Market Overview

| Study Period | 2021 - 2031 |

|---|---|

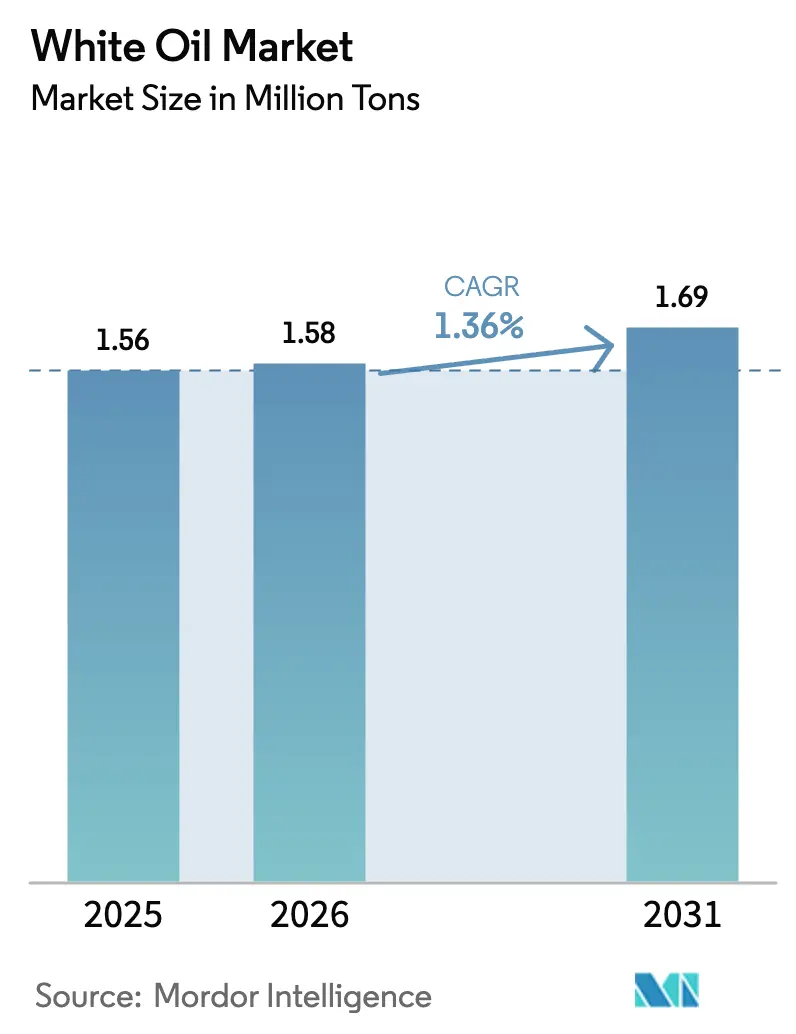

| Market Volume (2026) | 1.58 Million tons |

| Market Volume (2031) | 1.69 Million tons |

| Growth Rate (2026 - 2031) | 1.36% CAGR |

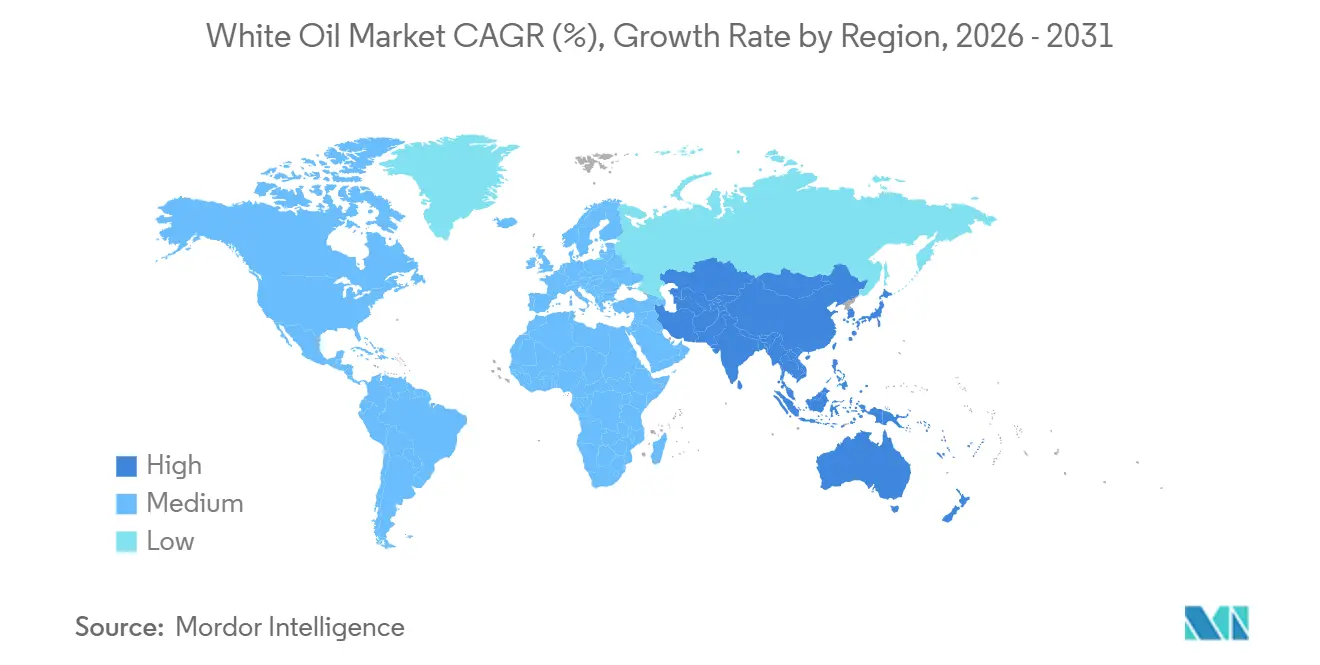

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

White Oil Market Analysis by Mordor Intelligence

The White Oil Market size is expected to grow from 1.56 Million tons in 2025 to 1.58 Million tons in 2026 and is forecast to reach 1.69 Million tons by 2031 at 1.36% CAGR over 2026-2031. Demand is tilting toward high-purity grades because hydrocracked Group II and III oils comply with U.S. and European pharmacopoeial limits on sulfur, nitrogen, and polycyclic aromatic hydrocarbons. Pharmaceutical manufacturers in Asia-Pacific are locking in multi-year supply agreements to secure USP-grade inputs, while flexible-packaging converters in Europe substitute recycled inks with food-grade white oils to meet MOAH and MOSH limits. Personal-care brands in India and the Middle-East continue to rely on light-paraffinic carriers that satisfy Ayurvedic and halal standards, reinforcing regional divergence in formulation strategy. Competitive dynamics favor integrated refiners that can swing paraffinic streams between fuels and specialties, yet niche blenders retain pricing power when they bundle viscosity customizations with batch certificates of analysis.

Key Report Takeaways

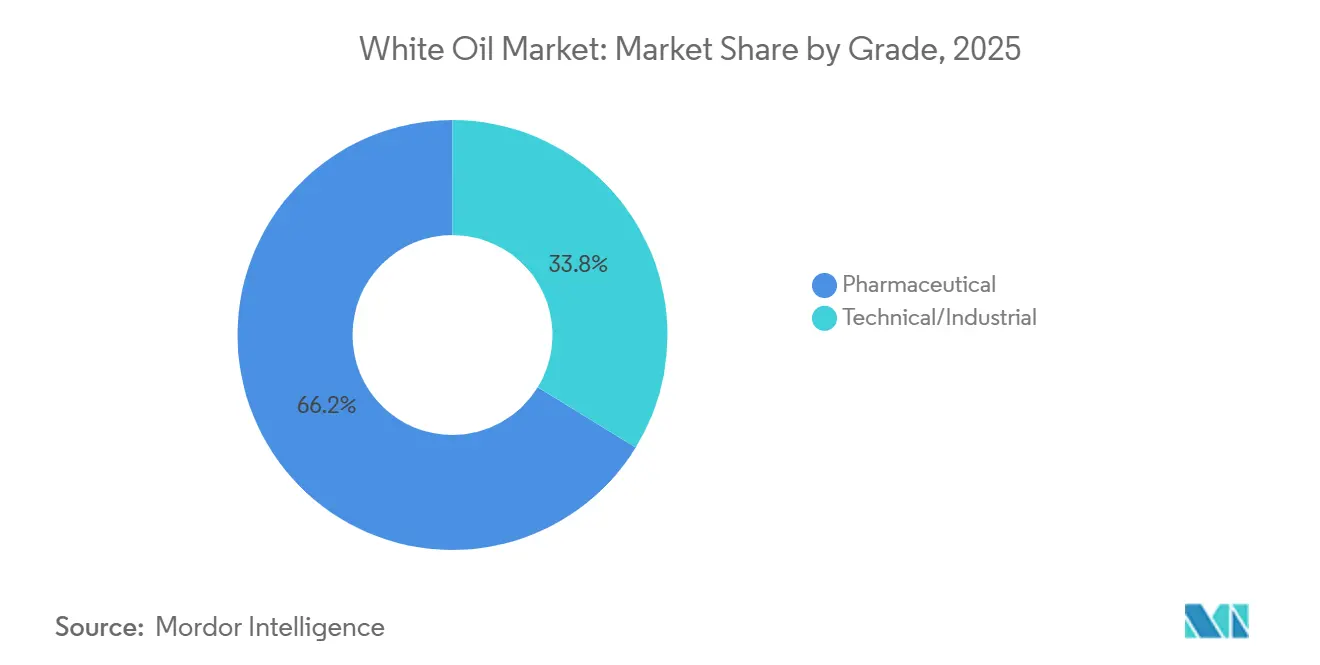

- By grade, pharmaceutical grade retained 66.23% of the white oil market share in 2025 and is advancing at a 1.32% CAGR to 2031.

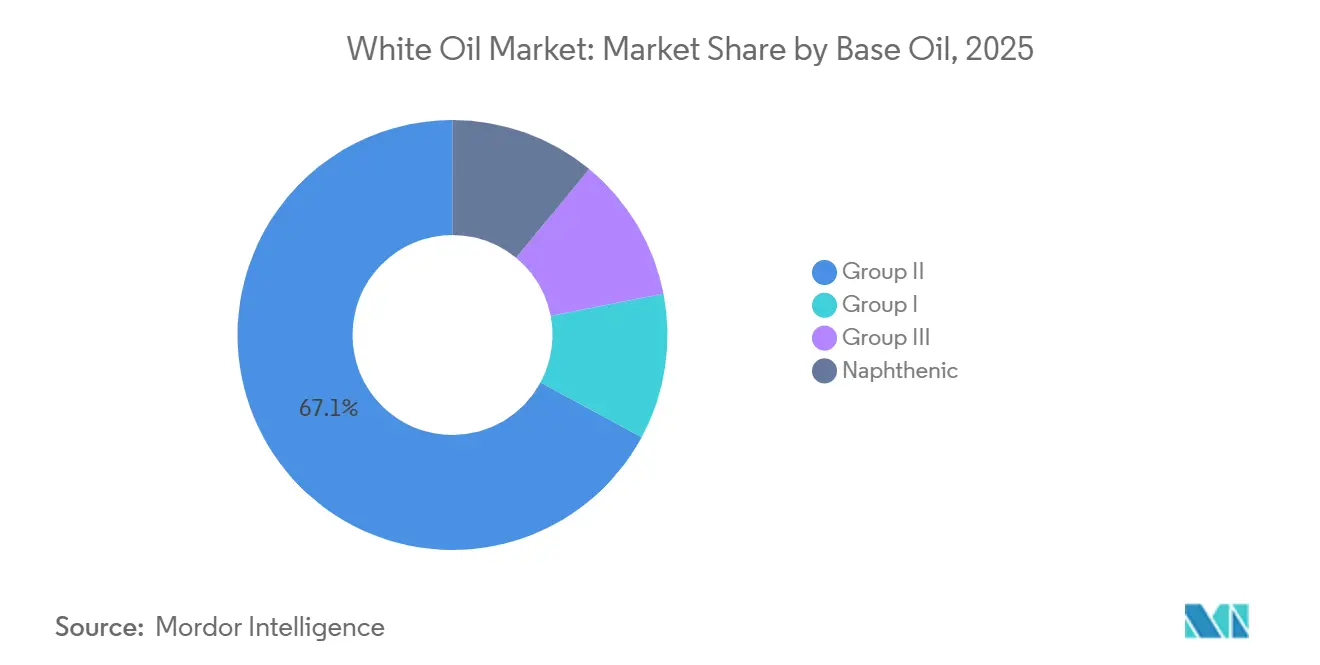

- By base oil, Group II accounted for 67.12% of the white oil market share in 2025 and is advancing at a 1.73% CAGR to 2031.

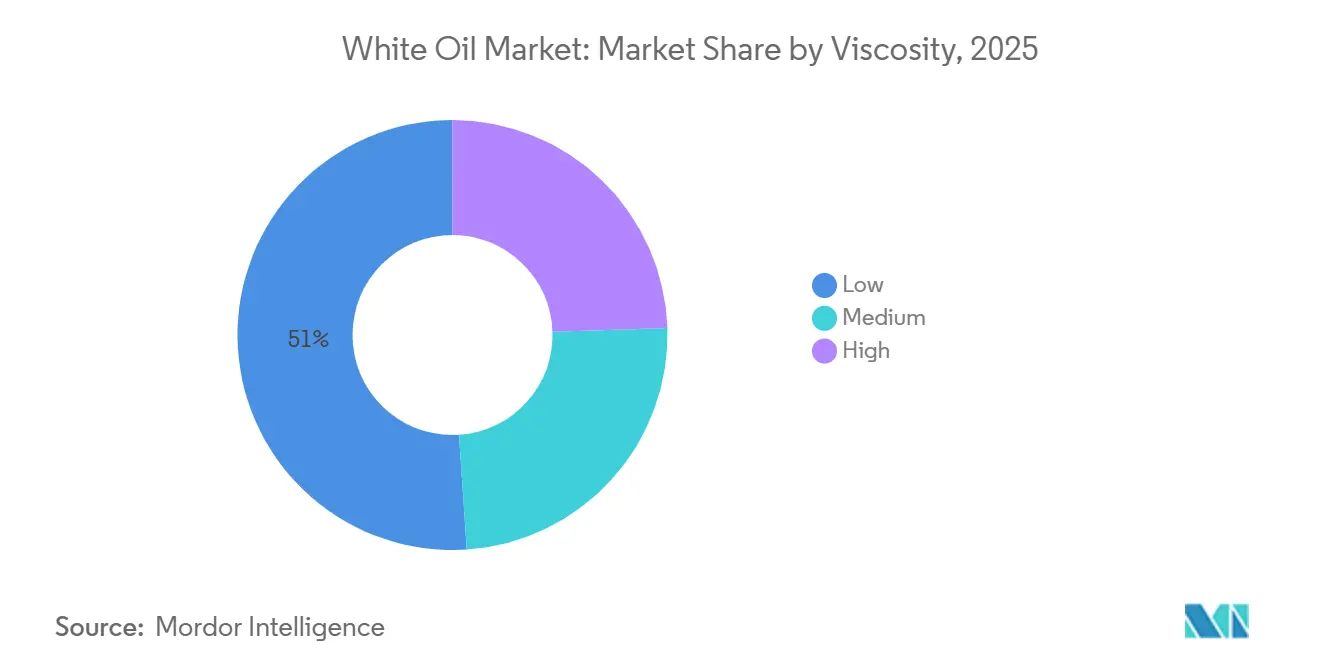

- By viscosity, low-viscosity held 51.08% of volume in 2025 and is advancing at a 1.41% CAGR to 2031.

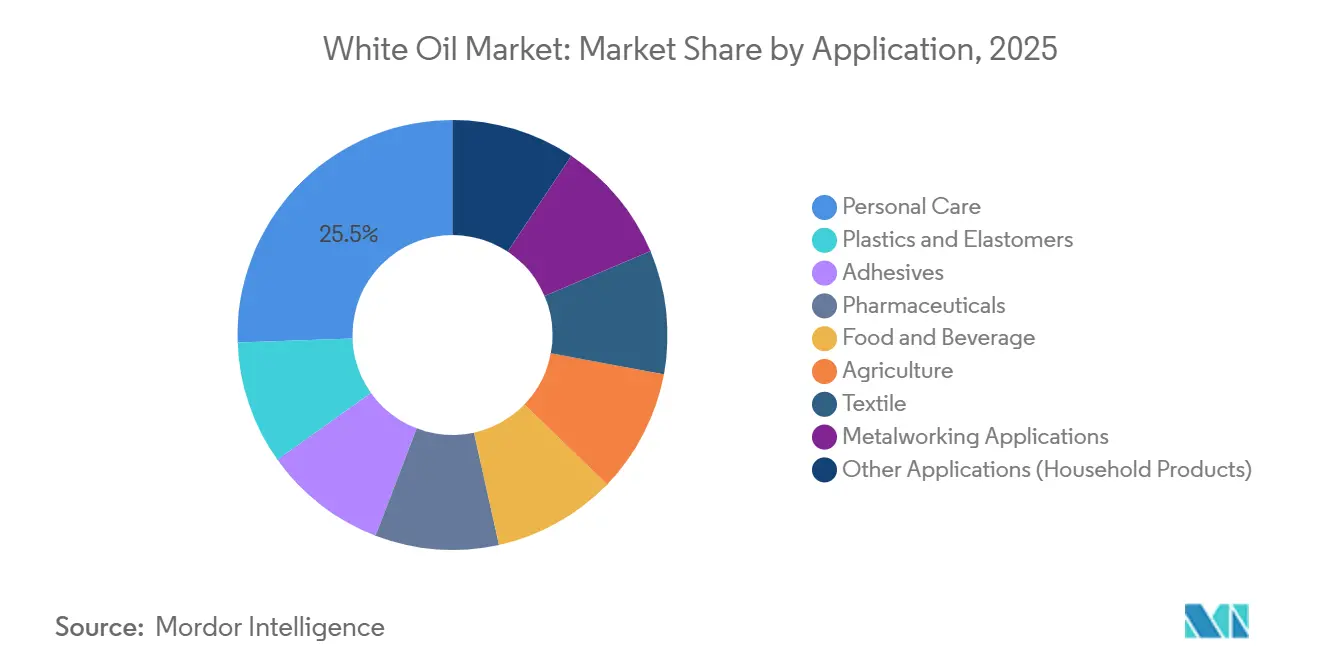

- By application, personal care accounted for 25.56% of the white oil market share in 2025 and is advancing at a 2.11% CAGR to 2031.

- By geography, Asia-Pacific captured 63.44% of global volume in 2025 and the region is advancing at a 1.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global White Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Asia-Pacific Biologics Fill-Finish Lines Demanding USP-Grade White Oils | +0.3% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| Europe MOAH/MOSH Limits Accelerating Shift to Food-Grade White Oils in Packaging | +0.2% | Europe, with adoption in North America | Short term (≤ 2 years) |

| Indian Ayurvedic-Cosmetics Boom Fuelling Light-Paraffinic White-Oil Usage | +0.2% | India, with export gains in Middle-East and Southeast Asia | Medium term (2-4 years) |

| Expansion in Polymer and Plastic Processing in Emerging Economies | +0.2% | Asia-Pacific, Middle-East, Latin America | Long term (≥ 4 years) |

| GCC Pharma Capacity Build-Out Boosting Imports of High-Purity Grades | +0.1% | Saudi Arabia, UAE, with regional distribution to North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Asia-Pacific Biologics Fill-Finish Lines Demanding USP-Grade White Oils

Biologics capacity additions in China and India exceeded 50 new fill-finish sites between 2024 and 2025. Each line specifies white oils with endotoxin below 0.25 EU/mL and PAH below 3%, criteria that exclude legacy Group I streams while favoring hydrocracked outputs. Contract manufacturers serving Western biosimilar demand impose FDA-aligned documentation, so suppliers providing real-time batch analytics win long-term contracts. The trend lifts volumes of premium low-viscosity grades and compresses margins for commodity blenders that lack pharmaceutical validation.

Europe MOAH/MOSH Limits Accelerating Shift to Food-Grade White Oils in Packaging

Converters of flexible packaging are adopting hydrogenated white oils certified under FDA 21 CFR 178.3620(a) after EFSA confirmed MOAH migration above 2 mg/kg in dry foods. Brand owners pay EUR 200-300 per ton premiums for certified lots, yet smaller suppliers struggle to absorb third-party testing costs. Rapid compliance cycles mean specialty refiners with in-house GC-FID capability secure volume gains.

Indian Ayurvedic-Cosmetics Boom Fuelling Light-Paraffinic White-Oil Usage

India’s Ayurvedic personal-care value surged 12% year-over-year in 2025. White oils compliant with Bureau of Indian Standards IS 1083 act as stable, odorless carriers for herbal actives and satisfy halal traceability for exports to Gulf retailers[1]Bureau of Indian Standards, “IS 1083: Light Liquid Paraffin,” bis.gov.in. Domestic producers expanded capacity at double-digit rates, creating a regional hub that offsets European volume softness.

Expansion in Polymer and Plastic Processing in Emerging Economies

PVC and PP compounders in Southeast Asia and the Middle-East employ technical-grade white oils as internal lubricants that cut melt viscosity and reduce die buildup. Vietnam’s plastics output advanced 9% in 2025, absorbing additional medium-viscosity supply. Saudi Arabia’s TA’ZIZ hub imported white oils for its USD 5 billion PVC complex because local refineries prioritize fuels. Sustained infrastructure investment suggests long-run support despite potential circular-economy pivots.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Micro-Plastic Directive Curbing Mineral-Oil-Based Cosmetic Formulations | -0.2% | Europe, with spillover to North America and Australia | Short term (≤ 2 years) |

| North American Infant-Food Players Pivoting to Bio-Based Esters | -0.1% | United States, Canada | Medium term (2-4 years) |

| IMO-2020 Sulfur Caps Tightening High-Quality Feedstock Supply | -0.1% | Global, most acute in Asia-Pacific refining hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Micro-Plastic Directive Curbing Mineral-Oil-Based Cosmetic Formulations

Regulation 2023/2055 restricts synthetic polymer microparticles in rinse-off cosmetics, prompting European brands to substitute mineral-oil carriers with plant-derived esters to avoid petrochemical labeling[2]European Commission, “Regulation 2023/2055,” eur-lex.europa.eu . Although mineral oils are not microplastics, consumer perception drove a 3-4% decline in regional personal-care demand during 2025. Reformulation cycles average 18-24 months, so most substitution will conclude by 2027.

North American Infant-Food Players Pivoting to Bio-Based Esters

Nestlé and Abbott eliminated mineral oils from spray-drying and emulsifier systems in 2024 after focus-group data showed 68% parental distrust of “mineral oil” descriptors. Falling bio-ester prices narrowed cost gaps to USD 100-150 per ton, making switchovers economically neutral. The restraint is localized yet signals sensitivity to non-scientific consumer sentiment in high-visibility applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharmaceutical Dominance Anchored by Regulatory Barriers

Pharmaceutical grade held 66.23% of 2025 volume, underlining entrenched regulatory moats that discourage new entrants. The segment grows at a 1.32% CAGR, reflecting mature demand rooted in chronic-care and dermatology formulations. Batch-to-batch viscosity must remain within ±0.5 cSt, and heavy metals stay below 1 ppm, requirements that raise compliance costs. Technical-grade volumes rise faster in plastics and adhesives where cost trumps purity, but lack of pharmacopoeial coverage limits their conversion into higher-margin channels.

Second-order effects concentrate on the procurement side. Leading pharmaceutical firms now demand blockchain-enabled traceability that tracks drum numbers to refinery runs, reducing supply flexibility for smaller blenders. Meanwhile, industrial users tolerate wider viscosity bands, enabling discount suppliers to survive on price plays. The segmentation thus preserves a two-tier structure that insulates incumbents yet caps growth potential. The white oil industry maintains this divide by reinvesting in analytical labs rather than new distillation hardware.

By Base-Oil: Group II Hydrocracking Gains Share on Purity Mandates

Group II captured 67.12% of volume in 2025 and is progressing at a 1.73% CAGR, fuelled by sulfur-free outputs that align with European food-contact directives. In 2025, Group III remained a niche premium option with higher oxidative stability premiums. Group I volumes erode in pharmaceutical and food uses but continue in adhesives where cost pressures dominate.

Integrated refiners use swing units to toggle between fuels and specialty outputs. When marine-fuel margins spiked after IMO 2020, paraffinic feedstocks diverted away from white oils, lifting spot prices by 6-8%. Despite this volatility, Group II capacity additions on the U.S. Gulf Coast and in China reaffirm long-term supply security. Group III opportunities lie in injectable-drug devices and high-temperature metalworking fluids, yet price elasticity tempers adoption. The white oil market continues to migrate toward hydrocracked purity, an irreversible shift for regulated sectors.

By Viscosity: Low-Viscosity Grades Propelled by Pharmaceutical and Cosmetic Uptake

Low-viscosity contributed 51.08% of 2025 throughput and enjoys a 1.41% growth trajectory. This cut underpins ophthalmic preparations, baby oils, and biologics fill-finish lubricants where droplet size and spreadability matter. Medium grades hold share in extrusion and molding, balancing fluidity with film strength, while high-viscosity products fill niche lubrication roles. Producing narrow 8-10 cSt cuts needs deeper hydrocracking and tight distillation, adding USD 80-120 per ton to production costs, yet premiums in pharmaceutical tenders offset the expense.

Pressure on medium grades stems from synthetic polyalphaolefins in metalworking that offer longer drain intervals. High-viscosity oils confront bio-grease substitution in environmentally sensitive jobs. Suppliers that master vacuum distillation and real-time viscosity control sustain competitive advantage as variability tolerances tighten. In absolute terms, low-viscosity lines will anchor volume growth for the white oil market through 2031.

By Application: Personal Care Leads Growth Despite Clean-Beauty Headwinds

Personal care consumed 25.56% of 2025 volume and is forecast to advance at a 2.11% CAGR, the quickest among applications. Ayurvedic hair oils, halal moisturizers, and mass-market baby products adopt light-paraffinic carriers thanks to odorless profiles and resistance to rancidity. Plastics and elastomers follow, yet circular-economy policies in Europe temper momentum. Adhesives, food, and beverage absorb steady volumes due to MOAH/MOSH compliance upgrades.

Pharmaceutical demand, although slower growing, remains larger in absolute tonnage. Agricultural, textile, and household uses shrink or stagnate depending on regional adoption of water-based substitutes. Personal-care resilience could waver if EU microplastic sentiment spreads to Asia-Pacific or if bio-ester costs fall further. For now, the white oil market finds its highest incremental gains in beauty and hygiene segments that blend cultural preferences with regulatory permissibility.

Geography Analysis

Asia-Pacific anchored 63.44% of volume in 2025, yet its 1.35% forecast CAGR lags personal-care growth, showing that bulk polymer processing is plateauing. China contributes major consumption through pharmaceutical clusters in Jiangsu and plastics bases in Guangdong, but stricter refinery emission targets limit incremental capacity. India emerges as the fastest-growing node, benefiting from Ayurvedic cosmetics, domestic drug production, and polymer expansions in Gujarat. Southeast Asian economies, notably Vietnam and Thailand, upscale white-oil imports for flexible packaging and food handling, though freight volatility introduces procurement risk.

In North America, U.S. pharmaceutical excipient standards shield demand for USP-grade lots, yet bio-based substitutions in infant food and microplastic-driven cosmetic reformulations curtail upside. Canada’s reliance on imports sustains steady buying but lacks internal refining upgrades. Mexico’s growth hinges on technical-grade needs from rising auto parts and packaging output. Regulatory complexity lengthens product-qualification cycles, favoring incumbents.

Europe’s demand is shaped by food-contact reforms and antiplastics sentiment. Germany leads adoption of premium food-grade oils in packaging, offsetting weaker personal-care call-offs. United Kingdom and France mirror this pattern, while Nordic countries progress faster toward bio-alternatives. Southern Europe sustains mineral-oil legacy formulas in cosmetics and processed foods but faces harmonization by 2028. The Middle-East and Africa combined account for a smaller share, driven by GCC pharmaceutical ambitions and South African industrial lubricants, yet political risk and infrastructure gaps temper immediate growth. Collectively, regional dynamics underscore that the white oil market growth story rests on regulated purity upgrades rather than sheer volume expansion.

Value Chain Analysis

The white oil value chain starts with crude refining, where paraffinic and naphthenic base-oil fractions and slack wax streams are generated and then routed to specialty upgrading. Value creation is concentrated in severe purification steps, typically vacuum distillation and hydroprocessing (hydrocracking, catalytic or solvent dewaxing, and hydrofinishing), which reduce aromatics, sulfur, nitrogen, and PAH to meet pharmaceutical and food-contact specifications. Integrated refiners (ExxonMobil, Shell, Chevron, TotalEnergies, Sinopec, PetroChina) benefit from captive feedstock and the ability to shift streams between fuels and specialties, while niche specialists and regional refiners or blenders (H&R Group, Sonneborn, Calumet, Savita, Apar, Gandhar) rely on higher-purity cuts, tighter viscosity control, and documentation packages.

Downstream, certified product moves in bulk, ISO tanks, drums, and IBCs to distributors and toll blenders, then into end-user formulations for pharma excipients, personal care, food-contact packaging and processing aids, adhesives, and polymer processing. Qualification and compliance act as structural checkpoints, including US FDA food-grade provisions (21 CFR 172.878 and 21 CFR 178.3620(a)), USP/NF excipient expectations for pharma, and national standards such as China GB 4853-2008. Bottlenecks typically show up in testing and certification throughput (MOAH/MOSH screening, pharmacopeial assays, traceability), which favors suppliers with in-house analytical capability and longer-term contracts, while non-integrated blenders face margin pressure when feedstock economics tighten.

Competitive Landscape

Integrated refiners control about 45-50% of global capacity, supplying hydrocracked Group II streams at cost positions smaller blenders cannot match. ExxonMobil, Shell, Chevron, TotalEnergies, Sinopec, and PetroChina toggle output between low-sulfur fuels and specialty base oils, tightening or loosening supply as margins dictate. When marine-fuel margins widened after IMO 2020, specialty allocations shrank, driving an 8% price spike that advantaged players with captive feedstock.

Niche suppliers such as H&R Group, Nynas, Sonneborn, and Sasol compete on pharmaceutical certifications, custom viscosity cuts, and technical support. H&R’s 2025 hydrogenation upgrade in Hamburg added 25,000 tons of pharmaceutical capacity, enabling rapid responses to biologics contract bids. Indian producers—Savita, Gandhar, Apar—leverage cost advantages and ISO certification to penetrate price-sensitive Asia-Pacific and Gulf uses, though they struggle in FDA-regulated channels.

Technology is emerging as the next battleground. Suppliers investing in inline viscosity analytics, blockchain traceability, and real-time MOAH screening can charge premiums in food and pharma tenders. Conversely, regional blenders lacking hydrocracking assets and analytical labs confront margin compression as Group I demand wanes. Three Southeast Asian producers exited in 2025 as feedstock economics turned unfavorable. The white oil market therefore balances scale economics of integrated majors with specialization advantages of certified niche operators.

White Oil Industry Leaders

Exxon Mobil Corporation

Shell plc

China Petroleum & Chemical Corporation

Chevron Corporation

Sasol

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities cluster around compliance-led substitution and regionalization of supply for high-purity and food-contact grades. In Europe, packaging converters adopting certified hydrogenated white oils to address MOAH/MOSH concerns and to meet buyers' FDA-aligned food-contact requirements (21 CFR 172.878) create room for suppliers that can deliver consistent low-aromatic cuts with third-party testing and rapid lot release. Asia-Pacific remains the key volume center (63.44% share in 2025), and documented demand pull from biologics fill-finish lines in China and India lifts the value of USP-grade, low-viscosity oils supported by validated documentation and tight viscosity tolerances.

Recent capacity and integration actions point to practical whitespace for scale and quality upgrades. Chevron Lummus Global commissioned a major white-oil hydroprocessing unit for Hongrun Petrochemical in Shandong (including 200,000 t/y food-grade white oil), reinforcing the shift toward world-scale, hydroprocessed supply in China. In agriculture-adjacent uses, the European Commission issued Implementing Regulation (EU) 2026/870 renewing approval for paraffin oil (CAS 8042-47-5) in plant protection products from July 1, 2026, supporting continuity for regulated paraffin-oil applications that overlap with high-purity mineral-oil supply chains. On the supplier side, Indian specialty players are increasing focus on higher-margin consumer and healthcare end uses (e.g., PHPO portfolios), which can support partnership space for regional distribution, pharmacopoeial documentation services, and co-development of grades designed for local cosmetic and pharma formulations.

Recent Industry Developments

- April 2026: The European Commission issued Implementing Regulation (EU) 2026/870 renewing approval for paraffin oil (CAS 8042-47-5) for use in plant protection products, with application from July 1, 2026. The action sustains regulatory continuity for paraffinic mineral-oil uses and reinforces the importance of traceable, specification-controlled supply into regulated end markets.

- July 2025: Shell plc completed the acquisition of 100% equity in Raj Petro Specialities Private Limited (formerly owned by Brenntag Group), expanding Shell's lubricants footprint in India. The deal added manufacturing sites in Chennai and Silvassa and brought Raj Petro branded white oils into Shell's portfolio, strengthening local conversion capacity and distribution reach in a high-growth consumption hub.

- January 2024: Chevron Lummus Global commissioned a major white oil hydroprocessing unit for Hongrun Petrochemical in Weifang, China, including a 200,000 tonnes/year food-grade white oil line alongside a larger Group III base oil unit. The commissioning increased availability of hydroprocessed, food-grade supply in Asia and raised the competitive bar for producers reliant on legacy streams without comparable purification capability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the white oil market covers highly refined mineral oils sold as colorless, odorless base fluids for regulated and industrial uses, and sized at the point of primary sale across major producing and consuming regions.

Scope exclusions: It does not count synthetic substitutes (such as silicone fluids) or finished retail blends where white oil is only one ingredient.

Segmentation Overview

- By Grade

- Pharmaceutical

- Technical/Industrial

- By Base-Oil

- Group II

- Group I

- Group III

- Naphthenic

- By Viscosity

- Low

- Medium

- High

- By Application

- Personal Care

- Plastics and Elastomers

- Adhesives

- Pharmaceuticals

- Food and Beverage

- Agriculture

- Textile

- Metalworking Applications

- Other Applications (Household Products)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping supply, trade flows, and end use signals that are visible in public records, because white oil is closely linked to base oil refining and downstream compliance. We referenced sources such as USGS mineral and energy statistics, U.S. International Trade Commission trade data, UN Comtrade, Eurostat industrial output series, and regulator-facing pharmacopeia notes that clarify purity and allowable applications.

To connect the supply side to demand, we also reviewed company annual reports, investor decks, and plant announcements that indicate capacity changes, base oil slate shifts, and product positioning by grade. When needed, a paid subscription for company financials and a shipment-level import and export database were used to cross-check producer footprints and major trade lanes. The desk sources listed here are illustrative, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to validate what gets counted as white oil in real transactions, and to pressure-test the conversion between volume movement and pricing by grade. We spoke with a mix of refiners, distributors, and large end users in personal care, pharma-related processing, plastics, and industrial applications, covering APAC, EMEA, and the Americas so regional pricing and specification practices could be compared.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 38% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 20% | Managers: 48% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where refining output signals, base oil supply mix, and trade statistics were used to reconstruct the realistic pool of white oil volumes by region, before being adjusted for specification-driven usable yield. To keep the totals practical, we then corroborated them using selective bottom-up approximations such as sampled producer and distributor volume checks, channel conversations, and a simple ASP times volume sanity check for key grades.

Key inputs that shaped the model included base oil capacity additions and outages, typical viscosity splits used in downstream formulations, the share of pharmaceutical versus technical grades in each region, import dependence indicators, and observed price spreads between high-purity and industrial grades. Forecasting relied on scenario analysis supported by expert views on capacity utilization, downstream consumption trends in personal care and plastics, and expected normalization of feedstock costs. Where bottom-up visibility was limited, gaps were handled by using regional consumption proxies and then re-tested against trade balances and interview feedback until the numbers aligned.

Data Validation & Update Cycle

Outputs were checked in several steps so obvious overstatements and regional mismatches could be caught early. We compared modeled volumes with independent signals such as net trade direction, reported refinery operating rates, and downstream activity indicators, and then flagged variances for a second analyst review.

If an assumption moved results meaningfully, respondents were re-contacted to confirm whether it was a one-off event or a structural change. Reports are refreshed each year, and interim updates are made when material events occur, such as major capacity changes or policy shifts. Before publication, a final pass is completed so clients receive an updated view that reflects the latest available data.

Mordor Intelligence's White Oil Market Size Compared Against Other Published Estimates

Published market sizes for white oil often diverge because the unit of measurement is not consistent, and because firms can widen or narrow the product boundary depending on whether they treat white oil as a base fluid category or as a finished product space.

The table shows a clear spread because some sources report revenue while our report sizes the market in volume, and because the conversion from tons to USD depends heavily on grade mix, regional pricing, and the timing of currency assumptions. The table also points to another driver: in Mordor Intelligence's model, only primary sales of white oil are counted and finished consumer blends are not added on top, which usually lifts revenue-based totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.56 M (2025) | |

| Global Consultancy A | USD 2.25 B (2025) | Uses a revenue lens, which can fold in wider price assumptions by grade and region, and may also include packaged or formulated products where white oil is an input rather than the traded base fluid. |

| Industry Publisher B | USD 2.20 B (2024) | Uses a different base year and a USD sizing approach, which is sensitive to currency timing and inflation assumptions, and it is not always clear how pharmaceutical-grade purity boundaries are handled. |

When the unit, scope boundary, and price logic are aligned, the gap typically narrows quickly, and the remaining difference comes from how each model treats grade mix and regional trade flows. By keeping the calculation traceable to observable volumes and then stress-testing the implied pricing through interviews, the estimate stays repeatable and easier to reconcile with real movement in the market.

Key Questions Answered in the Report

How large is the white oil market?

The white oil market size is 1.58 million tons in 2026 and is forecast to reach 1.69 million tons by 2031 with a projected 1.36% CAGR to 2031.

Which application is expanding fastest?

Personal care leads growth at a 2.11% forecast CAGR as Ayurvedic and halal brands step up purchases of light-paraffinic grades.

Why are Group II base oils gaining share?

Hydrocracking removes sulfur and aromatics to meet stricter European and North American purity limits, pushing Group II to 67.12% share in 2025.

Which region dominate demand?

Asia-Pacific accounts for 63.44% of global volume in 2025, driven by pharmaceutical and plastics manufacturing clusters.

Page last updated on: