Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

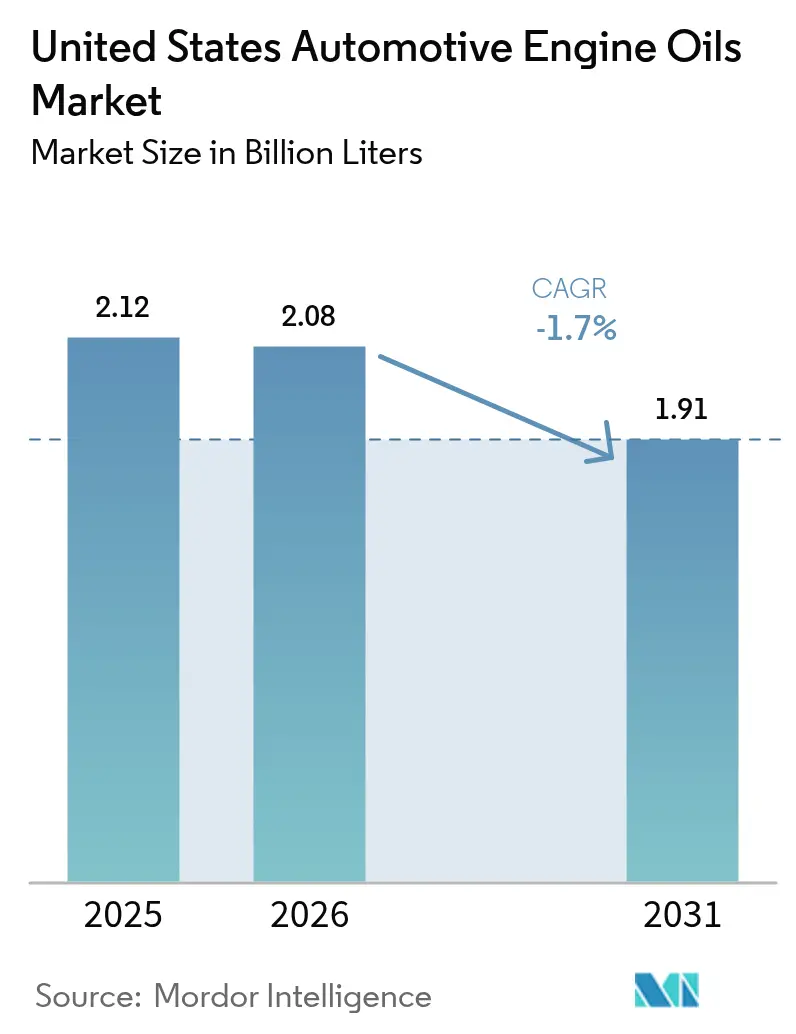

| Base Year Market Size (2025) | 2.12 Billion liters |

| Market Volume (2026) | 2.08 Billion liters |

| Market Volume (2031) | 1.91 Billion liters |

| Growth Rate (2026 - 2031) | -1.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Automotive Engine Oils Market Analysis by Mordor Intelligence

The United States Automotive Engine Oils Market size is projected to be 2.12 billion liters in 2025, 2.08 billion liters in 2026, and decline to 1.91 billion liters by 2031, declining at a CAGR of -1.7% from 2026 to 2031. A structural shift is driving this contraction: life-of-vehicle factory-fill programs, predictive-maintenance algorithms, and ultra-low-viscosity specifications raise lubricant quality even as per-vehicle consumption falls. API SP and ILSAC GF-7 standards, introduced in March 2025, have already licensed more than 1,800 formulations that rely on costlier additive chemistries and extensive dynamometer testing. Meanwhile, Ford’s Intelligent Oil-Life Monitor more than doubled the average drain interval to 10,000 miles by late 2025, and Valvoline secured Cummins approval for a 100,000-mile heavy-duty oil the same year. Although these advances elevate product margins, they also shrink the serviceable volume pool, anchoring the long-term downtrend for the United States automotive engine oils market.

Key Report Takeaways

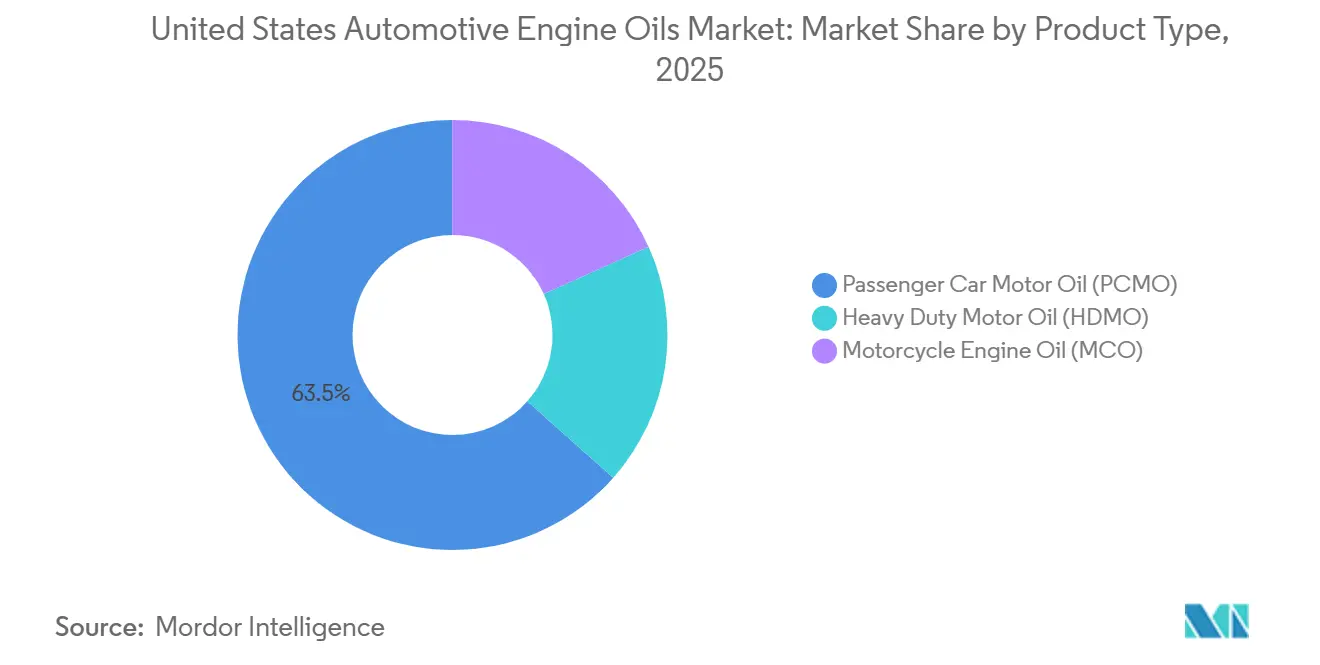

- By product type, passenger car motor oil commanded 63.45% of the United States Automotive Engine Oils market share in 2025, while motorcycle engine oil posted the most resilient performance with a -1.64% CAGR through 2031.

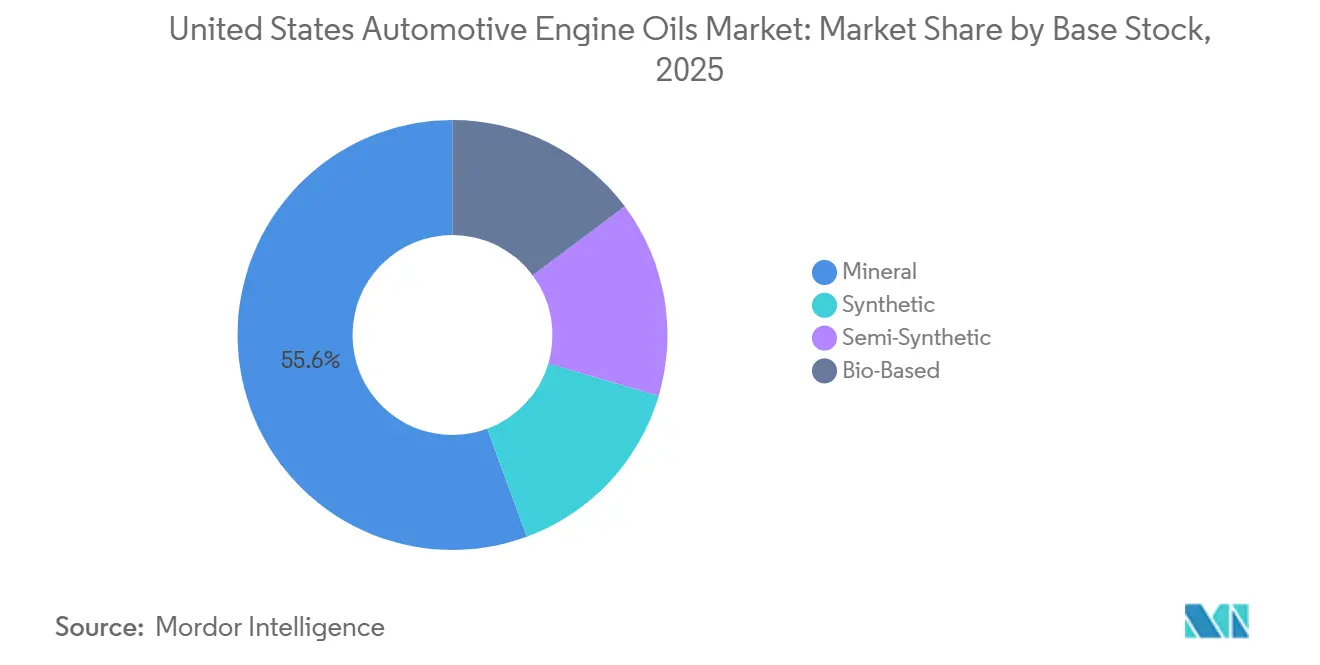

- By base stock, mineral oils held a 55.63% share of the United States Automotive Engine Oils market size in 2025; synthetic variants recorded the mildest decline at -1.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| API SP/ILSAC GF-7 specification roll-out | +0.3% | National, concentrated in Detroit and Southeastern assembly corridors | Medium term (2-4 years) |

| Rapid shift to full-synthetic and less than or equal to 0W-20 grades | +0.4% | National, accelerated in California and the Northeast | Medium term (2-4 years) |

| Aging vehicle parc more than 12 years | +0.5% | National, strongest in Rust Belt and rural markets | Long term (≥ 4 years) |

| AI-driven predictive-maintenance programs | +0.6% | National, earliest in commercial fleets | Medium term (2-4 years) |

| OEM carbon-credit strategies favoring ultra-low-viscosity factory fill | +0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

API SP/ILSAC GF-7 Specification Roll-Out

Launched in March 2025, API SP and ILSAC GF-7 have already licensed more than 1,800 blends, yet certification backlogs of 6-9 months persist because only a handful of North American labs own the requisite Sequence IX and Sequence X stands[1]American Petroleum Institute, “Engine Oil Licensing & Certification System,” api.org. Each test cycle costs USD 50,000-75,000 and ties up a dynamometer for up to six weeks, favoring producers with captive facilities. Ford, General Motors, Toyota, Honda, and Stellantis mandated GF-7 for 2026 factory fills, letting certified brands capture 10-15% price premiums over legacy API SN Plus oils. As mid-tier blenders exit or co-license additive packages from Lubrizol or Infineum, volume erosion continues, but margin per litre widens, adding roughly 0.3 percentage points to the United States automotive engine oils market CAGR.

Rapid Shift to Full-Synthetic and less than or equal to 0W-20 Grades

Synthetic formulas represented close to 68% of lubricant value in 2024, with 0W-20 appearing in 42% of new-vehicle owner manuals. By 2025, more than 70% of model-year specifications called for 0W-20 or thinner, and select hybrid lines moved to 0W-16 to meet tightening EPA fleet-average CO₂ ceilings of 85 g/mile by 2032. Blenders responded by investing in Group III and PAO feedstock: ExxonMobil’s Singapore Resid Upgrade, commissioned early 2025, added 1.2 million ton/year of high-viscosity-index base stocks for global allocation. Although litre demand keeps falling, the synthetic share grows fast enough to contribute a net 0.4 percentage-point lift to the United States automotive engine oils market trajectory.

Aging Vehicle Parc more than 12 Years Sustaining Demand

The average light vehicle on U.S. roads hit 12.8 years in 2025, with roughly 290 million units still powered by internal-combustion engines. Owners of older cars, who often lack connected-car diagnostics, stick to 3,000-5,000-mile oil changes and favor lower-priced mineral blends at quick-lube chains and DIY retailers. Valvoline reported that 29% of US drivers performed their own oil change at least once during fiscal 2025 because of inflationary pressure. This entrenched maintenance culture adds about 0.5 percentage points to the United States automotive engine oils market CAGR, although the cushion weakens after 2028 as early-2010s models retire.

AI-Driven Predictive-Maintenance Programs Extending Drain Intervals

Connected-vehicle telemetry now feeds machine-learning algorithms that measure oil oxidation in real time. Ford’s Intelligent Oil-Life Monitor, GM’s OnStar diagnostics, and Castrol’s Fleet Health collectively lifted average service intervals to at least 10,000 miles by late 2025. In heavy-duty transport, Cummins approved Valvoline’s Premium Blue One Solution Gen 2 for 100,000-mile drains, triple the legacy standard, cutting annual oil demand per Class-8 truck by roughly one-third. Because telematics adoption in commercial fleets already tops 60%, the drag on volumes is sizable, subtracting about 0.6 percentage points from the United States automotive engine oils market CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Base-oil price and supply volatility | -0.4% | Gulf Coast and Midwest refining hubs | Short term (≤ 2 years) |

| Limited GF-7 test-stand capacity | -0.2% | Blenders without captive facilities | Short term (≤ 2 years) |

| OEM life-of-vehicle factory-fill oils | -0.8% | High new-vehicle-sales states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Base-Oil Price and Supply Volatility

Group II and Group III spot prices swayed 15-20% quarter-to-quarter during 2024-2025 because of refinery turnarounds and lighter crude slates, leaving independent blenders exposed to margin compression[2]Petroleum Economist, “Base Oil Price Volatility,” petroleum-economist.com. Additive elements such as molybdenum and boron climbed 12-18%, further squeezing costs. US refinery additions remain unlikely under energy-transition pressure, so volatility will persist and shave around 0.4 percentage points off the United States automotive engine oils market CAGR until new Asian capacity backfills domestic shortfalls.

Limited GF-7 Test-Stand Capacity Delaying Certifications

Fewer than 10 independent North American labs own the engines needed for Sequence IX and X testing, so mid-tier blenders faced certification queues of up to one year in 2025. Each sequence run costs as much as USD 75,000, and large producers use long-term contracts to block-book capacity, leaving smaller brands to wait or license pre-certified additive packages from Lubrizol or Infineum. This bottleneck keeps higher-margin GF-7 synthetics from coming online quickly, trimming roughly 0.2 percentage points from the United States automotive engine oils market CAGR over the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Anchors Volume, MCO Declines Slowest

Passenger car motor oil accounted for 63.45% of the United States Automotive Engine Oils market size in 2025, reflecting the nation’s 290 million-unit vehicle parc. Although internal-combustion cars continue to dominate the fleet, PCMO volume is forecast to fall as electrification, telematics, and factory-fill longevity reshape service patterns. Heavy-duty motor oil volumes erode more slowly because long-haul diesels remain hard to electrify and typically stay in service 15-20 years. Motorcycle engine oil shows the smallest contraction (-1.64% CAGR during the forecast period (2026-2031)) because cruiser and touring riders maintain legacy drain intervals and have limited electric alternatives.

The internal mix is also changing. Within PCMO, 0W-20 and thinner grades expand fastest, driven by OEM mandates tied to multi-pollutant standards. Conventional 10W-30 and 10W-40 grades retreat to a shrinking pool of vehicles built before 2015. HDMO mirrors this trend as fleets adopt 0W-30 or 5W-30 CK-4 oils for cold-start efficiency. Valvoline’s 100,000-mile Cummins-approved HDMO illustrates how extended drains deepen litre-volume shrinkage even when product value rises.

By Base Stock: Synthetic Gains Share Despite Overall Decline

Mineral oils supplied 55.63% of the 2025 volume in the United States Automotive Engine Oils market, but they are falling as consumers trade up to blends and full synthetics. Synthetics, fueled by OEM mandates and longer drain certifications, decline more gently at -1.53% CAGR during the forecast period (2026-2031), allowing share to rise within the shrinking pool. Semi-synthetic blends appeal to price-sensitive drivers who want a step-up benefit without paying full PAO premiums.

Emerging bio-based and re-refined Group III+ options, Novvi’s plant-derived SynNova and ReGen III’s re-refined stocks, tap corporate sustainability scorecards and federal procurement guidelines. TotalEnergies’ Rubia EV3R and Quartz EV3R, both launched in 2025, contain more than 50% recycled base oil and meet heavy-duty or passenger-car GF-7 requirements. Although these volumes remain small, they are the fastest-growing niche, projected to reach 5-8% of base-stock volume by 2031.

Geography Analysis

California, Texas, and Florida collectively account for most of the United States Automotive Engine Oils market volume because of large light-vehicle registrations and high annual mileage. California leads adoption of 0W-16 and 0W-20 synthetic grades owing to stringent state emissions rules that stack on top of federal CAFE standards; consequently, synthetic penetration already exceeds 80% of factory fills at West-Coast dealerships.

Midwestern states, Ohio, Michigan, and Indiana, demonstrate higher retention of 5W-30 and 10W-30 because the regional fleet skews older. Quick-lube chains concentrate in these markets to serve high DIY participation, sustaining mineral-oil demand despite national headwinds. The Rust Belt also hosts several additive and blending facilities that rely on proximity to both refinery feedstock and interstate logistics corridors, anchoring supply even as local demand eases.

The Gulf Coast remains the production backbone of the United States automotive engine oils market, with Texas and Louisiana refineries supplying Group II and Group III base stocks to blenders nationwide. Hurricane-related shutdowns create spot shortages that reverberate inland, amplifying price volatility. New or expanded capacity, such as ExxonMobil’s Singapore barrels aimed at export back-fill, will not fully cushion these swings, so regional distributors often forward-contract six months of supply as a hedge.

Competitive Landscape

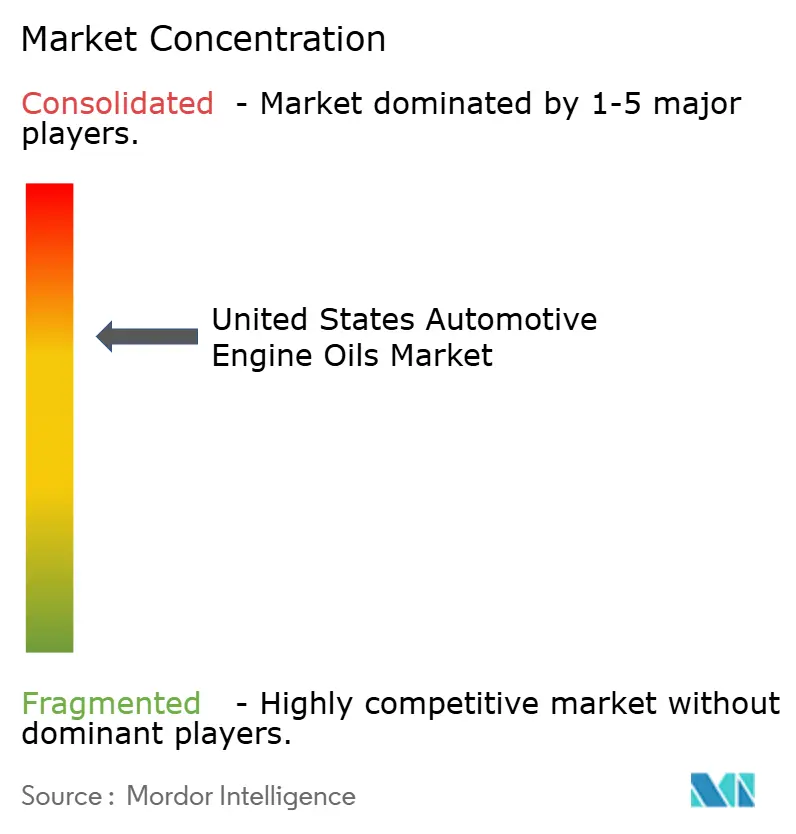

The United States Automotive Engine Oils market is moderately consolidated. Technology also redraws boundaries. Lubrizol, Infineum, and Afton Chemical patent nano-additive systems that mitigate low-speed pre-ignition while lowering sulfur and phosphorus content, giving blenders a pathway to meet GF-7 without costly base-stock upgrades. Castrol and Ford embed proprietary algorithms into vehicle infotainment stacks, locking in oil-life data streams that tether customers to recommended service brands. As PC-12 heavy-duty standards (CL-4 and FB-4) go live in January 2027, integrated producers with captive test stands appear best positioned to defend share and margin.

United States Automotive Engine Oils Industry Leaders

ExxonMobil Corporation

Shell plc

Chevron Corporation

Saudi Arabian Oil Co.

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: LIQUI MOLY announced the start of local motor oil production in the United States to serve American customers more quickly and with more flexibility.

- June 2025: BP plc formally launched the sale of its Castrol lubricants business as part of a broader USD 20 billion divestment strategy by 2027. The move reflects BP’s shift toward upstream oil and gas operations.

United States Automotive Engine Oils Market Report Scope

Automotive engine lubricants are sophisticated chemical solutions engineered to minimize mechanical friction, mitigate thermal stress, and maintain internal component cleanliness. The primary function of these fluids is to establish a hydrodynamic film between high-speed moving parts, such as crankshaft journals and cylinder walls, preventing metal-to-metal contact and catastrophic engine failure.

The United States Automotive Engine Oils market report is segmented by resin type (passenger car motor oil, heavy duty motor oil, and motorcycle engine oil) and base stock (mineral, synthetic, semi-synthetic, and bio-based). The market forecasts are provided in terms of volume (liters).

By Resin Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Resin Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How large is the United States automotive engine oils market in 2026?

The United States automotive engine oils market size stands at 2.08 billion litres in 2026.

What is the expected CAGR for US automotive engine oils between 2026 and 2031?

Volume is projected to contract at –1.70% CAGR over the 2026-2031 interval.

Which product segment holds the largest share of demand?

Passenger car motor oil leads, accounting for 63.45% of 2025 volume.

Why are synthetic engine oils gaining share even as total litres fall?

OEM mandates for 0W-20 and 0W-16 factory fills, extended-drain approvals, and fuel-economy gains favor Group III and PAO synthetics.

How will EPA’s February 2026 action affect lubricant demand?

The rescission of the GHG Endangerment Finding could slow OEM adoption of ultra-low-viscosity factory fills, marginally easing the pace of synthetic uptake.

Page last updated on: