Transformer Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

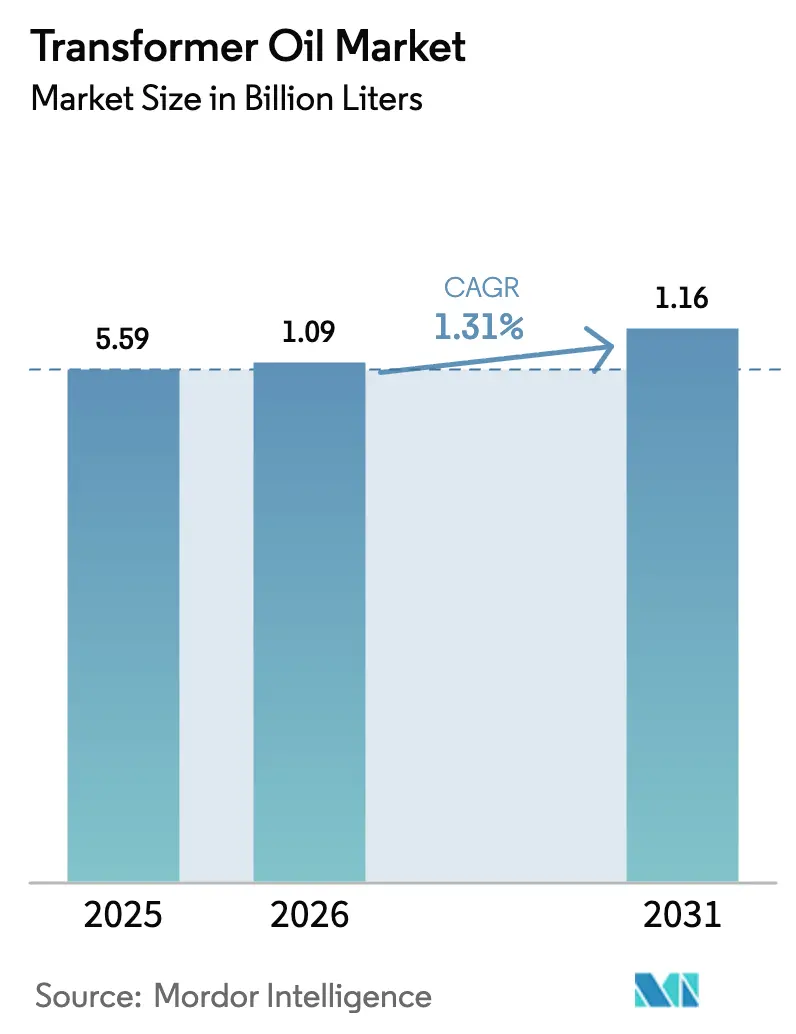

| Market Volume (2026) | 1.09 Billion liters |

| Market Volume (2031) | 1.16 Billion liters |

| Growth Rate (2026 - 2031) | 1.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transformer Oil Market Analysis by Mordor Intelligence

The Transformer Oil Market size is expected to grow from 5.59 Billion liters in 2025 to 1.09 Billion liters in 2026 and is forecast to reach 1.16 Billion liters by 2031 at 1.31% CAGR over 2026-2031. Grid-reinforcement programs in Asia–Pacific, mandated replacement of aging units in the United States and Europe, and the rise of offshore-wind converter platforms are sustaining steady, volume-driven growth. Mineral-based formulations still dominate global demand, yet their cost advantage is narrowing as Group-I base-oil supplies tighten and disposal liabilities escalate. Bio-based esters, supported by fire-safety codes and biodegradability rules, are gaining traction in urban substations, data centers, and environmentally sensitive zones. Competitive dynamics hinge on supply-chain resilience, portfolio breadth, and the ability to offer lifecycle-cost models rather than commodity pricing.

Key Report Takeaways

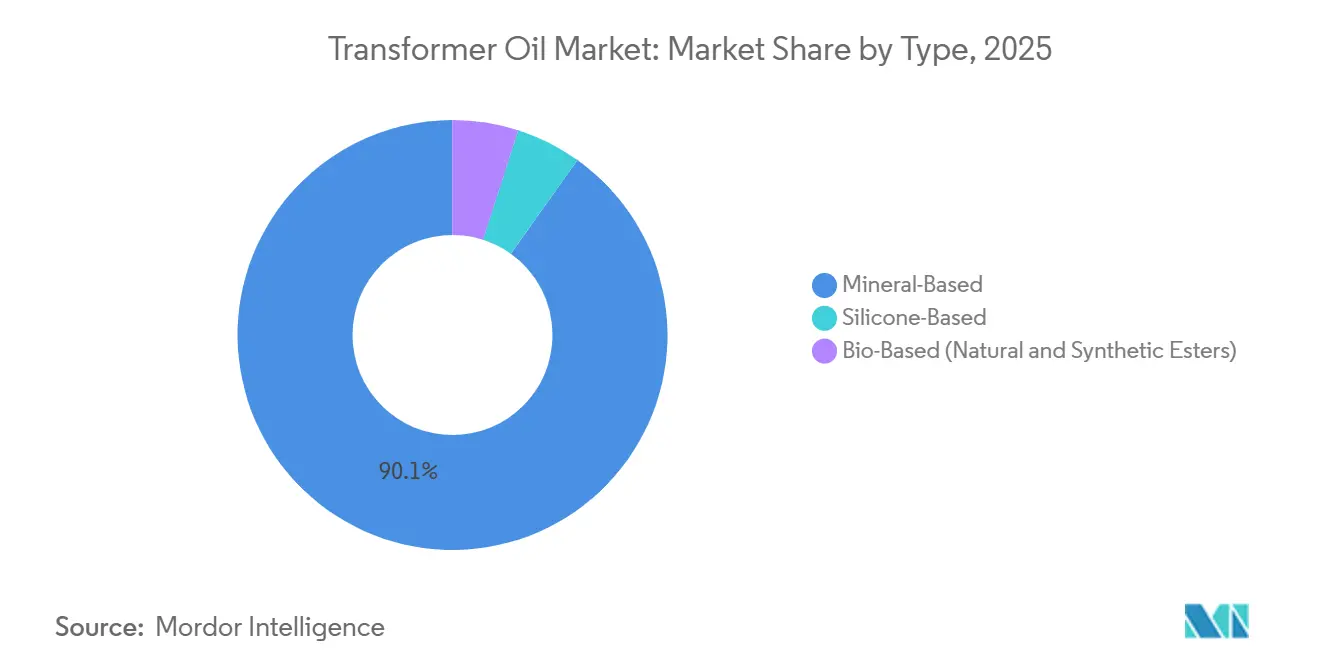

- By type, mineral-based held the largest share of 90.12% in 2025, whereas bio-based esters are expected to grow at a CAGR of 7.92% during the forecast period (2026-2031).

- By application, transformers held the largest market share of 73.83% in 2025 and are expected to grow at a CAGR of 1.86% during the forecast period (2026-2031).

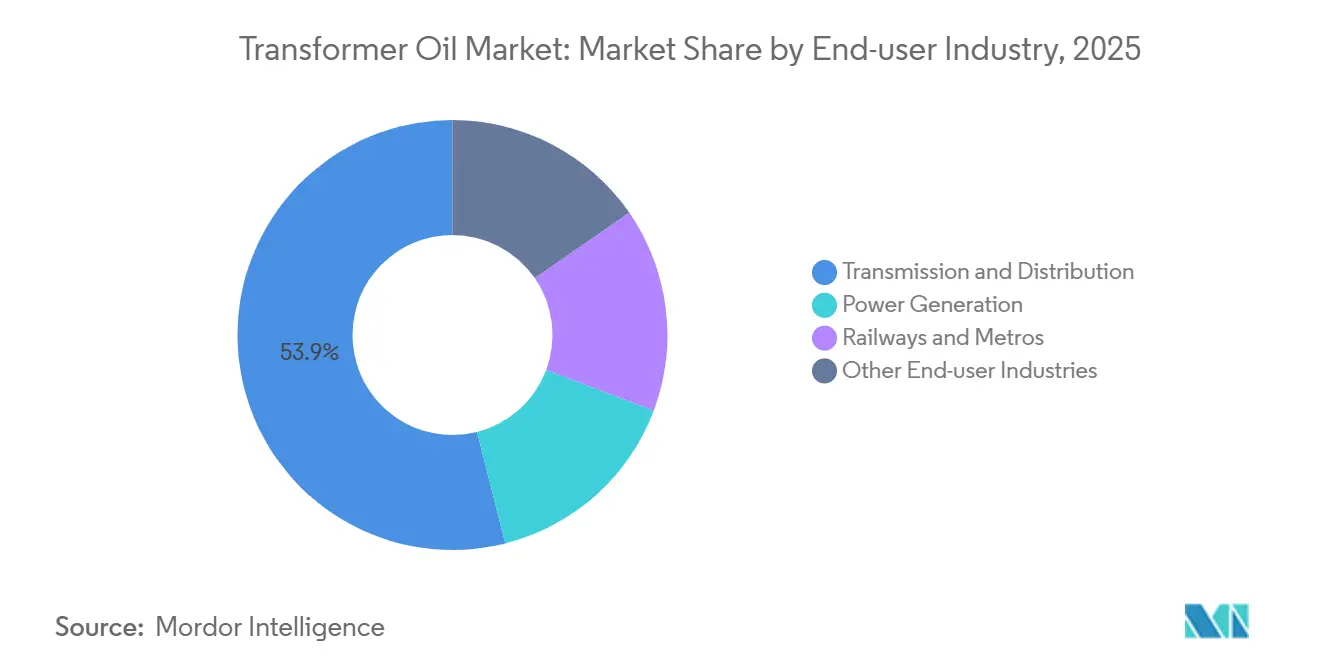

- By end-user industry, transmission and distribution held the market share of 53.94% in 2025 and are expected to grow at a CAGR of 1.75% during the forecast period (2026-2031).

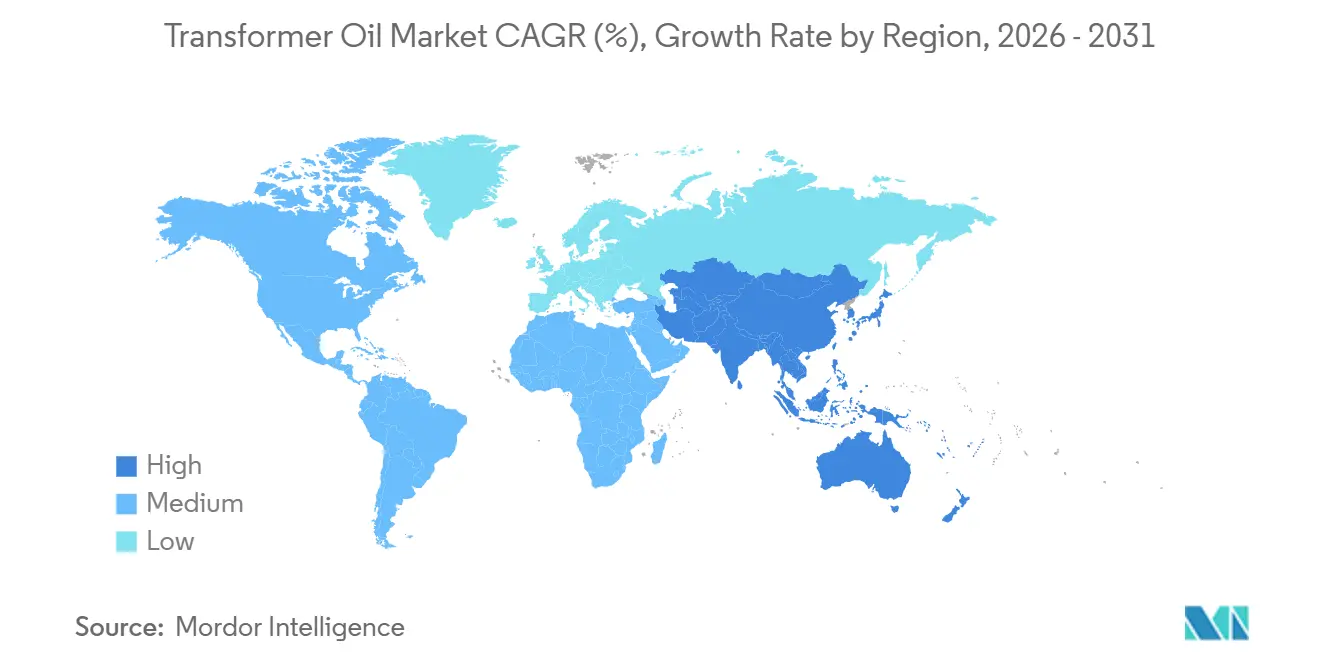

- By geography, the Asia-Pacific region had the largest share of 47.77% in 2025, and this share is expected to grow at the fastest CAGR of 1.82% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Transformer Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing electric grids in Asia-Pacific | +0.6% | Asia-Pacific core, spillover to Middle East & Africa | Medium term (2-4 years) |

| Upgradation of aging transformers in OECD markets | +0.4% | North America & Europe | Long term (≥4 years) |

| DOE-mandated efficiency standards for distribution transformers | +0.3% | United States, with influence on Canada and Mexico | Short term (≤2 years) |

| Offshore-wind converter platforms demanding high-flash-point oils | +0.2% | Europe (North Sea), United States (East Coast), Asia (Taiwan Strait) | Medium term (2-4 years) |

| Utility-scale battery storage build-out | +0.2% | Global, with early concentration in California, Texas, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Electric Grids in Asia-Pacific

Asia-Pacific utilities are building redundancy into networks, driving step-change transformer oil demand. China’s State Grid invested USD 89 billion in 2025 to extend ultra-high-voltage corridors, and each 1,000 kV unit requires 10,000 to 20,000 liters of oil[1]State Grid Corporation of China, “Annual Investment Plan 2025,” sgcc.com.cn. India has earmarked Rs 9.16 trillion (USD 109 billion) for 1,274 GVA of new transformation capacity by 2032. ASEAN projects will add up to 13,780 MW of cross-border links that rely on synthetic-ester or silicone fluids resilient to tropical humidity. Investment is driven less by electrification and more by network reliability, creating a stable base for the transformer oil market.

Upgradation of Aging Transformers in OECD Markets

North American and European utilities are confronting end-of-life fleets installed during the 1970s-1980s. US lead times have lengthened to 24 months for replacement units, partly due to shortages of electrical steel. Europe anticipates 34,000 tonnes of annual oil demand by 2030 as 400/100 kV substations are modernized to integrate offshore wind. Australia is retrofitting rural assets with fire-resistant esters at insurers’ insistence. Replacement schedules remain uneven; Japan and South Korea are delaying upgrades for budgetary reasons, preserving long-tail mineral demand.

DOE-Mandated Efficiency Standards for Distribution Transformers

The 2024 U.S. rule obliges manufacturers to adopt amorphous-metal cores that increase oil volume per unit by up to 15%. Compliance costs of USD 300 to 500 per transformer weigh most on small cooperatives. Canada and Mexico are aligning designs to avoid cross-border supply-chain friction. OEMs and oil producers are co-engineering antioxidant packages capable of withstanding higher core temperatures without sludge formation. Near-term US procurement is, therefore, a demand accelerator for the transformer oil market.

Offshore-Wind Converter Platforms Demanding High-Flash-Point Oils

Europe’s offshore wind fleet reached 30 GW in 2025, each gigawatt requiring up to 300 tonnes of oil across converter stations[2]WindEurope, “Offshore Wind Statistics 2025,” windeurope.org. US Atlantic leases total 8 GW with first projects due in 2027. Synthetic esters dominate because they meet K-class fire ratings and marine environmental standards. Taiwan aims for 15 GW by 2035, spurring local blending of high-flash-point fluids. Suppliers able to certify formulations to IEC 61039 gain premium pricing and long-term contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Group-I base-oil supply after European refinery closures | -0.2% | Europe, with spillover to North America and Asia-Pacific | Short term (≤2 years) |

| Mineral-oil environmental liabilities and disposal costs | -0.1% | North America & Europe, with emerging pressure in Asia-Pacific | Long term (≥4 years) |

| Ester-fluid price premium in cost-sensitive Asia-Pacific utilities | -0.1% | Asia-Pacific, particularly India, Indonesia, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight Group-I Base-Oil Supply After European Refinery Closures

European shutdowns have removed 2 million tonnes of Group-I capacity since 2024, forcing blenders to import higher-priced feedstock. Freight premiums of 15-20% and six-month delivery lags undermine pricing visibility. North American formulators are migrating to Group-II base oils, necessitating reformulation to match dielectric performance. Asian suppliers in South Korea and Singapore are scaling exports, but their logistics chains add cost and quality variability. Supply tightness, therefore, subtracts about 0.2 percentage points from the transformer oil market CAGR.

Mineral-Oil Environmental Liabilities and Disposal Costs

The U.S. EPA classifies oil containing >50 ppm PCBs as hazardous, raising disposal costs to USD 1,500-3,000 per tonne. European insurers are lifting premiums for mineral-filled urban substations. Utilities, internalizing these liabilities, now apply lifecycle cost models that favor biodegradable esters despite a 20-30% price premium. China and India are drafting soil-contamination rules that mirror Western standards, signaling wider adoption of bio-based fluids. Long-term compliance pressure erodes mineral-oil demand in mature grids and shapes future transformer oil market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bio-Based Esters Gain Ground on Fire Safety

Mineral-based products accounted for 90.12% of the 2025 volume, reflecting entrenched procurement habits and lower unit cost. Bio-based esters are advancing at a 7.92% CAGR to 2031, anchored in K-class fire-safety performance and rapid biodegradability. Natural esters find favor in data centers and hospitals where fire risks and environmental liabilities are highest. Synthetic esters, engineered from polyol bases, outperform under high thermal cycling, making them the preferred choice for offshore wind platforms and rail traction transformers. The transformer oil market size for bio-based esters is therefore expanding faster than the legacy mineral segment.

Europe specifies natural esters in roughly one-third of new installations, spurred by insurer incentives and carbon-disclosure mandates. North American adoption remains at 15-20% as utilities validate long-term performance. Asia–Pacific remains price-driven, yet China’s draft law requiring biodegradable fluids near water bodies could shift 10-15% of its installed base to esters by 2030. Silicone oils occupy a niche for temperatures above 200°C, notable in furnace transformers, but face cost hurdles. Collectively, these trends reshape the product mix within the transformer oil market.

By Application: Transformers Dominate Amid Grid Modernization

Transformers consumed 73.83% of global volume in 2025 and are forecast to expand at a 1.86% CAGR, supported by US efficiency rules and Asia’s ultra-high-voltage projects. Distribution units, operating at 11-33 kV, anchor replacement demand in OECD grids. Power transformers above 132 kV drive greenfield volumes in China and India, where single units can require up to 20,000 liters of fluid. The transformer oil market size for these high-rating assets is therefore rising in tandem with renewable integration targets.

Switchgear accounts for 12-15% of demand, growing with substation automation. Circuit breakers and capacitors together make up under 10%, but an increasing share shifts to synthetic esters for extended service life. Niche uses, including reactors and voltage regulators, round out the balance. Every kilowatt of electricity passes through at least one transformer, making this application an enduring pillar of the transformer oil market.

By End-User Industry: Transmission and Distribution Lead Investment

Transmission and distribution utilities absorbed 53.94% of 2025 volume and are projected to grow at a 5.75% CAGR through 2031 on the back of multi-billion-dollar grid programs in China, India, and the United States. Power generation sites are led by coal retrofits in India and renewable-plant step-ups worldwide. Railways and metros are also growing as electrified corridors expand across Asia and Europe. The transformer oil market size linked to rail projects rises in line with rolling-stock electrification.

Other industrial end-users, including mining and data centers, account for the residual share, with project-specific specifications dictating fluid choice. The strategic importance of uninterrupted supply in transmission grids ensures that transformer oil procurement remains a non-discretionary expense, buffering the market from short-term economic cycles.

Geography Analysis

Asia–Pacific held 47.77% of global volume in 2025 and is expected to grow at 1.82% annually to 2031. China’s USD 89 billion grid program and India’s USD 109 billion transmission plan underpin the region’s leadership. ASEAN interconnection projects call for high-performance esters able to operate in humid, salt-spray environments. Mature markets such as Japan and South Korea generate steady replacement demand for higher-efficiency units.

North America contributed just over some of the 2025 volume. US DOE rules, offshore-wind investments, and 12 GW of new battery storage underpin growth. Canada’s export-oriented transmission upgrades and Mexico’s substation modernizations add incremental demand.

Europe’s market share is driven by 30 GW of offshore wind and urban-substation retrofits that specify fire-resistant fluids. Replacement of 400/100 kV transformers adds 34,000 tonnes of annual oil demand by 2030.

South America and the Middle East & Africa together represent a significantly lower market share. Brazil is extending transmission lines into the Amazon to integrate hydro assets, while Saudi Arabia’s Vision 2030 allocates USD 50 billion for grid upgrades. South Africa and Nigeria focus on urban reliability and rural electrification respectively, favoring lower-cost mineral oils but gradually trialing esters in donor-funded projects.

Competitive Landscape

The transformer oil market is moderately consolidated. The balance is fragmented among small blenders serving niche or geographically isolated markets. Innovation centers on bio-based formulations; Cargill’s FR3 natural ester now competes head-to-head on cost in select markets after securing K-class approvals. Strategic moves include TotalEnergies partnering with Siemens Energy on synthetic esters for offshore converters and ExxonMobil launching Mobil Transformer Oil 500E for rail traction.

Transformer Oil Industry Leaders

Shell plc

NYNAS AB

China Petrochemical Corporation

CNPC

Ergon, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: KONČAR's 630 kVA distribution transformer in Zagreb was filled with NYTRO BIO 300X, a bio-based transformer fluid from NYNAS AB. This marks the inaugural use of the fully renewable insulating liquid. The milestone was achieved through a successful collaboration among Nynas, KONČAR - D&ST, and HEP ODS, the national Distribution System Operator of Croatia.

- May 2025: Hitachi Energy successfully tested a pioneering 765 kilovolt (kV) / 400 kV single-phase transformer. With a capacity of 250 megavolt-amperes (MVA), this transformer stands as the world's first at its voltage and power level. The use of natural ester oil underscores its innovative edge.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the transformer oil market as the total annual demand for liquid insulating and cooling media, principally mineral, silicone, and natural-ester oils, used in oil-filled power, distribution, and specialty transformers, as well as related switchgear and capacitors. Consumption is expressed in million liters and, where needed, converted to value using region-specific average selling prices.

Scope exclusion: dry-type transformers that rely on solid or air insulation are outside the sizing framework.

Segmentation Overview

- By Type

- Mineral-Based

- Silicone-Based

- Bio-Based (Natural and Synthetic Esters)

- By Application

- Transformer

- Switchgear

- Circuit Breakers

- Capacitors

- Other Applications (reactor, etc.)

- By End-User Industry

- Power Generation

- Transmission and Distribution

- Railways and Metros

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic Countries

- Russia

- Turkey

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Nigeria

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed transformer OEM engineers, utility maintenance managers across Asia-Pacific, Europe, and the Americas, and specialty-oil formulators. These conversations validated load factors, replacement cycles, and emerging ester uptake, filling gaps that public data leave and letting us refine preliminary assumptions.

Desk Research

We began by compiling public-domain datasets that describe the installed transformer base and grid build-outs, such as the International Energy Agency's electricity statistics, UN Comtrade trade flows for HS 2710 and 2909 codes, and T&D investment briefs from bodies such as ENTSO-E and the Central Electricity Authority of India. These were complemented by transformer failure and refurbishment rates reported in CIGRE working groups, patent filings on ester formulations accessed via Questel, and financial disclosures from listed oil refiners. Company 10-Ks, investor decks, and respected business press rounded out early demand signals.

Subscription resources, including D&B Hoovers for manufacturer revenues and Dow Jones Factiva for tender awards, supplied granular clues on shipment mix and pricing movements. The sources cited here illustrate, rather than exhaust, the reference library that Mordor analysts reviewed.

Market-Sizing & Forecasting

A top-down build traces national transformer fleets, new substation additions, and average oil fill per kVA to reconstruct liters consumed, which are then cross-checked through selective bottom-up supplier shipment roll-ups and channel price audits. Key variables fed into the model include: (1) kilometers of new high-voltage lines commissioned, (2) average MVA rating of newly installed transformers, (3) oil fill per MVA, (4) refurbishment rate of units beyond 25 years, and (5) bio-based oil penetration. Multivariate regression on these drivers, supported by primary-expert consensus, produces the 2025-2030 outlook and scenario bands. Where supplier data are patchy, interpolations are flagged and revisited once fresh evidence surfaces.

Data Validation & Update Cycle

Before sign-off, outputs are reviewed for variance against historical oil import statistics and utility capex trends; anomalies trigger re-interviews or recalibration. Reports refresh annually, with interim revisions when material events, such as a crude-price shock, shift underlying assumptions.

Why Mordor's Transformer Oil Baseline Is Widely Trusted

Published estimates often diverge because firms choose different unit bases, pricing sets, and refresh cadences.

Key gap drivers include whether volumes or revenues anchor the model, the transparency of ASP conversion, and the frequency with which grid-expansion statistics are rolled into forecasts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 5.59 billion liters (2025) | Mordor Intelligence | |

| USD 3.03 billion (2024) | Global Consultancy A | Relies on historical refinery sales without adjusting for rising ester share |

| USD 2.00 billion (2023) | Industry Association B | Uses constant 2019 ASPs, excludes aftermarket oil replacements |

| USD 3.15 billion (2023) | Regional Consultancy C | Forecasts stop at grid orders, omitting in-service top-up demand |

In sum, by grounding volumes first, layering verifiable price series, and updating the model each year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeat with confidence.

Key Questions Answered in the Report

How large is the transformer oil market in 2026?

The transformer oil market size reached 1.09 billion liters in 2026 and is set to grow at a 1.31% CAGR to 2031.

Which product type is growing the fastest?

Bio-based esters are growing at a 7.92% CAGR, driven by fire-safety and biodegradability mandates.

Why are utilities shifting toward ester-based fluids?

Utilities face rising environmental liabilities and insurance premiums on mineral oils, making esters more attractive over the lifecycle despite higher upfront cost.

Which region contributes the most volume?

Asia–Pacific accounts for 47.77% of global volume in 2025, propelled by large-scale grid investments in China, India, and ASEAN countries.

How will U.S. efficiency rules affect demand?

The 2024 DOE standards increase oil volume per distribution transformer by up to 15%, boosting near-term demand in North America.

Page last updated on: