Sleeping Bruxism Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

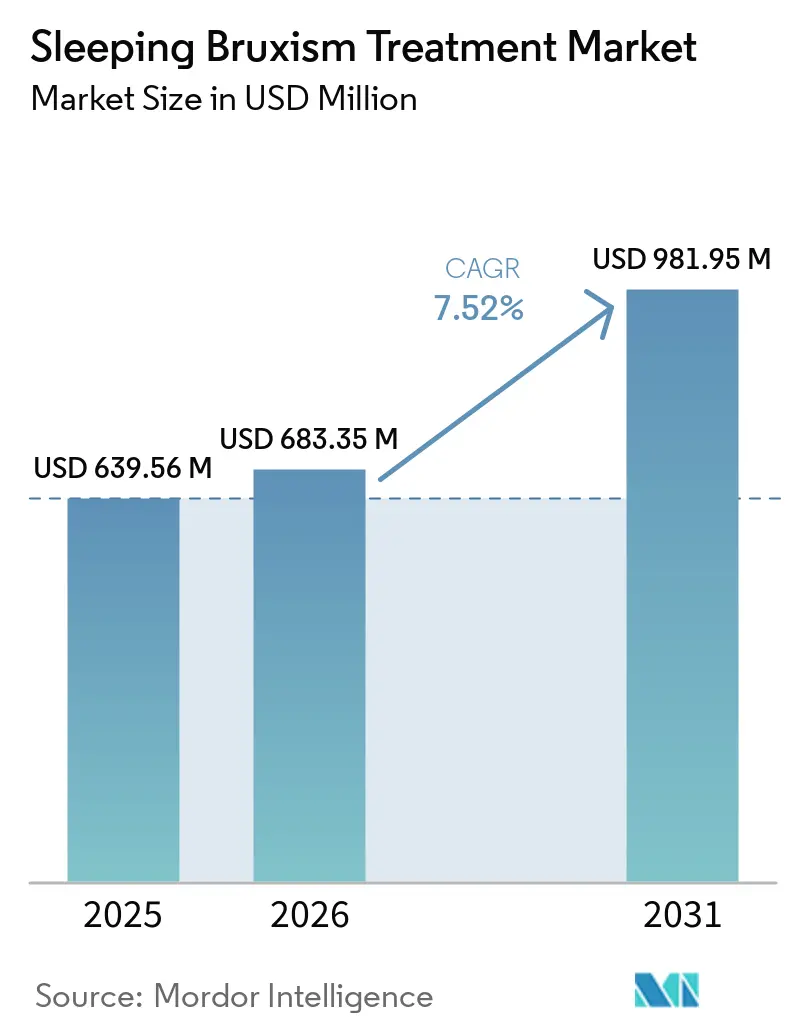

| Market Size (2026) | USD 683.35 Million |

| Market Size (2031) | USD 981.95 Million |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sleeping Bruxism Treatment Market Analysis by Mordor Intelligence

The Sleeping Bruxism Treatment Market size is expected to increase from USD 639.56 million in 2025 to USD 683.35 million in 2026 and reach USD 981.95 million by 2031, growing at a CAGR of 7.52% over 2026-2031.

The sleep bruxism treatment market is drawing stronger clinical attention because it sits across dental care, sleep medicine, and behavioral health, and that overlap is pushing providers to coordinate diagnosis and treatment more closely. Published evidence shows that 49% of adults diagnosed with OSA also present with sleep bruxism, and this overlap is turning single-condition treatment decisions into demand for dual-use appliances and broader care pathways. Diagnosis is also moving beyond routine dental-only pathways toward sleep laboratories and multidisciplinary sleep centers where polysomnography is available, which is changing how prescribers shape therapy choice across the sleep bruxism treatment market. Competition now spans OTC guards, custom laboratory-made appliances, and sensor-enabled premium devices, which is placing price pressure on the middle of the sleep bruxism treatment market while opening room for innovation at the premium end. The main risks remain underdiagnosis and uneven reimbursement, yet the sleep bruxism treatment market still has room to expand as multimodal care, home-based delivery, and OSA co-diagnosis become more common.

Key Report Takeaways

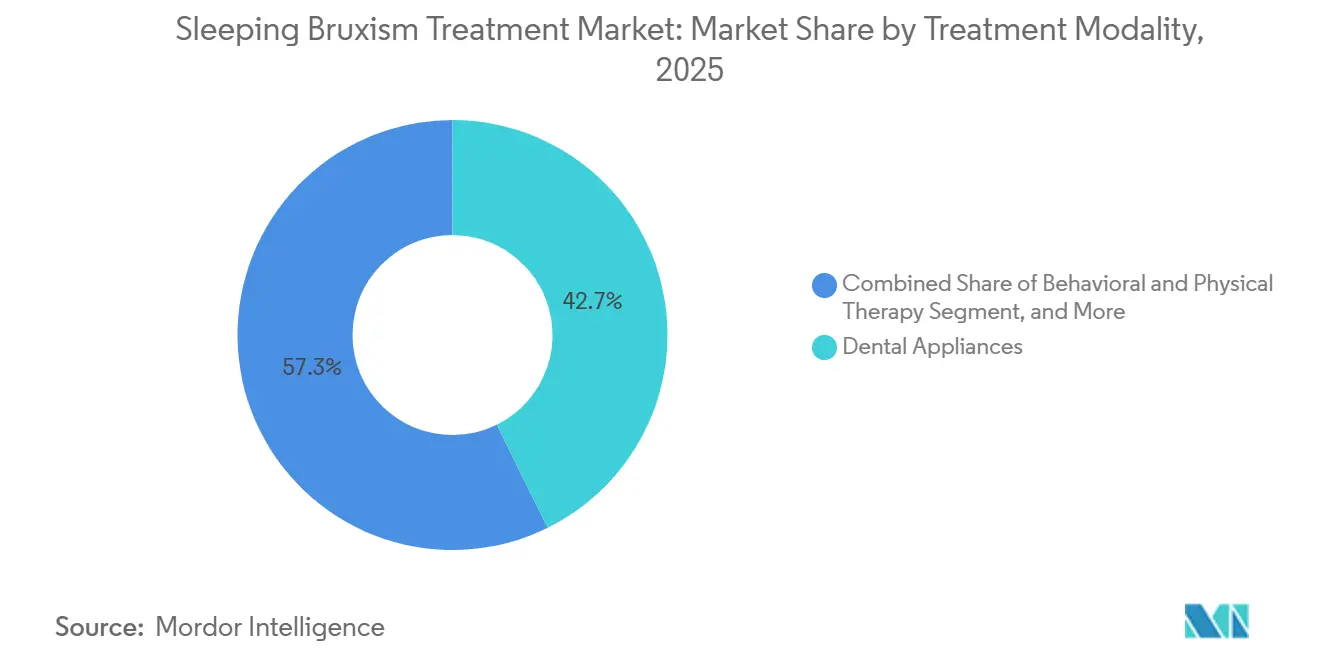

- By treatment modality, dental appliances held 42.68% of the sleep bruxism treatment market share in 2025, while behavioral and physical therapy are forecast to grow at an 8.22% CAGR through 2031.

- By product type, mouth guards accounted for 45.17% of the sleep bruxism treatment market size in 2025, while smart and biofeedback devices are projected to expand at a 7.92% CAGR through 2031.

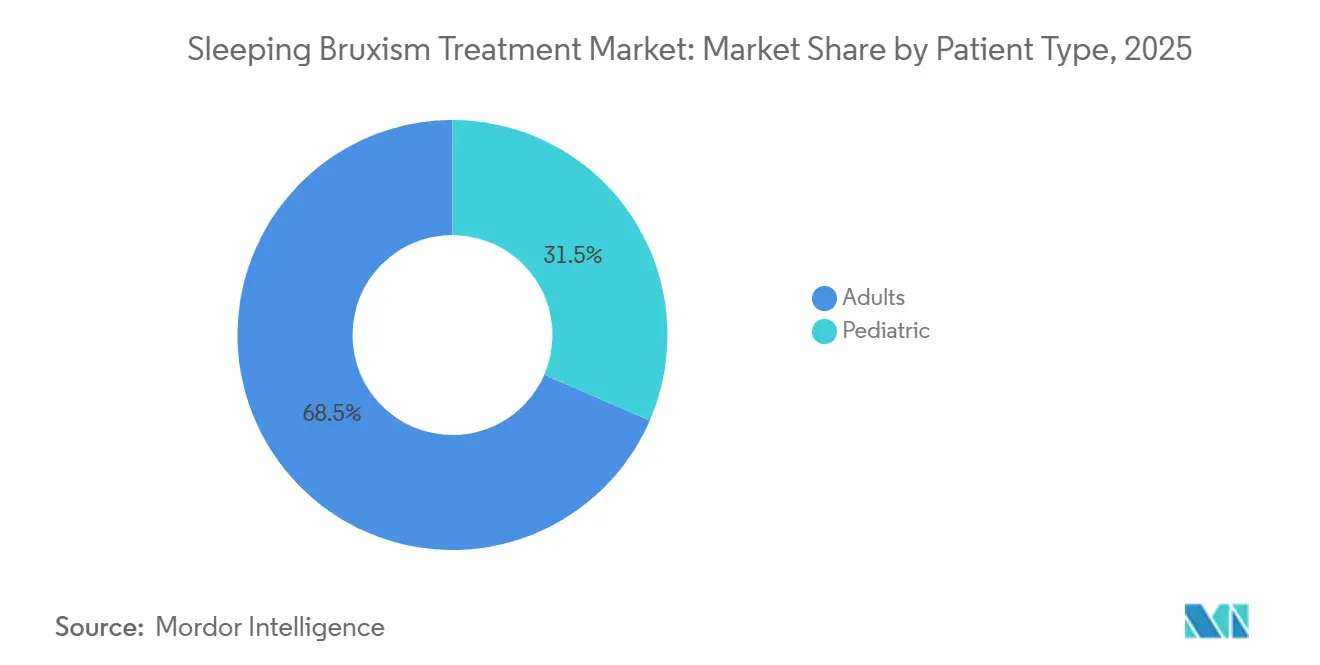

- By patient type, adults represented 68.48% share in 2025, while pediatric treatment is expected to advance at an 8.84% CAGR through 2031.

- By end user, dental clinics captured 57.35% share in 2025, while home care settings are forecast to grow at 10.01% CAGR through 2031.

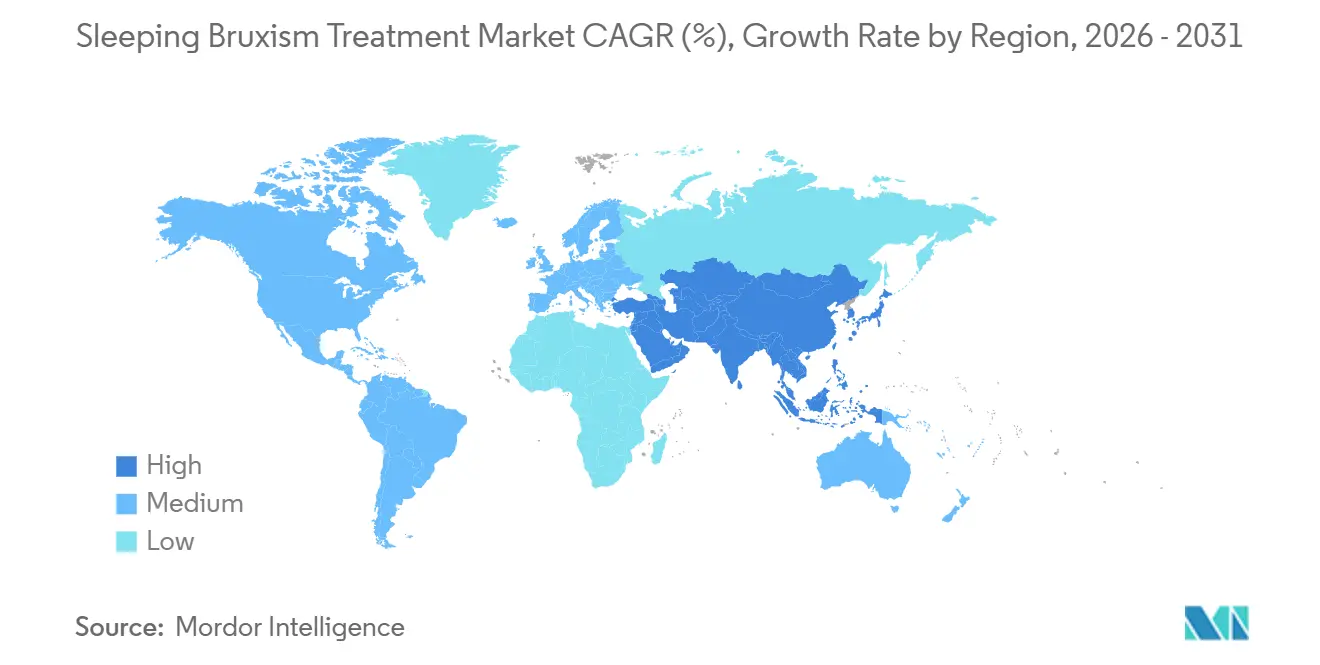

- By geography, North America held 37.24% share in 2025, while Asia-Pacific is projected to record a 9.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sleeping Bruxism Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosis of sleep bruxism with OSA overlap | +1.8% | Global, with highest intensity in North America and Europe | Medium term (2-4 years) |

| Shift toward custom oral appliances and digital dentistry | +1.5% | North America, Western Europe, and APAC including Japan, Australia, and South Korea | Medium term (2-4 years) |

| Adult stress and anxiety burden sustaining treatment demand | +1.4% | Global, with strongest intensity in North America, Western Europe, and urban East Asia | Short term (≤ 2 years) |

| Growth of direct-to-consumer custom night guard channels | +0.8% | North America primarily, with emerging activity in Western Europe and APAC | Short term (≤ 2 years) |

| Smart oral appliances and biofeedback devices entering premium care | +0.7% | North America and Europe, with early-stage APAC activity | Medium term (2-4 years) |

| Dual-use OSA and bruxism appliances opening new treatment pathways | +0.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis of Sleep Bruxism with OSA Overlap

The convergence of bruxism and OSA diagnosis inside multidisciplinary sleep workflows is changing how patients enter the sleep bruxism treatment market. Polysomnography data from 345 OSA patients showed that 13.6% had concurrent sleep bruxism, and this subgroup also had higher daytime sleepiness and reduced REM sleep. A separate study of 105 OSA patients found sleep bruxism in 37.1% of cases, and EMG-measured muscle tone produced an AUC of 0.9, which supports the use of wearable EMG for co-screening in sleep settings.[1]Janine Sambale, “Occlusion, Jaw Function and Nocturnal Muscle Tone in Obstructive Sleep Apnea With and Without Sleep Bruxism,” Clinical Oral Investigations, doi.org. This matters commercially because co-diagnosed patients are more likely to move toward dual-use mandibular advancement devices or combined treatment plans instead of single-condition night guards. The literature is also increasingly anchored to AASM-linked diagnostic framing, which suggests sleep medicine standards will continue to shape prescriber behavior in the sleep bruxism treatment market, especially in North America. As these care pathways widen, providers that can address both airway management and tooth protection are likely to capture more of the sleep bruxism treatment market.

Shift Toward Custom Oral Appliances and Digital Dentistry

Digital fabrication is changing the cost, speed, and delivery model of custom oral appliances across the sleep bruxism treatment market. CAD/CAM milling, intraoral scanning, and additive manufacturing are shortening turnaround times and making remote fulfillment models more viable than before.[2]Ravinder S. Saini, “Comparison of Digital Splints Versus Traditional Splints for Bruxism Management, A Systematic Review,” BDJ Open, doi.org. SomnoMed reported that manufacturing investments through 2025 reduced production turnaround from more than 20 days to under 10 days and expanded capacity by more than 40%, which strengthened its ability to convert users from competing products. Panthera’s digitally manufactured nylon appliances carry FDA 510(k) clearance, CE marking, and HCPCS billing support, which improves reimbursement fit and broadens their commercial reach beyond fully self-pay patients. A 2026 systematic review found that digital splints tended to reduce symptom severity more than conventional acrylic splints, although the trials were still limited in size. The result is a sleep bruxism treatment market that is becoming less dependent on the older multi-visit workflow and more responsive to faster custom production.

Adult Stress and Anxiety Burden Sustaining Treatment Demand

Stress and anxiety continue to support demand across the sleep bruxism treatment market, especially in adult and working-age populations. A cross-sectional study of 111 health science students found that 55.4% of bruxers had clinically relevant anxiety, and the rate was 2.8 times higher than in non-bruxers. A 12-month study of 136 dental students found that awake bruxism behaviors increased significantly over time, and each unit rise in perceived stress score raised the odds of bruxism behavior by 16% in the later phase.[3]Alona Emodi-Perlman, “Impact of Long-Term Stress on Awake Bruxism,” Dental and Medical Problems, dmp.umw.edu.pl. These findings support the view that treatment demand is tied to persistent psychological burden rather than only short-lived episodes. That pattern gives providers and manufacturers a more durable demand base across the sleep bruxism treatment market, even when economic conditions improve. It also helps explain why multimodal protocols that combine physical protection with behavior-focused care are gaining traction.

Smart Oral Appliances and Biofeedback Moving into Premium Care

Biofeedback is moving from the research stage into premium care pathways within the sleep bruxism treatment market. Aesyra’s clinical investigation in 26 adults showed a 60.6% reduction in total sleep bruxism duration per hour, with no adverse events and positive comfort feedback. The company began its FDA submission in early 2026 and plans European regulatory filing after that, which points to near-term commercial readiness. An AI-enabled intraoral biofeedback prototype also achieved 91% accuracy and 90% specificity in distinguishing pathological occlusal force events after training on more than 50,000 data points. The clinical direction suggests that biofeedback may work best when paired with occlusal protection, especially in patients who need both activity reduction and protection from tooth wear. This keeps the premium end of the sleep bruxism treatment market focused on combined functionality rather than on simple substitution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Underdiagnosis and absence of a universally accepted care standard | -1.2% | Global, with greatest pressure in South America, the Middle East and Africa, and emerging APAC markets | Long term (≥ 4 years) |

| High out-of-pocket costs and fragmented reimbursement coverage | -1.0% | North America, Western Europe, and APAC | Medium term (2-4 years) |

| Low-cost OTC guards reducing conversion to custom appliances | -0.8% | North America and Western Europe | Short term (≤ 2 years) |

| Limited long-term adherence to appliance wear and behavioral protocols | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Underdiagnosis and No Universally Accepted Care Standard

The absence of a universally adopted clinical protocol continues to limit diagnosis and consistent treatment across the sleep bruxism treatment market. An overview of 31 systematic reviews concluded that the evidence base for oral appliances, pharmacological options, and biofeedback remained too heterogeneous to define a clear standard of care. That fragmentation means the same patient can receive different labels and different therapy recommendations depending on whether the first visit is with a general dentist, a sleep physician, or an orofacial pain specialist. Polysomnography remains the gold standard for definitive diagnosis, but cost and access still confine it to specialist settings, so many patients are managed under possible or probable bruxism categories rather than confirmed diagnosis. Reference systems such as ICSD-3 and AASM provide a useful framework, but routine use outside specialist practice remains limited. This slows patient conversion, weakens treatment consistency, and keeps part of the sleep bruxism treatment market below its epidemiological potential.

High Out-of-Pocket Costs and Patchy Reimbursement

Patient costs and uneven reimbursement continue to limit conversion to higher-value therapies in the sleep bruxism treatment market. Kaiser Permanente’s 2025 dental plan covers removable bruxism appliances at 35% coinsurance and limits replacement to once every 5 years, while HMSA excludes bite guards entirely. Blue Shield of California reimburses custom hard occlusal guards at USD 113 per appliance, which leaves a meaningful gap against normal clinical fabrication costs. Low reimbursement ceilings and replacement limits raise multi-year out-of-pocket exposure for patients who need ongoing appliance management. That cost burden pushes some patients toward OTC guards instead of clinician-guided custom care. It also narrows the addressable base for premium products and makes price sensitivity a persistent check on growth in the sleep bruxism treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Behavioral Therapies Outpace Legacy Appliance Volumes

Dental appliances held 42.68% of treatment modality revenue in 2025, which kept them at the center of the sleep bruxism treatment market. Custom-fitted night guards, Michigan splints, and mandibular advancement devices remain the core products because they align with familiar first-line practice patterns in established dental systems. Their lead also reflects the established laboratory supply chain that manufactures and distributes these products at scale across clinic networks. Behavioral and physical therapy is projected to grow at an 8.22% CAGR through 2031, making it the fastest-rising treatment approach in the sleep bruxism treatment market. That growth reflects a broader shift toward non-invasive care that can reduce symptom burden without introducing a device-wear barrier for every patient. The sleep bruxism treatment industry is therefore moving toward a more balanced mix of protection, habit management, and supportive care.

The IAPD’s 2024 consensus on pediatric bruxism supports CBT and proprioceptive approaches when psychosocial factors are present, and that position is starting to influence wider protocol design. Pharmacological and injectable therapy remains relevant for patients with masseteric hypertrophy or TMD comorbidity, but the role of botulinum toxin in reducing episode frequency is still debated. A 2024 systematic review of 9 randomized trials found that botulinum toxin improved pain and EMG activity over the first 3 to 16 weeks, but the benefit weakened by 3.5 months. Device-assisted monitoring and biofeedback remain early in commercialization, yet clinical validation is giving that segment a clearer position inside the sleep bruxism treatment industry. Combination therapy is also drawing more interest in premium care settings where patients are willing to pay for broader protocols that unite protection, retraining, and monitoring.

By Product Type: Smart Devices Reframe the Night Guard Category

Mouth guards accounted for 45.17% of the sleep bruxism treatment market size in 2025, which made them the largest product category. Soft, hard, and dual-laminate designs remain widely used because they are familiar to prescribers and can be produced across major dental laboratory networks. Hard acrylic Michigan-style guards and flat-plane stabilization splints continue to dominate prescribed use because they provide durable occlusal protection across repeated wear cycles. Dual-laminate and hybrid designs are gaining attention because they try to combine durability with better comfort, and that directly addresses a common adherence barrier. In a German multicenter study, respiratory impairment from a splint reduced adherence by a factor of 10 after insertion, which shows how directly product comfort affects actual use.

Smart and biofeedback devices are projected to grow at a 7.92% CAGR through 2031, making them the fastest-growing product segment in the sleep bruxism treatment market. Their growth reflects the spread of sensor-based monitoring and the appeal of products that do more than passively shield teeth. Sensor-embedded intraoral devices and wearable EMG systems are moving treatment toward measurement, feedback, and remote follow-up rather than simple protection alone. This is one reason the sleep bruxism treatment market is seeing more premium product development, even while conventional guards still dominate volumes. Injectable and oral drug products still serve patients with poor appliance adherence or distinct pain-related needs, but they add incremental revenue rather than replacing appliance-led care across the sleep bruxism treatment market.

By Patient Type: Pediatric Diagnosis Driving a Latent Demand Wave

Adults represented 68.48% of revenue in 2025, which made them the main diagnosed and treated population in the sleep bruxism treatment market. Working-age and older adults account for most current demand because stress-related presentations and OSA-linked bruxism are more visible in these groups. Middle-aged adults are especially important commercially because they are the most active users of custom appliances and adjunctive therapies. Older adults are also becoming more relevant as restorative and prosthetic complications create additional reasons to seek treatment. This adult base keeps present revenue concentrated even as other patient groups expand.

Pediatric treatment is projected to grow at an 8.84% CAGR through 2031, which makes it the fastest-growing patient category in the sleep bruxism treatment market. A 2024 meta-analysis reported sleep bruxism prevalence of 28% in North American minors, 24% in South American minors, and 14.4% in Asian minors, which shows that the addressable population is larger than current treatment volumes imply. The IAPD’s 2024 recommendations also noted that prevalence reached 90.9% among children with tonsil hypertrophy, restricted tongue mobility, or nasal obstruction, linking airway issues to treatment need. This is pushing more attention toward earlier recognition by pediatric dentists and general practitioners. As recognition improves, the sleep bruxism treatment market is likely to convert more latent pediatric demand into active monitoring and treatment.

By End User: Home Care Models Disrupting Dental Clinic Primacy

Dental clinics held 57.35% of end-user revenue in 2025, which kept them as the leading access point in the sleep bruxism treatment market. Their position comes from their central role in prescribing and dispensing custom-fitted appliances and injection-based therapies. Close commercial ties between clinics and dental laboratories also support recurring appliance orders when devices need replacement or adjustment. Hospitals and multidisciplinary sleep centers form the next important tier, and their role is rising as more diagnoses flow through polysomnography-based sleep workflows. That shift means treatment decisions are increasingly shaped by sleep physicians as well as by dentists.

Home care settings are projected to grow at 10.01% CAGR through 2031, which gives them the highest growth rate among end users in the sleep bruxism treatment market. Direct-to-consumer custom guard platforms, at-home impression kits, and scan-based remote delivery are the main reasons this channel is expanding so quickly. Specialty sleep and neurology centers are also emerging as prescribing points for smart appliances and biofeedback devices in higher-severity cases. As care moves closer to the home, regulatory and reimbursement frameworks for prescription appliances and connected biofeedback devices become more important to what can be marketed and paid for. This is gradually redistributing value within the sleep bruxism treatment market from the clinic-only model toward hybrid care delivery.

Geography Analysis

North America held 37.24% of the sleep bruxism treatment market share in 2025, making it the largest regional segment. The region benefits from relatively strong dental insurance access, broad custom appliance use, and active work on dual-use OSA and bruxism solutions. The United States anchors most regional revenue because it combines a large dental channel with a more developed sleep medicine ecosystem. Diagnosis is also shifting toward multidisciplinary sleep settings, which increases the role of sleep laboratories and sleep physicians in therapy selection. That mix keeps North America commercially mature while still leaving room for premium device innovation and home-based care expansion.

Asia-Pacific is projected to expand at a 9.16% CAGR through 2031, giving it the fastest regional growth within the sleep bruxism treatment market size. Growth across the region is uneven, with Australia contributing more than 80% of SomnoMed’s APAC revenue while also facing competitive and economic pressure in the first half of FY26. China, Japan, and India remain underpenetrated markets where diagnosis is still limited or treatment remains conservative. That leaves a large untreated patient pool across the broader sleep bruxism treatment market. Rising dental infrastructure and consumer health spending continue to support the region’s forward growth path.

Europe remains the second-largest regional segment, and SomnoMed reported 17% revenue growth in Europe to AUD 32.7 million (USD 21.3 million) in the first half of FY26 as reimbursement expanded in France, Sweden, Germany, Norway, and Finland. Germany stands out as a notable demand center because the market combines meaningful patient volume with structured reimbursement and billing channels. The Middle East, Africa, and South America remain smaller today, but both regions are developing gradually as dental infrastructure and awareness improve. Brazil’s clinical research activity and the GCC’s ongoing dental investment support future entry opportunities for premium appliance suppliers. These regions still face cost constraints, which keep treated volumes below the level suggested by underlying epidemiology.

Competitive Landscape

The sleep bruxism treatment market remains moderately fragmented, with large dental laboratory groups, specialist oral appliance makers, newer medtech firms, and OTC consumer brands competing across different price points. National Dentex Labs, Glidewell, S4S Dental Laboratory, and Crown World Dental Lab form an important part of the custom appliance manufacturing base used across clinical channels. SomnoMed remains the most globally scaled specialist player in this space, reporting AUD 60.7 million (USD 39.5 million) in group revenue in the first half of FY26, a 61.3% gross margin, and FY26 revenue guidance of AUD 119 million to AUD 126 million (USD 77.4 million to USD 81.9 million). That scale gives SomnoMed a clear advantage in production, channel relationships, and prescriber reach within the sleep bruxism treatment market. The structure also reflects a three-tier pattern, with OTC products competing on price, custom appliances holding the middle, and digital or sensor-based systems competing on differentiated value.

SomnoMed’s October 2024 FDA clearance for Rest Assure as the first oral device with built-in compliance monitoring is a notable move because it adds objective adherence tracking to oral appliance therapy. The company also expanded manufacturing capacity and shortened turnaround times, which supports faster conversion of competing product users and strengthens channel stickiness. Panthera is pushing premium competition through digitally manufactured nylon appliances and reimbursement-ready positioning, which helps it compete on workflow speed and payer fit instead of only on chairside preference. Aesyra is pursuing a biofeedback-led route, and that shows how innovation at the premium end is widening beyond passive guards. These strategic moves are gradually raising the technology threshold for differentiation in the sleep bruxism treatment market.

Remote monitoring remains an open competitive space because few products fully connect home-use data with routine clinician oversight. OTC boil-and-bite products continue to pressure entry pricing, which makes it harder for first-time custom products to compete on cost alone. At the same time, digital workflows such as intraoral scanning, 3D printing, and app-connected monitoring are forcing mid-market laboratories to invest faster or risk losing ground to more integrated models. Consumer-facing biofeedback products from newer firms also suggest that part of the next competitive phase may develop outside the traditional dental prescribing channel.

Sleeping Bruxism Treatment Industry Leaders

-

GuardLab

-

National Dentex Labs

-

Panthera Dental

-

SomnoMed Limited

-

The Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SomnoMed Limited reported record 1H FY26 revenue of AUD 60.7 million (+13%), expanded manufacturing capacity by over 20% with additional milling machines, and reduced production turnaround time by over 50%. The company reaffirmed FY26 revenue guidance of AUD 119-126 million.

- January 2026: Aesyra SA announced positive results from clinical investigation NCT06153810 for AesyBite Active, demonstrating a 60.6% reduction in total sleep bruxism duration per hour (p < 0.001) in 26 adult patients. The Swiss medtech company initiated FDA regulatory submission targeting US approval in 2026 and plans European submission thereafter, with go-to-market activities with existing partners beginning in 2026.

- January 2026: Kronos Advanced Technologies Inc. completed the acquisition of Zyppah Inc., an FDA-cleared anti-snoring mouthpiece company, establishing it as a new wholly-owned subsidiary and integrating Zyppah's products with KronosMD's AI-driven 3D ultrasound remote dental imaging platform for digital custom-fitted sleep appliances.

Global Sleeping Bruxism Treatment Market Report Scope

The Sleep Bruxism Treatment Market refers to the global healthcare, pharmaceutical, and dental industry sector dedicated to the diagnosis and management of sleep bruxism a subconscious, repetitive jaw muscle activity characterized by involuntary teeth grinding and clenching during sleep.

The Sleep Bruxism Treatment Market Report is Segmented by Treatment Modality (Dental Appliances, Pharmacological and Injectable Therapy, Behavioral and Physical Therapy, Device-Assisted Monitoring and Biofeedback, Combination Therapy), Product Type (Mouth Guards, Occlusal Splints, Smart and Biofeedback Devices, Injectable and Oral Drug Products), Patient Type (Adults, Pediatric), End User (Dental Clinics, Hospitals and Multidisciplinary Sleep Centers, Home Care Settings, Specialty Sleep and Neurology Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Dental Appliances | Mouth Guards | Custom-Fitted Night Guards |

| OTC Boil-and-Bite Guards | ||

| Occlusal Splints | Michigan Splints | |

| Stabilization Splints | ||

| Anterior Deprogrammers / NTI-tss | ||

| Mandibular Advancement and Dual-Use Sleep Appliances | ||

| Pharmacological and Injectable Therapy | Botulinum Toxin Type A | |

| Muscle Relaxants | ||

| Anxiolytics and Sedative-Hypnotics | ||

| Behavioral and Physical Therapy | Cognitive Behavioral Therapy and Stress Management | |

| Sleep Hygiene and Relaxation Training | ||

| Physiotherapy and TMJ Support | ||

| Device-Assisted Monitoring and Biofeedback | EMG Biofeedback Devices | |

| Smart Oral Appliances | ||

| Home Sleep Monitoring Devices | ||

| Combination Therapy | ||

| Mouth Guards | Soft |

| Hard | |

| Dual-Laminate / Hybrid | |

| Occlusal Splints | Michigan Splints |

| Flat-Plane Stabilization Splints | |

| Anterior Bite Planes / NTI-tss | |

| Smart and Biofeedback Devices | Headband-Based Biofeedback |

| Sensor-Embedded Oral Appliances | |

| Injectable and Oral Drug Products | Botulinum Toxin Type A |

| Oral Prescription Drugs |

| Adults | Younger Adults |

| Middle-Aged Adults | |

| Older Adults | |

| Pediatric |

| Dental Clinics |

| Hospitals and Multidisciplinary Sleep Centers |

| Home Care Settings |

| Specialty Sleep and Neurology Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Dental Appliances | Mouth Guards | Custom-Fitted Night Guards |

| OTC Boil-and-Bite Guards | |||

| Occlusal Splints | Michigan Splints | ||

| Stabilization Splints | |||

| Anterior Deprogrammers / NTI-tss | |||

| Mandibular Advancement and Dual-Use Sleep Appliances | |||

| Pharmacological and Injectable Therapy | Botulinum Toxin Type A | ||

| Muscle Relaxants | |||

| Anxiolytics and Sedative-Hypnotics | |||

| Behavioral and Physical Therapy | Cognitive Behavioral Therapy and Stress Management | ||

| Sleep Hygiene and Relaxation Training | |||

| Physiotherapy and TMJ Support | |||

| Device-Assisted Monitoring and Biofeedback | EMG Biofeedback Devices | ||

| Smart Oral Appliances | |||

| Home Sleep Monitoring Devices | |||

| Combination Therapy | |||

| By Product Type | Mouth Guards | Soft | |

| Hard | |||

| Dual-Laminate / Hybrid | |||

| Occlusal Splints | Michigan Splints | ||

| Flat-Plane Stabilization Splints | |||

| Anterior Bite Planes / NTI-tss | |||

| Smart and Biofeedback Devices | Headband-Based Biofeedback | ||

| Sensor-Embedded Oral Appliances | |||

| Injectable and Oral Drug Products | Botulinum Toxin Type A | ||

| Oral Prescription Drugs | |||

| By Patient Type | Adults | Younger Adults | |

| Middle-Aged Adults | |||

| Older Adults | |||

| Pediatric | |||

| By End User | Dental Clinics | ||

| Hospitals and Multidisciplinary Sleep Centers | |||

| Home Care Settings | |||

| Specialty Sleep and Neurology Centers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is driving growth in sleep bruxism treatment through 2031?

Growth is being supported by rising OSA co-diagnosis, broader use of digital oral appliances, stronger stress-linked adult demand, and faster adoption of home-based care models.

Which treatment approach leads current revenue?

Dental appliances lead current revenue with 42.68% share in 2025, reflecting their continued role as the main first-line option in established dental channels.

Which product category is growing the fastest?

Smart and biofeedback devices are the fastest-growing product category, with a projected 7.92% CAGR through 2031 as monitoring and feedback features gain clinical support.

Why is the pediatric category attracting more attention?

Pediatric treatment is forecast to grow at 8.84% CAGR through 2031 because awareness is improving and the underlying addressable population is larger than present treatment volumes.

Which region offers the strongest near-term opportunity?

Asia-Pacific offers the strongest growth outlook, with a projected 9.16% CAGR through 2031, even though North America remains the largest regional revenue base today.

How large is the sleep bruxism treatment by 2031?

The sleep bruxism treatment is forecast to reach USD 981.95 million by 2031, with a 7.52% CAGR from 2026 to 2031.

Page last updated on: