Taiwan Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

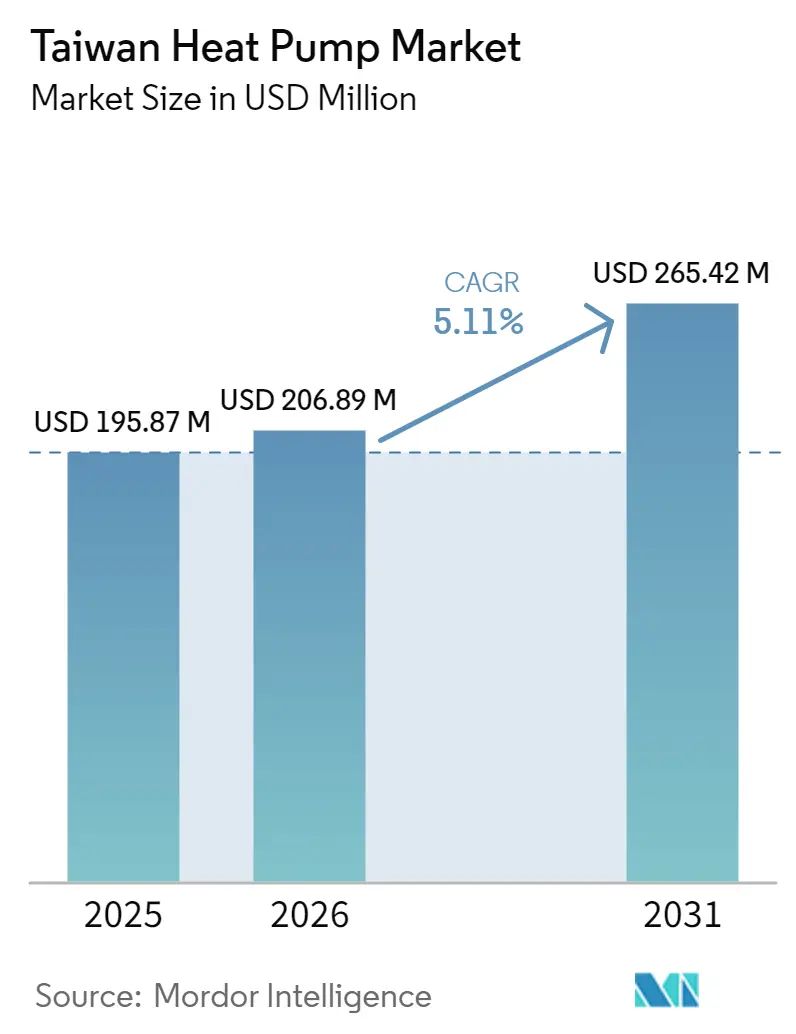

| Base Year Market Size (2025) | USD 195.87 Million |

| Market Size (2026) | USD 206.89 Million |

| Market Size (2031) | USD 265.42 Million |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Heat Pump Market Analysis by Mordor Intelligence

The Taiwan heat pump market size was valued at USD 195.87 million in 2025 and is estimated to grow from USD 206.89 million in 2026 to reach USD 265.42 million by 2031, at a CAGR of 5.11% during the forecast period (2026-2031). Robust semiconductor capital expenditure, a municipal push to phase out fuel-oil boilers, and widening electricity-to-gas price differentials are redirecting building and industrial budgets toward high-efficiency electrified heating and cooling. Industrial players now view waste-heat recovery as a hedge against soaring energy intensity, while policy-backed subsidies accelerate payback periods for mid-rise residential retrofits. At the same time, localization by Japanese and European manufacturers is tightening delivery cycles, giving large commercial buyers confidence to lock in multi-year procurement contracts. Together, these forces keep the Taiwan heat pump market on a steady, policy-anchored growth path even as grid-stability concerns linger.

Key Report Takeaways

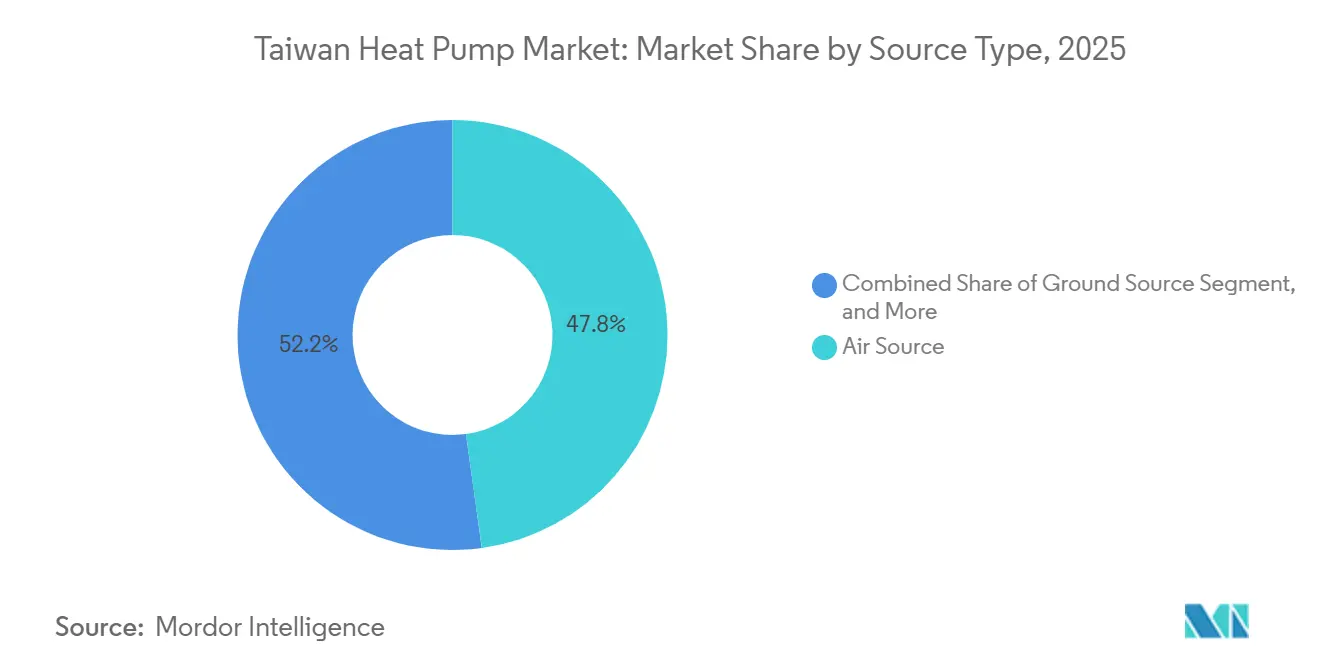

- By source type, air source systems commanded 47.83% revenue share in 2025, while water source heat pumps are advancing at a 6.23% CAGR through 2031.

- By technology, air-to-water units led with 41.62% of 2025 revenue; water-to-water configurations post the fastest 5.97% CAGR to 2031.

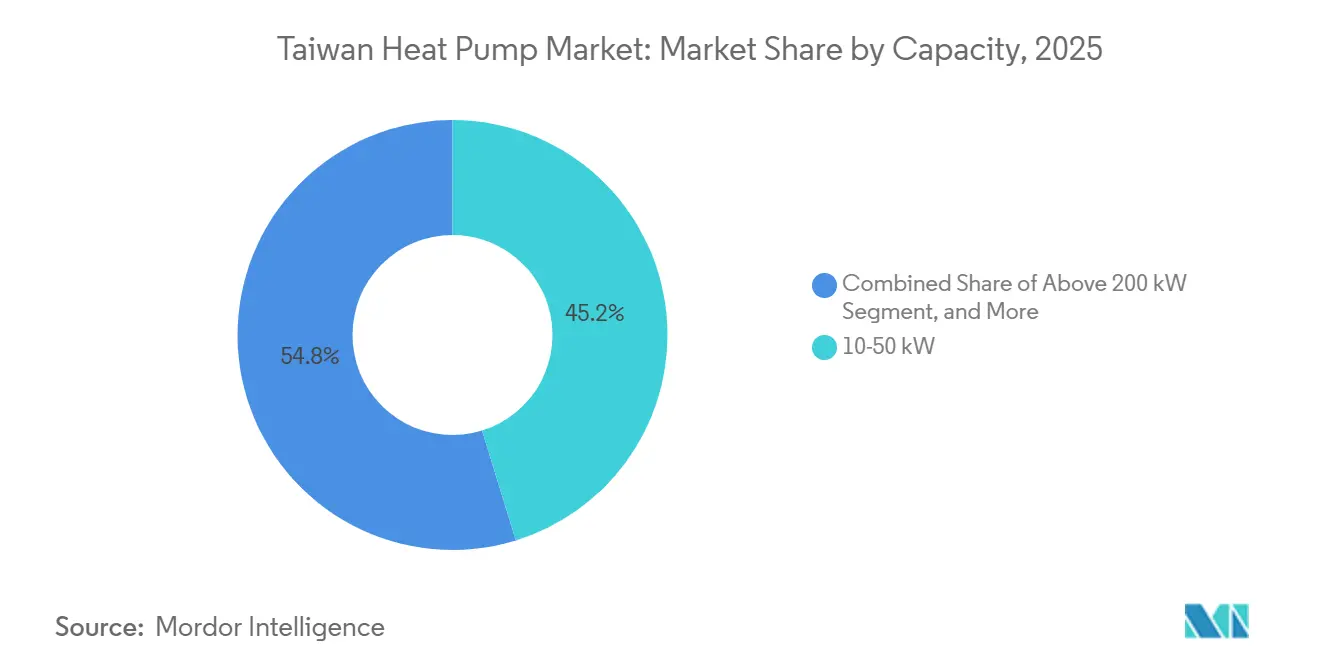

- By capacity, the 10-50 kilowatt band accounted for 45.23% of 2025 installations, yet ≥200 kilowatt units are growing at 5.67% annually.

- By application, domestic and sanitary hot-water held 43.42% share in 2025, whereas space cooling is the fastest-growing use case at a 5.86% CAGR.

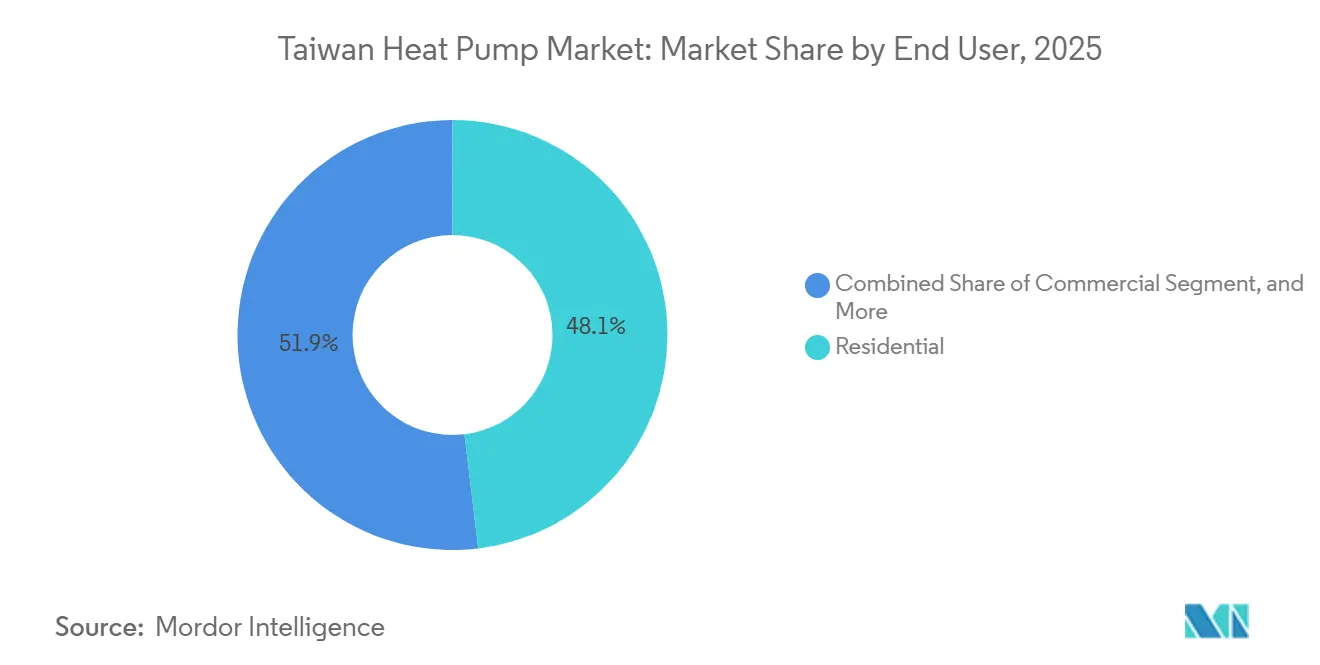

- By end user, residential customers represented 48.09% of the 2025 market, while commercial deployments are accelerating at 5.52% a year.

- By installation, new-builds captured 54.43% of 2025 shipments, but retrofits are expanding at 5.27% annually as subsidy windows narrow.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Taiwan Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuation of Green-Building Codes and Subsidies | +1.4% | Taipei, Taichung, Kaohsiung metros | Medium term (2-4 years) |

| Electrification Targets Driving Fuel Switch | +1.2% | New Taipei City, Taoyuan industrial corridors | Medium term (2-4 years) |

| Semiconductor Fabs’ Waste-Heat Recovery | +1.0% | Hsinchu, Taichung, Tainan science parks | Long term (≥4 years) |

| Data-Center Demand for Low-Carbon Cooling | +0.8% | Taipei, New Taipei, Taichung, Kaohsiung | Medium term (2-4 years) |

| Volatile LNG Imports Widen Price Gap | +0.5% | National | Short term (≤2 years) |

| Heat-Pump Drying in Food Processing | +0.2% | Yilan, Pingtung coastal zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Continuation of Green-Building Codes and Subsidies

Taiwan has extended its tax breaks and direct-purchase incentives to 2027, offering up to 50% equipment-cost coverage for commercial projects and NTD 3,000 (USD 93) per residential unit. Developers respond by front-loading 2026 procurement schedules to avoid a potential incentive gap in 2028. Compliance with ISO 50001 energy-management standards is now a prerequisite for public tenders, so design teams specify centralized heat-pump loops with supervisory controls that log kilowatt-hour savings in real time. New hydronic standards within the EEWH rating system further cement heat pumps as default equipment for mid-rise residential and Class-A office towers. As a result, incentive pull-through is shifting market demand toward larger multi-unit arrays that better exploit the per-project subsidy cap.[1]Li Ke-yen, “全國首座火山型地熱開發案 估計年發電量將達16億度,” MyHousing, myhousing.com.tw

Electrification Targets Driving Fuel Switch Away from LPG and Fuel Oil

New Taipei City’s 2030 ban on fuel-oil boilers removes a legacy technology from hotels, hospitals, and industrial laundries, forcing owners to weigh modest carbon cuts from natural-gas retrofits against full electrification via heat pumps. Propane-indexed LPG prices show higher monthly volatility than time-of-use electricity, making COP ≥ 3.0 heat pumps economically compelling even without subsidies. Amendments to Taiwan’s Electricity Act in 2025 streamlined interconnection reviews, trimming approval cycles to 90 days for projects that co-install battery storage or rooftop solar. However, shared-infrastructure hurdles in older apartment blocks slow adoption, keeping most near-term conversions focused on new construction and major gut-renovations.

Semiconductor Fabs’ Waste-Heat Recovery Requirements

TSMC and peer foundries already consume more than 12% of national electricity, and each advanced-node fab rejects 50-100 °C waste heat. Lithium-bromide absorption heat pumps boost that stream to 110-170 °C, cutting steam-boiler runtime while qualifying for renewable-energy certificates. Local governments now tie new-fab permits to energy-efficiency audits, prompting cleanroom designers to integrate cascaded heat-pump skids with wastewater warm-up loops. Daikin and Leading Electric inaugurated a Changhua County plant in 2025 to build air handlers married to Daikin chillers, slashing shipping lead-times and securing service contracts for temperature-tolerant semiconductor.[2]Narushi Nakai, “Daikin to Sell Air Conditioners to Taiwan Chip Fabs via Joint Venture,” Nikkei Asia, asia.nikkei.com

Data-Center Expansion Needing Low-Carbon Cooling Loops

Google’s equity stake in a 10 MW geothermal plant, scheduled for 2029 service, doubles Taiwan’s current geothermal capacity and supplies round-the-clock power for liquid-cooling heat-pump chillers. Local vendors Delta Electronics and Asia Vital Components now ship immersion-ready cold-plates that raise rack density from 10 kW to 50 kW, creating loads only water-to-water heat pumps can manage. Because Taiwan lacks binding power-usage-effectiveness rules or peak-pricing penalties, corporate ESG charters, rather than regulation, drive adoption of these higher-capex but lower-lifecycle-carbon systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront and Retrofit Installation Costs | -0.9% | Legacy stock in Taipei and Taichung | Short term (≤2 years) |

| Shortage of Certified Installers | -0.6% | Rural counties and offshore islands | Medium term (2-4 years) |

| Grid-Stability Concerns During Summer Peaks | -0.4% | Taoyuan and Kaohsiung industrial zones | Medium term (2-4 years) |

| Limited Local Component Manufacturing | -0.3% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Retrofit Installation Costs

Labor for split-system installs ranges from NTD 3,500 to NTD 13,000 (USD 109 to USD 406), while copper piping and high-rise rigging can push a mid-capacity retrofit to NTD 11,000 (USD 343), 30-40% above equipment cost. Commercial retrofits face plenum modifications and panel upgrades that often breach the NTD 500,000 (USD 15,620) subsidy cap, delaying investment until stakeholders receive greater clarity on the post-2027 incentive regime. Persistent material inflation, including an 18% rise in copper prices and supply tightness in R32 refrigerant, erodes installer margins on fixed-price contracts.[3]PRO360 editorial, “冷氣費用要多少?,” pro360.com.tw

Shortage of Certified Installers and Service Technicians

OSHA’s December 2025 rules lengthened certification to 60 hours plus a new field-assessment, choking technician throughput just as retrofit demand peaks. Service calls inside Taiwan’s main island cost NTD 1,200-3,000 (USD 37-94); technicians willing to reach Penghu or Kinmen levy NTD 4,000-6,000 (USD 125-187) travel surcharges, suppressing adoption in those areas. More than 40% of the workforce is over 50 years old, and vocational enrollment is shrinking, so manufacturers are racing to embed remote diagnostics that cut on-site troubleshooting, yet still cannot eliminate the need for field refrigerant charging.[4]TVBS News, “Taiwan Explores Geothermal Power for 12,000 Households,” news.tvbs.com.tw

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Water Source Gains On Industrial Thermal Integration

Air source units held a 47.83% slice of the Taiwan heat pump market share in 2025, buoyed by easier permitting and rooftop availability in dense urban cores. Water source systems, however, are lifting the Taiwan heat pump market size in fabs and data centers at a 6.23% CAGR, thanks to closed-loop towers that deliver year-round 25 °C inlet temperatures and raise real-world COP above 4.5. A second-order effect is the gradual retreat of hybrid air-source-plus-electric-heater packages, because modern enhanced-vapor-injection compressors sustain minus-25 °C heating without resistive backup. Industry trials show ground-source COP of 6.4 in Tainan’s shoulder months, yet seismic uncertainty and NTD 1,500 (USD 46)-per-meter drilling costs limit wider adoption.

Ground-coupled systems may still find traction in university campuses and industrial parks that can amortize borefield costs across multiple buildings and lock in stable thermal input for 25 years. Meanwhile, lithium-bromide absorption heat pumps, manufactured domestically, open a waste-heat-to-process-steam pathway for chemical plants, potentially doubling useful energy output relative to input heat.[5]Taiwan Heat Transfer Co., “Lithium Bromide Absorption Heat Pump,” en.thtco.com.tw

By Technology: Water-To-Water Configurations Serve High-Density Loads

Air-to-water platforms captured 41.62% of revenue in 2025, proving ideal for retrofitting apartment hydronic loops without major structural changes. Water-to-water models grow at 5.97% per year, because hyperscale data halls demand chilled-water precision and seamless tie-in with stratified thermal tanks. Mitsubishi Electric’s R290-based PUZ-WZ series now delivers 75 °C supply even at minus-15 °C ambient, giving owners a drop-in solution for radiator retrofits without upsizing emitters.[6]Mitsubishi Electric Germany, “New Air Conditioning, Ventilation and Heat Pump Program 2025/2026,” mitsubishi-les.com

Air-to-air split systems remain numerically dominant in legacy residential cooling but face gradual displacement as codes steer multifamily projects toward shared water loops that can couple with solar-PV-powered heat pumps. On institutional sites, ground-to-water arrays appeal to facility teams that favor low-maintenance, once-through borefields capable of delivering stable supply over decades.

By Capacity: ≥200 Kilowatt Units Scale With Hyperscale Infrastructure

Systems rated 10-50 kW supplied 45.23% of 2025 shipments, reflecting Taiwan’s mid-rise residential towers and boutique hotels. Installations ≥200 kW are accelerating at 5.67% as semiconductor expansions and AI-ready data centers specify modular chiller plants that enable N+1 redundancy. Daikin’s PUMY-M200 VRF platform positions itself at the tip of the 10-50 kW range by linking 12 indoor heads to one outdoor condenser, maximizing rooftop density.

Freight constraints encourage partial localization; Changhua County assembly now trims large-unit lead-times from 12 weeks to six. Capacity segmentation is blurring, because modular skids let developers start with two 100 kW frames then scale incrementally, aligning capital layout with lease-up or production ramp.

By Application: Space Cooling Accelerates Amid Grid and Climate Pressures

Space-cooling demand is reshaping the Taiwan heat pump market share as domestic and sanitary hot-water applications, while still leading at 43.42% revenue in 2025, give way to a 5.86% CAGR for reversible units that handle both cooling and mild-season heating. The subtropical climate keeps summer load profiles three times heavier than winter peaks, so asset owners select air-to-water chillers that swing seasonally without adding a second piece of equipment. Hotels replace electric resistance tanks with heat pumps to earn EEWH points, while hospitals favor high-temperature R290 models that sanitize plumbing loops without chemical dosing. Food processors trial low-temperature dryers to meet export-quality rules, cutting fuel burn 50% and improving worker safety in enclosed production halls. Heat-pump ability to ride through time-of-use tariffs with programmable start times cements its role in demand-response pilots in Taipei and Taoyuan.

Space-cooling momentum also reflects grid-stability priorities, because every kilowatt shifted from electric resistance heaters to high-COP chillers trims reserve-margin stress during midday peaks. Municipal retrofit funds let owners bundle window-unit removal, loop piping, and smart-meter upgrades in a single grant cycle, compressing disruption into one off-season. Semiconductor cleanroom operators employ water-to-water skids that capture 25 °C process waste heat and boost it to 60 °C for on-site hot-water loops, effectively zero-basing incremental gas demand. The Taiwan heat pump market size linked to process-cooling is still small, yet each hyperscale data hall installs ≥5 MW of capacity, so a few projects can move the needle quickly. Agricultural cooperatives in Pingtung now reserve floor space for modular dryers that reach 60 °C on 1.8 kW COP-3.5 units, opening a pilot channel for broader rural adoption.

By End User: Commercial Segment Pulls Ahead on Retrofit Economics

Residential buyers provided 48.09% of 2025 installations, driven by Taipei condominiums where developers pre-install split hydronic loops to gain marketing leverage. However, commercial facilities, hotels, hospitals, class-A offices, are advancing at a 5.52% annual clip because the 50% capital subsidy, capped at NTD 500,000 (USD 15,620), compresses payback into three years for multi-zone systems. Energy-service companies now bundle equipment, installation, and five-year O&M into a flat monthly fee that sits off balance sheet, removing a key hurdle for property funds. Semiconductor fabs and hyperscale data centers fall under the industrial category but account for a disproportionate flow of ≥200 kW orders, underscoring how uptime and precision trump first cost in mission-critical environments.

The market pivot to commercial retrofits follows policy and economics rather than climate alone, because LPG price volatility and the 2030 New Taipei fuel-oil boiler ban both punish combustion technologies. Hospitals adopt twin-circuit air-to-water units that deliver 80 °C return water for sterilization, replacing dual-fuel boilers that struggled with NOx compliance. Office landlords embrace smart sub-metering that passes energy savings through to tenants, raising occupancy rates and net operating income at once. Retail centers in Taichung extend mall hours into humid evenings, so owners shift from chilled-water plants to multi-split heat pumps that ramp fast when crowds surge. As a result, the Taiwan heat pump market size linked to commercial real estate is forecast to close the gap with the residential segment before 2029.

By Installation: Retrofit Momentum Builds As Subsidy Clock Ticks

New-build projects held 54.43% of 2025 shipments because architects specified heat pumps from day one, integrating them with curtain-wall shading and rooftop PV to satisfy EEWH gold targets. Retrofits, expanding 5.27% per year, now dominate contractor order books as property managers race to lock in subsidies that expire after 2027. Simple condenser swaps in mid-rise apartments take one day of crane time plus refrigerant line flush, whereas full hydronic conversions in 1990s towers require panel upgrades and drywall patching that can triple labor hours. Installers meet the timeline crunch by using quick-connect piping kits and pre-wired controllers, shaving two site visits per unit.

Policy also nudges replacement cycles: New Taipei’s boiler sunset date and fresh OSHA safety rules make owners rethink deferred maintenance, prompting cluster upgrades that pool labor scaffolding across neighboring buildings. Travel premiums keep retrofit penetration low on Kinmen and Penghu, yet a 2026 pilot offers 30% extra cost coverage for offshore counties to close that gap. Modular air-to-water skids sized at 30-40 kW can enter service elevators, eliminating costly façade penetrations on older concrete shells. Relocation fees of NTD 5,000-8,000 (USD 156-250) push owners to scrap rather than move decade-old units, accelerating the turnover rate of the installed base. As these factors converge, retrofit demand is on track to overtake new construction volumes inside the Taiwan heat pump market share after 2028.

Geography Analysis

Northern Taiwan, led by Taipei, New Taipei, and Taoyuan, concentrates more than 50% of the Taiwan heat pump market share because dense high-rises make hydronic retrofits cost-effective and because Hsinchu’s fabs procure high-capacity water-to-water skids at the design stage. The region also benefits from the deepest installer pool, so service premiums stay below NTD 2,000 (USD 62) per job, encouraging proactive maintenance that sustains long equipment life. Local governments layer extra property-tax rebates on top of national subsidies, nudging condo boards to approve central hot-water loops that replace LPG cylinders stored on balconies.

Central Taiwan, especially Taichung and Changhua, is the fastest-growing corridor as semiconductor expansion dovetails with Daikin’s Changhua assembly plant that halves eight-ton chiller lead-times. Average summer wet-bulb of 26 °C raises air-source de-rating, steering fabs toward closed-loop water source units that keep COP above 4.5 throughout June and July. Municipal grants now cover up to NTD 300,000 (USD 9,370) for projects that tie waste-heat recovery into district-energy pilots, so new industrial parks pre-install underground distribution mains. Mountain districts remain niche because seismic risk inflates drilling insurance for ground-source boreholes, yet a pilot in Guguan taps 70 °C geothermal brine to feed a 500 kW absorption heat pump for a spa resort.

Southern metros, chiefly Tainan and Kaohsiung, skew toward cooling-optimized air-to-water units because winter lows rarely dip below 15 °C, limiting the hours when space heating is needed. Google’s 10 MW geothermal agreement in Tainan promises 24/7 firm power to data-center chillers by 2029, setting a precedent for pairing deep-well resources with district chilled-water networks. Offshore islands lag because technicians charge NTD 4,000-6,000 (USD 125-187) travel surcharges, so the Ministry of Economic Affairs tests a remote-monitoring voucher that reimburses 80% of IoT gateway costs to cut manual service visits. Together, these geographic nuances illustrate why unified national forecasting still requires city-level policy tracking and why localization of manufacturing remains a strategic hedge for global brands active in the Taiwan heat pump market.

Competitive Landscape

The Taiwan heat pump market hosts a mix of global majors and local specialists. European brands Vaillant, Viessmann, and Stiebel Eltron ride premium status by shipping R290 high-temperature models into retrofit jobs that legacy air conditioners cannot handle, backed by EUR 2 billion (USD 2.1 billion) in global capacity expansion since 2016.[7]Vaillant Group press release, “Vaillant Invests up to €2 Billion,” vaillant-group.com Japanese suppliers Daikin, Mitsubishi Electric, and Panasonic leverage service networks plus semiconductor HVAC know-how, with Daikin’s JPY 800 million (USD 5.1 million) Changhua joint venture halving delivery cycles for cleanroom air handlers.

Price-competitive Chinese vendors, led by PHNIX, and Taiwanese assemblers Rechi Precision and Jin Hong Li target sub-50 kW residential and light-commercial units, undercutting European MSRP by 20-30% but conceding after-sales breadth. Emerging disruptors include energy-service firms bundling equipment, installation, and O&M into multiyear operating-expense contracts, though regulatory clarity on third-party energy sales remains pending.

Technology differentiation orbits refrigerant choice: R290 dominates high-temperature retrofits, R32 holds mainstream residential, and R454B gains ground in low-GWP mandates. Digital integration is another wedge; Mitsubishi’s MELCloud and Daikin’s chiller BMS interfaces enable predictive maintenance that trims truck rolls, a critical edge amid technician scarcity.

Taiwan Heat Pump Industry Leaders

Stiebel Eltron GmbH & Co. KG

Viessmann Climate Solutions SE

Glen Dimplex Group

WaterFurnace International Inc.

PHNIX Eco-Energy Solution Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: NIBE Group reported 2025 net sales of SEK 40.8 billion (USD 3.9 billion) and a 10.5% operating margin, crediting natural-refrigerant launches for renewed demand.

- April 2025: Mitsubishi Electric debuted its 2025-26 catalog, including the R290 PUZ-WZ air-to-water line and PUMY-M200 VRF outdoor unit.

- January 2025: Daikin Malaysia, Leading Electric, and Hotai Development inaugurated a JPY 800 million (USD 5.1 million) Changhua joint venture to supply semiconductor cleanrooms.

- January 2025: PHNIX introduced the HeroPremium inverter EVI air-to-water series with R32 refrigerant and 39 dB(A) sound profile for dense urban projects.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Taiwan heat pump market as all factory-built systems that extract ambient heat from air, water, or shallow ground and elevate it via electrically driven vapor-compression cycles to deliver space conditioning or domestic hot water across residential, commercial, industrial, and institutional premises.

Scope exclusion: gas-fired absorption and adsorption heat pumps, window AC units with heat pump mode, and chiller-based district energy loops are not counted.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Desk Research

Mordor analysts first mapped the demand pool through publicly available data sets such as Taiwan's Bureau of Energy appliance registration, customs HS-code imports, and construction completion statistics, supplemented by quarterly building permit releases from the Ministry of the Interior. Trade association white papers from the Taiwan Refrigeration and Air-Conditioning Industry Association, scholarly journals covering low-carbon HVAC, and patent trends accessed through Questel gave insight into technology uptake. Company filings, investor presentations, and reputable business press helped trace selling prices and channel margins. The sources listed illustrate the breadth of material consulted; many additional documents were reviewed to cross-check figures and terminology.

Primary Research

Telephone interviews and online surveys with installers, distributor networks, facility engineers at semiconductor fabs, and energy efficiency officials across North, Central, and Southern Taiwan validated unit mix, replacement cycles, and subsidy pass-through. These conversations filled data gaps on retrofit share and typical seasonal performance factors before the model was finalized.

Market-Sizing & Forecasting

A top-down reconstruction started with 2024 stock and shipment estimates derived from import records and local assembly volumes, which are then multiplied by sampled average selling prices to reach the 2024 value baseline. Bottom-up spot checks, manufacturer shipment disclosures and installer invoice samples, were used to sense-check totals and adjust channel mark-ups. Key variables feeding the forecast include new apartment completions, electricity to LPG price spreads, MEPS tiers, semiconductor clean room floor additions, and the MOEA subsidy budget trajectory. Multivariate regression combined with scenario analysis projects how these drivers influence annual sales; results are aligned with expert consensus on efficiency uptake and learning curve price erosion. Where bottom-up gaps remained, conservative share assumptions were applied and highlighted for review.

Data Validation & Update Cycle

Before sign-off, outputs pass a two-analyst variance check against independent metrics such as power company heat pump tariff enrollment and building energy use surveys. The report is refreshed each year, with interim updates triggered by material policy or price shocks; a final sense check takes place immediately prior to delivery.

Why Our Taiwan Heat Pump Baseline Commands Reliability

Published estimates often diverge because each firm chooses its own product mix, performance thresholds, and update cadence.

Key gap drivers include: some publishers include only ductless units or focus on air to air technology, others apply aggressive subsidy continuation scenarios, and a few translate volumes using unverified average prices or outdated exchange rates, whereas Mordor ties every assumption to traceable variables and revisits them annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 195.9 million (2025) | Mordor Intelligence | - |

| USD 185.7 million (2024) | Regional Consultancy A | Ductless scope only; no industrial usage captured |

| USD 510 million (2024) | Trade Journal B | Counts air to air units plus packaged HVAC hybrids; ASP inflated by retail mark-ups |

These comparisons show that while figures vary, Mordor's disciplined variable selection, transparent adjustments, and yearly refresh deliver a balanced baseline that decision makers can reproduce and stress test with confidence.

Key Questions Answered in the Report

What is the current Taiwan heat pump market size and how fast is it growing?

The Taiwan heat pump market size stands at USD 206.89 million in 2026 and is projected to reach USD 265.42 million by 2031, registering a 5.11% CAGR for 2026-2031.

Which capacity range sees the most installations?

Units rated 10-50 kW dominate with 45.23% of 2025 shipments because they match Taiwan's mid-rise residential and small commercial building profiles.

Why are water-to-water systems gaining traction?

Hyperscale data centers and semiconductor fabs need precise chilled-water control and easy integration with thermal storage, driving a 5.97% CAGR for water-to-water configurations.

How do subsidies influence commercial retrofits?

Commercial projects can recoup up to 50% of equipment cost, capped at NTD 500,000 (USD 15,600), leading to 3-5-year paybacks that push hotels, hospitals, and offices to accelerate retrofits before the 2027 sunset.

What limits heat pump uptake on offshore islands?

Technician shortages and NTD 4,000-6,000 (USD 125-185) travel premiums inflate service costs, discouraging adoption despite favorable renewables potential.

Which refrigerants are most common in Taiwan?

R32 dominates mainstream residential units, R290 serves high-temperature retrofits, and R454B is emerging for low-GWP compliance in upcoming product lines.

Page last updated on: