Silicone Elastomers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

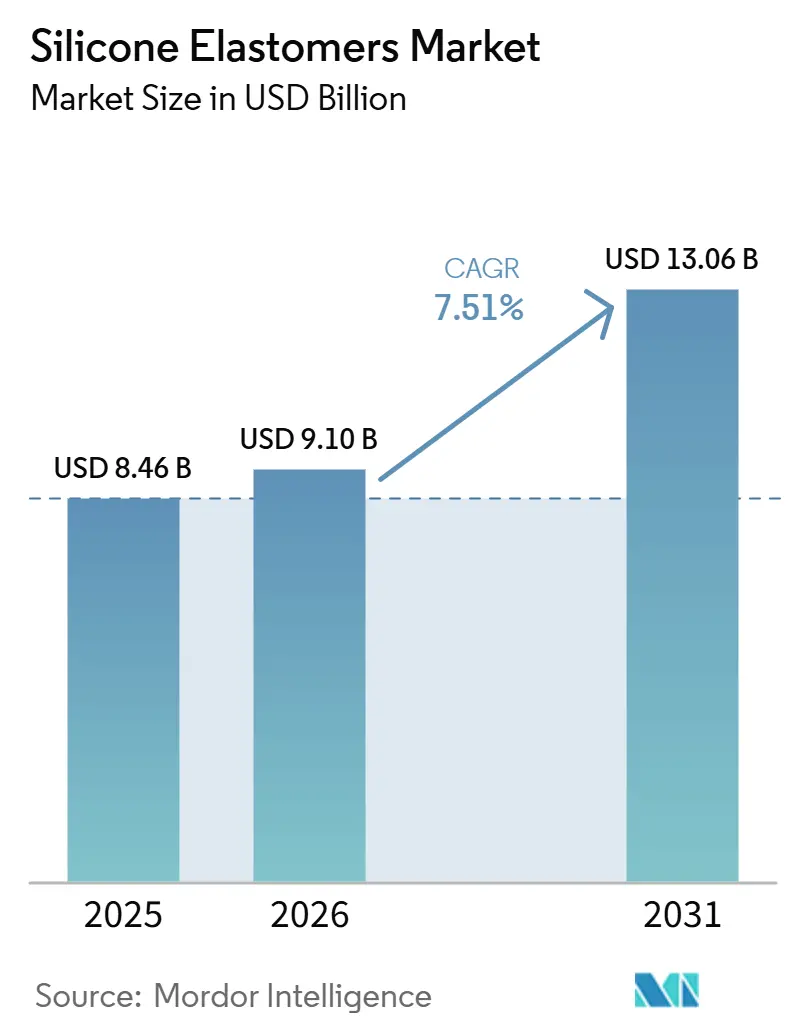

| Market Size (2026) | USD 9.10 Billion |

| Market Size (2031) | USD 13.06 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

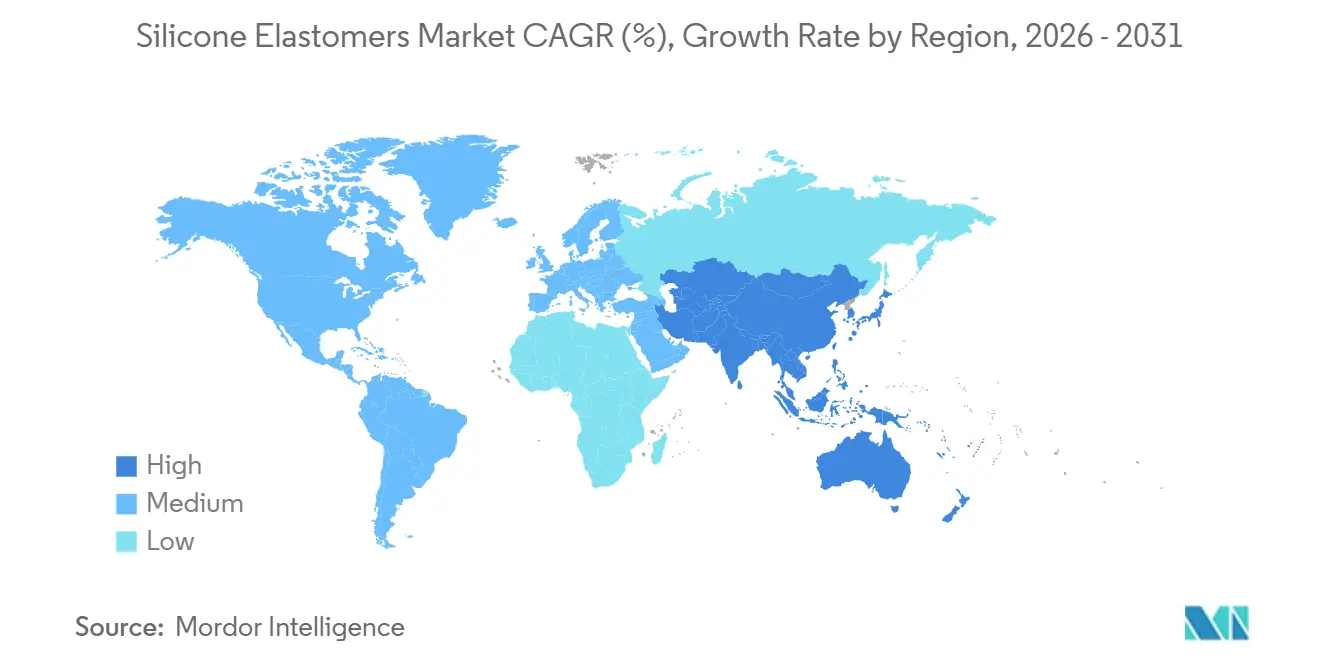

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

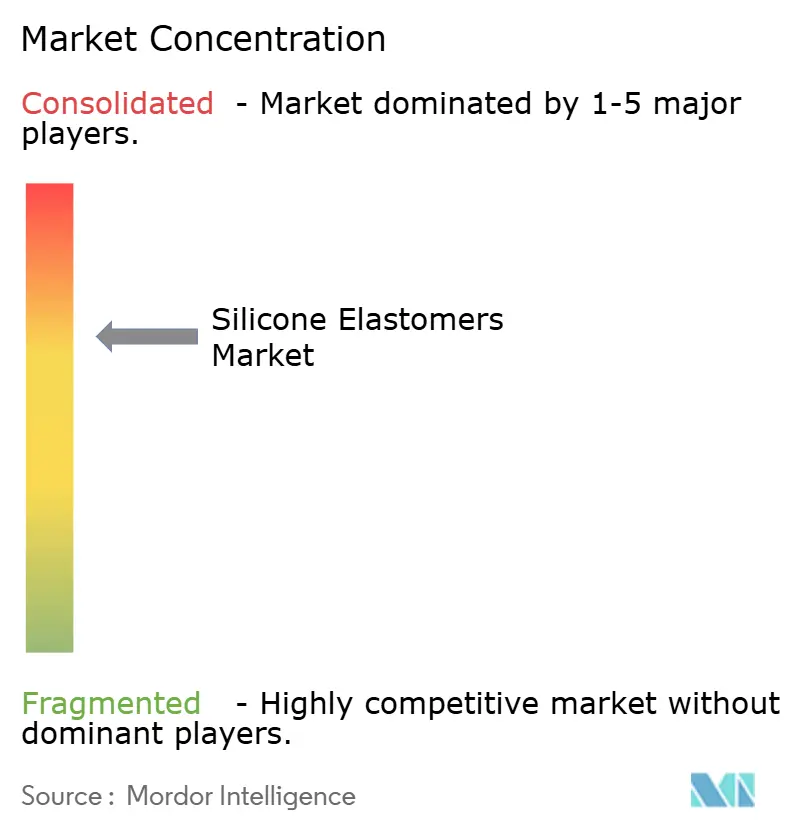

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicone Elastomers Market Analysis by Mordor Intelligence

The Silicone Elastomers Market size was valued at USD 8.46 billion in 2025 and is estimated to grow from USD 9.10 billion in 2026 to reach USD 13.06 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031). High-performance applications in electric vehicles, fifth-generation infrastructure, and medical devices are driving premium pricing for silicone grades, a position that thermoplastic elastomers struggle to challenge. Liquid silicone rubber, advanced thermal-management compounds, and medical-grade formulations are seeing heightened demand. In Europe, regulatory pressures are pushing a shift towards linear siloxanes that meet restrictions under the Registration, Evaluation, Authorization, and Restriction of Chemicals framework. While this reformulation raises raw material costs, it benefits integrated producers with control over upstream metal-silicon and dimethyldichlorosilane capacity. Non-integrated converters face challenges due to feedstock volatility, influenced by methanol supply disruptions and the significant share of siloxane intermediates controlled by specific regions. Meanwhile, additive manufacturing technologies are paving the way for custom geometries and reduced development lead times. The Asia-Pacific region stands as the epicenter of the silicone elastomer market, buoyed by trends like electronics miniaturization, data-center growth, and capacity expansions from industry giants like Shin-Etsu, Wacker Chemie, and KCC. Concurrently, advantages in vertical integration, reformulation expertise, and access to low-carbon feedstocks are becoming pivotal in the competitive landscape.

Key Report Takeaways

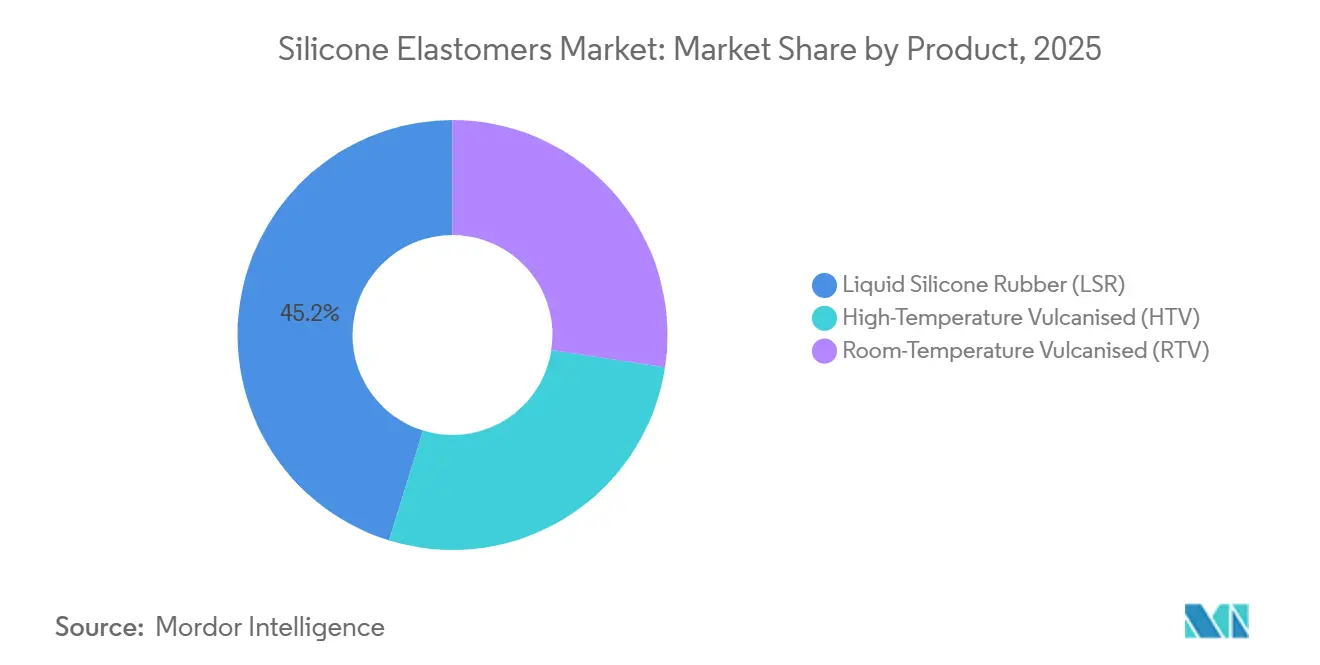

- By product type, Liquid Silicone Rubber held 45.22% of the silicone elastomer market share in 2025 and is projected to expand at an 8.34% CAGR through 2026 to 2031.

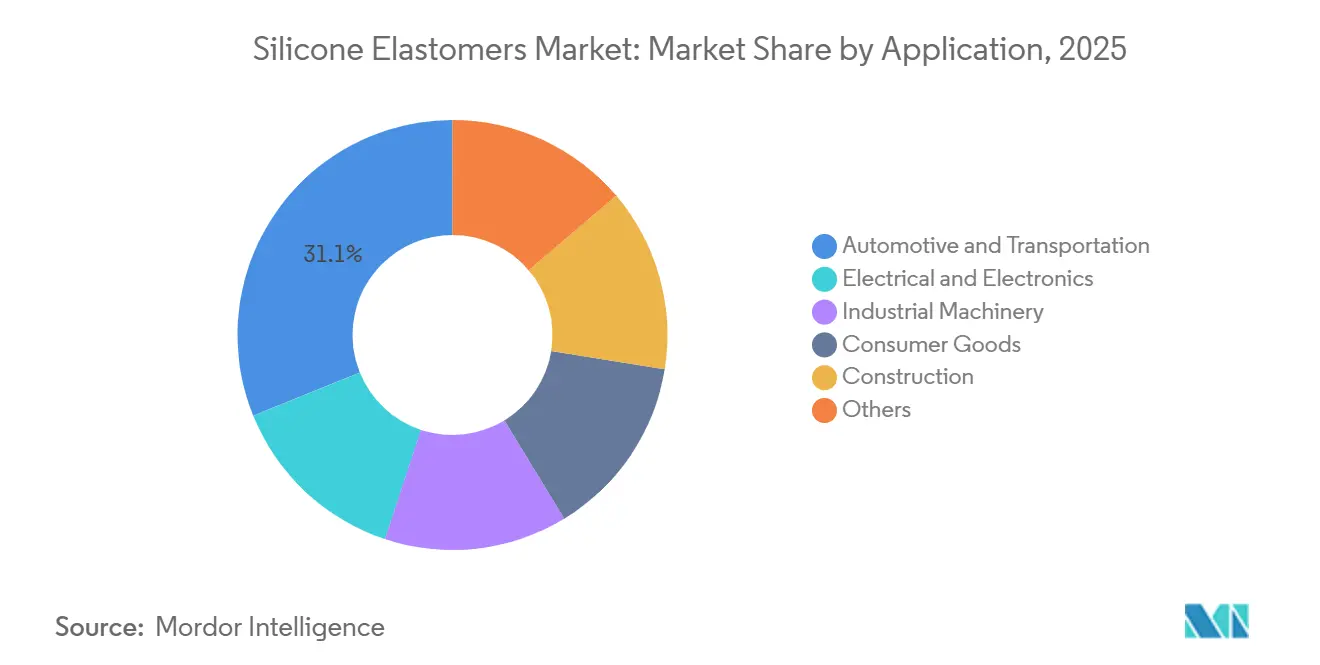

- By application, Automotive and Transportation commanded 31.13% share of the silicone elastomer market size in 2025 and is advancing at a 7.91% CAGR through 2026 to 2031.

- By geography, Asia-Pacific accounted for 46.67% of the silicone elastomer market size in 2025 and is forecast to grow at an 8.11% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silicone Elastomers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronics miniaturization and 5G thermal management | +1.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Medical-grade LSR adoption in wearable healthcare | +1.2% | North America, Europe | Medium term (2-4 years) |

| Construction sealants in net-zero buildings | +0.9% | Europe, North America, the Middle East | Long term (≥ 4 years) |

| Additive manufacturing of silicone parts | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Antimicrobial and conductive LSR | +0.8% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electronics Miniaturization and 5G Thermal Management

As the demand for higher power densities increases in fifth-generation base stations and artificial intelligence accelerators, the requirement for silicone thermal-interface materials with advanced conductivity has become critical. Dow's DOWSIL TC-5550 and Wacker's SEMICOSIL 9649 TC meet these requirements. Additionally, these materials ensure excellent electrical insulation and can withstand a wide range of temperature cycles[1]Dow Inc., “DOWSIL Thermal Management Portfolio,” dow.com. By substituting alumina fillers with boron nitride and graphene, manufacturers have significantly reduced thermal resistance. This development supports the adoption of passive cooling solutions in both compact consumer electronics and automotive electronics. Meanwhile, Shin-Etsu has established a new facility in Pinghu, China. This line is specifically designed to meet the stringent ionic purity standards essential for semiconductor packaging, highlighting the region's growing importance in the high-purity supply chain.

Medical-Grade LSR Adoption in Wearable Healthcare

Manufacturers are transitioning from thermoplastic elastomers to liquid silicone rubber for devices like continuous glucose monitors, cardiac patches, and drug-delivery systems. Liquid silicone rubber not only complies with ISO 10993 standards but also allows for extended skin contact without irritating. DuPont introduced its Liveo C6-8XX series, offering a range of hardness and an extended pot life, significantly reducing molding downtime on automated lines. Meanwhile, Elkem's SILBIONE liquid silicone rubber EC 70 incorporates carbon-nanotube conductivity, enabling the creation of dry electrodes for electrocardiogram patches. This innovation eliminates the need for pre-use skin preparation and streamlines clinical workflows.

Construction Sealants in Net-Zero Buildings

In Leadership in Energy and Environmental Design Platinum projects, silicone sealants, known for their long service life and minimal thermal expansion, significantly reduce façade maintenance costs. Dow has achieved carbon-neutral certification for select sealant grades, enabling architects to earn emissions credits under Scope 3. Momentive’s SilPruf SCS9000 and Sika’s Sikasil WS-605 S, both compliant with ultra-low volatile organic compound thresholds and stringent weathering standards, are expected to be specified in numerous net-zero towers across Europe and the Middle East in the near future.

Additive Manufacturing of Silicone Parts (3-D/LAM)

Liquid additive manufacturing significantly reduces tooling costs and shortens lead times for intricate gaskets and diaphragms. Elkem’s AMSil 20503 produces parts with Shore A hardness and high elongation, comparable to conventional liquid silicone rubber properties. Meanwhile, KL Technik’s FlexSiliconAdditive enables the creation of multi-durometer seals designed for aerospace fuel systems. While adoption has been strong in aerospace and medical prototyping, it is now expanding into industrial machinery due to improvements in printer throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Siloxane feedstock supply-chain volatility | -1.1% | Europe, North America | Short term (≤ 2 years) |

| Substitution risk from high-performance TPEs | -0.6% | Global, automotive, and consumer goods | Medium term (2-4 years) |

| EU REACH cyclic-siloxane restrictions and reformulation | -0.9% | Europe, export-oriented Asia-Pacific producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Siloxane Feedstock Supply-Chain Volatility

Metal silicon prices experienced a significant increase from the beginning to the latter part of the year. This rise was driven by disruptions in methanol supply from Iran and an explosion at a plant in Shandong, which collectively reduced the production capacity of dimethyldichlorosilane. Non-integrated European converters faced a notable decline in margins, while a company with upstream integration benefited from reduced feedstock costs and achieved a recovery in operating profit.

EU REACH Cyclic-Siloxane Restrictions and Reformulation

European regulations mandate that D4 levels in industrial and leave-on formulations must remain below a specified threshold. While linear siloxane replacements provide an alternative, they are more expensive and result in slower cure rates. In response to these regulatory changes, Wacker Chemie has incurred significant re-validation expenses. At the same time, smaller compounders are shifting their focus, discontinuing non-compliant product lines, and consolidating their market share within the industry's top-tier[2]European Chemicals Agency, “Cyclic Siloxane Restrictions,” echa.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Liquid Silicone Rubber Extends Lead in Precision Molding

Liquid Silicone Rubber captured 45.22% silicone elastomer market share in 2025, and its slice of the silicone elastomer market size is forecast to widen at an 8.34% CAGR through 2026 to 2031. With a low viscosity, automated injection cycles can be completed quickly, achieving precise tolerances. This precision is vital for high-volume wearables and sensors in electric vehicles. DuPont’s Liveo C6-8XX and Elkem’s conductive SILBIONE liquid silicone rubber showcase functional enhancements that maintain the competitive edge of liquid silicone rubber. High-temperature vulcanized grades are crucial for applications demanding high service temperatures or significant tear strength, such as in turbocharger hoses and wire insulation. Meanwhile, room-temperature vulcanized silicone is preferred for on-site construction sealants, curing at ambient conditions and boasting ultra-low volatile organic compound emissions.

Liquid silicone rubber's growing prominence is evident in consumer products. Items like bottle nipples, baking mats, and personal-care brushes benefit from liquid silicone rubber's compliance with food-grade standards, ensuring taste neutrality and durability through autoclaving. Ceramifying liquid silicone rubber, exemplified by Wacker ELASTOSIL R 531/60, is now safeguarding electric vehicle busbars from thermal runaway, highlighting silicone's pivotal role in the safety of next-generation batteries.

By Application: Automotive Electrification Accelerates Thermal-Management Demand

Automotive and Transportation accounted for 31.13% of the 2025 demand and will add a 7.91% CAGR through 2026 to 2031. The silicone elastomer market is set to witness significant growth. In the realm of electric vehicles, battery packs are increasingly turning to advanced materials. These include high-voltage seals, flame-retardant liquid silicone rubber potting, and thermally conductive adhesives. Notably, Sika's Sikasil AS-110 is making waves. This adhesive not only replaces traditional mechanical fasteners but also streamlines assembly lines, significantly reducing time. Freudenberg's silicone gaskets, on the other hand, are achieving impressive helium leak rates, a feat that supports their long-term warranties, as reported by FST.COM. In the semiconductor realm, specialized elastomers are safeguarding radar and LiDAR modules, ensuring they operate seamlessly across a wide temperature range, all while maintaining the integrity of millimeter-wave signals.

While the Electrical and Electronics sector may be smaller, it is rapidly growing, fueled by fifth-generation network rollouts and the cooling demands of artificial intelligence data centers. DOWSIL's TC-3035 S, with its high conductivity, is specifically designed for power amplifiers that dissipate significant heat. Meanwhile, Shin-Etsu's ultraclean production lines are delivering ionic silicones with extremely low levels, catering to the needs of advanced packaging. In industrial machinery, silicone diaphragms are proving their worth. With a low compression set after enduring high temperatures, these diaphragms ensure extended maintenance intervals.

Geography Analysis

Asia-Pacific dominated the silicone elastomer market with a 46.67% share in 2025 and is projected to compound at 8.11% through 2026 to 2031. Shin-Etsu's investment in its Pinghu plan and Wacker's expansion at Zhangjiagang are strategically timed with the burgeoning electronics and electric vehicle sectors in China, India, and Southeast Asia. Thanks to policy-driven consolidation in China, utilization rates are projected to significantly increase, tightening upstream supply and bolstering pricing power.

North America secured a notable share of the market. DuPont’s Hemlock site in Michigan is ramping up production of medical-grade liquid silicone rubber to cater to the biopharmaceutical sector's single-use needs and the growing wearables market. Simultaneously, United States data-center constructions are increasingly opting for silicone seals, crucial for enduring sub-ambient glycol loops. Meanwhile, Mexico's automotive nearshoring trend is pulling silicone compounding operations closer to vehicle assembly hubs, bolstering the region's economic resilience.

Europe, holding a significant market share, is witnessing modest growth. However, regulatory constraints are inflating reformulation costs. Despite this, the continent's commitment to net-zero building codes and a push towards automotive electrification are keeping demand robust. Notably, Sika's Sikasil WS-605 S is being utilized in numerous net-zero towers currently under construction. Yet, with Dow planning to shutter its Barry, United Kingdom site, the local merchant siloxane supply is set to tighten, nudging converters to seek integrated sources in Asia.

South America and the combined regions of the Middle East and Africa account for a smaller portion of global silicone consumption. Brazil's push towards electric vehicles and Saudi Arabia's ambitious NEOM megaproject are emerging as significant growth areas, capitalizing on silicone sealants renowned for withstanding the desert's scorching heat and abrasive sand.

Competitive Landscape

The Silicone Elastomers Market is moderately concentrated. Dow is reducing its operations in Europe, while both Shin-Etsu and Wacker are expanding in the Asia-Pacific, highlighting their distinct regional strategies. Elkem divested its silicones unit to China National Bluestar, bolstering China's upstream dominance and eliminating a European competitor. Technology is a key differentiator: Wacker's SEMICOSIL 9649 TC, with high thermal conductivity, and Dow's DOWSIL TC-5550, with even greater thermal conductivity, are making inroads in the electric vehicle inverter and artificial intelligence server cooling markets. Regulatory certifications such as ISO 13485 and REACH Substances of Very High Concern heighten entry barriers, pushing smaller converters to specialize in niche areas such as antimicrobial, conductive, or additive-manufacturing grades.

Silicone Elastomers Industry Leaders

Dow

Elkem ASA

Momentive

Shin-Etsu Chemical Co., Ltd.

Wacker Chemie AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DuPont launched the Liveo C6-8XX USP Class VI LSR range for wearable and short-term implant devices.

- October 2025: Elkem introduced SILBIONE LSR EC 70, combining antimicrobial silver ions and conductive carbon nanotubes for hygienic electronics.

Global Silicone Elastomers Market Report Scope

Silicone elastomers are versatile synthetic polymers derived from silicone, combining flexibility, durability, and resistance to extreme temperatures, chemicals, and UV radiation. They are formed through vulcanization processes, producing materials with rubber-like properties suitable for diverse applications. Widely used in electronics, automotive, healthcare, construction, and consumer goods, silicone elastomers provide excellent electrical insulation, biocompatibility, and long-term stability, making them essential in advanced industrial and everyday products.

The Global Silicone Elastomer Market is segmented by product, application, and geography. By Product, the market is segmented into high-temperature vulcanized (HTV), room-temperature vulcanized (RTV), and liquid silicone rubber (LSR). By Application, the market is segmented into electrical and electronics, automotive and transportation, industrial machinery, consumer goods, construction, and others. The report also covers the market size and forecasts for the Global Silicone Elastomer Market in 22 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| High-Temperature Vulcanised (HTV) |

| Room-Temperature Vulcanised (RTV) |

| Liquid Silicone Rubber (LSR) |

| Electrical and Electronics |

| Automotive and Transportation |

| Industrial Machinery |

| Consumer Goods |

| Construction |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product | High-Temperature Vulcanised (HTV) | |

| Room-Temperature Vulcanised (RTV) | ||

| Liquid Silicone Rubber (LSR) | ||

| By Application | Electrical and Electronics | |

| Automotive and Transportation | ||

| Industrial Machinery | ||

| Consumer Goods | ||

| Construction | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current silicone elastomer market size and projected CAGR to 2031?

The silicone elastomer market size stands at USD 9.10 billion in 2026 and is forecast to reach USD 13.06 billion by 2031, registering a 7.51% CAGR.

Which product segment leads global consumption?

Liquid Silicone Rubber leads with a 45.22% share in 2025 and is projected to advance at an 8.34% CAGR through 2031.

Why is Asia-Pacific so dominant in consumption?

Asia-Pacific hosts concentrated electronics and automotive manufacturing, numerous capacity expansions, and supportive government programs, giving it 46.67% share in 2025 and the fastest regional CAGR at 8.11%.

How are REACH regulations affecting European demand?

REACH restrictions on cyclic siloxanes are pushing reformulation costs up 15-20% and favoring integrated suppliers, yet net-zero building and EV initiatives keep European demand positive.

What strategic moves are leading players making?

Firms such as Elkem are divesting to consolidate Chinese capacity, Shin-Etsu and Wacker are investing in Asia-Pacific lines, and DuPont is rolling out medical-grade LSR ranges to secure higher-margin niches.

Page last updated on: