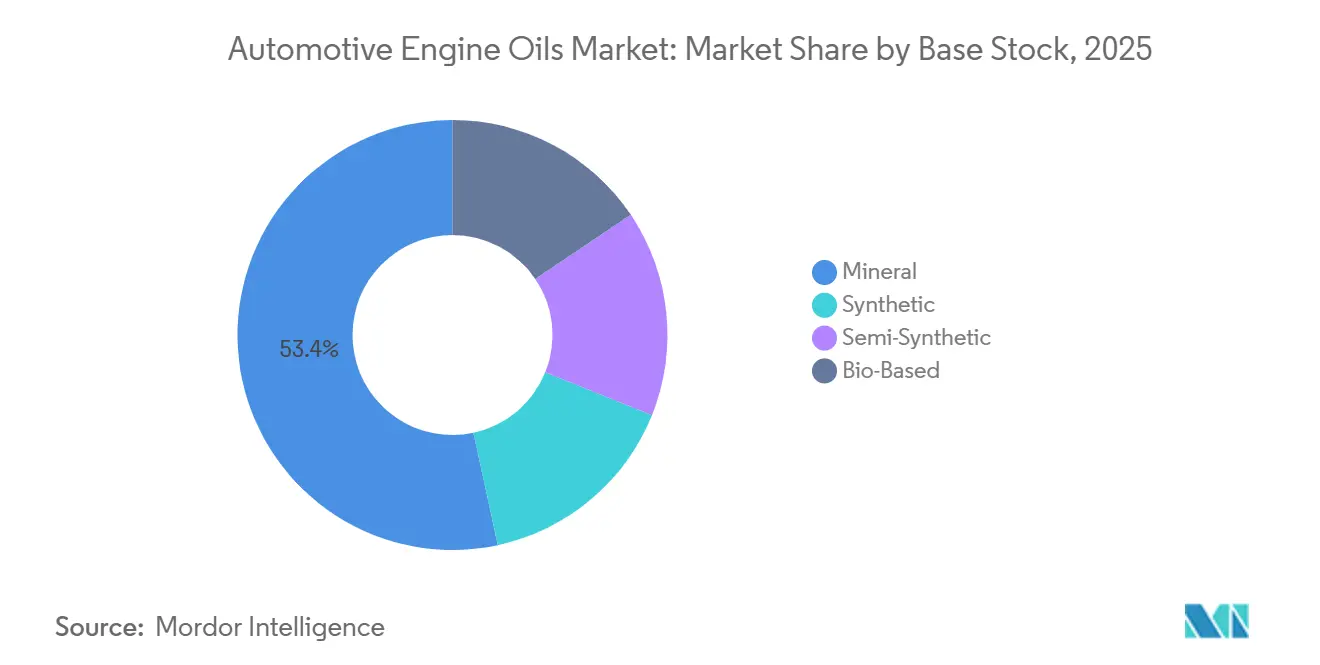

The Automotive Engine Oils Market size is expected to increase from 14.26 billion liters in 2025 to 14.38 billion liters in 2026 and reach 14.88 billion liters by 2031, growing at a CAGR of 0.85% over 2026-2031. Passenger car motor oil (PCMO) accounted for a 62.49% volume share in 2025, but its outlook is dampened by accelerating vehicle electrification that lowers lubricant demand per car. Motorcycle engine oil (MCO) counters this drag, expanding at a robust 9.97% CAGR on the back of two-wheeler parc growth in India, Indonesia, and Vietnam. Synthetic formulations are penetrating faster than mineral grades as original-equipment manufacturers (OEMs) mandate lower-viscosity 0W-20 and 0W-16 oils for hybrid thermal cycles. Meanwhile, Asia-Pacific anchored 43.89% of global volume in 2025, aided by India’s forecast 29 million two-wheeler sales in fiscal 2027. Integrated majors are re-engineering refineries toward higher-margin Group III and IV base stocks, even as counterfeit products erode brand equity in developing aftermarkets.

Key Report Takeaways

- By product type, passenger car motor oil commanded 62.49% of the Automotive Engine Oils market share in 2025, while Motorcycle Engine Oil is forecast to advance at a 9.97% CAGR through 2031.

- By base stock, mineral oils retained a 53.38% share of the Automotive Engine Oils market size during 2025, yet fully synthetic grades are projected to expand at a 1.18% CAGR to 2031.

- By geography, Asia-Pacific led with 43.89% revenue share in 2025; the Middle East and Africa are expected to post the fastest 2.29% CAGR over the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital quick-lube platforms and e-commerce broadening aftermarket reach | +0.2% | North America, Europe, Asia | Short term (≤ 2 years) |

| Emerging-market two-wheeler and passenger-car parc expansion | +0.3% | India, Indonesia, Vietnam | Medium term (2-4 years) |

| OEM proprietary long-drain specifications increasing oil value per fill | +0.15% | North America, Europe, China | Medium term (2-4 years) |

| PAO and GTL supply expansion lowering synthetic cost | +0.1% | Global | Long term (≥ 4 years) |

| ICE-synthetic oils optimized for hybrid thermal cycles | +0.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Quick-Lube Platforms and E-Commerce Broadening Aftermarket Reach

Digital catalogues that match vehicle identification numbers with lubricant specifications have slashed ordering errors from roughly 10-14% to near 6%, trimming costly returns and letting distributors channel premium synthetics to workshops[1]Infopro Digital Automotive, “OATS Lubricant Advisor Coverage,” oats-automotive.com. These platforms integrate enterprise-resource-planning feeds so inventory, pricing, and promotions update in real time, accelerating order-to-delivery cycles. The approach also improves SKU visibility, letting blenders rationalize low-turn mineral grades and devote blending capacity to 0W-20 and 5W-30 synthetics. Digital engagement supports tailored seasonal campaigns that expand the automotive engine oils market by capturing DIY buyers who once relied on brick-and-mortar retailers. Over the short term, incremental unit growth stems mainly from Europe and North America, where repair shops already depend on electronic parts catalogues.

Emerging-Market Two-Wheeler and Passenger-Car Parc Expansion

India’s two-wheeler sales are projected at 29 million units in fiscal 2027, up 7-9% from FY 2025, while Indonesia logged 6.4 million motorcycle sales in 2025 and maintained a 3.1% year-on-year lift in January 2026. Vietnam added 3.4 million bikes in 2025, the fastest regional climb at 14.9%. Rising incomes translate to a premiumization tilt toward 150-350 cc models, which require multigrade or semi-synthetic oils that carry higher margins. Passenger-car ownership is also widening, with Pakistan and Bangladesh both adding more than 300,000 new cars annually, thereby enlarging the automotive engine oils market. These structural tailwinds outweigh electrification headwinds for two-wheelers in the medium term.

OEM Proprietary Long-Drain Specifications Increasing Oil Value Per Fill

OEMs now promote proprietary 0W-20 or 0W-30 formulations capable of 10,000-mile drains, doubling traditional service intervals. Castrol’s long-drain diesel oils promise 80,000-mile change intervals when combined with oil analysis programs. Longer drains reduce workshop visits but increase revenue per fill, reshaping the automotive engine oils market toward fewer, higher-value transactions. Independent blenders must therefore invest in advanced additive packs and certification fees to stay listed on OEM approval sheets. In China and Europe, proprietary specs also bundle extended emissions-equipment warranties, strengthening dealer lock-in.

PAO and GTL Supply Expansion Lowering Synthetic Cost

Chevron Phillips Chemical doubled low-viscosity PAO output at its Beringen plant to 120,000 t/y in August 2025[2]Chevron Phillips Chemical, “Press Release: Beringen PAO Expansion,” cpchem.com. INEOS Oligomers added 120,000 tons/year at Chocolate Bayou the same year. Rising Group IV supply tempers price premiums and enables wider OEM migration to 0W-16 grades that support stringent fuel-economy norms. QatarEnergy’s 2024 on-spec ramp-up of its 10,000 barrels-per-day gas-to-liquids base-oil project will inject new Group III+ volumes, further compressing synthetic spreads versus Group II. Over the long term, these projects expand the automotive engine oils market by making full synthetics affordable in price-sensitive regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality lubricants in developing markets | -0.15% | Malaysia, Indonesia, South Africa | Short term (≤ 2 years) |

| Rapid OEM electrification targets shrinking long-term ICE fleet | -0.25% | Global | Long term (≥ 4 years) |

| Stricter used-oil disposal and recycling compliance costs | -0.1% | India, EU, select U.S. states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Low-Quality Lubricants in Developing Markets

Malaysian authorities seized RM 1 million worth of fake oils in Selangor during November 2025, arresting 42 suspects. In January 2026, South African officials confiscated more than 20,000 liters of illicit lubricants bottled in 210 liters drums. Counterfeits erode legitimate volumes, harm engines, and undermine consumer trust, shrinking the automotive engine oils market in price-sensitive countries. OEMs now embed QR authentication on caps, yet enforcement gaps persist. Short-term growth is therefore trimmed until regulatory oversight tightens and buyers shift from informal channels to branded e-commerce.

Rapid OEM Electrification Targets Shrinking Long-Term ICE Fleet

The International Energy Agency expects global electric-vehicle stock to hit 250 million units by 2030, up from 45 million in 2023. Shell predicts more than 50% of new car sales will be electric by 2030. Pure battery models virtually eliminate engine oil demand, removing roughly 4 liters per passenger car per year from forecasts. Commercial-vehicle electrification, while lagging, is accelerating as global zero-emission mandates extend to long-haul fleets. Consequently, the automotive engine oils market faces a structural volume decline in the long term, even if hybrid oils sustain value per litre.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Motorcycle Oils Surge Amid Passenger Car Stagnation

Passenger car motor oil maintained the largest share at 62.49% in 2025, yet electrification curbs its long-term outlook. Motorcycle engine oil is forecast to climb at 9.97% CAGR to 2031, the quickest trajectory within the automotive engine oils market. Growing two-wheeler populations in India and Indonesia underpin volume expansion, while premium 150-350 cc bikes demand semi-synthetic multigrades that lift revenue per litre. Heavy-duty motor oil remains linked to freight activity; API’s forthcoming PC-12 categories tighten oxidation and wear limits for 2027 model engines.

Viscosity trends also diverge. PCMO 0W-20 and 5W-30 grades gain ground as OEMs chase fuel-economy credits. HDMO fleets in North America adopt 10W-30 to extract 1-1.5% fuel savings, even though 15W-40 still dominates vocational segments. In price-sensitive ASEAN markets, monograde MCO lingers, yet premium multigrades outpace overall two-wheeler oil growth. This bifurcation sustains differentiated pricing that enlarges the automotive engine oils market size for high-performance synthetics targeting hybrids and motorcycles alike.

By Base Stock: Synthetic Gains Ground as PAO Capacity Expands

Mineral oils continued to dominate with a 53.38% slice of the Automotive Engine Oils market share in 2025, but synthetic volumes are climbing at a 1.18% CAGR as PAO and Group III costs fall. OEM mandates for low-viscosity 0W-16 lubricants compatible with turbocharged gasoline direct-injection engines accelerate synthetic uptake in North America, Europe, and China. Semi-synthetic blends bridge the affordability gap in emerging Asia, helping sustain growth while meeting OEM warranty requirements.

On the supply side, Chevron Phillips Chemical and INEOS collectively added 240,000 tons/year of new low-viscosity PAO capacity in 2025, while ExxonMobil’s 8,000-barrel-per-day Baytown Group III project will lift US supply from 2028. The incremental output narrows the price differential between Group II+ and Group III+, encouraging formulators to switch platforms without sacrificing margins. Mineral oils, however, still dominate heavy-duty and rural motorcycle channels where cost sensitivity outweighs performance gains, ensuring the blended landscape retains diversity within the broader automotive engine oils market.

Geography Analysis

Asia-Pacific produced 43.89% of the global Automotive Engine Oils market volume in 2025, led by India, Indonesia, and Vietnam. India’s premium shift toward mid-capacity bikes alongside rising export volumes has kept demand buoyant despite nascent BEV adoption. Indonesia’s steady GDP growth and repeated interest-rate reductions boosted motorcycle financing, translating into higher lubricant consumption. Vietnam’s double-digit two-wheeler growth, including early adoption of electric bikes, creates a mixed demand picture where ICE oils remain essential for a large in-use parc. Regional counterfeit crackdowns, such as Malaysia’s November 2025 seizure, reinforce the push toward authenticated branded products that support value retention within the automotive engine oils market.

North America emphasizes high-performance synthetics and extended drains. NHTSA’s CAFE Rule III keeps OEMs focused on reducing tailpipe CO₂ from gasoline engines, sustaining lubricant innovation designed for turbocharged downsized powertrains. ExxonMobil’s additional Group III capacity will reduce reliance on imports, while API PC-12 will shift heavy-duty fleets toward lower-viscosity oils by 2027. The United States also witnesses growth in hybrid models, creating demand for oils with enhanced corrosion inhibitors. Canada remains a cold-start market, accelerating adoption of 0W-20 grades with improved low-temperature pumpability. Collectively, these factors lift premium-grade penetration and enhance profitability per litre, upholding the automotive engine oils market in a region slowly transitioning toward electrification.

The Middle East and Africa represent the fastest regional CAGR at 2.29% through 2031. Saudi Aramco’s Luberef will expand Yanbu base-oil output to 1.53 million tons/year by late 2026, improving regional supply security. Yet the Strait of Hormuz disruption in March 2026, which slashed 20 million barrels per day of crude and products, demonstrated lingering geopolitical risk. African markets exhibit elevated counterfeit activity, with South Africa’s January 2026 sting revealing large-scale illicit blending. Nonetheless, rising vehicle imports and gradual GDP growth sustain consumption growth, inching the automotive engine oils market size upward across both passenger and commercial segments.

Competitive Landscape

The Automotive Engine Oils market is moderately fragmented. Start-ups and regional blenders pursue e-commerce channels to bypass legacy distributors. Price transparency pressures margins for commodity 20W-50 monogrades, but majors defend share using marketing alliances with ride-hailing fleets and quick-lube chains. Hybrid-specific and long-drain formulations function as premium profit pools that justify research and development spending. Overall, the market’s structure remains moderately concentrated yet fiercely contested, with innovation cycles quickening as electrification redefines future demand patterns.

Automotive Engine Oils Industry Leaders

TotalEnergies

Shell plc

Exxon Mobil Corporation

Chevron Corporation

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: LIQUI MOLY announced the start of local motor oil production in the United States to serve American customers more quickly and with more flexibility.

- June 2025: BP plc formally launched the sale of its Castrol lubricants business as part of a broader USD 20 billion divestment strategy by 2027. The move reflects BP’s shift toward upstream oil and gas operations.

Global Automotive Engine Oils Market Report Scope

Automotive engine oils or lubricants are sophisticated chemical solutions engineered to minimize mechanical friction, mitigate thermal stress, and maintain internal component cleanliness. The primary function of these fluids is to establish a hydrodynamic film between high-speed moving parts, such as crankshaft journals and cylinder walls, preventing metal-to-metal contact and catastrophic engine failure.

The Automotive Engine Oils market report is segmented by product type (passenger car motor oil, heavy duty motor oil, and motorcycle engine oil), and base stock (mineral, synthetic, semi-synthetic, and bio-based). The report also covers the market size and forecasts for automotive engine oils in 31 countries across major regions. The market forecasts are provided in terms of volume (liters).

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

By Geography

| Asia-Pacific | China |

| India | |

| Pakistan | |

| Bangladesh | |

| Japan | |

| South Korea | |

| Taiwan | |

| Australia | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Iran | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Pakistan | ||

| Bangladesh | ||

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Australia | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Iran | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for automotive engine oils be by 2031?

Consumption is projected to reach 14.88 billion litres by 2031, expanding at a modest 0.85% CAGR from 2026 to 2031.

Which product category is growing fastest?

Motorcycle engine oil is forecast to post a 9.97% CAGR through 2031, fueled by expanding two-wheeler fleets in emerging Asia.

Why are synthetic engine oils gaining ground?

New PAO and Group III capacity is cutting cost premiums, while OEMs demand low-viscosity 0W-16 and 0W-20 grades that only synthetics can deliver efficiently.

What risks do counterfeit lubricants pose?

Counterfeits damage engines, erode brand trust and subtract legitimate sales, trimming short-term growth, especially in Malaysia, Indonesia and South Africa.

How will electrification affect lubricant suppliers?

Rising EV adoption removes engine-oil volume, forcing suppliers to pivot to hybrid-specific fluids, specialty EV coolants and industrial lubricants to offset the decline.

Page last updated on: