Singapore Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

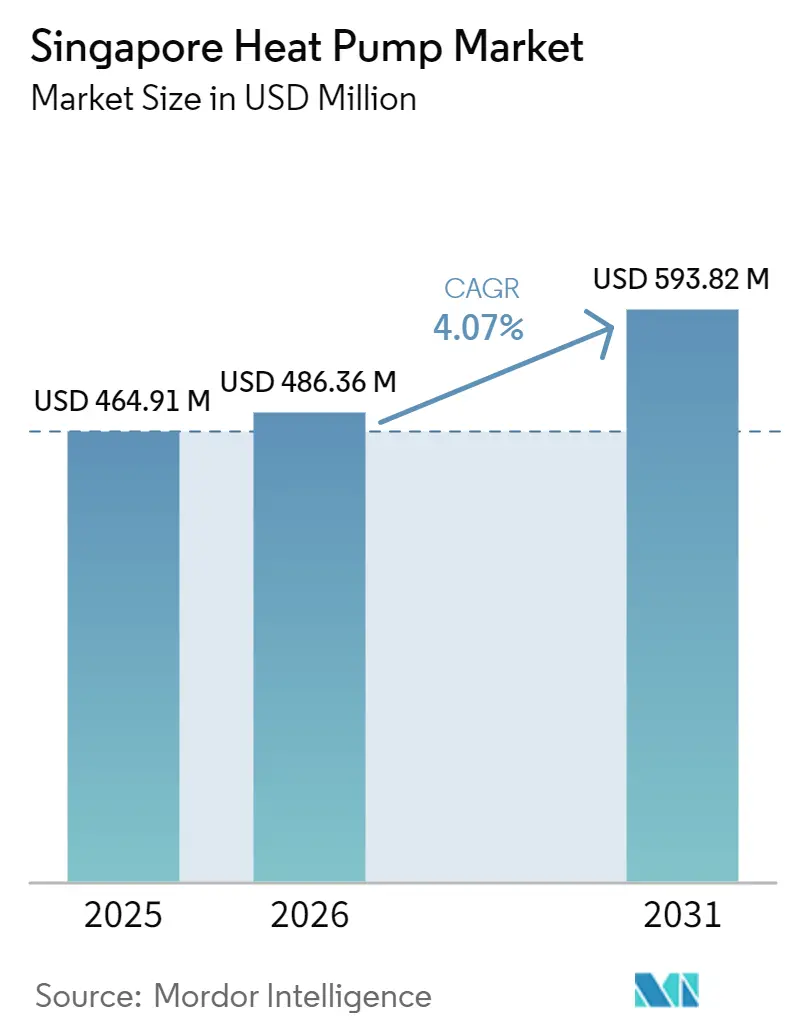

| Base Year Market Size (2025) | USD 464.91 Million |

| Market Size (2026) | USD 486.36 Million |

| Market Size (2031) | USD 593.82 Million |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Heat Pump Market Analysis by Mordor Intelligence

The Singapore heat pump market size is projected to be USD 464.91 million in 2025, USD 486.36 million in 2026, and reach USD 593.82 million by 2031, growing at a CAGR of 4.07% from 2026 to 2031. Structural demand is rising because retrofit mandates inside the Green Plan 2030 force building owners to replace aging water heaters and chillers with efficient, ultra-low-GWP heat pumps. District cooling build-outs in Marina Bay, Jurong Lake District, Tengah, and HarbourFront are shifting purchases toward high-capacity, air-to-water units that integrate with chilled-water networks. Suppliers are also benefiting from the National Environment Agency’s five-tick energy label, which places conventional electric resistance and gas heaters at a regulatory disadvantage. At the same time, data-center developers that already use about 7% of national power are specifying magnetic-bearing chillers and large heat pumps, creating a second growth engine for the Singapore heat pump market.

Key Report Takeaways

- By technology, air-to-water systems led with 51.31% of the Singapore heat pump market share in 2025 and are projected to advance at a 5.02% CAGR through 2031.

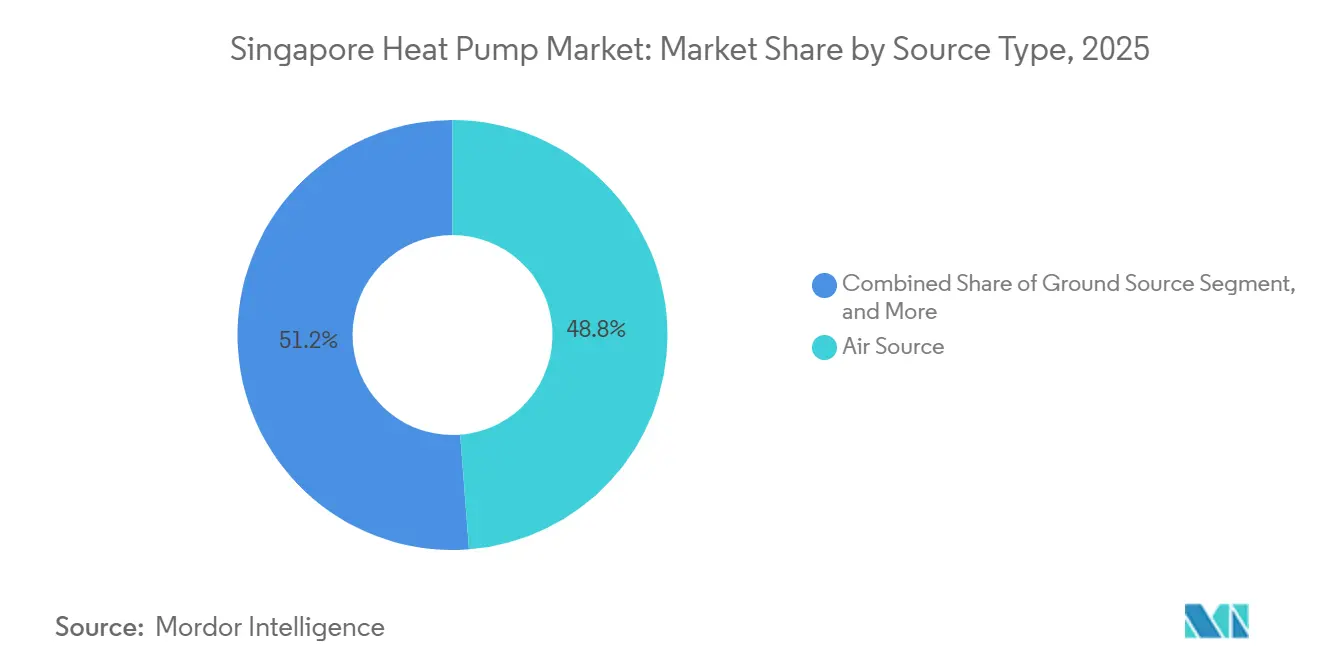

- By source type, air-source units held 48.78% share of the Singapore heat pump market in 2025, while hybrid source systems are forecast to post the fastest 4.81% CAGR over 2026-2031.

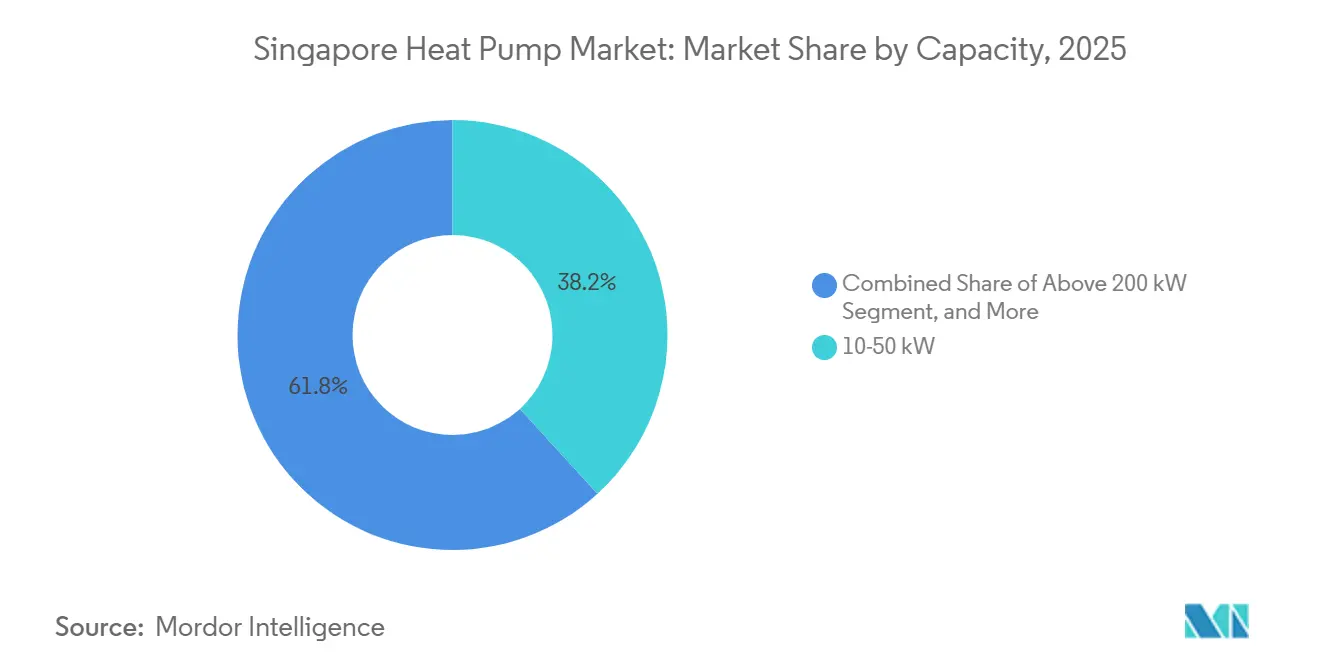

- By capacity, the 10-50 kW segment accounted for 38.23% of the Singapore heat pump market size in 2025, whereas the 50-200 kW bracket is anticipated to record the highest 4.46% CAGR up to 2031.

- By application, domestic and sanitary hot-water solutions captured 42.82% of the Singapore heat pump market share in 2025, while industrial and process heating is projected to expand at a 4.63% CAGR through 2031.

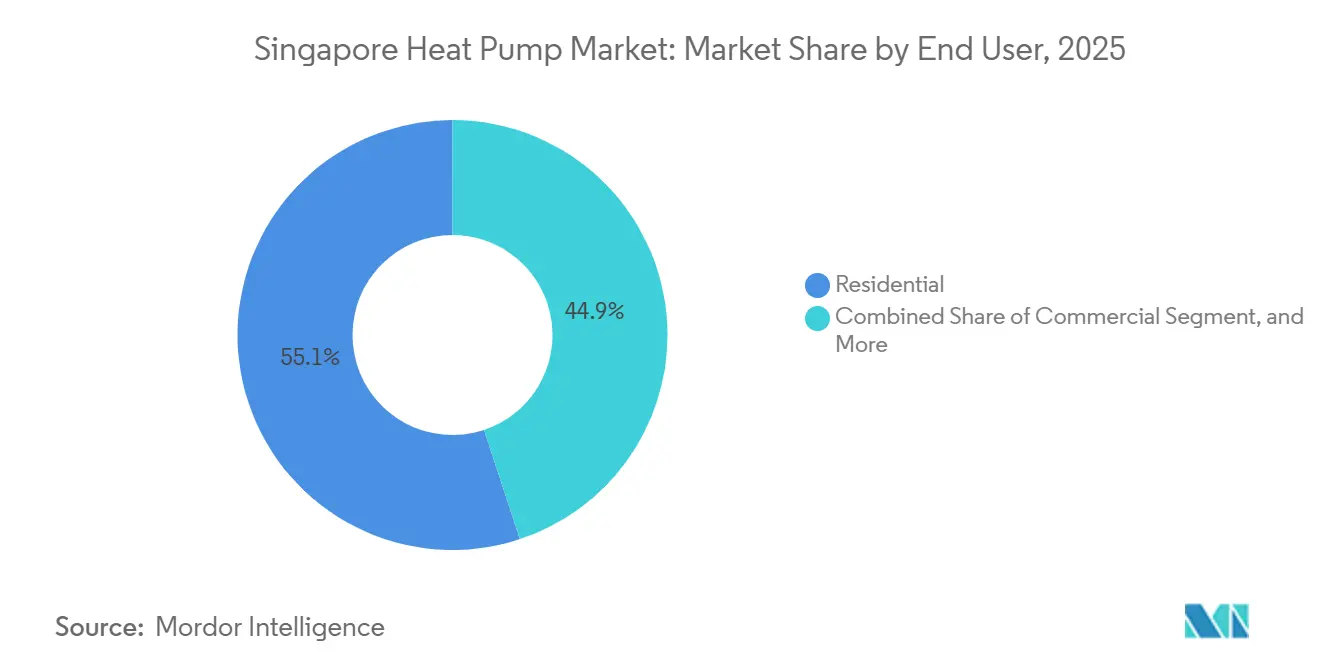

- By end user, residential properties commanded 55.09% share of the Singapore heat pump market in 2025, but commercial facilities are set to register the quickest 4.29% CAGR during 2026-2031.

- By installation, retrofit projects dominated with 61.43% of the Singapore heat pump market size in 2025 and are expected to grow at a 4.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public Sector Retrofit Grants Under Green Plan 2030 | +0.9% | National, with early momentum in CBD, Jurong Lake District, Marina Bay | Medium term (2-4 years) |

| Mandatory Energy-Labeling for Water Heaters | +0.7% | National | Short term (≤ 2 years) |

| Commercial and Municipal District-Cooling Expansion | +1.1% | Marina Bay, Jurong Lake District, Tengah, HarbourFront | Long term (≥ 4 years) |

| Rising Carbon-Tax Trajectory | +0.6% | National | Medium term (2-4 years) |

| Integration of High-COP Heat Pumps With Floating PV Pilots | +0.4% | Tengeh Reservoir, Jurong Island | Long term (≥ 4 years) |

| Demand for Ultra-Low-GWP Refrigerant Systems | +0.8% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Public Sector Retrofit Grants Under Singapore Green Plan 2030

The Government earmarked SGD 63 million (USD 47 million) for the Grant for Energy Efficient Measures in Existing Buildings 2.0, extended to March 2027, to help commercial and municipal owners upgrade HVAC systems.[1]Building and Construction Authority, “Green Mark 2025,” bca.gov.sg Grant-related projects prioritize comprehensive packages that couple heat pumps with building-management software and chiller replacements, rewarding vendors that can deliver turnkey retrofits. Because eligible floor space is concentrated in the Central Business District and emerging polycentric hubs, contractors with prior relationships in those zones are winning early orders. Building owners also lean on partners that can navigate Green Mark paperwork and energy-performance verification to unlock disbursements. The three-year runway allows suppliers to lock in multiyear pipelines, tightening competition for high-capacity air-to-water units.

Mandatory Energy-Labeling Pushing Premium-Efficiency Heat Pumps

The National Environment Agency introduced a five-tick label and a uniform energy-factor test for water heaters effective 1 April 2025.[2]National Environment Agency, “Minimum Energy Performance Standards for Water Heaters,” nea.gov.sg Heat-pump water heaters consistently achieve four or five ticks, while conventional electric resistance units rarely reach two ticks, guiding buyers toward premium efficiency. Because manufacturers must lodge models with the agency before sales, smaller brands without accredited laboratories face entry barriers. Transparent labels highlight lifecycle savings and shrink the information gap that once made capital-intensive heat pumps a hard sell. As a result, distributors report a pivot in ordering patterns ahead of the April deadline, especially from hospitality chains seeking visible sustainability credentials.

Commercial and Municipal District-Cooling Expansion

Keppel Infrastructure won a 30-year contract for Jurong Lake District’s plant and SP Group secured a distributed system for HarbourFront in January 2026, totaling 17,150 refrigeration tonnes.[3]SP Group, “HarbourFront Precinct District Cooling,” spgroup.com.sg Centralized networks improve load factors, eliminate redundant rooftop units, and support large-capacity heat pumps that deliver chilled and hot water on a single loop. Tengah’s public-housing deployment extends the model to residential estates, though early condensation issues triggered stricter material and quality-control rules. Brownfield retrofits such as HarbourFront reveal an additional upside because owners must replace nearing-end-of-life chillers and now prefer concession models that shift capex to the operator.

Growing Demand for Ultra-Low-GWP Refrigerant Systems Ahead of 2028 HFC Phase-Down

A consultation concluded in September 2025 proposes a 150-GWP ceiling for new systems from April 2027. Manufacturers already responded: Daikin launched the EWYK-QZ module with R290 in late 2025, Panasonic followed with the Aqua-G EVO in March 2026, and Alfa Laval adapted brazed plate heat exchangers for propane and R1234ze blends. Early adopters lock in lower leak liabilities and compliance certainty, while laggards risk stock obsolescence once the rule takes effect. The accelerated roadmap compresses product-development cycles, pushing component suppliers to invest in higher-pressure designs and field training for flammable refrigerants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capex Versus Gas Water Heaters | -0.5% | National, strongest in residential estates | Short term (≤ 2 years) |

| Limited Roof and Plant Space in High-Rise Buildings | -0.3% | Urban core commercial and residential districts | Medium term (2-4 years) |

| Technical Workforce Shortages for Installation and Service | -0.2% | National | Short term (≤ 2 years) |

| Grid-Reserve Constraints During Weekday Peak Cooling Hours | -0.4% | National, acute in CBD, Marina Bay, Jurong clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex Versus Gas Water Heaters

Residential heat-pump water heaters cost about SGD 3,400 (USD 2,520) for a 60-liter unit against gas heaters under SGD 1,000 (USD 740).[4]Housing and Development Board, “Centralized Cooling Pilot at Tengah,” hdb.gov.sg The extra wiring, drainage, and ventilation work adds another SGD 500 to 1,000 (USD 370 to 740). Because the Energy Efficiency Grant excludes individual homeowners, no offsetting subsidy shortens payback, so many owners still choose cheaper gas models. Resale-flat dwellers and condominium management committees often postpone upgrades until failures occur, constraining annual unit sales in the sub-10 kW class, even though operating savings reach SGD 500 (USD 370) over three years.

Limited Roof and Plant Space in High-Rise Buildings

Singapore’s skyline forces rooftop real-estate to be shared by solar PV, telecom equipment, maintenance access, and HVAC plants. Green Mark credits for PV tilt decisions toward panels over heat-pump outdoor units. Retrofitting requires acoustic enclosures to respect residential noise limits and sometimes structural reinforcement, escalating cost and project timelines. Developers mitigate these hurdles by favoring high-capacity water-cooled plants in basement or podium plantrooms, which explains why the 50-200 kW band is growing faster than smaller sizes tied to facade-mounted units.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominates, Hybrid Gains Traction

Air-source units delivered 48.78% of the Singapore heat pump market share in 2025. Warm ambient air of 25 °C and above supports stable year-round coefficients of performance while avoiding costly boreholes or seawater intakes. Comparable upfront pricing and simpler permitting make the format the default for residential retrofits and small offices. In hybrid deployments, facility managers pair an air-source heat pump with a back-up gas boiler or electric element to arbitrage tariff fluctuations, driving a 4.81% CAGR forecast up to 2031. Water-source models serve niche maritime and petrochemical sites where seawater is plentiful, yet anti-corrosion expenses and discharge rules cap volume. Ground-source options remain rare because vertical drilling is price-prohibitive on land-scarce plots. Auditors certified under the Building and Construction Authority scheme often default to air-source recommendations, reinforcing incumbent momentum.

System suppliers increasingly pre-install smart controllers that modulate fan speeds and defrost cycles to handle Singapore’s high humidity, reducing maintenance callbacks. Component makers such as Copeland rolled out digital scroll compressors fine-tuned for the tropical envelope, nudging market acceptance of higher-se efficiency classes. Even so, service companies report that customers remain cautious about refrigerant-charge limits inside shafts and rooftops, which keeps retrofit penetration below potential in older tower blocks.

By Technology: Air-to-Water Leads on District Cooling Integration

Air-to-water platforms represented 51.31% of 2025 revenue and are set for a 5.02% CAGR through 2031, the quickest pace among technology groups. District-cooling networks in Marina Bay and Jurong Lake District distribute chilled water, so an air-to-water heat pump can supply both space-cooling and 60 °C domestic hot-water loads from a single shell-and-tube exchanger, cutting duplicate equipment. Air-to-air units remain common in public-housing corridors where split-unit air conditioners already populate balconies, but they lose share to hydronic systems in premium offices where owners value heat recovery. Water-to-water and ground-to-water selections, despite higher theoretical efficiencies, demand either seawater permits or boreholes that can delay projects for months, unsettling developers working on tight construction calendars.

Manufacturers now ship modular skids that fit inside constrained mechanical rooms and scale upward in 50 kW steps, an attractive feature for expansion phases in mixed-use projects. The National Environment Agency product-registration database shows a threefold increase in R290 and R1234ze air-to-water listings since 2025, confirming the technology’s compliance momentum. Engineers who specify new podium plantrooms confess the deciding factor is often spatial: one multi-service module frees enough roof for PV arrays that boost Green Mark scores, satisfying corporate net-zero declarations.

By Capacity: Mid-Range Dominates, Large Systems Accelerate

Units between 10 kW and 50 kW controlled 38.23% of the Singapore heat pump market share in 2025, reflecting standardized packaged products stocked by distributors. Mechanical contractors favor this size because it fits service elevators and does not require mobile cranes for high-rise lifts, slashing installation labor. Yet the 50-200 kW bracket will clock the fastest 4.46% CAGR on the back of district-cooling buildouts and process-heat retrofits in breweries, bakeries, and pharmaceutical plants. Sub-10 kW systems geared to single apartments lag because homeowners balk at capex, while >200 kW chillers stay niche in data centers and hospitals that demand oil-free compressors and redundancy.

Equipment suppliers such as Trane market magnetic-bearing centrifugal chillers that hit efficiencies above 5.0 under data-center loads, appealing to hyperscalers chasing a 1.2 power-usage-effectiveness ceiling. Distributors note higher quotation activity for 150 kW modular units in logistics warehouses at Tuas and Changi because those sites value scalability as e-commerce volumes fluctuate.

By Application: Domestic Hot Water Leads, Industrial Heating Surges

Domestic and sanitary hot water made up 42.82% of 2025 demand thanks to mandated energy-labels that spotlight heat-pump efficiency against electric resistance heaters. Hotels and hostels in Chinatown and Orchard Road cite 20% energy-bill reductions within one year of switching to 80 °C heat-pump boilers. Industrial and process heating will expand at a 4.63% CAGR as food and beverage plants harvest 30% to 40% energy savings during pasteurization and drying. Space-cooling growth plateaus because variable-refrigerant-flow air conditioners already saturate commercial spaces, and heating degree days are negligible in the equatorial climate.

Component firms like Alfa Laval introduced brazed plate heat exchangers compatible with R290 that tolerate the 45-bar pressures seen in high-temp applications, enabling breweries on Jalan Boiler Road to retire steam coils. Across all uses, the Singapore heat pump market size benefits when building owners monetize energy savings through sustainability-linked loans offered by DBS and UOB that tie interest margins to actual power cuts.

By End User: Residential Largest, Commercial Fastest

Residential properties delivered 55.09% of 2025 sales, principally public-housing flats where centralized systems are pre-installed in new Build-To-Order projects. Growth, however, slows because retrofit grants focus on commercial nodes, and householders seldom replace functional gas heaters early. Commercial buildings will post the swiftest 4.29% CAGR through 2031 as offices, hotels, retail centers, and data centers chase Green Mark and corporate net-zero commitments. Industrial sites lag on volume but yield high-ticket orders for 100 °C hot-water units used in pharma and semiconductor cleanrooms.

LG’s Multi V i VRF shipments to a 59,800 m² Tuas logistics center illustrate how corporate landlords import commercial-grade systems to secure Platinum Super Low Energy certification and draw premium tenants. Facility managers also favor predictive-maintenance dashboards that flag compressor wear, aligning with manpower-scarce conditions in Singapore’s technical labor pool.

By Installation: Retrofit Dominates on Policy Push

Retrofits absorbed 61.43% of 2025 turnover and retain a 4.16% CAGR forecast as the Mandatory Energy Improvement Regime penalizes inefficient chiller plants inside buildings over 5,000 m². Because new construction adds only 2% to stock annually, suppliers gear marketing toward hotel operators and mall owners scheduling phased plantroom swaps outside trading hours. New builds still specify air-to-water packages to win GoldPlus or Platinum Green Mark ratings but contribute limited absolute volume.

Centralized-cooling concessionaires such as Keppel finance turnkey plants, then charge chilled-water fees, easing capital burdens for municipal landlords.[5]Keppel Infrastructure, “Jurong Lake District District Cooling,” keppel.com Early Tengah pilots revealed pipe-sweating and floor-trenching challenges that lifted contingency budgets by up to 10%, but lessons learned are now embedded in Housing and Development Board tenders calling for industrial-grade insulation and welded stainless-steel risers.

Geography Analysis

Commercial cores in the Central Business District and Marina Bay act as anchor buyers for large-capacity air-to-water units because skyscraper owners chase premium Green Mark scores in competition for multinational tenants. HarbourFront’s 17,150-RT district-cooling retrofit, to be fully live by 2031, broadens heat-pump uptake in mixed-use waterfront estates. Jurong Lake District, planned as the second CBD, offers a clean-sheet canvas where chillers, heat pumps, and thermal tanks are embedded under podiums, minimizing rooftop congestion. Tengah, branded Singapore’s first smart town, pilots residential district cooling for 42,000 residents and interlinks rooftop chillers with the Tengeh Reservoir floating PV array for carbon-light electricity supply.

Jurong Island, Singapore's petrochemical and energy hub, presents niche opportunities for water-source and hybrid heat pumps in industrial process-heating applications, where coastal proximity enables seawater-cooled systems and the availability of process waste heat from refineries and chemical plants creates cascaded energy-recovery potential. The island’s concentration of food and beverage manufacturers, pharmaceutical producers, and precision-manufacturing facilities drives demand for reliable, high-temperature heat pumps capable of delivering 60 °C to 90 °C hot water for pasteurization, sterilization, and cleaning processes, with energy savings of 30% to 40% versus steam boilers and electric resistance heaters justifying the higher capital expenditure. However, Jurong Island’s industrial users face unique challenges including saltwater corrosion of heat-exchanger materials, stringent safety and environmental permitting for refrigerant systems, and the need for redundant capacity to ensure continuous operation in mission-critical processes, factors that favor established manufacturers with proven track records in harsh operating environments and comprehensive after-sales service networks.

The Energy Market Authority’s 2025 Electricity Demand and Supply Outlook projected peak demand rising from 8.2 GW in 2025 to 10.2 GW by 2034 under the base case, with data centers and electrified cooling contributing significantly to load growth, underscoring the geographic concentration of demand in data-center clusters such as Loyang, Jurong, and the upcoming Tuas mega data-center precinct, where hyperscale and colocation operators are specifying high-efficiency cooling systems including air-cooled magnetic-bearing chillers and water-cooled heat pumps to minimize power-usage effectiveness and comply with the Building and Construction Authority’s data-center energy-efficiency standards.

Competitive Landscape

The Singapore heat pump market shows moderate concentration. Five multinationals, Daikin, Mitsubishi Electric, LG, Carrier, and Panasonic, hold about 60% combined share, leveraging regional parts depots, accredited training centers, and catalogs that span residential water heaters to 2 MW modular chillers. Regulatory focus on ultra-low-GWP refrigerants narrows effective competition to brands able to certify R290 or R1234ze systems before the 2027 phase-down, widening their pricing latitude. Keppel Infrastructure and SP Group sit atop the district-cooling value chain, contracting 20- to 30-year concessions that lock in captive orders for OEMs.

Johnson Controls is scaling its Singapore Innovation Centre with a USD 60 million outlay to tailor data-center cooling solutions, recognizing that electricity-hungry server farms remain a semi-regulated build category.[6]Johnson Controls, “Singapore Innovation Centre Expansion,” johnsoncontrols.com Bosch’s 2025 acquisition of Johnson Controls’ residential HVAC arm shows ongoing consolidation as conglomerates hunt regional service networks and certification libraries they can redeploy across Southeast Asian capitals. Component specialists such as Alfa Laval and Copeland fill white spaces by supplying heat-exchanger plates and digital scroll compressors optimized for flammable refrigerants, allowing smaller assembly brands to leapfrog compliance hurdles.

Installer certification requirements under the Building and Construction Authority create a service moat. Distributors must field training curricula that help mechanical contractors pass examinations or risk penalties up to SGD 5,000 (USD 3,880), so manufacturers with in-house academies enjoy advantaged shelf space at local wholesalers. Competition therefore tilts toward technology leadership, lifecycle support, and policy fluency rather than head-to-head sticker-price wars.

Singapore Heat Pump Industry Leaders

Johnson Controls International Plc

Rheem Manufacturing Company

Alfa Laval AB

Daikin Industries, Ltd.

LG Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Panasonic launched the Aqua-G EVO R290 commercial propane heat pump targeting large buildings in Singapore and Southeast Asia.

- March 2026: Trane debuted the HSAG air-cooled magnetic-bearing centrifugal chiller for Asia-Pacific data centers, using R1234ze and achieving COP above 5.0.

- January 2026: SP Group secured a distributed district-cooling contract for HarbourFront Precinct covering 17,150 RT across five buildings, scheduled for full operation by 2031.

- January 2026: Johnson Controls committed USD 60 million over five years to expand its Singapore Innovation Centre and grow headcount to about 100 engineers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Singapore heat pump market as all factory-built air, water, and ground-source heat pump systems that deliver space conditioning or sanitary hot water across residential, commercial, and light-industrial premises. Equipment revenue includes indoor and outdoor units, controls, and integrated cylinders that are sold through direct, distributor, or e-commerce channels.

Scope exclusion: absorption chillers, portable AC units, and pure component sales (compressors, valves) are not counted.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Singapore-based HVAC contractors, district-cooling operators, housing board energy managers, and component suppliers. Discussions verified installed base growth, average service life, and price erosion, and they clarified how government grants actually convert into procurement budgets across HDB estates and private offices.

Desk Research

We began with national datasets from agencies such as the Building and Construction Authority, the National Environment Agency, and Singapore Customs, which reveal annual retrofit volumes, minimum COP rules, and HS-code import values. Trade association bulletins from the Asia Pacific Heat Pump Alliance and peer-reviewed papers in Applied Thermal Engineering give technology efficiency spreads that inform coefficient of performance ranges. Company 10-Ks, investor decks, and local press releases help us track selling prices and installer margins. Subscription resources in Mordor's tool kit, including D&B Hoovers for financials and Dow Jones Factiva for deal flow, round out ownership patterns. This list is illustrative; many additional public and paid references supported data gathering and cross-checks.

Market-Sizing & Forecasting

A top-down and bottom-up blend anchors the model. We reconstruct demand from housing stock counts, Green Mark certified floor area, and data-center cooling footprints, and then validate totals with sampled distributor shipment rolls and typical ASP × volume math. Key drivers, retrofit rate of pre-1995 buildings, average COP uplift, HDB Green Towns funding cadence, electricity tariff trends, and import duty movements feed a multivariate regression that projects uptake through 2030. Gaps in bottom-up evidence are bridged by applying conservative penetration assumptions derived from primary interviews before final calibration.

Data Validation & Update Cycle

Outputs pass variance tests against historical import statistics and EMA electricity-saving targets. Senior reviewers question anomalies, and updates are issued yearly, with interim refreshes when policy incentives or large infrastructure projects materially shift demand.

Why Mordor's Singapore Heat Pump Baseline Commands Reliability

Published figures often diverge because firms choose different product baskets, valuation layers, and refresh rhythms. Our disciplined scope, visible variables, and annual audit give decision-makers a traceable baseline they can replicate with modest resources.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 466.6 million (2025) | Mordor Intelligence | - |

| USD 11.5 billion (2025) | Global Consultancy A | Bundles installation labor, after-sales service, and hybrid heat-pump-chiller systems, inflating value |

| USD 18 million (2024) | Industry Database B | Uses a single customs code that omits locally assembled units and retrofit kits |

| USD 5.4 billion (2024) | Market Tracker C | Counts only split-type units yet prices them at regional average ASPs that exceed Singapore transaction levels |

The comparison shows how differing scope choices and pricing assumptions create wide swings. Mordor's transparent variables, peer-review checks, and measured ASP inputs yield a balanced market view clients can trust for planning and investment decisions.

Key Questions Answered in the Report

How large will Singapore heat-pump revenues be by 2031?

They are projected to reach USD 593.82 million, reflecting a 4.07% CAGR from 2026 to 2031.

Which technology leads unit sales today?

Air-to-water systems hold 51.31% share because they integrate seamlessly with growing district-cooling networks.

What segment shows the fastest growth through 2031?

50-200 kW capacity heat pumps will grow the quickest at a 4.46% CAGR, fueled by commercial retrofits and industrial process heat.

How do new refrigerant rules affect supplier selection?

A planned 150-GWP cap starting April 2027 pushes buyers toward brands already offering R290, R32, or R1234ze systems.

Why are retrofit projects more common than new installs?

Grants under the Green Plan 2030 and the maturity of Singapore's building stock make equipment upgrades more plentiful than greenfield builds.

What limits residential adoption?

Upfront prices around SGD 3,400 (USD 2,520) for a 60-liter unit and limited homeowner subsidies extend payback periods beyond five years.

Page last updated on: