South Korea Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.09 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.84 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

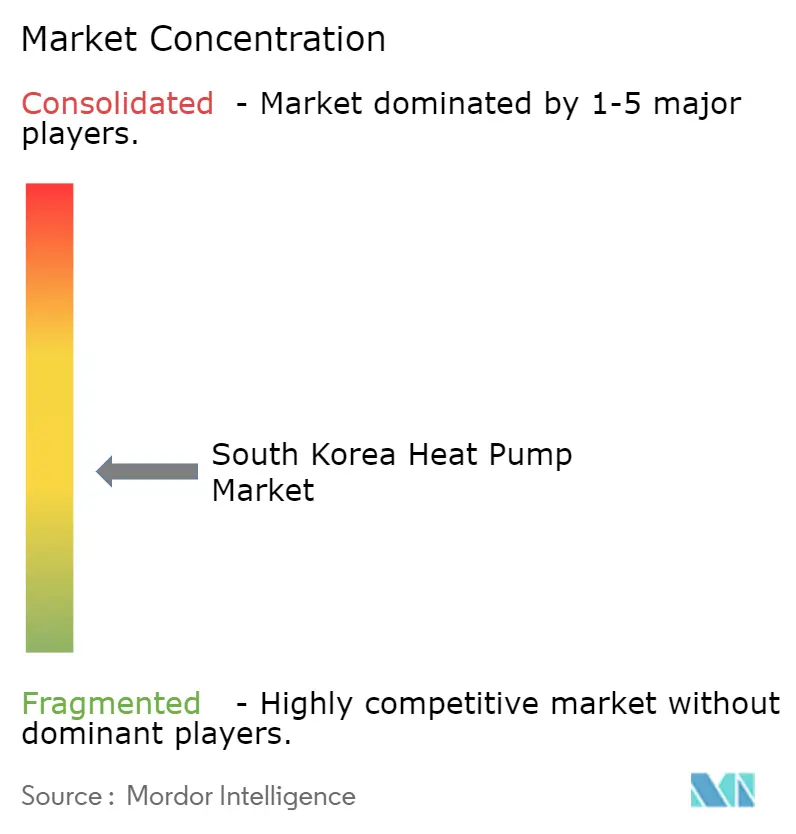

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Heat Pump Market Analysis by Mordor Intelligence

The South Korea heat pump market size was valued at USD 2.09 billion in 2025 and is estimated to grow from USD 2.21 billion in 2026 to reach USD 2.84 billion by 2031, at a CAGR of 5.14% over 2026-2031. Solid policy momentum since December 2025, a widening subsidy net and rapid electrification of detached homes on Jeju Island are combining to lift yearly unit sales well above the 2025 baseline. Manufacturers are accelerating cold-climate product launches that maintain performance at -25 °C, a feature that answers consumer anxiety over winter reliability in Seoul and Busan. Hybrid gas-plus-electric designs are gaining publicity because they hedge grid simultaneity risk during peak heating hours, while demand-response incentives are nudging owners to shift operation into daytime solar-rich windows. Fragmentation persists, yet domestic OEMs that pair equipment with integrated financing packages are starting to carve out sticky residential customer bases.

Key Report Takeaways

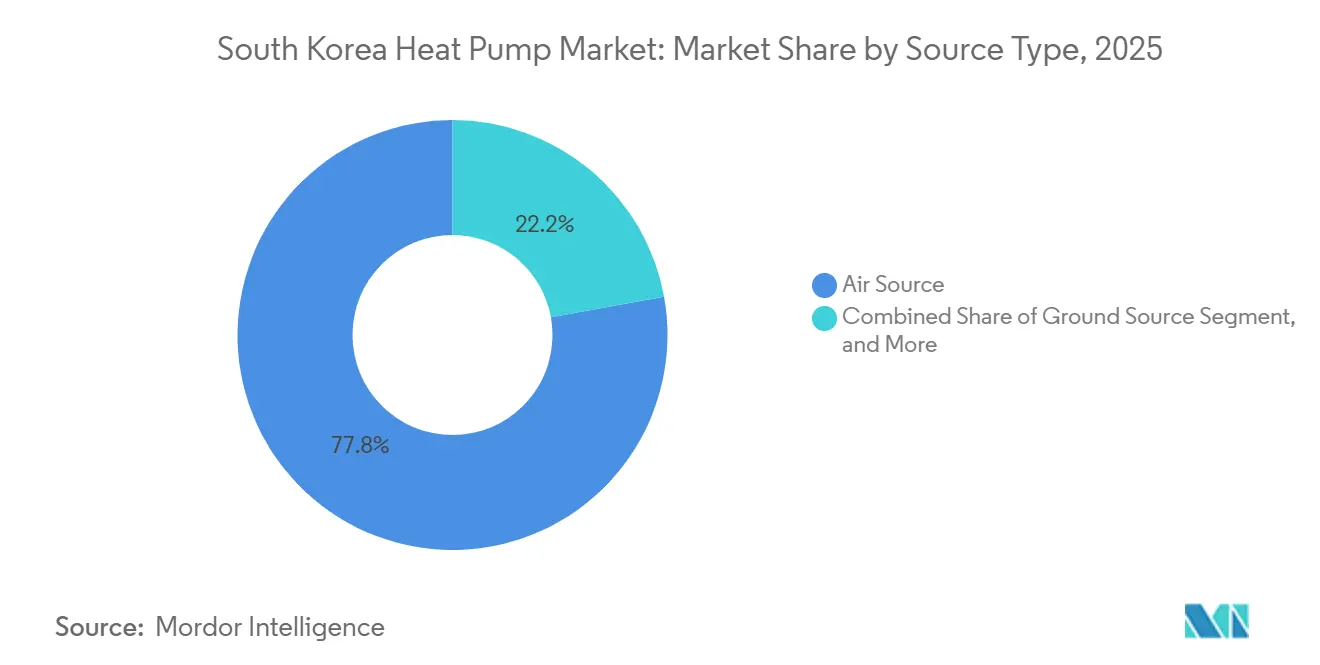

- By source type, air source systems led with 77.84% revenue share in 2025, whereas hybrid configurations are projected to post the fastest 5.72% CAGR to 2031.

- By technology, air-to-water units captured 53.91% of 2025 sales; ground-to-water variants are set to advance at a 6.03% CAGR through 2031.

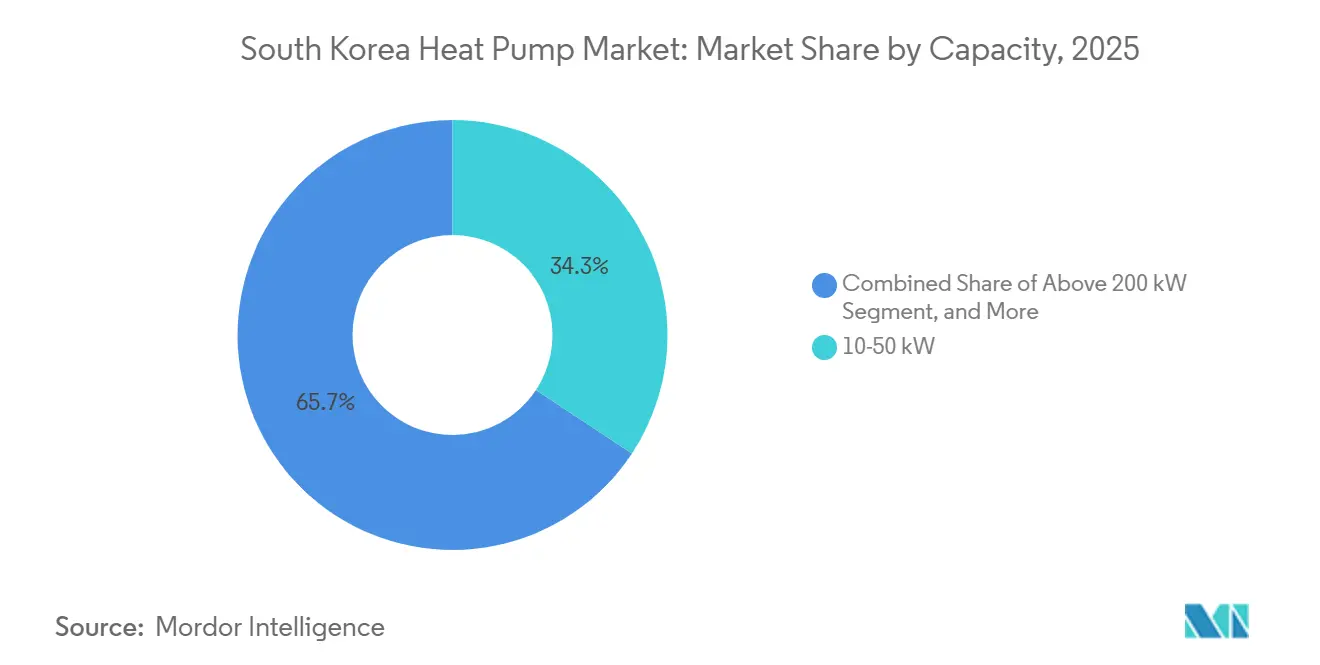

- By capacity, 10-50 kW models controlled 34.28% of 2025 demand, while sub-10 kW units are forecast to expand at a 5.86% CAGR.

- By application, space heating held 51.03% of orders in 2025; domestic and sanitary hot-water systems are on track for the quickest 5.64% CAGR.

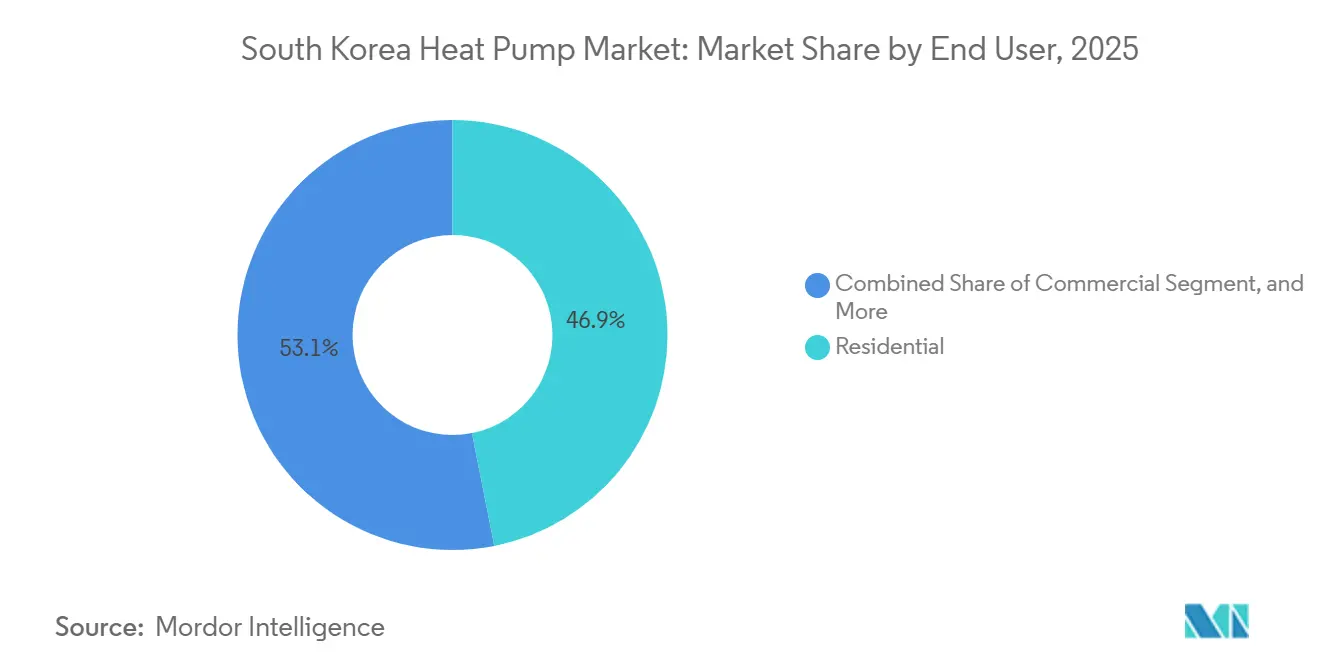

- By end user, residential buyers accounted for 46.89% of installations in 2025, yet industrial facilities will record the strongest 5.58% CAGR.

- By installation type, new-build projects represented 58.13% of 2025 shipments, but retrofit activity is expected to rise at a 5.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification Drive to Meet 2050 Carbon-Neutral Targets | +1.8% | National, early gains in Jeju and Seoul metro | Long term (≥ 4 years) |

| Aggressive Government Subsidies and Utility Rebates | +1.5% | National, strongest in rural areas and Jeju | Short term (≤ 2 years) |

| Expansion of District-Scale Apartment Retrofits | +0.9% | Seoul, Busan, Incheon | Medium term (2-4 years) |

| Integration of Heat Pumps with Hydrogen Boiler Systems | +0.4% | Industrial parks and greenhouse clusters | Long term (≥ 4 years) |

| Data-Center Waste-Heat Recovery Partnerships | +0.3% | Seoul and Gyeonggi data hubs | Medium term (2-4 years) |

| Proliferation of “All-Electric” Convenience Stores | +0.2% | Urban commercial districts nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification Drive to Meet 2050 Carbon-Neutral Targets

South Korea’s net-zero roadmap elevates heat pumps as the principal decarbonization lever for buildings, a sector that emitted around 15% of national CO₂ in 2024.[1]Min-Seong Choi, “Eco-Friendly Heat Pumps Gain Popularity in Building HVAC,” dnews.co.kr The Ministry of Climate, Energy and Environment aims to install 3.5 million units by 2035, implying annual deployments five times the 2025 volume. Jeju’s plan to electrify 100,000 homes blends rooftop solar with heat pumps, creating 1.5 GW of flexible capacity that absorbs excess daytime generation. This architecture supplies demand-response services that offset winter LNG peaker reliance. Legal recognition of ambient air heat as renewable energy in March 2026 allows installations to count toward mandatory zero-energy building quotas.

Aggressive Government Subsidies and Utility Rebates

The 2026 national budget earmarked KRW 14.45 billion (USD 10.3 million) for heating electrification, with 92.2% flowing to Jeju where each household may claim up to 70% of installed costs.[2]Ji-hye Jeon, “Jeju Allocates KRW 13 Billion for High-Efficiency Heat Pumps,” yna.co.kr Jeju Development Corporation reports that owner contributions of KRW 4.2 million (USD 3,000) can be recouped within two heating seasons thanks to energy savings of up to KRW 2.23 million (USD 1,600) per year. Pilot rent-to-own models, inspired by European heat-as-a-service schemes, eliminate upfront expense by bundling hardware and maintenance into monthly utility bill. Subsidy rules prioritize non-gasified rural zones where city-gas reach sits below 20%, easing fossil-fuel reliance.

Expansion of District-Scale Apartment Retrofits

Seoul Energy Corporation is transitioning high-rise complexes from centralized boilers to decentralized heat pumps that reuse existing hydronic loops. Korea District Heating Corporation complements the shift by integrating electric boilers and thermal storage at CHP plants to soak up off-peak renewables. Roughly 60% of urban housing was built 1990-2010, placing many systems at end-of-life and in line for mandatory efficiency upgrades. Jeju’s Geumsan-ro rental complex earned Zero Energy Building Plus certification after switching to air-to-water heat pumps paired with photovoltaics, proving retrofit viability in strata-owned blocks. Low-interest loans up to KRW 2 billion (USD 1.4 million) ease the collective investment hurdle.

Integration of Heat Pumps with Hydrogen Boiler Systems

The Korea Institute of Machinery and Materials demonstrated greenhouse heating that blends hydrogen fuel cells, solar PV and heat pumps to cut CO₂ by 58.1% versus LPG baselines. Seoul National University simulations show gas-plus-heat-pump hybrids maintaining 60 °C supply temperatures during -20 °C cold snaps with lower operating costs than pure gas. Industrial pilots in textiles and food processing adopt similar arrangements to decarbonize sub-200 °C process heat while shielding factories from volatile peak tariffs. Although green-hydrogen logistics remain nascent, dual-fuel control logic offers resilience against simultaneous grid load spikes that worry policymakers.[3]Soo-Seong Han, “Heating Cost Paradox of High-Efficiency Heat Pumps,” fnnews.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Installation Costs and Building-Code Compliance | -0.7% | Nationwide, acute in retrofits | Short term (≤ 2 years) |

| Limited Skilled Installer Base and Permitting Delays | -0.5% | Seoul, Busan, Incheon metros | Medium term (2-4 years) |

| Land Scarcity Driving Up Ground-Source Drilling Costs | -0.3% | Seoul and Busan city cores | Long term (≥ 4 years) |

| Consumer Skepticism After Early-Generation Noise Issues | -0.2% | Dense residential districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Installation Costs and Building-Code Compliance

Residential systems cost between KRW 5-15 million (USD 3,600-10,700), a hurdle even after 70% subsidies, especially in rental housing where owners pay for gear but tenants pocket fuel savings.[4]Korea Energy Economics Institute, “Analysis of Building Energy-Efficiency Market Factors,” keei.re.kr Ground-source options escalate further because drilling averages KRW 1 million (USD 715) per meter in urban bedrock. Building codes demand outdoor clearance, thermal-storage space and connectivity with virtual-power-plant platforms, adding design complexity. Hydronic loops sized for 80 °C boiler feed often need radiator upgrades when switched to low-temperature heat pumps unless high-temperature 75 °C models are specified.

Limited Skilled Installer Base and Permitting Delays

South Korea must train thousands of installers skilled in refrigerant handling and building-automation integration to hit the 3.5-million-unit goal. Fragmented local codes slow approvals, which Jeju is tackling via one-stop permitting portals and on-site verification protocols.[5]Min-Soo Oh, “Jeju Expands Heat Pump Distribution to 1,563 Households,” ihalla.com Workforce shortages are severe in rural subsidy zones, where travel premiums inflate labor costs. Industry associations plan standardized curricula and manufacturer-backed certification paths, but scaling will take several years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Shift Toward Hybrid Resilience

Air source units dominated 77.84% of 2025 demand because they install quickly and avoid drilling permits, giving the South Korea heat pump market an easy entry point in crowded city blocks. Hybrids that marry heat pumps with gas or hydrogen boilers are set for a 5.72% CAGR, reflecting industrial buyers’ desire to curtail emissions without surrendering backup capacity during rare deep-freeze events that can sap coefficient of performance. Water-source systems carve out small coastal niches where aquaculture and data centers take advantage of stable seawater temperatures. Ground-source designs are favored for public institutions that own surrounding land, yet drilling prices above KRW 1 million (USD 715) per meter in granite deter high-rise retrofits, slowing their share gain in the South Korea heat pump market.

Hybrid case studies underscore economic upside. A hydrogen-PV-heat-pump greenhouse cut CO₂ by 58.1% against LPG heating while steadying nightly temperature swings. Seoul National University’s lab work shows gas-boiler assists lifting supply temperatures above 60 °C when outdoor air drops below -20 °C, safeguarding occupant comfort. Water-source variants see earliest traction in Busan’s fish-farming belts, yet national rules for small-scale heat sales remain under review, tempering momentum. As tariff reform progresses, hybrids are likely to secure more favorable peak-price arbitrage, enhancing their value proposition in the broader South Korea heat pump industry.

By Technology: Ground-to-Water Accelerates in Process Heat

Air-to-water machines owned 53.91% of revenue in 2025 because they tie neatly into Korea’s ubiquitous radiant-floor circuits, sustaining the South Korea heat pump market share leadership. Ground-to-water models target a 6.03% CAGR through 2031 as factories and data centers adopt geothermal loops that provide 24-hour baseload temperatures without stressing the grid. Air-to-air units linger mainly in legacy ducted villas, while water-to-water packages fill specialized cooling positions in electronics plants and aquaculture tanks.

Technological refinement centers on refrigerants and installation simplicity. LG’s March 2026 R290 monobloc shifts the refrigerant circuit outdoors, streamlining retrofits in high-rise apartments and reinforcing safety as propane becomes mainstream. Samsung’s R32-based EHS All-in-One, rated for -25 °C, neutralizes cold-weather performance anxiety in the South Korea heat pump market. Ground-loop adopters benefit from stable subsurface temperatures that allow year-round coefficients of performance above 4, a critical factor for data-center waste-heat partnerships in Gyeonggi Province. Air-to-water manufacturers reply with high-temperature 74 °C outlet variants, narrowing the domestic-hot-water gap that formerly required fossil fuel backup. These moves keep the South Korea heat pump industry technologically agile while regulations phase down high-GWP refrigerants.

By Capacity: Sub-10 kW Units Ride Jeju’s Detached-Home Push

Models in the 10-50 kW band accounted for 34.28% of 2025 invoices, fitting apartment towers and mid-size commercial loads that typify Korean cities, yet sub-10 kW units will grow by 5.86% yearly as Jeju targets single-family housing electrification. The South Korea heat pump market size for small units benefits from rooftop solar synergies that soak up excess midday generation on the island’s solar-heavy grid. Systems in the 50-200 kW class serve schools, hotels and light industry, while designs above 200 kW are deployed in data centers and greenhouse complexes requiring centralized heat.

Scalability trends underscore modular thinking. Mitsubishi Electric Trane’s 40 kW CAHV modules cascade to 640 kW, letting engineering firms tailor output without oversizing single compressors. Automotive component specialist Hanon Systems crossed the 1-million-unit milestone for CO₂ compressors, a volume that can slash per-unit costs for residential heat pumps if cross-sector adoption accelerates. Sub-10 kW vendors highlight quiet operation below 55 dB(A) to satisfy dense urban codes, an attribute critical for broader uptake in metropolitan apartment balconies. The South Korea heat pump market share gains in this band hinge on streamlined permitting and installer familiarity, both advancing due to vocational training rollouts.

By Application: Domestic Hot Water Leaps on 75 °C Performance

Space heating still supplied 51.03% of 2025 demand as winter comfort dominates buyer priorities, yet domestic hot water scores the quickest 5.64% CAGR through 2031 now that high-temperature air-to-water models reach 75 °C outlet temperatures. That capability aligns with Korean bathing habits, allowing full boiler displacement without electric resistance boosters in the South Korea heat pump market. Industrial low-temperature process heat below 200 °C is another fertile field, accounting for roughly three-quarters of factory heat demand, where hybrids can cut fuel bills while maintaining steam redundancy.

LG’s Combi indoor unit packs a 200-liter stainless tank, space heating and cooling in one enclosure, shrinking mechanical-room footprints for high-rise retrofits. Mitsubishi Electric Trane’s 74 °C CAHV further narrows the performance delta to gas boilers, easing institutional conversion.[6]Lior Kahana, “Mitsubishi Electric Trane Announces New Hydronic Heat Pump,” pv-magazine.com Reversible systems that double as air conditioners add value as climate change raises cooling-degree days. Greenhouse trials mixing hydrogen fuel cells, solar PV and heat pumps suggest agricultural operations can achieve 58.1% lower CO₂ emissions while stabilizing temperature, a signal of future diversification inside the wider South Korea heat pump industry.

By End User: Industry Embraces Hybrid Economics

Residential buyers represented 46.89% of 2025 volume, yet industrial sites will post the liveliest 5.58% CAGR as factories decarbonize process heat and qualify for carbon-credit revenue streams. Time-of-use electricity pricing enables hybrid configurations to charge thermal storage at off-peak rates, then discharge during price spikes, trimming levelized heat costs by roughly 15% versus standalone gas boilers in pilot projects. Commercial properties, from retail chains to offices, bank on reversible functionality to avoid buying separate chillers.

Split-incentive issues hobble rental apartments because landlords fund equipment but tenants enjoy lower bills, perpetuating lower-efficiency choices in the South Korea heat pump market. Hotels pursuing RE100 commitments look to rooftop solar plus air-to-water heat pumps to demonstrate 100% renewable coverage in Jeju’s tourism economy. Industrial clusters in steel, textiles and semiconductors evaluate water-source or ground-loop solutions that supply 24-hour baseload temperatures without flaring peak electricity. Combined with hydrogen backup, these plants preserve resilience under extreme weather, a core purchasing criterion.

By Installation Type: Retrofits Surge as Apartments Age

New-builds captured 58.13% of 2025 shipments because zero-energy codes allow designers to optimize low-temperature hydronic layouts from day one, but retrofits will accelerate at 5.78% as apartment blocks erected in the 1990s approach mechanical end-of-life. The South Korea heat pump market size for retrofits is magnified by government loans up to KRW 2 billion (USD 1.4 million) that ease strata financing. Jeju’s Geumsan-ro project proved energy self-sufficiency over 120% once heat pumps and rooftop solar were installed, a replicable playbook for 96,000 more homes by 2035.

LG’s 2026 Hydro indoor unit cuts volume 30% by integrating valves and an expansion tank, a boon for cramped mechanical closets in high-rise retrofits. Retrofit labor complexity revolves around resizing radiators or floor circuits designed for 80 °C supply; installers increasingly specify 75 °C heat pumps to avoid expensive emitter changes. Korea District Heating Corporation’s power-to-heat pilots demonstrate how legacy CHP pipework can distribute low-carbon heat when paired with large-scale electric boilers and stratified tanks, spreading retrofit economics beyond individual buildings into district networks. Such schemes keep the South Korea heat pump market diversified across both building-level and neighborhood-scale opportunities.

Geography Analysis

Jeju Province is the undisputed front-runner, absorbing 92.2% of the 2026 national electrification budget despite housing under 2% of the population. The island’s 18.5% city-gas penetration leaves kerosene and LPG dominant, allowing heat pumps complemented by rooftop solar to slash household heating costs by up to 80% and push many homes into net-export status on sunny days. The provincial goal of 100,000 installations by 2035 foresees a 1.5 GW virtual power plant that will flatten solar curtailment midday and release stored heat at night, a blueprint now studied by other regions.

Greater Seoul, including Incheon and Gyeonggi, hosts six in ten of the nation’s high-rise apartments built before 2010, making it the largest retrofit prize in the South Korea heat pump market. Seoul Energy Corporation’s pilot conversions shift complexes off centralized boilers, yet negotiations with strata committees can delay adoption by 12-18 months. Land scarcity and granite bedrock drive ground-loop costs, pushing most projects toward air-source gear that meets voluntary 55-65 dB(A) noise guidelines. Data-center waste-heat recovery in Gyeonggi strengthens the case for water-source links that circulate warm return flows into district heating mains, unlocking year-round utilization.

Coastal Busan leverages seawater-source potential for shipyards, fish farms and waterfront hotels. Regulatory uncertainty around small-scale heat sales has slowed private investment, but municipal planners are drafting tariffs that would let industrial players monetize thermal by-products, widening the regional South Korea heat pump industry. Rural counties receive elevated subsidies because installers must travel long distances and local labor pools are thin. These territories enjoy the strongest payback because they currently burn high-priced kerosene or LPG, but workforce gaps remain a governor on acceleration until vocational programs deliver certified technicians.

Competitive Landscape

Domestic incumbents and global giants coexist without clear dominance, leaving the South Korea heat pump market fragmented. LG Electronics and Kyungdong Navien exploit intimate knowledge of Korean building codes and dense service networks, bundling low-interest financing that resonates with value-conscious households. Samsung differentiates via cold-climate engineering, promising −25 °C operation without auxiliary heaters, a pledge that attracts northern provincial buyers. Japanese and German brands such as Daikin, Mitsubishi Electric and Stiebel Eltron leverage European test data and low-GWP refrigerants to court commercial clients seeking long-run regulatory headroom.

Strategic positioning diverges sharply. LG’s R290 indoor monobloc removes indoor refrigerant lines, speeding apartment retrofits that prize minimal occupant disruption. Mitsubishi Electric Trane’s modular CAHV stack scales to 640 kW, catering to hospitals and factories that need plug-and-play redundancy. Hanon Systems, better known for automotive HVAC, hit 1 million CO₂ compressor shipments in March 2026, signaling cost-curve compression that could spill into residential heat pumps and shake price structures. Chinese manufacturers Gree, Midea and Haier have yet to enter at scale but monitor subsidy frameworks that could unlock a price-led assault.

Noise performance and refrigerant choice now act as de-facto qualifiers. Products above 65 dB(A) struggle in dense neighborhoods, while R290, R454C and R744 compliance earns favor as the government eyes GWP limits mirroring EU F-Gas rules. Energy-service companies offering subscription models enter as new channel partners, bundling equipment, installation and maintenance into a single monthly fee that demystifies ownership for cash-strapped households. Competition is therefore broadening beyond hardware to encompass finance, software and after-sales ecosystems.

South Korea Heat Pump Industry Leaders

Daikin Industries Ltd.

Mitsubishi Electric Corp.

LG Electronics Inc.

Fujitsu General Ltd.

Carrier Global Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: LG Electronics broadened its Therma V R290 monobloc line with Combi, Hydro and Control indoor variants, each delivering up to 75 °C domestic hot water while housing all refrigerant outdoors for safer apartment retrofits.

- March 2026: LG and Samsung unveiled next-generation compressors at AHR Expo 2025, emphasising fast retrofits.

- March 2026: Hanon Systems commercialised a fourth-generation EV heat-pump module first deployed in the Kia EV3, enhancing vehicle winter range.

- March 2026: Samsung acquired FläktGroup for EUR 1.5 billion (USD 1.63 billion) to accelerate its industrial HVAC footprint.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study considers every newly installed, factory-built system that transfers heat into or out of buildings in South Korea through an electrically driven vapor-compression cycle, covering air-source, water-source, and ground-source units across residential, commercial, industrial, and institutional premises. Accessories, maintenance services, window air-conditioners, and pure refrigeration equipment fall outside this scope.

Scope exclusion: stand-alone electric heaters and fossil-fuel boilers are not modeled.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and short surveys with heat-pump OEM engineers, distributor networks, energy-service contractors, and local officials across Seoul, Busan, and Jeju help us validate uptake drivers, subsidy pass-through rates, and prevailing average selling prices. Follow-up calls ensure assumptions on installation labor cost and coefficient of performance are grounded in field reality.

Desk Research

Mordor analysts first compile historic demand and price clues from non-paywalled tier-1 sources such as the Korea Energy Agency's Renewable Heat Statistics, Korea Customs Service HS-code shipment data, KOSIS building completion records, and policy papers from the Ministry of Trade, Industry and Energy. International context is taken from IEA Heat Pump Centre digests and peer-reviewed HVAC journals. Company filings, investor presentations, and press releases enrich competitor revenue splits, while paid tools like D&B Hoovers and Dow Jones Factiva supply corroborative financials. The sources listed here are illustrative; many additional materials are screened to cross-check facts and fill gaps.

Market-Sizing & Forecasting

A top-down model reconstructs 2019-24 demand by aligning local production, import, and export flows with replacement cycles and stock-turnover logic. Outputs are then cross-checked through a bottom-up roll-up of sampled supplier revenues and installer channel checks. Key variables tested include new-dwelling completions, heating-degree days, electricity-to-gas tariff differentials, government rebate budgets, average COP drift, and unit ASP trends. A multivariate regression links these drivers to shipments, while ARIMA smooths short-term shocks before projections to 2030. Any bottom-up shortfalls are bridged using calibrated penetration-rate proxies derived from primary interviews.

Data Validation & Update Cycle

Outputs pass three rounds of analyst review, variance screening against external energy-use indicators, and senior sign-off. The model refreshes annually, with interim updates triggered by material subsidy revisions or major policy announcements. A final check is run just before each report release.

Why Mordor's South Korea Heat Pump Baseline Is Widely Trusted

Published market values can diverge because firms choose different product mixes, price bases, and refresh cadences. By anchoring estimates to verified trade flows and on-the-ground rebate uptake, Mordor Intelligence minimizes hidden assumption drift.

Key gap drivers include rival studies that exclude ground-source units, apply uniform ASP escalation, or roll forward historic growth rates without testing them against housing starts and tariff movements. Our annual update cycle and double-source validation reduce these discrepancies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.11 B (2025) | Mordor Intelligence | - |

| USD 1.29 B (2024) | Regional Consultancy A | Omits retrofit segment and uses static ASP |

| USD 1.22 B (2024) | Trade Journal B | Excludes industrial heat-pump demand and assumes conservative subsidy uptake |

Differences aside, the comparison shows that Mordor's blended top-down with bottom-up check delivers a balanced, transparent baseline that decision-makers can reliably trace back to clear data points.

Key Questions Answered in the Report

How large is the South Korea heat pump market in 2026?

The market stands at USD 2.21 billion in 2026 and is on course for USD 2.84 billion by 2031.

What annual growth rate is expected through 2031?

From 2026 to 2031 the compound annual growth rate is projected at 5.14%.

Which segment grows fastest within the market?

Hybrid source systems record the quickest 5.72% CAGR thanks to their grid-resilience appeal.

Why is Jeju Province significant for heat pump adoption?

Jeju secures more than 90% of the 2026 subsidy budget and plans 100,000 installations by 2035, forming a 1.5 GW virtual power plant.

How are policy incentives structured for homeowners?

Subsidies cover up to 70% of installed cost and upcoming rent-to-own models remove the remaining upfront payment.

What technology addresses cold-climate performance concerns?

Newly launched air-to-water units from Samsung and Mitsubishi Electric sustain output at -25 °C while delivering 74-75 °C hot water.

Page last updated on: