Workwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

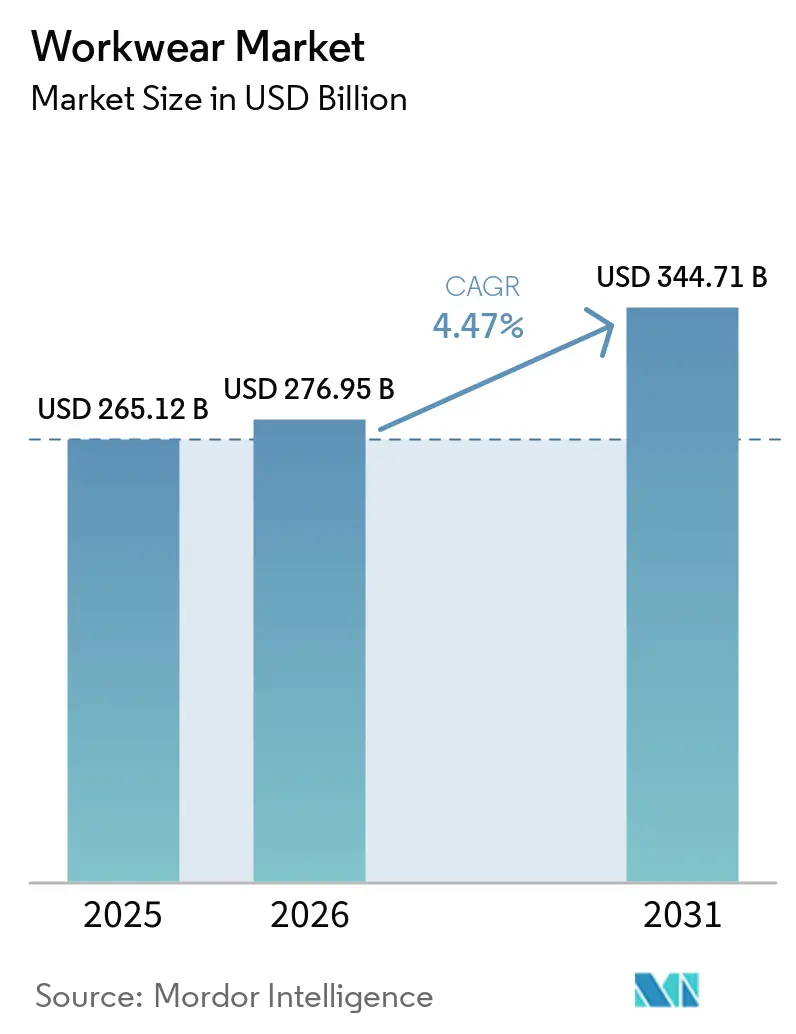

| Market Size (2026) | USD 276.95 Billion |

| Market Size (2031) | USD 344.71 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Workwear Market Analysis by Mordor Intelligence

The workwear market size was valued at USD 265.12 billion in 2025 and estimated to grow from USD 276.95 billion in 2026 to reach USD 344.71 billion by 2031, at a CAGR of 4.5% during the forecast period (2026-2031). Corporate hiring remains the main support for the workwear market because new hiring and replacement cycles both lift purchases of office apparel, footwear, and related accessories. ManpowerGroup reported a Global Net Employment Outlook of 31% in Q2 2026 across 42 countries, with 45% of employers planning staff increases, which supports demand for professional clothing in both developed and emerging economies. Formalwear demand is also being supported by stronger workplace expectations in finance, law, hospitality, and other client-facing fields, even as more casual dress codes continue to spread in technology and creative roles. Product quality, comfort features, and premium positioning are raising spending per unit, while rising female workforce participation is widening the addressable base for the workwear market in Asia and other fast-growing regions. Competition remains mixed between global apparel groups and regional specialists, with larger brands leaning on direct channels, portfolio upgrades, and selective acquisitions to protect margins and broaden reach in the workwear market

Key Report Takeaways

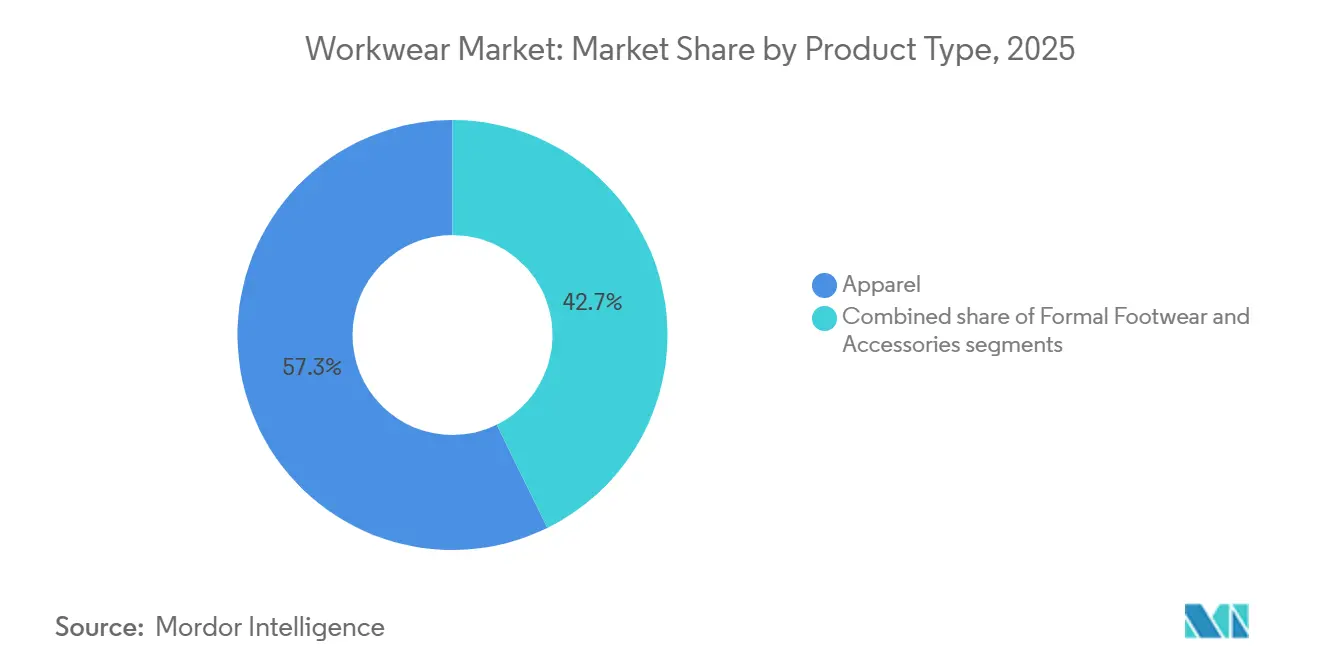

- By product type, Apparel accounted for 57.28% of the workwear market size in 2025, while Formal Footwear is projected to expand at a 5.89% CAGR through 2031.

- By category, the Mass segment held 67.17% share in 2025, while the Premium segment is forecast to grow at a 6.12% CAGR through 2031.

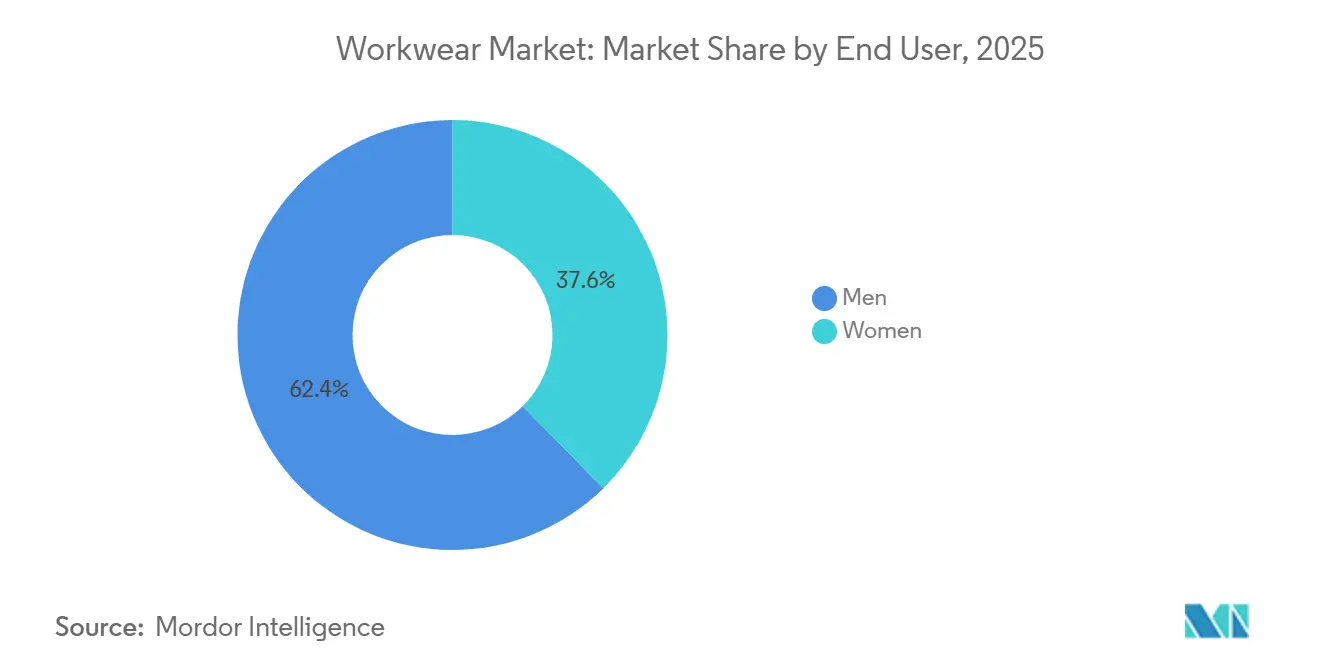

- By end user, Men held 60.31% of the workwear market in 2025, while Women recorded the highest projected CAGR at 5.76% through 2031.

- By distribution channel, Offline Stores represented 62.38% of the workwear market share in 2025, while Online Stores are expected to grow at a 6.34% CAGR through 2031.

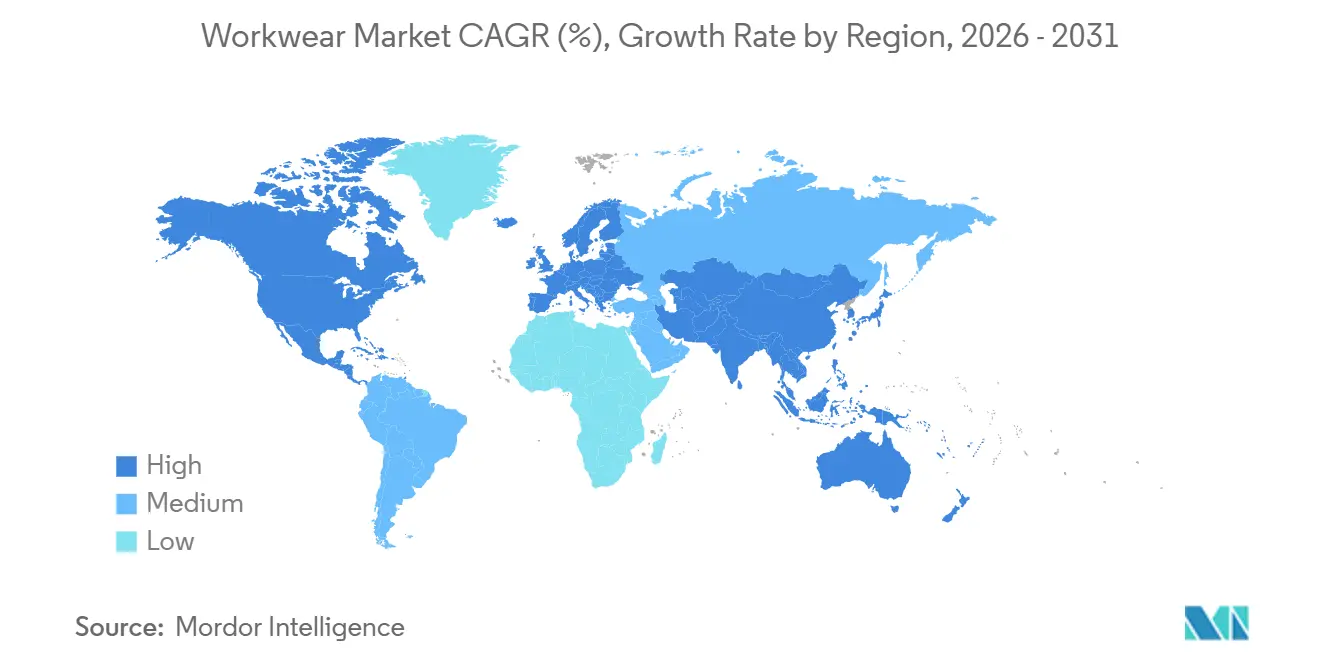

- By geography, Asia-Pacific held 35.41% of the workwear market share in 2025 and is also the fastest-growing region with a 5.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in corporate employment worldwide | +1.2% | Global, concentrated in Asia-Pacific (India, Vietnam, Australia) and United States | Short term (≤ 2 years) |

| Increasing emphasis on professional workplace appearance | +0.7% | Global, strongest in financial and legal sectors across North America and Europe, Middle East and Africa | Medium term (2–4 years) |

| Rising demand for premium and tailored office apparel | +0.5% | North America, Europe, Japan, China high-income urban professional corridors | Medium term (2–4 years) |

| Growth of women's participation in corporate workforce | +0.6% | Asia-Pacific core (India, Southeast Asia), spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Product innovation in comfort, stretch, and wrinkle-resistant fabrics | +0.3% | Global, early adoption in North America and Northern Europe | Medium term (2–4 years) |

| Corporate dress codes and uniform policies | +0.2% | Global, strongest in finance, hospitality, and regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in corporate employment worldwide

Growth in corporate employment worldwide is a key driver of the corporate workwear market, as expanding office-based workforces directly increase demand for professional apparel. Rising recruitment across industries generates both first-time purchases by new employees and recurring replacement demand from existing professionals, supporting steady sales of office shirts, tailored trousers, blazers, formal footwear, and business-casual attire. According to ManpowerGroup, the global net employment outlook reached 26% in Q3 2026 across more than 40,500 employers in 42 countries, indicating sustained hiring momentum in the corporate sector[1]Source: Manpower Group, "ManpowerGroup Employment Outlook Survey Q3 2026", manpowergroup.com. India recorded the strongest hiring confidence in the Asia-Pacific region with a net employment outlook of 48%, reinforcing the region’s position as a major growth engine for the corporate workwear market. As white-collar payrolls continue to expand, organizations and employees are investing more in workplace-appropriate clothing, driving demand across both premium and mass-market workwear segments. This trend is expected to support long-term market growth, particularly in emerging economies experiencing rapid corporate sector development.

Increasing emphasis on professional workplace appearance

The increasing emphasis on professional workplace appearance is a significant driver of the workwear market, as organizations continue to recognize the role of employee presentation in strengthening brand image, customer trust, and corporate identity. Many businesses maintain formal or business-casual dress standards to promote professionalism and consistency across their workforce, particularly in client-facing roles. As competition intensifies across industries, employers are investing in high-quality workwear that reflects organizational values while enhancing employee confidence and workplace etiquette. The growing prevalence of corporate events, in-person meetings, and customer interactions has further reinforced the need for polished and professional attire. In addition, employees increasingly view well-designed workwear as an important element of career development and personal branding.

Rising demand for premium and tailored office apparel

The rising demand for premium and tailored office apparel is a key driver of growth in the workwear market, as professionals increasingly prioritize quality, comfort, fit, and versatility in their workplace clothing. This premiumization trend is enabling brands to increase average selling prices and revenue even in markets where unit sales growth remains moderate. Consumers are showing greater willingness to invest in garments made from superior fabrics, customized fits, and durable designs that can transition seamlessly between formal office settings and business-casual environments. The trend is reflected in the performance of leading premium apparel companies; for instance, the Ermenegildo Zegna Group reported net profit of EUR 109.5 million in 2025, up 20% year-over-year, while direct-to-consumer revenue reached EUR 1.45 billion, increasing by 4.2%. Similarly, Hugo Boss has continued to strengthen its formalwear positioning through its long-term growth strategy, demonstrating sustained confidence in the premium office apparel segment[2]Source: Hugo Boss, "Annual Report-2025", hugoboss.com. As a result, corporate workwear brands that successfully balance quality, contemporary styling, and affordability are well positioned to capture growing demand and drive higher market value growth.

Growth of women’s participation in corporate workforce

The workwear market is benefiting from the increasing participation of women in the formal workforce, particularly across rapidly developing economies in Asia. As more women enter professional and office-based roles, demand for women’s business attire, tailored separates, formal dresses, blazers, and professional footwear continues to expand. According to Invest India, the female labor force participation rate in India increased significantly from 23.3% in 2017–18 to 41.7% in 2023–24, reflecting a substantial growth in the number of working women and, consequently, the potential customer base for corporate apparel. Additionally, women accounted for 55.5% of textile purchases in 2024, highlighting their growing influence on apparel spending and fashion consumption trends[3]Source: Invest India, "10 facts about India’s labour market every investor should know", investindia.gov.in. The combination of rising workforce participation and increasing purchasing power is creating a sustained demand stream for professional workwear. As a result, manufacturers and brands offering purpose-designed women’s corporate clothing with enhanced fit, comfort, functionality, and contemporary styling are well positioned to capitalize on this expanding market opportunity.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of casual and smart-casual workplace attire | -1.0% | Global, most pronounced in North America tech/startup hubs and Northern Europe | Short term (≤ 2 years) |

| Increasing popularity of athleisure and business-casual clothing | -0.7% | North America, Western Europe, Australia, Japan | Medium term (2–4 years) |

| Counterfeit and low-quality formal apparel products | -0.5% | Asia-Pacific, South America, Middle East and Africa; increasingly infiltrating North American online channels | Medium term (2–4 years) |

| Environmental concerns regarding textile manufacturing and waste | -0.3% | Europe (primary), North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of casual and smart-casual workplace attire

The growing adoption of casual and smart-casual workplace attire is emerging as a significant restraint for the workwear market. Across many industries, organizations are relaxing traditional dress codes in favor of more flexible and comfortable clothing styles that align with evolving workplace cultures and employee preferences. The expansion of hybrid work models and technology-driven workplaces has further accelerated the shift away from formal business attire, reducing the frequency of purchases for suits, blazers, dress shirts, and other conventional office wear. Employees are increasingly opting for versatile garments that can be worn across professional, social, and remote work settings, limiting demand for dedicated corporate apparel. In addition, younger professionals tend to prioritize comfort, functionality, and personal expression over strict adherence to formal dress standards.

Increasing popularity of athleisure and business-casual clothing

The growing preference for athleisure and business-casual apparel is limiting demand for traditional corporate workwear across many professional environments. Employees are increasingly seeking clothing that offers greater comfort, mobility, and versatility, resulting in a shift away from formal office attire toward more relaxed yet professional-looking garments. The widespread adoption of flexible and hybrid work models has reinforced this trend, as workers no longer require formal business clothing for daily office attendance. Business-casual outfits and athleisure-inspired designs are also valued for their ability to transition seamlessly between work, travel, and leisure activities, enhancing their appeal among modern professionals. In response, many organizations have relaxed workplace dress standards, reducing the necessity for suits, blazers, dress shirts, and other formal apparel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Anchors Revenue While Formal Footwear Accelerates

Apparel held a dominant 57.28% share in 2025, comprising shirts, trousers, blazers and jackets, skirts and dresses, and related categories. The breadth of this segment spanning entry-level business shirts through tailored executive suiting gives it structural resilience across economic cycles. Within apparel, blazers and structured separates benefit from the ongoing return-to-office transition, as professionals selectively invest in versatile layering pieces that meet corporate dress codes without the full commitment of a suit. Skirts and dresses have emerged as a particularly dynamic sub-segment, with women's formalwear designers reporting acceleration in structured midi skirts and tailored dresses as alternatives to traditional trouser suiting.

Formal Footwear is the fastest-growing product segment, with a 5.89% CAGR projected over 2026–2031. This rate meaningfully exceeds the overall market growth of 4.47%, reflecting both under-penetration in emerging markets and a post-pandemic normalization of shoe spend. Innovation in this sub-segment is accelerating: the shift toward ergonomically designed formal shoes that combine professional aesthetics with all-day comfort absorbing lessons from athleisure is widening the addressable consumer base to include workers previously deterred by traditional rigid dress shoes. DuPont's Sorona® Agile, a partially bio-based stretch fiber now being incorporated into formal footwear insoles and linings, illustrates how material science is dissolving the long-standing trade-off between comfort and professional appearance in this category

By Category: Mass Market Holds Scale While Premium Commands Margin

The mass category accounted for the largest share of the global workwear market, representing 67.17% of total revenue in 2025. The segment’s dominance is primarily attributed to its affordability and broad accessibility. Mass-market products are widely available through both offline and online distribution channels, further supporting their adoption. In addition, the growing demand for standardized uniforms and protective apparel in emerging economies has strengthened the segment’s market position. Manufacturers continue to focus on offering durable, comfortable, and regulation-compliant products at competitive prices, ensuring sustained demand for the mass category across global markets.

The premium category is projected to register the fastest growth in the workwear market, expanding at a CAGR of 6.12% through 2031. Growth in this segment is being supported by increasing consumer and employer preference for high-performance, ergonomic, and aesthetically appealing workwear solutions. Companies are increasingly investing in premium apparel that enhances employee comfort, productivity, and brand image, particularly in corporate sector. Technological advancements in fabrics, including moisture-wicking, stretchable, lightweight, and sustainable materials, are further accelerating demand for premium products.

By End User: Men Lead but Women Generate Disproportionate Growth

In 2025, men's workwear dominated the market with a 60.31% share, as companies leveraged the established infrastructure of formal menswear, including suit separates, dress shirts, ties, and formal footwear. This dominance stemmed from the historically higher male representation in professional employment globally, which consistently drove demand for such attire. Organizations in industries like finance, consulting, and law actively reinforced this growth by adhering to strict dress codes and fostering strong corporate account relationships. These relationships not only ensured consistent demand but also encouraged high repeat purchase rates, further strengthening the segment's position in the market.

Women are driving transformative growth in the corporate workwear market, with their segment projected to achieve the fastest CAGR of 5.76% during the forecast period of 2026 to 2031. This rapid expansion highlights the increasing focus on designing professional attire that caters specifically to the needs and preferences of women in corporate roles. Companies are prioritizing the development of diverse and inclusive workwear collections, offering a blend of functionality, comfort, and style to meet the expectations of modern working women. This trend underscores the evolving workplace culture and the growing recognition of women as a significant consumer base within the workwear market.

By Distribution Channel: Offline Retains Volume, Online Captures Growth

Offline stores held 62.38% of distribution in 2025, reflecting the enduring role of physical retail in workwear purchasing particularly for suiting and tailored garments where fit verification, alteration services, and premium presentation remain key purchase drivers. Large-format specialty retailers, department stores, and brand-owned boutiques continue to serve the professional buyer's need for tactile engagement with fabrics and silhouettes. Germany's mid-market apparel data reinforces the offline-online bifurcation: total clothing trade grew roughly 1% nominally in 2025, but internet and mail-order retail expanded 10.8% in real terms more than 10 times the growth rate of brick-and-mortar,

Online Stores are the fastest-growing distribution channel with a 6.34% CAGR over 2026–2031. Asia-Pacific is the primary accelerator: over 40% of fashion sales in the region already occur online, with Asia-Pacific apparel e-commerce projected to reach USD 315 billion by 2030, nearly tripling from present levels. Direct-to-consumer digital platforms particularly in the premium segment are generating higher margins by eliminating wholesale intermediaries; Ermenegildo Zegna's DTC revenues growing to EUR 1.45 billion in 2025 (+4.2%) while wholesale revenue softened demonstrates the structural channel shift underway at the top end. Platforms investing in authentication infrastructure and AI-powered fit guidance tools are reducing return rates while building the supplier relationships that underpin longer-term category loyalty.

Geography Analysis

Asia-Pacific accounted for 35.41% of workwear demand in 2025, making it the largest regional market. The region is also projected to register the fastest growth, expanding at a CAGR of 5.94% through 2031. Strong economic development, rapid urbanization, and the continued expansion of service-oriented industries are driving demand for professional workplace attire across major economies such as China, India, Japan, and Southeast Asian countries. The growth of multinational corporations, business process outsourcing centers, and financial services sectors has increased the adoption of formal workplace dress codes. In addition, rising disposable incomes and growing workforce participation, particularly among women, are supporting demand for premium and branded corporate workwear. The increasing penetration of e-commerce platforms is further improving product accessibility and market expansion across the region.

North America and Europe remain mature yet highly significant markets for corporate workwear, supported by established corporate sectors and strong purchasing power. In North America, demand is driven by large employment bases across finance, technology, healthcare, legal, and professional services industries, where formal and business-casual attire continues to play an important role. The region is also witnessing growing demand for sustainable and performance-enhanced workwear products. Europe benefits from a well-developed corporate culture, stringent workplace standards, and strong consumer preference for high-quality apparel. Countries such as Germany, the United Kingdom, and France continue to contribute substantially to market revenues through demand for premium and fashion-oriented corporate clothing. Across both regions, employers are increasingly prioritizing employee comfort, functionality, and sustainability, encouraging innovation in corporate apparel design and materials.

South America, the Middle East, and Africa collectively represent emerging opportunities within the corporate workwear market. In South America, rising formal employment levels, economic recovery efforts, and the expansion of service industries are supporting demand for professional workplace attire, particularly in countries such as Brazil and Argentina. The Middle East is benefiting from ongoing economic diversification initiatives, growth in financial and business hubs, and increasing participation of international companies, all of which contribute to greater adoption of corporate dress standards. Meanwhile, Africa is witnessing gradual market development driven by urbanization, expanding private-sector employment, and increasing foreign investments.

Competitive Landscape

The workwear market remains moderately concentrated, with global names such as PVH Corp., Ralph Lauren, and Hugo Boss holding strong positions in premium and mid-premium segments. Their advantage comes from brand recognition, formalwear credibility, direct distribution, and global sourcing and merchandising capabilities. At the same time, the workwear market still has a broad field of regional manufacturers, local tailoring specialists, and managed uniform providers serving specific countries, sectors, or price bands. That mix keeps competition active across both consumer and institutional demand pools. Premium players are increasingly focused on better mix, stronger direct-to-consumer execution, and tighter control over product quality and pricing.

Company results from 2025 underscore the significance of larger players in the workwear market. PVH posted a 3% increase in its 2025 revenue, totaling USD 8.95 billion. Ralph Lauren's fiscal 2025 revenue climbed 7% to USD 7.1 billion. Meanwhile, Hugo Boss achieved a 2% growth in currency-adjusted sales, bolstered by a robust performance in formalwear. Ermenegildo Zegna highlighted the profitability safeguards of premium direct channels, noting a 4.2% rise in direct-to-consumer revenue for 2025. As firms pivot towards seeking scale or targeting higher-value niches, rather than merely chasing volume, their strategic maneuvers become increasingly evident. Cintas sealed a USD 5.5 billion deal to acquire UniFirst, Kontoor Brands bolstered its premium and performance portfolio with the acquisition of Helly Hansen, and Lindström's purchase of ORK Poland aims to enhance European production capabilities for professional clothing and uniforms.

In the workwear market, there's a noticeable gap in women's professional apparel, digital fit tools, and managed replenishment services tailored for corporate accounts. Specialist brands are stepping in, addressing these gaps with enhanced comfort fabrics, performance tailoring, and a more focused product design. This shift is significant as buyers now seek officewear that harmonizes appearance, comfort, and usability throughout the workweek. Furthermore, as sustainability standards gain traction in procurement, manufacturers aiming to cater to corporate and institutional clients at scale face heightened expectations. Looking ahead, the market's top performers will likely be those adept at merging brand trust, efficient channels, and product relevance, all while maintaining pricing discipline.

Workwear Industry Leaders

-

PVH Corp.

-

Ralph Lauren Corporation

-

Brooks Brothers Group, Inc.

-

Hugo Boss AG

-

Burberry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Commonwealth Bank of Australia partnered with Gabriella (Bella) Pereira, an esteemed Australian designer, and her label, Beare Park, to revamp the bank's corporate uniforms for frontline staff. This initiative crafted a modern and functional wardrobe for employees while underscoring the bank's dedication to uplifting local businesses and celebrating Australian design talent, continuing its 40-year tradition of championing Australian design.

- March 2026: Fabindia launched its latest workwear campaign, ‘Write Your Own Code,’ which modernized traditional Indian textiles for the contemporary professional landscape. The collection departed from conventional corporate uniforms and embraced a ‘mix-and-match’ approach, seamlessly integrating heritage crafts like Ikat, Ajrakh, and Dabu prints with contemporary silhouettes. By using premium textured cotton and linen, Fabindia catered to the growing demand for breathable, high-performance workwear that maintained professionalism and comfort during long hours.

- February 2025: S&S Activewear (S&S), a tech-driven distributor of apparel and accessories across North America, rolled out AllPro, its exclusive brand tailored for the corporate sector and teams. The diverse lineup catered to various needs, from school and corporate uniforms to styles for active individuals. Featuring budget-friendly t-shirts, sport shirts, and quarter-zips, the collection was designed for men, women, and youth alike.

Global Workwear Market Report Scope

Workwear refers to professionally designed clothing and accessories worn by employees in office, administrative, managerial, and other corporate workplace environments. The workwear market is segmented by product type, category, end user, distribution channel and geography. By product type. the market is segmented into apparel, footwear and accessories. By category, the market is segmented into mass and premium. Based on end user, the market is segmented into men and women. Based on distribution channel, the market is segmented into offline stores and online stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Apparel | Shirts |

| Trousers/Pants | |

| Blazers and Jackets | |

| Skirts and Dresses | |

| Others | |

| Formal Footwear | |

| Accessories |

| Mass |

| Premium |

| Men |

| Women |

| Online Stores |

| Offline Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East & Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Apparel | Shirts |

| Trousers/Pants | ||

| Blazers and Jackets | ||

| Skirts and Dresses | ||

| Others | ||

| Formal Footwear | ||

| Accessories | ||

| By Category | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | Online Stores | |

| Offline Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East & Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for the workwear market?

The workwear market size is projected to rise from USD 276.95 billion in 2026 to USD 344.71 billion by 2031 at a 4.47% CAGR, supported by hiring growth, premiumization, and stronger women’s workforce participation.

Which region leads global demand for workwear?

Asia-Pacific leads with 35.41% share in 2025 and is also the fastest-growing region at a 5.94% CAGR through 2031, helped by stronger hiring activity and rapid digital adoption.

Which product segment is growing fastest in workwear?

Formal Footwear is the fastest-growing product segment with a 5.89% CAGR through 2031, while Apparel remains the largest contributor with 57.28% share in 2025.

Why are premium office apparel and footwear gaining traction?

Buyers are trading up toward better fit, comfort, and fabric quality, which is lifting spending per unit even when volume growth is moderate. This is why Premium is forecast to grow faster than Mass at 6.12% CAGR.

How important are online channels in workwear sales?

Offline stores still led with 62.38% share in 2025, but Online Stores are growing faster at a 6.34% CAGR as brands improve digital convenience, fit support, and direct-to-consumer execution.

Page last updated on: