Silicone Additives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 2.98 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

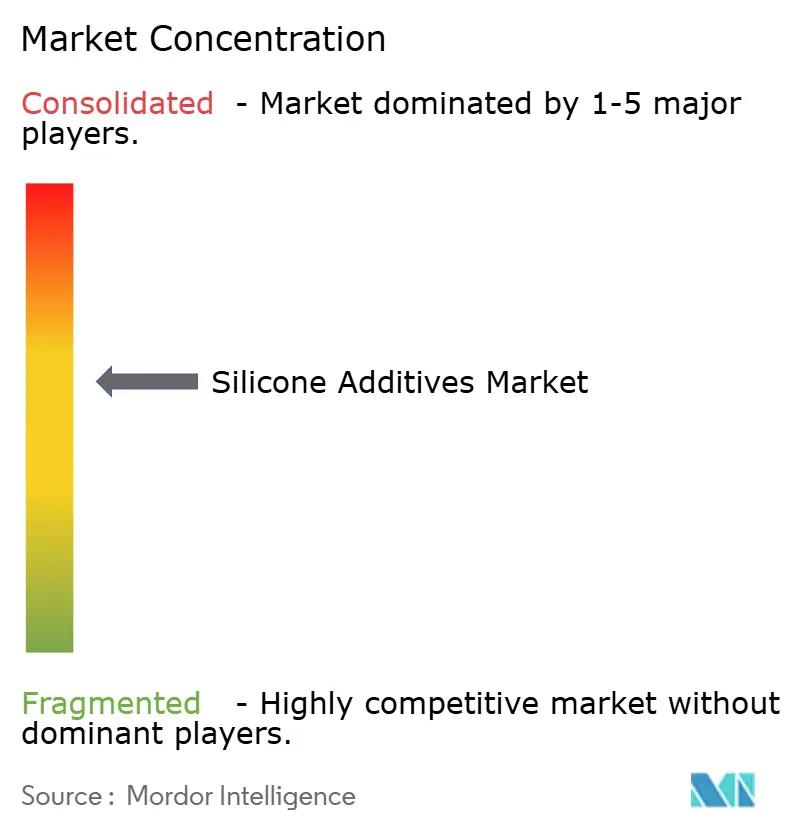

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicone Additives Market Analysis by Mordor Intelligence

The Silicone Additives Market size was valued at USD 2.09 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 2.98 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031). Robust demand stems from manufacturers seeking additives that keep coatings, polymers, and fluids stable under heat, chemicals, and harsh weather. Regulatory pressure to cut volatile-organic-compound (VOC) emissions is steering formulators toward silicone-rich systems that match performance with compliance . Growth momentum also reflects deeper penetration in thermal management for electric vehicles, bio-based personal-care launches, and rising food-processing automation across emerging economies. Industry consolidation—most notably KCC’s take-over of Momentive in 2024—signals a shift toward scale advantages, vertical integration, and faster innovation pipelines.

Key Report Takeaways

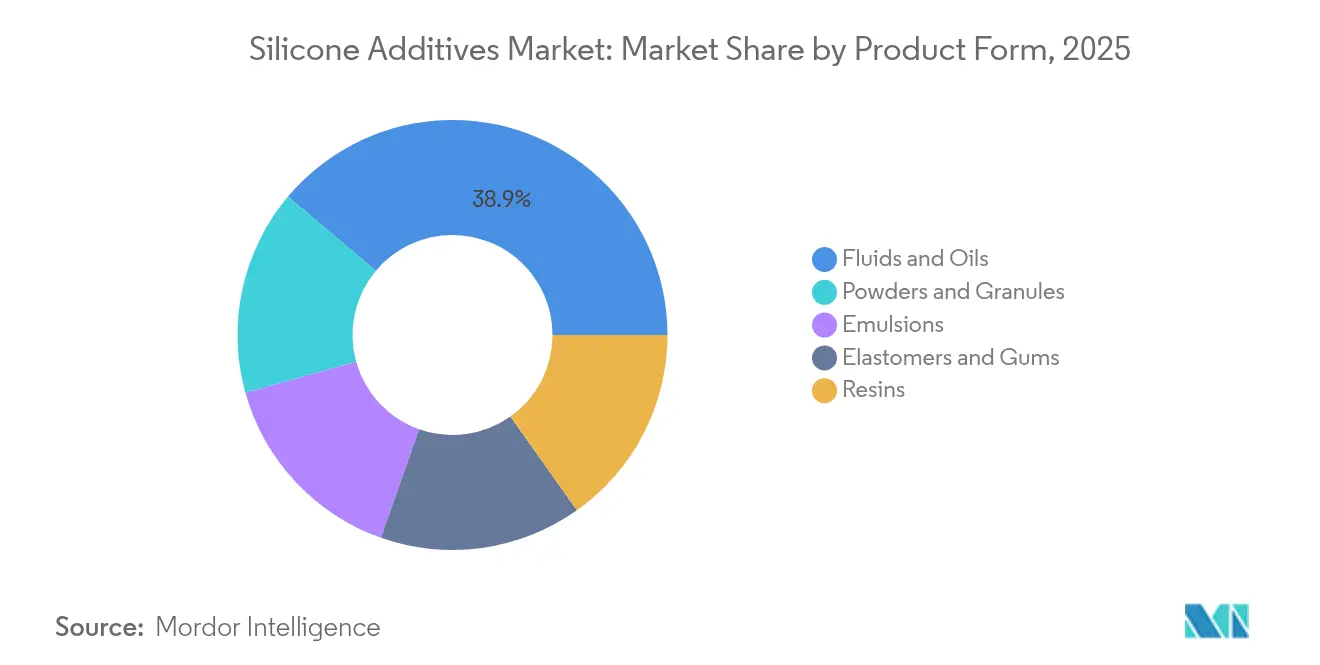

- By product form, silicone fluids led with 38.87% of silicone additives market share in 2025; powders and granules are projected to accelerate at a 7.34% CAGR to 2031.

- By application, defoamers held 35.62% revenue share of the silicone additives market size in 2025, whereas “other applications” (thermal management, aerospace, 3D printing) are poised for a 6.88% CAGR through 2031.

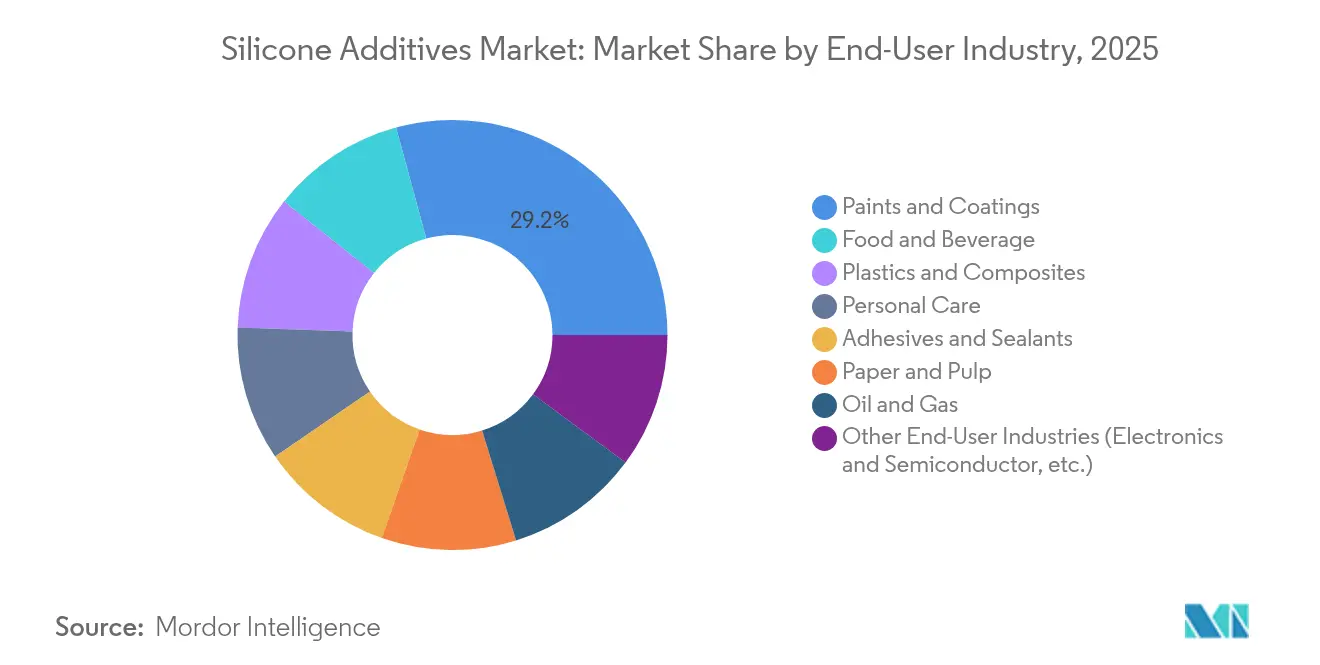

- By end-user industry, paints and coatings captured 29.23% of the silicone additives market size in 2025; electronics and semiconductors are the fastest grower at an 7.78% CAGR.

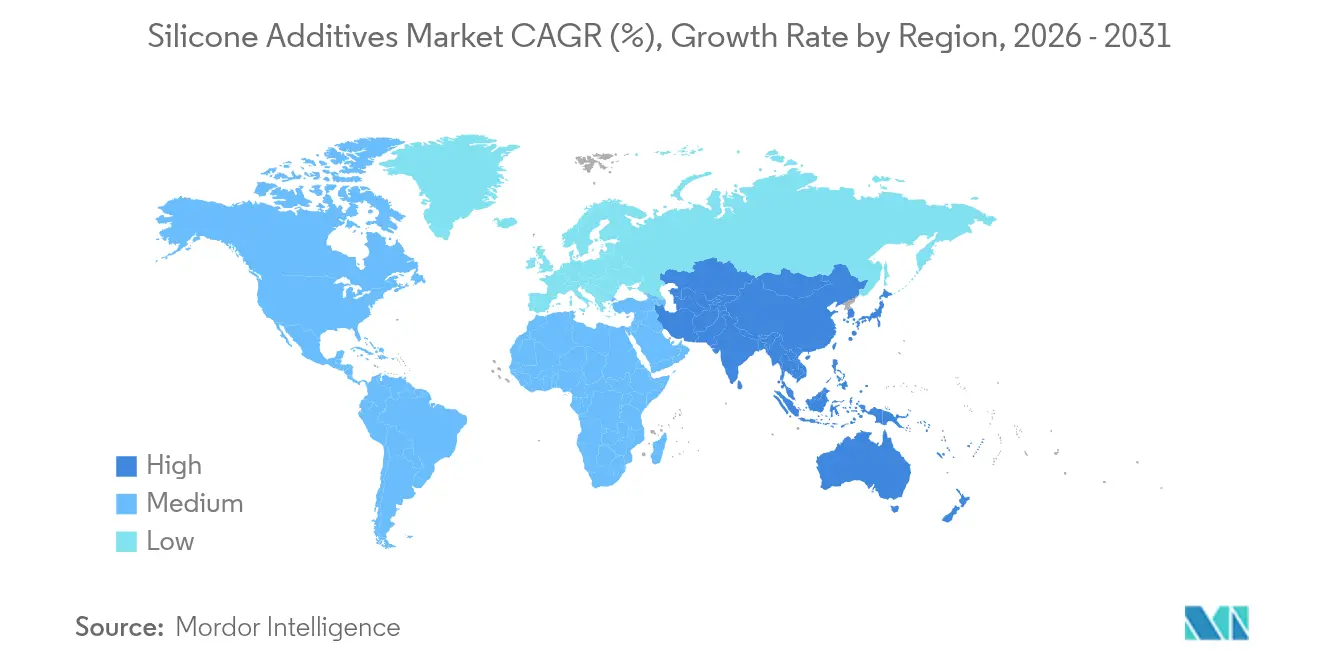

- By geography, Asia-Pacific commanded 46.81% of the silicone additives market in 2025 and is expected to advance at a 6.92% CAGR to 2031, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicone Additives Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Demand from Personal Care Industry | +1.2% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Growing Focus on Low-VOC Products in Paints and Coatings | +1.0% | North America & EU primarily, expanding to APAC | Long term (≥ 4 years) |

| Growing Demand from Food-Processing Industry | +0.8% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Increasing Usage in Medical and Healthcare Applications | +0.9% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| High Utilization from the Automotive Industry | +1.1% | APAC core, expanding to North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increase in Demand from Personal Care Industry

Consumers gravitate toward light, non-oily textures, prompting formulators to favor silicone fluids for silky spread and lasting moisture. Shin-Etsu’s elastomer-in-oil line, for example, builds stable oil-in-water emulsions that meet regional bans on cyclic siloxanes while sustaining the desired skin-feel[1]Shin-Etsu Chemical, “Silicone Elastomer Gels for Personal Care,” shinetsu.co.jp. Suppliers are rolling out plant-origin C13-15 alkane carriers such as Elkem’s PURESIL ORG gels, proving that sensory performance and natural positioning can coexist. Asia-Pacific labels are leveraging these attributes to bridge gaps with global premium brands, widening the silicone additives market in color cosmetics and sun care.

Growing Focus on Low-VOC Products in Paints and Coatings

Legislators in Europe and North America cap allowable solvent content, making low-VOC compliance a prerequisite rather than a feature. Evonik’s TEGO Guard 9000 delivers early-rain resistance in exterior coatings without breaching eco-label thresholds[2]Evonik Industries, “TEGO Guard 9000: Water-Resistant Additive for Exterior Paints,” evonik.com. Siltech has shown that long-chain alkyl silicones lift solids content yet cut VOC totals, letting formulators maintain durability while meeting Green Seal or LEED targets. The ripple effect extends to emerging markets, where builders increasingly specify water-based paints fortified with silicone surface additives for stain repellence and long-term color retention.

Growing Demand from Food-Processing Industry

Automated dairy, beverage, and ready-meal plants cannot tolerate foam-induced overflows. FDA-cleared silicone defoamers such as Elkem’s AMSil series ensure continual throughput while keeping taste and safety intact. As urban diets drive packaged-food output across Asia, processors lean on silicone emulsions to curb micro-bubble formation in viscous sauces and broths, safeguarding fill accuracy and reducing clean-down cycles. The trend feeds a specialized slice of the silicone additives market where compliance with food-contact regulations is non-negotiable.

Increasing Usage in Medical and Healthcare Applications

Implantables demand materials that remain inert, stretchy, and stable inside the body. NuSil’s MED-grade silicones, certified to USP Class VI, prove critical for catheters, pacer leads, and neuro-stimulation devices. The march toward patient-specific implants ushers in 3D-printed silicone parts: additives that fine-tune cure kinetics enable complex lattices tailored to each anatomy. With global populations aging, the silicone additives market taps a durable growth engine in healthcare.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Additive Migration at High Temperatures | -0.7% | Global, with particular impact in automotive & aerospace | Medium term (2-4 years) |

| Volatile Raw-material Costs | -0.9% | Global, with supply chain concentration in Asia | Short term (≤ 2 years) |

| Technical Challenges such as Migration and Adhesion Issues | -0.6% | Global, affecting high-performance applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Additive Migration at High Temperatures

Above 200 °C, low-molecular-weight siloxanes can bleed to surfaces, dulling optical clarity or weakening adhesion. Studies on high-phenyl silicone rubbers reveal improved thermal stability, with only 5% weight loss at 478 °C, yet premium grades raise costs. EV traction motors and aerospace ducting need formulations that curb volatilization, pressuring R&D budgets.

Volatile Raw-Material Costs

Dimethyl-siloxane monomer relies on energy-intensive metallurgical-grade silicon. Plant shutdowns—like Dow’s 2024 closure in Wales—send prices swinging and squeeze smaller producers. To hedge, majors bundle upstream quartz sourcing with captive ferrosilicon smelting, while startups explore bio-based feedstocks. Until those alternatives scale, margin risk shadows the silicone additives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Fluids Dominate Versatility While Powders Drive Precision

Silicone fluids accounted for 38.87% of the silicone additives market in 2025 by revenue, riding on wide use as slip, leveling, and heat-transfer agents in coatings, personal care, and lubricants. Their low surface tension and broad temperature stability underpin a resilient demand base. Emulsions and resins complement fluids by enabling water-borne systems and structural finishes, particularly in construction sealants. In contrast, elastomers address gasket, seal, and medical-tube niches needing lasting elasticity.

Powders and granules, although less than one-quarter of sales, post the fastest 7.34% CAGR through 2031. Their dry format aids 3D printing feedstocks and masterbatch compounding, granting formulators fine rheology control and dust-free dosing. Emerging UV-curable polysiloxane powders simplify on-demand cross-linking for rapid prototypes, shrinking design-to-part cycles and enlarging the silicone additives market size for additive manufacturing. As printer fleets spread beyond aerospace into dental and consumer goods, powdered silicones capture fresh avenues for growth.

By Application: Defoamers Hold the Lead, Electronics Catalyze “Other” Uses

Defoamers locked in a 35.62% slice of the silicone additives market size in 2025 by eliminating bubbles that hamper throughput across pulp, food, and chemical reactors. High efficiency at low treat rates keeps them entrenched even as green certifications tighten. Rheology modifiers follow, crucial for leveling and anti-sag in low-VOC coatings. Wetting and dispersing agents further smooth coating films and pigment slurries, lifting shelf life and consistency.

“Other applications” form the sprinter cohort, advancing at a 6.88% CAGR. Thermal interface materials capitalize on EV battery demand, while release agents tailored for semiconductor mold compounds gain traction. PFAS-free textile finishes built on organosilicone backbones repel oil and water without fluorine, reflecting regulatory shifts. As aerospace primes adopt silicone-enabled ablatives and anti-icing skins, revenue streams in this bucket diversify, enlarging the silicone additives market share captured by emerging uses.

By End-User Industry: Coatings Anchor Today, Electronics Power Tomorrow

Paints and coatings claimed 29.23% of the silicone additives market size in 2025. The segment banks on long standing relationships with resin suppliers, clear cost-benefit math, and strict VOC rules that make silicone flow agents indispensable. Architectural paints benefit from water repellence and self-cleaning attributes, while automotive refinish shops value mar resistance. Personal care trails but remains vital, embedding silicones for spreadability and silky touch across hair serums and color cosmetics.

Electronics and semiconductors headline the fastest 7.78% CAGR. Rapid inverter and 5G antenna rollouts need thermally conductive gap fillers and low-dielectric coatings. In chip packaging, release agents slash defect counts when precise molding tolerances are paramount. Medical devices and renewable-energy storage round out other high-growth customers, widening the silicone additives market for specialized, high-margin grades.

Geography Analysis

Asia-Pacific sat atop the silicone additives market with 46.81% revenue share in 2025 and is marching at a 6.92% CAGR toward 2031. China’s Zhangjiagang and Nanjing clusters anchor upstream siloxane capacity for Wacker and Elkem, ensuring supply proximity to electronics and EV battery giants. India’s “Make in India” policy stokes domestic demand for quality-driven coatings and adhesives, compelling local formulators to incorporate silicone additives for premium finish and durability. Japan and South Korea each foster advanced R&D, channeling silicone additives into high-frequency electronics, photonics, and specialty films.

North America follows as a mature but innovation-rich arena. The United States leads adoption in medical devices and aerospace composites, relying on FDA/USP compliant silicone systems. Dow’s silicone recycling pilot in Michigan aims to trim polydimethylsiloxane (PDMS) carbon footprints by 50% and resonates with buyers under ESG mandates. Canada’s EV-battery investments and Mexico’s automotive clusters promise incremental pull-through for thermal-management additives.

Europe ranks third in size yet first in sustainability stringency. REACH and impending PFAS bans intensify R&D for cyclic-free and bio-based silicone alternatives. Evonik’s Smart Effects business line combines siloxane and organic specialties to tackle lightweighting, e-mobility, and digital health markets. Germany and France concentrate vehicle electrification grants, while the United Kingdom emphasizes life-science coatings, collectively protecting a steady flow of high-margin orders.

Competitive Landscape

The silicone additives market demonstrates moderate consolidation. The 2024 KCC-Momentive merger produced a top-tier supplier boasting siloxane monomer to formulated additive integration, broader regional reach, and stronger bargaining power. Dow, Wacker, and Shin-Etsu sustain leadership through capacity scale, application labs near customers, and cross-industry portfolios. Elkem and CHT Group carve specialist positions in additive manufacturing and EV thermal interfaces, respectively.

Sustainability drives strategy. Dow’s tie-up with Circusil targets silicone circularity, tackling a 1.7 ton CO₂-equivalent saving per ton of recycled PDMS and offering buyers verified Scope 3 reductions. Wacker pilots enzymatic routes that slash methanol consumption, hinting at lower energy intensity. Start-ups position bio-based alkyl-silicone hybrids as drop-in sensory enhancers, pressing incumbents to hedge with venture investments.

Silicone Additives Industry Leaders

Wacker Chemie AG

Shin-Etsu Chemical Co., Ltd.

Momentive

Evonik Industries AG

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: At the European Coatings Show 2023, WACKER Group introduced SILRES BS 338, a silicone additive for silicate paints and interior brush-on plasters. This aqueous emulsion improves processing, storage stability, and coating properties.

- April 2025: Dow’s Performance Silicones Business announced a 5–10% price increase in Greater China, effective April 20, 2025, or as contracts permit. The adjustment reflects Dow's commitment to reliable, high-quality silicone solutions.

Global Silicone Additives Market Report Scope

The global silicone additives market report includes:

| Fluids and Oils |

| Elastomers and Gums |

| Resins |

| Powders and Granules |

| Emulsions |

| Defoamers |

| Rheology Modifiers |

| Surfactants |

| Wetting and Dispersing Agents |

| Lubricating Agents |

| Adhesion Promoters |

| Other Applications (Release Agents, etc.) |

| Food and Beverage |

| Plastics and Composites |

| Paints and Coatings |

| Personal Care |

| Adhesives and Sealants |

| Paper and Pulp |

| Oil and Gas |

| Other End-User Industries (Electronics and Semiconductor, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Form | Fluids and Oils | |

| Elastomers and Gums | ||

| Resins | ||

| Powders and Granules | ||

| Emulsions | ||

| By Application | Defoamers | |

| Rheology Modifiers | ||

| Surfactants | ||

| Wetting and Dispersing Agents | ||

| Lubricating Agents | ||

| Adhesion Promoters | ||

| Other Applications (Release Agents, etc.) | ||

| By End-User Industry | Food and Beverage | |

| Plastics and Composites | ||

| Paints and Coatings | ||

| Personal Care | ||

| Adhesives and Sealants | ||

| Paper and Pulp | ||

| Oil and Gas | ||

| Other End-User Industries (Electronics and Semiconductor, etc.) | ||

| Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Silicone Additives Market size?

The silicone additives market size reached USD 2.22 billion in 2026.

How fast will the silicone additives market grow through 2031?

Revenue is projected to rise at a 6.11% CAGR, taking the market to USD 2.98 billion by 2031.

Which region dominates global demand?

Asia-Pacific holds 46.81% of global revenue and is expanding the fastest, supported by China’s EV manufacturing and India’s industrial upgrades.

Which application segment is growing most quickly?

Electronics-related “other applications” are advancing at a 6.88% CAGR due to thermal-management needs in EV batteries and semiconductor packaging.

Page last updated on: