Thailand Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

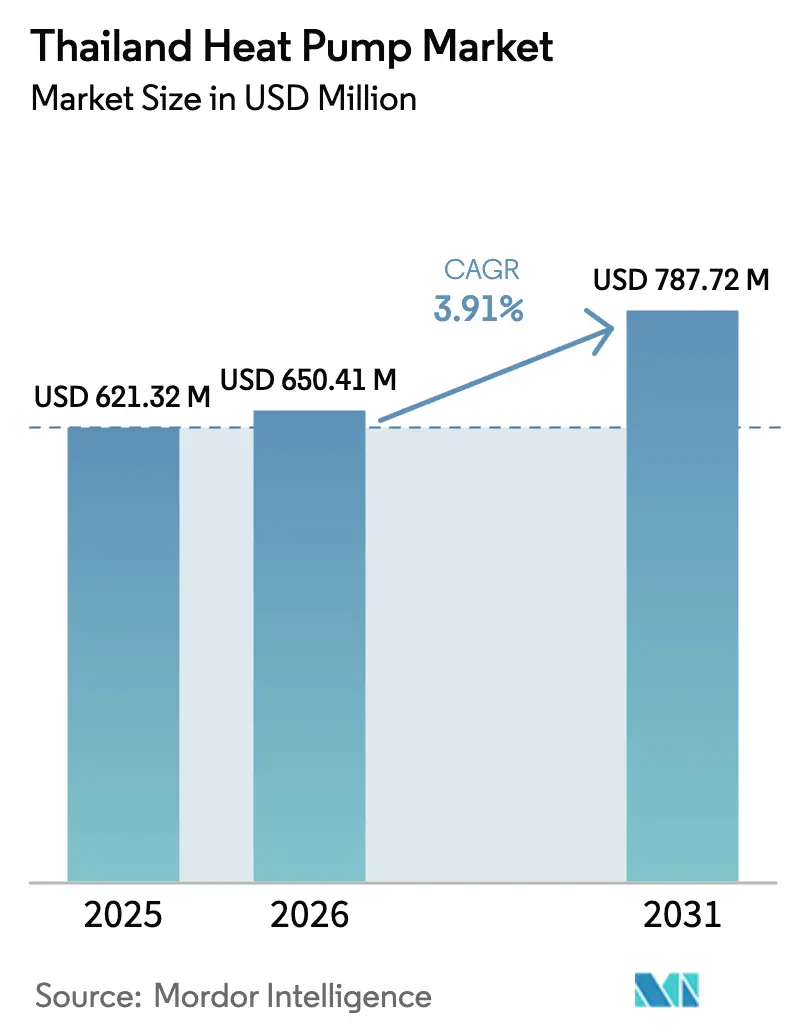

| Base Year Market Size (2025) | USD 621.32 Million |

| Market Size (2026) | USD 650.41 Million |

| Market Size (2031) | USD 787.72 Million |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Heat Pump Market Analysis by Mordor Intelligence

The Thailand heat pump market size was valued at USD 621.32 million in 2025 and estimated to grow from USD 650.41 million in 2026 to reach USD 787.72 million by 2031, at a CAGR of 3.91% during the forecast period (2026-2031). Demand is anchored in aggressive government electrification mandates, a Kigali-driven refrigerant transition, and widening time-of-use tariff spreads that improve lifecycle economics. Data-center build-outs across the Eastern Economic Corridor, five-star tax deductions for high-efficiency equipment, and Energy Efficiency Revolving Fund rebates are accelerating commercial and industrial adoption. At the same time, fragmented after-sales networks outside Greater Bangkok, volatile component tariffs, and muted consumer awareness moderate near-term growth momentum. Multinational brands continue to leverage well-established air-conditioning channels, but local integrators and lower-priced Chinese original-equipment partnerships are making in-roads among price-sensitive buyers.

Key Report Takeaways

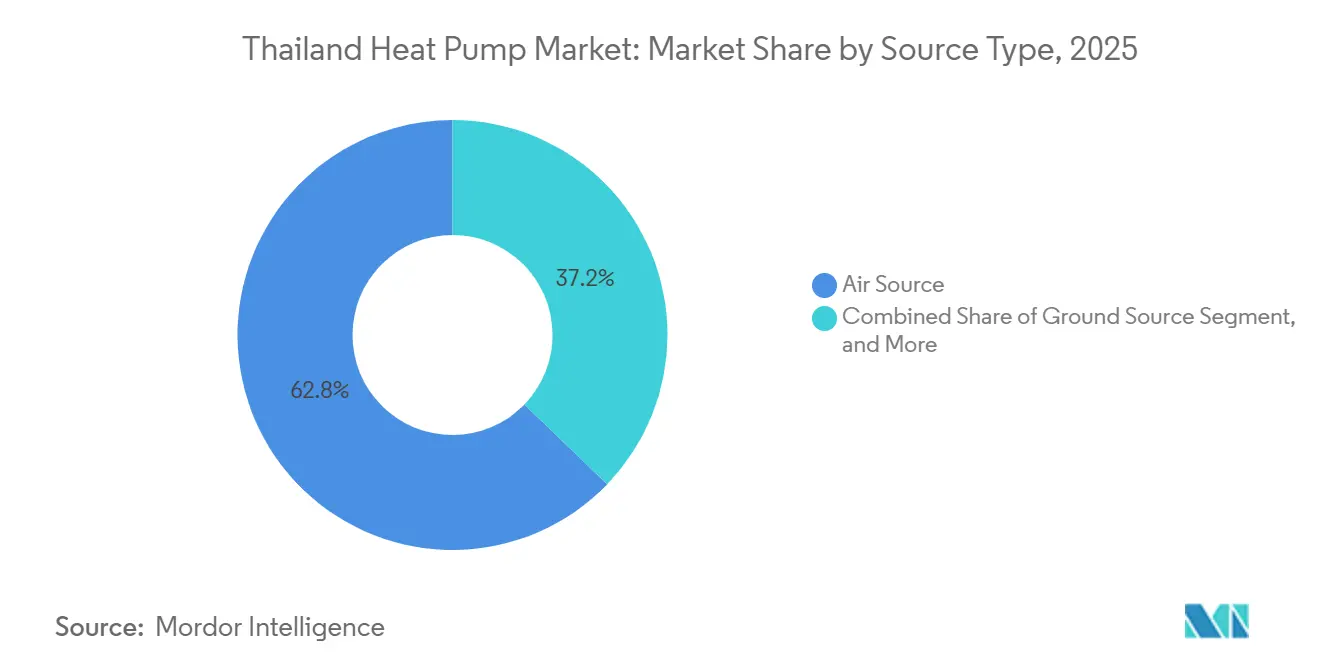

- By type, air source systems led with 62.78% of Thailand heat pump market share in 2025, while hybrid systems are on track for the fastest expansion at a 4.61% CAGR through 2031.

- By technology, air-to-water units accounted for 48.31% of the Thailand heat pump market size in 2025 and ground-to-water solutions are set to grow at a 5.02% CAGR to 2031.

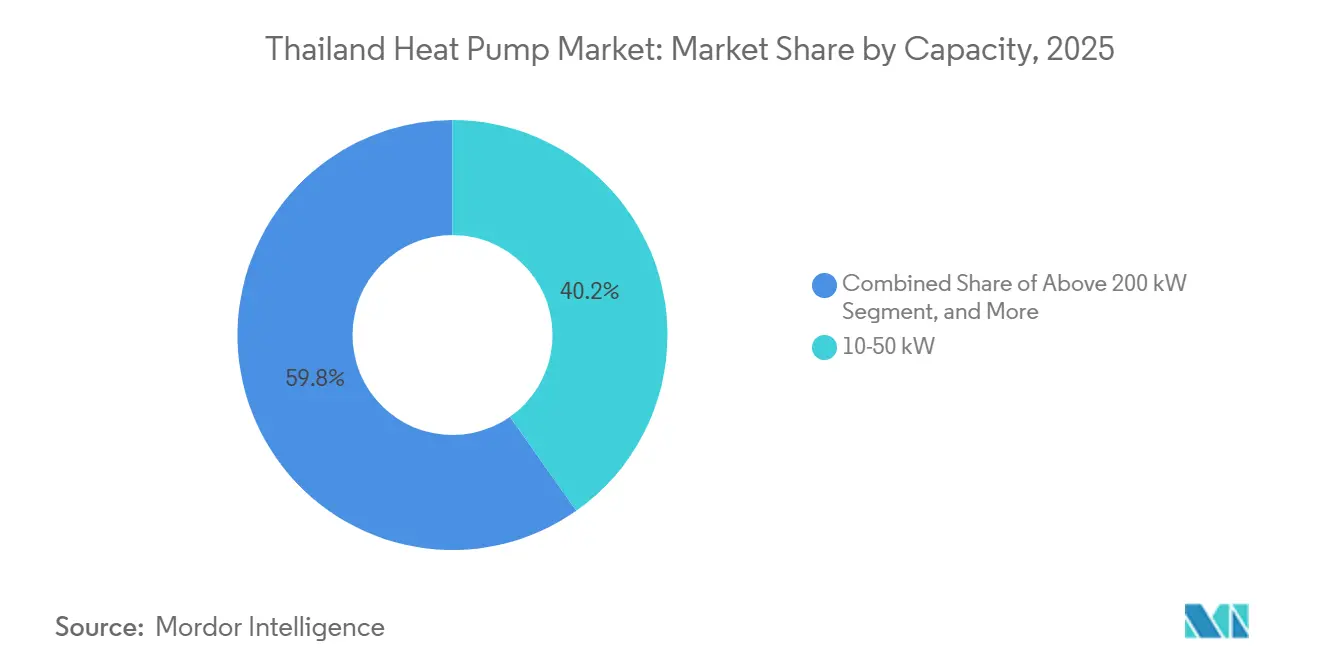

- By capacity, the 10-50 kW bracket commanded 40.23% of the Thailand heat pump market size in 2025, whereas above-200 kW installations are advancing at a 4.42% CAGR on hyperscale data-center demand.

- By application, domestic and sanitary hot-water dominated with 46.82% share of the Thailand heat pump market size in 2025, yet industrial and process heating is the quickest climber at a 4.86% CAGR.

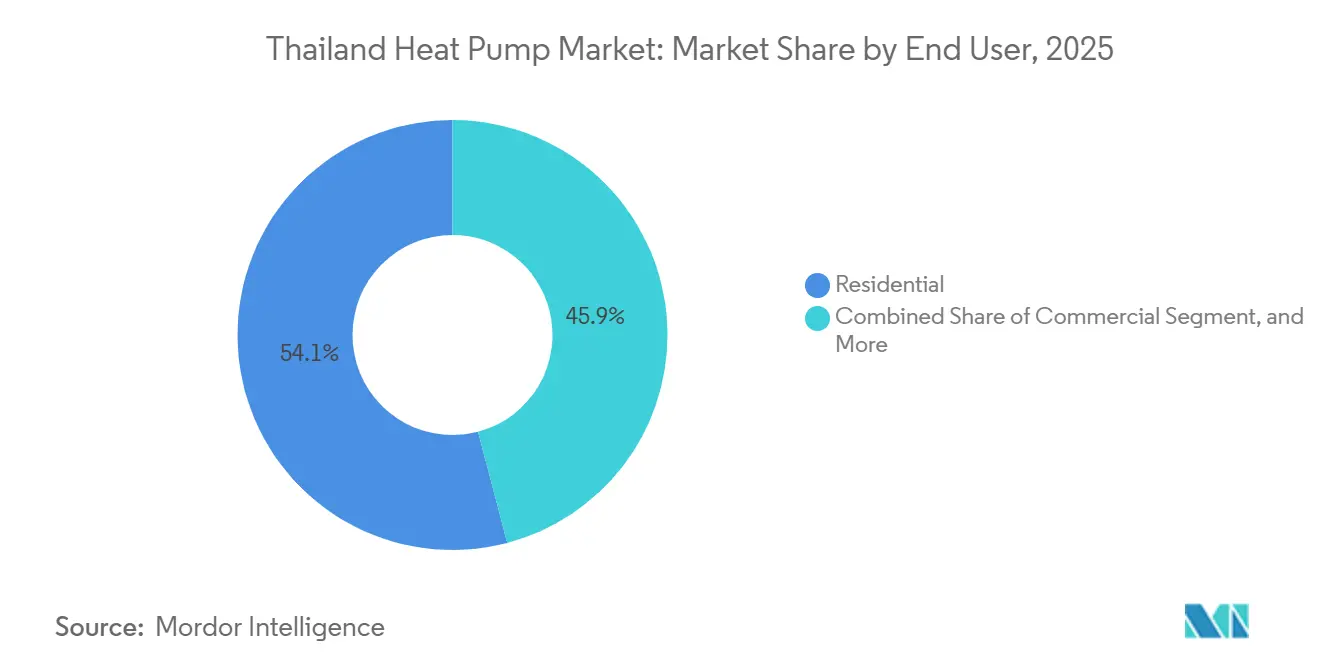

- By end user, residential customers held 54.09% share in 2025, but industrial adopters are projected to record the strongest growth at a 4.28% CAGR.

- By installation, new-build projects represented 64.43% of 2025 deployments, while retrofit activity is growing at a 4.16% CAGR as financing mechanisms mature.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Electrification Targets in Thailand's Power Development Plan | +1.2% | National, especially Bangkok and Eastern Economic Corridor | Medium term (2-4 years) |

| Extension of EGAT Time-of-Use Tariffs Favoring Heat Pump Economics | +0.9% | EGAT, MEA, PEA supply areas | Short term (≤ 2 years) |

| Energy-Efficiency Fund Rebates for Commercial Buildings | +0.7% | Greater Bangkok, provincial capitals | Medium term (2-4 years) |

| Crowding-In of Green Real Estate Investment Trusts | +0.5% | Bangkok, Chonburi, Phuket | Long term (≥ 4 years) |

| Shift Toward Low-GWP Refrigerants Mandated by Ozone Protection Act Amendments | +0.8% | National manufacturing and import channels | Short term (≤ 2 years) |

| Growth of Data Centers Requiring High-Efficiency Cooling | +0.6% | Bangkok, Chonburi, Rayong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Electrification Targets in Thailand's Power Development Plan

Thailand’s 2026-2050 Power Development Plan lifts the renewable-generation target to 51% by 2037, reinforcing policy pressure to electrify space-conditioning and process-heating loads.[1]International Energy Agency, “Thailand Electricity Demand Outlook 2024-2027,” iea.org Rising industrial electricity demand in the Eastern Economic Corridor is already stressing peak generation windows, and grid operators view heat pumps as controllable loads that can absorb overnight solar surplus. EGAT’s Energy Plus rebates link eligibility to five-star labels and smart-grid-ready controls, enabling projects such as Thai Honda Manufacturing’s 400 kW unit that trimmed natural-gas use and achieved a 2.4-year payback. Compliance with Bio-Circular-Green Economy disclosure rules further incentivizes manufacturers to switch from gas boilers to heat pumps, ensuring export competitiveness in carbon-constrained market.

Extension of EGAT Time-of-Use Tariffs Favoring Heat Pump Economics

EGAT widened the peak-to-off-peak differential to 1.8 THB (USD 0.055) kWh in 2026, cutting levelized energy costs for load-shifting heat-pump users by up to 40%.[2]Electricity Generating Authority of Thailand, “Energy Plus Incentive Program,” egat.co.th Hospitality properties have quickly capitalized; Rayavadee Krabi reported 70% hot-water electricity savings after installing more than 100 inverter units that operate almost exclusively during discounted hours. The pricing spread is also spurring a 4.61% CAGR for hybrid configurations that bypass high-tariff windows entirely, although financing models still grapple with tariff-review uncertainty beyond three-year horizons.

Energy-Efficiency Fund Rebates for Commercial Buildings

The Energy Efficiency Revolving Fund now covers up to 30% of heat-pump equipment and installation costs for non-residential buildings above 1,000 m². Projects must verify ≥ 20% savings under International Performance Measurement and Verification Protocol rules, prompting widespread engagement of certified energy-service companies. The Government Complex Bangkok leveraged the scheme to integrate radiant-floor cooling, district chilled-water loops, and on-site solar that produces 2,200 kWh daily, cutting heat gain by 37%. Although 78% of approved applications concentrate in Greater Bangkok, a Super ESCO aggregator model under pilot testing could extend benefits to under-served provinces.

Shift Toward Low-GWP Refrigerants Mandated by Ozone Protection Act Amendments

Thailand’s Kigali ratification imposes an 80% hydrofluorocarbon phase-down by 2045, accelerating the move from R410A to R32 and R290.[3]Department of Environmental Quality Promotion, “Kigali Amendment Implementation Guidelines,” depqp.go.th Daikin’s 2026 VRV 7 solution secured an A+++ rating using R32, while Johnson Controls-Hitachi rolled out R1234ze and R32 chillers tailored to Southeast Asia. Propane units demand stricter leak-detection and ventilation, adding 10-15% to installed cost, yet annual compressor-quota allocations favor domestic manufacturers such as Mitsubishi Electric’s Thai plant, strengthening local supply resilience .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Installation Cost versus Split-Type HVAC Systems | -0.8% | National, acute in price-sensitive segments | Short term (≤ 2 years) |

| Limited Public Awareness of Heat Pump Benefits | -0.5% | Provincial areas outside Greater Bangkok | Medium term (2-4 years) |

| Fragmented After-Sales Service Network outside Greater Bangkok | -0.4% | Northern, Northeastern, Southern regions | Long term (≥ 4 years) |

| Volatile Import Duties on Key Components such as Compressors | -0.3% | National import-reliant channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Installation Cost Versus Split-Type HVAC Systems

Typical 10 kW residential units cost 180,000-250,000 THB (USD 5,140-7,140) installed, three times the price of comparable split air conditioners, deterring buyers who discount future savings at double-digit rates. Specialized hydronic piping and multi-trade coordination inflate labor outlays by up to 50%. Only 12% of commercial projects in 2025 leveraged performance-based Energy Service Company contracts, as lenders demand standardized measurement protocols before underwriting shared-savings streams.[4]OECD, “Clean Energy Finance and Investment Roadmap Thailand,” oecd.org Import-duty swings of 5-10% on compressors compound budgeting risk, although local suppliers are exploring domestically sourced components to narrow the cost gap.

Limited Public Awareness of Heat Pump Benefits

A 2025 Thai Green Building Institute survey found that 68% of homeowners and 54% of small-business operators could not distinguish heat pumps from conventional air conditioning.[5]Thai Green Building Institute, “Heat Pump Awareness Survey 2025,” tgbi.or.th Marketing budgets have historically centered on solar-PV and LED campaigns, leaving heat-pump messaging underfunded. Myths about noise and complexity persist despite empirical data showing modern inverter units below 35 dB. Hotels that tout sustainability retrofits on social media spark interest among affluent travelers, yet this channel fails to reach mass-market residential customers. Absence of standardized residential Energy Performance Certificates further clouds consumer understanding and stalls broad-based uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominance Reflects Retrofit Flexibility

Air source units delivered 62.78% Thailand heat pump market share in 2025, propelled by plug-and-play installation that avoids drilling or cooling-tower tie-ins. Commercial retrofits in mid-rise Bangkok hotels underline the appeal of minimal disruption and rapid commissioning. Water- and ground-source systems together held 28%, clustered in condominiums and industrial plants where higher capital outlays are offset by efficiency gains during Thailand’s hot season. Ground-source installations, though just a niche today, are gathering momentum among luxury condominiums marketing geothermal systems as premium amenities.

Hybrid architectures are the quickest-growing slice at a 4.61% CAGR. Industrial users facing peak-tariff exposure value the redundancy of auxiliary gas or electric backup, while data centers view hybridization as a hedge against grid instability. Manufacturers are rolling out enhanced-vapor-injection compressors and variable-speed fans to keep air-source coefficient-of-performance drops below 15% even when ambient temperatures top 38 °C.[6]Stiebel Eltron (Thailand), “WWK Series Performance Data,” stiebel-eltron.co.th

By Technology: Air-to-Water Units Lead on Versatility

Air-to-water platforms captured 48.31% of 2025 revenue, serving space cooling and hot-water loads from a shared hydronic loop. Hotels and hospitals appreciate the single-plantroom footprint and consolidated maintenance contracts. Air-to-air variable refrigerant flow systems held roughly one-third share, thriving where chilled-water distribution is absent. Ground-to-water solutions are expanding at 5.02% CAGR as manufacturers seek stable year-round 40-80 °C process heat while curbing liquefied-petroleum-gas use under Scope 1 disclosure mandates.

Water-to-water designs remain niche but showcase technical frontiers: GR TECH’s HEATAQUA simultaneously produces 5 °C chilled water and 80 °C hot water for food plants, demonstrating co-generation potential. Public projects like the Government Complex Bangkok validate hydronic architectures that favor water-based heat-pump roll-outs.

By Capacity: Mid-Range Units Dominate, Hyperscale Plants Surge

Systems rated 10-50 kW secured 40.23% Thailand heat pump market size in 2025, matching loads of mid-scale hotels, restaurants, and light industry. Sub-10 kW residential heaters followed at roughly 31%, energized by five-star subsidies. Installations above 200 kW, though only a small fraction today, are climbing at 4.42% CAGR as hyperscale data-center campuses commission megawatt-scale thermal plants. Trane’s new CDU platform, scalable to 1,700 kW, underscores this trend.

Large industrial retrofits such as Honda Automobile Thailand’s 1,000 kW unit highlight paybacks below five years, yet secondary-city projects often face grid-connection delays and transformer upgrades that extend completion timelines. Developers therefore stage capacity additions alongside substation reinforcement to avoid protracted permitting.

By Application: Domestic Hot Water Leads, Process Heating Accelerates

Domestic and sanitary hot-water represented 46.82% of 2025 demand, led by hospitality properties cutting electricity outlays by as much as 70% through smart load scheduling. Space-cooling applications captured about 29%, while industrial process heating posted the fastest expansion at 4.86% CAGR as food, auto-parts, and textile plants displace gas boilers for 40-80 °C duty. CPF Thailand’s chicken-processing retrofit, registered under the Joint Crediting Mechanism, slashed 942 tCO₂ annually.

Space heating remains marginal in Thailand’s tropical climate, confined to controlled-environment farming and pharmaceutical cleanrooms. Swimming-pool heating and drying lines together held roughly 12%; PHNIX’s AI-driven R290 dryer promises 75% cost savings for fruit and seafood processors in the south.

By End User: Residential Volume vs. Industrial Value

Residential buyers supplied 54.09% of 2025 shipments, spurred by Metropolitan Electricity Authority incentives but tempered by limited awareness. Commercial facilities, hotels, offices, malls, hospitals, contributed 32% and prize lifecycle savings and certification credentials. Industrial adopters are the growth engine at 4.28% CAGR, leveraging shared-savings contracts that sidestep capital constraints while meeting export-market carbon rules. Thai Honda Manufacturing’s 400 kW deployment saved USD 154,000 annually at a 2.4-year payback.

Residential penetration outside Bangkok lags because homeowners lack Energy Performance Certificates to quantify savings and face sticker shock. Policy makers are evaluating Energy Savings Insurance to de-risk household investments, but take-up is limited to pilot projects.

By Installation: New Build Dominance, Retrofit Momentum

New construction accounted for 64.43% of 2025 volume as Building Energy Code compliance embeds heat pumps at design stage. Developers bundle systems with LEED or TREES certifications that fetch 8-12% rental premiums in Bangkok’s CBD. Retrofit installations, advancing at 4.16% CAGR, are catalyzed by preferential loans and Super ESCO aggregators that pool small projects for bulk procurement discounts.

Hospitality retrofits provide vivid case studies: Health Land Pattaya’s 24-unit rollout cut energy use 80% and served 11,000 L day of hot water. Legacy buildings, however, often require transformer upgrades or invasive hydronic piping that inflate budgets by USD 5,700-14,000 and delay schedules up to six months.

Geography Analysis

Greater Bangkok and adjacent provinces generated an estimated 58% of 2025 installations, benefiting from dense distributor networks, higher incomes, and showcase public projects like the Government Complex that produces 3.9 million kWh of solar power annually. Data-center clustering and automotive supply chains reinforce the capital’s dominance, while five-star tax incentives accelerate commercial retrofits.

The Eastern Economic Corridor, Chonburi, Rayong, Chachoengsao, ranks second as hyperscale cloud operators channel USD 5.71 billion in capacity expansion and enjoy eight-year corporate tax holidays. Industrial estates there adopt above-200 kW water-source chillers that recycle waste heat into district networks, yet seasonal water scarcity pushes operators toward air-cooled hybrids that cut water use 70-90%.

Southern tourism hubs like Phuket and Krabi are emerging hotspots; Rayavadee Krabi’s high-profile 100-unit installation spurred copy-cat projects among resorts seeking Net Zero branding. In contrast, northern and northeastern provinces lag due to fragmented service coverage and awareness deficits, 68% of homeowners remain unfamiliar with heat-pump technology. Targeted Super ESCO rollouts and mobile maintenance teams aim to bridge this regional divide.

Competitive Landscape

The top five suppliers, Daikin, Mitsubishi Electric, Johnson Controls-Hitachi, Stiebel Eltron, and LG, held a combined 52% share in 2025, leveraging broad air-conditioning channels and established service fleets. Daikin’s AI-enabled VRV 7 platform exemplifies a strategic pivot toward integrated building-management solutions. Mitsubishi Electric’s local compressor plant hedges against Kigali-quota shortages and tariff swings, reinforcing supply certainty

European specialists such as Stiebel Eltron, Viessmann, and NIBE target premium niches, with Stiebel Eltron investing USD 17.1 million to build a Thai export hub that feeds Australian and Chinese demand. Chinese entrants, PHNIX, ZenzAir, and others, compete on 20-30% lower prices while offering AI-driven R290 models that appeal to cost-sensitive small and medium enterprises.

Local integrators including Ignie, Forbest, PAC Corporation, and Leafs Heat Pump succeed through rapid service response and Thai-language technical support. Industrial process-heating retrofits and data-center district-cooling loops present white-space opportunities, yet absence of mandatory power-usage-effectiveness reporting constrains benchmarking and slows supplier differentiation.

Thailand Heat Pump Industry Leaders

Stiebel Eltron GmbH & Co. KG

Viessmann Climate Solutions SE

Glen Dimplex Group

PHNIX Eco-Energy Solution Ltd.

Vaillant Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Dhanarak Asset Development completed the Phod Duang government building in Bangkok, integrating radiant-floor cooling supplied by chilled water and on-site solar generation of 2 200 kWh day, managed via a digital-twin platform.

- January 2026: Trane introduced the DCDA Coolant Distribution Unit line for Asia-Pacific data centers, featuring 400 kW, 800 kW, and 1 350 kW bases with expansion to 1 700 kW and PUE as low as 1.1.

- January 2026: Dhanarak Asset Development expanded the Government Complex Bangkok’s green space from 36 rai to 138 rai and commissioned a district cooling plant paired with radiant flooring, reducing annual carbon dioxide emissions by over 2 000 t.

- September 2025: PHNIX launched the AI-driven i-GreenLine Ultra R290 pool heat pump claiming 30% extra energy savings and integrated propane leak-detection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Thai heat pump market as all newly manufactured, electrically driven air-source, water-source, ground-source, and hybrid units rated below and above 100 kW sold for space heating, space cooling, and sanitary hot-water service to residential, commercial, industrial, and institutional customers nationwide.

Standalone chillers, conventional air-conditioners that lack heat-pump functionality, used equipment sales, spare parts, and rental fleets are intentionally left outside the sizing scope.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Desk Research

We began with public datasets from Thailand's Energy Policy and Planning Office, the Department of Alternative Energy Development and Efficiency, and Customs Department shipment codes, then matched them with building stock statistics from the National Statistical Office and macro signals from the Bank of Thailand. Industry viewpoints were widened through open literature from the ASEAN Centre for Energy, peer-reviewed HVAC journals, and patent searches via Questel. Company filings accessed on D&B Hoovers and press releases supplied price and capacity benchmarks. These sources depict energy targets, import flows, and typical installed costs that seed our demand pool. The sources mentioned illustrate, but do not exhaust, the full list our analysts reviewed.

Primary Research

Mordor analysts interviewed Thai installers, OEM sales managers, hotel engineers, and EPC contractors across Bangkok, Chiang Mai, Rayong, and Phuket. The conversations clarified real installed prices, average seasonal COP, technician availability, and adoption triggers, letting us validate secondary numbers and plug data gaps before triangulating the final model.

Market-Sizing & Forecasting

A top-down build used household counts, commercial floor space, and industrial production indices to estimate the serviceable thermal load, which is then filtered through historical penetration rates and average replacement cycles. Select bottom-up checks, customs import volumes multiplied by sampled average selling price, and distributor channel checks keep totals grounded. Key variables tracked include electricity tariff trends, Building Energy Code 2025 compliance uptake, hotel room pipeline, average unit COP, and BOI tax-incentive utilization. A multivariate regression with ARIMA overlays generates the 2025-2030 outlook; outlier years are scenario tested for tariff or construction shocks. Gap areas in bottom-up inputs, for example, undisclosed direct OEM shipments, are bridged with conservative coefficient ranges vetted by field experts.

Data Validation & Update Cycle

Outputs pass an analyst peer review, variance checks against independent heat-pump import duties and utility tariff movements, and management sign-off. We refresh the model each year; material policy or price events trigger an interim revision so clients always receive our latest view.

Why Mordor's Thailand Heat Pump Baseline Commands Confidence

Published market values often differ because firms choose dissimilar equipment scopes, distinct price assumptions, and uneven update cadences.

Key gap drivers here include whether domestic hot-water only units are counted, how retrofit subsidies are reflected, and if analyst teams roll distributor mark-ups into sale price or not. Mordor Intelligence reports current-year outcomes rather than aggressive policy-target scenarios and is refreshed annually, which keeps our baseline realistic yet timely.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.62 B (2025) | Mordor Intelligence | - |

| USD 1.07 B (2025) | Regional Consultancy A | Includes all HVAC heat-pump capable ACs plus spare-part revenue, limited primary validation |

| USD 0.14 B (2024) | Trade Journal B | Tracks only "heat pumps other than AC machines," omits retrofit and >20 kW segments |

In short, our disciplined scope selection, dual-path modelling, and annual refresh mean decision-makers can rely on Mordor Intelligence figures as the balanced, transparent baseline for Thailand's heat-pump opportunity.

Key Questions Answered in the Report

What was the Thailand heat pump market size in 2025 and its expected value by 2031?

It stood at USD 621.32 million in 2025 and is projected to reach USD 787.72 million by 2031.

Which capacity bracket dominates installations?

Units rated 10-50 kW lead with 40.23% share, serving most mid-scale commercial properties.

Why are air-to-water systems favored in commercial buildings?

They deliver both chilled and hot water from a single plantroom, cutting equipment footprints and easing maintenance.

How is Royal Decree 805 influencing retrofit demand?

The 150% tax deduction on five-star equipment is shortening paybacks, driving a 4.16% CAGR in retrofit projects.

What restrains residential uptake outside Bangkok?

High upfront costs and limited consumer awareness, 68% of homeowners in provincial areas remain unfamiliar with heat-pump technology.

Page last updated on: