Automotive Elastomer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 40.5 Billion |

| Market Size (2031) | USD 54.81 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Elastomer Market Analysis by Mordor Intelligence

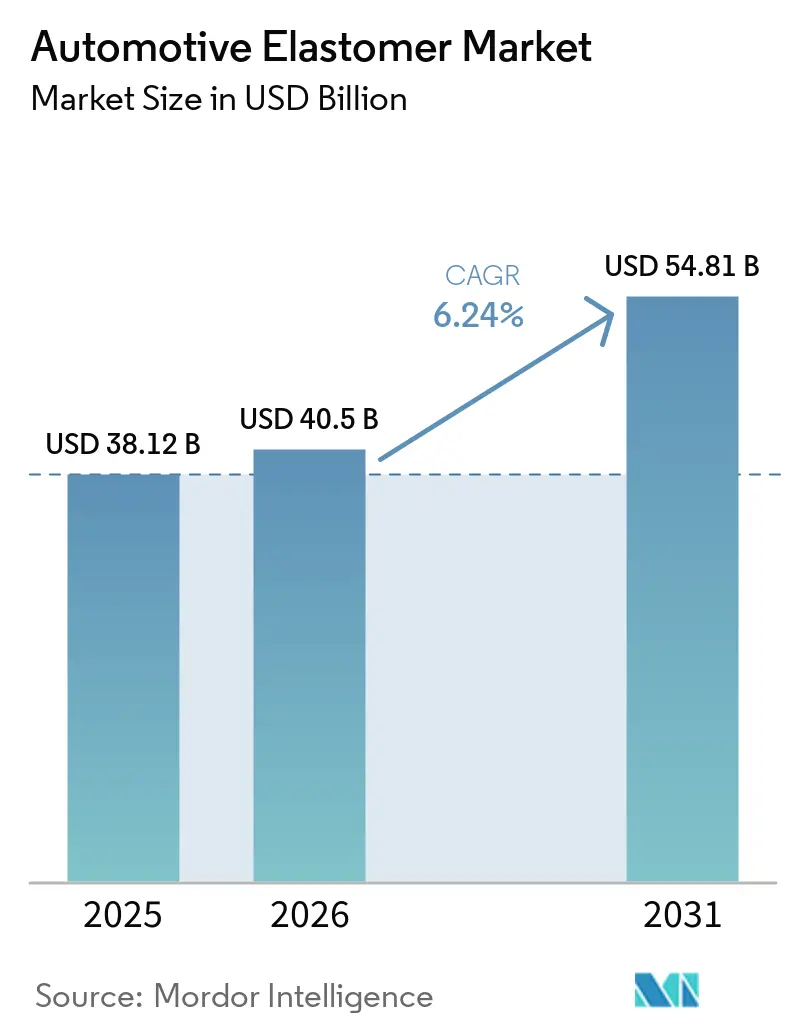

The Automotive Elastomer Market size is projected to be USD 38.12 billion in 2025, USD 40.5 billion in 2026, and reach USD 54.81 billion by 2031, growing at a CAGR of 6.24% from 2026 to 2031. Thermoset grades continue to dominate tire, chassis, and under-hood applications. However, the increasing availability of recyclable thermoplastic elastomers is influencing material selection for new programs. These materials can be injection-molded in short cycles, trimmed in-line, and recovered at the end of their lifecycle. The growing electrification of vehicles is driving demand for high-dielectric silicone and polyolefin elastomers, which provide insulation for 800-volt architectures while resisting thermal runaway. Additionally, new low-VOC regulations in China, the United States, and the European Union are prompting reformulations to eliminate solvent-based plasticizers and formaldehyde-generating crosslinkers. This has strengthened collaboration between OEMs and tier-one suppliers to accelerate material validation. Supply chains are also becoming more localized, with capacity expansions in China, India, and Southeast Asia reducing lead times. Blockchain-based digital product passports are now being used to track recycled and bio-based feedstocks at the lot level, addressing Scope 3 emission audits from automakers.

Key Report Takeaways

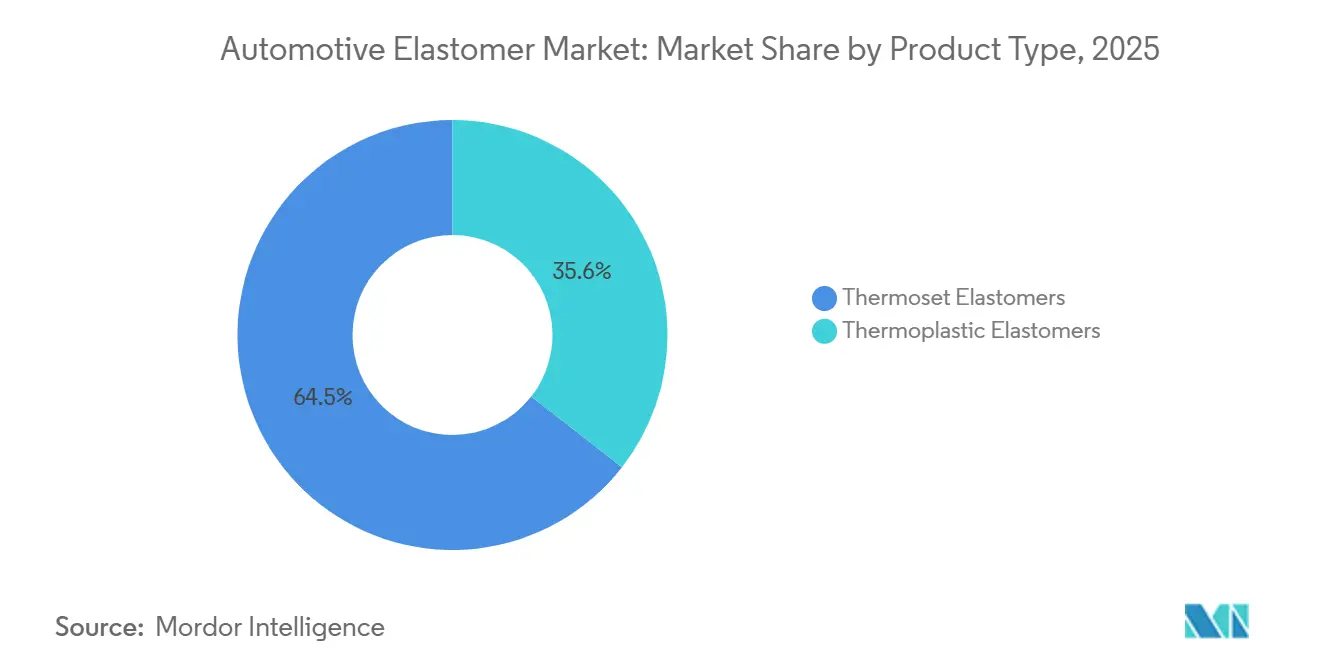

- By product type, thermoset elastomers led with 64.45% of the automotive elastomer market share in 2025, while thermoplastic elastomers are projected to expand at a 6.49% CAGR through 2031.

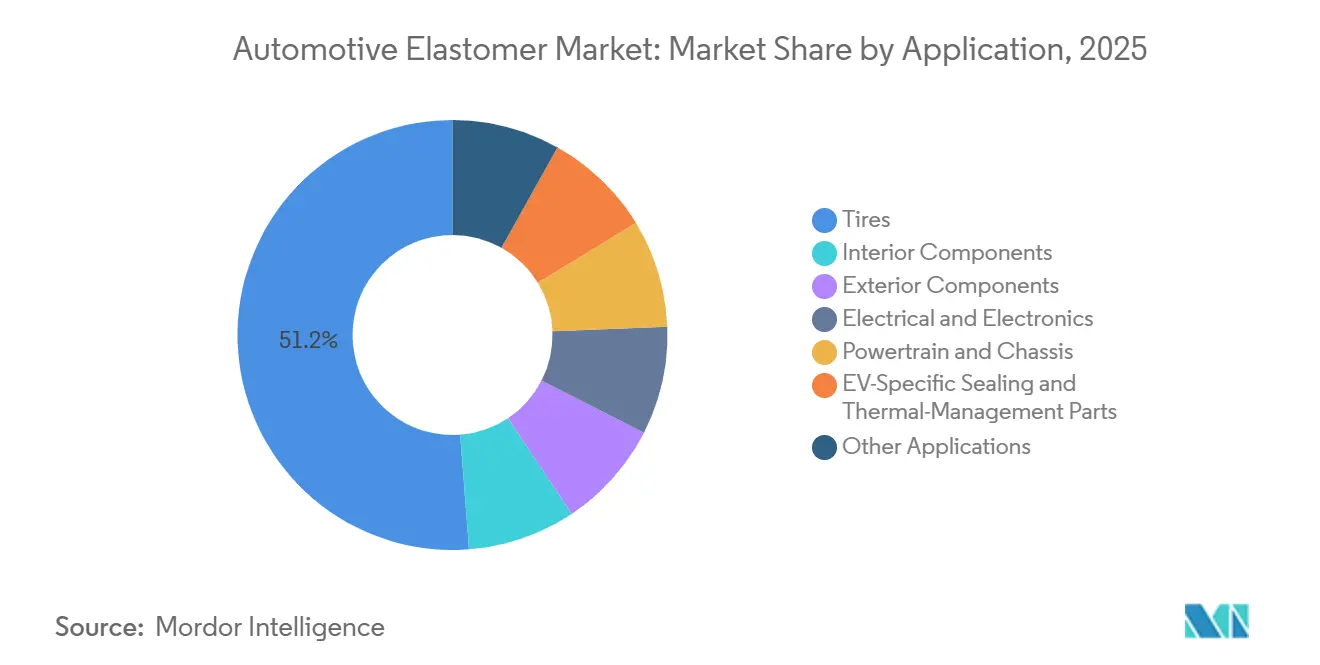

- By application, tires accounted for 51.22% of the automotive elastomer market share in 2025, while EV-specific sealing and thermal-management parts are advancing at a 6.89% CAGR through 2031.

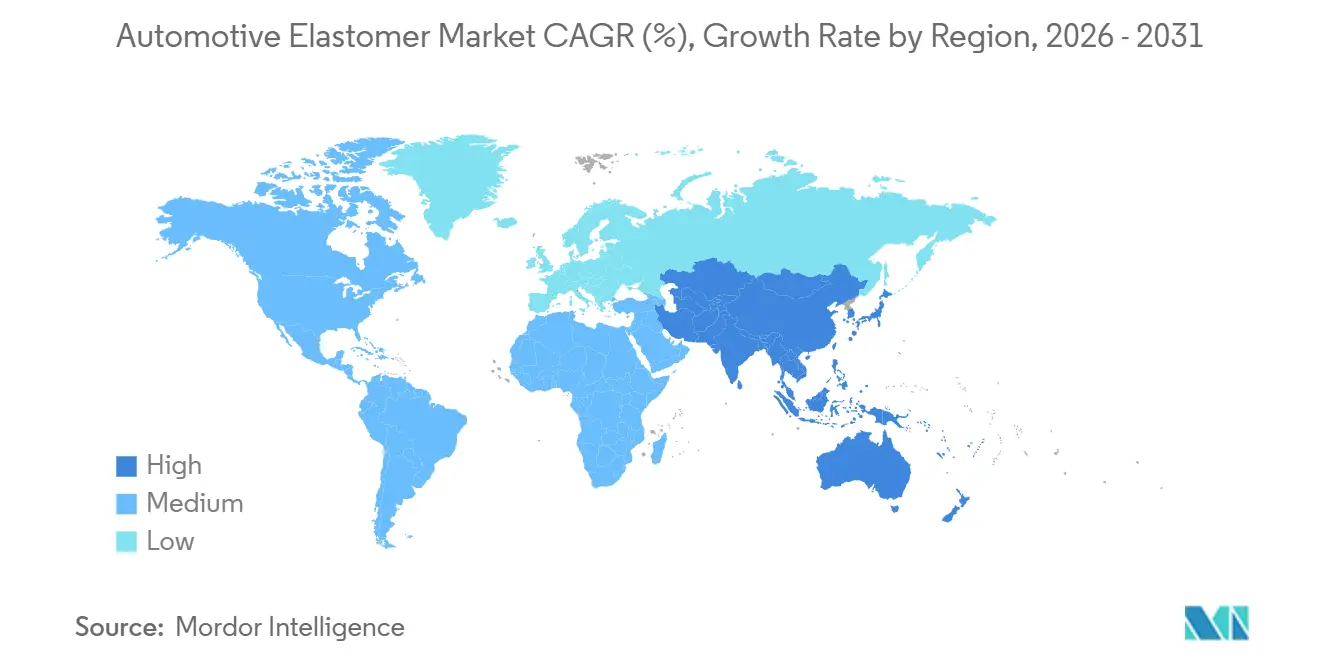

- By geography, Asia-Pacific commanded 44.48% of the automotive elastomer market share in 2025 and is forecast to post the quickest regional growth at a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Elastomer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-down replacement of conventional rubber compounds | +0.9% | Global, with early adoption in Asia-Pacific and Europe | Medium term (2-4 years) |

| Rapid tire-replacement cycles in emerging markets | +1.2% | Asia-Pacific core (India, China, ASEAN), spill-over to Middle-East and Africa | Short term (≤ 2 years) |

| OEM shift toward single-digit VOC interior materials | +0.7% | North America, Europe, China | Medium term (2-4 years) |

| 3D-printed elastomer gaskets enabling agile EV niche production | +0.4% | North America and Europe, pilot adoption in China | Long term (≥ 4 years) |

| Blockchain-enabled feedstock traceability boosting bio-elastomer uptake | +0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Down Replacement of Conventional Rubber Compounds

Bio-based elastomers and CO₂-derived polyols are transitioning from pilot projects to procurement as polymer producers secure renewable feedstocks to mitigate fossil fuel price fluctuations. Covestro’s Cardyon platform converts industrial CO₂ into polyurethane precursors, reducing the cradle-to-gate carbon footprint by 50% without compromising flame resistance. Ford is piloting this material in seat foam and aims to achieve 20% recycled or renewable plastics by 2025, pressuring compounders to qualify drop-in grades. BASF’s Zhanjiang complex, operational since 2025 and powered entirely by renewable electricity, is supplying lower-carbon ethylene for EPDM and styrene-butadiene rubber production. Industry research highlights chemical recycling and bio-feed substitution as scalable pathways to achieve cost parity with virgin elastomers by 2030[1]European Chemical Industry Council (CEFIC), “Circular Economy Study,” cefic.org. These developments are reinforcing a structural cost-down trend favoring high-volume, lower-carbon compounds in the automotive elastomer market.

Rapid Tire-Replacement Cycles in Emerging Markets

Price volatility in natural rubber, fluctuating between USD 1,400-1,800 per ton in 2025, is shifting demand toward synthetic blends that stabilize margins and simplify sourcing. Regional producers are expanding capacity, with Mitsui set to launch a 120,000 tpa Tafmer polyolefin elastomer line in Singapore by fiscal 2026 to supply tire and sealing manufacturers in ASEAN countries. The need to address short replacement cycles is driving cross-border arbitrage in butadiene and styrene, benefiting compounders capable of effectively hedging currency and feedstock fluctuations. This dynamic supports above-market growth in the automotive elastomer market.

OEM Shift Toward Single-Digit VOC Interior Materials

China’s GB 30981 standard, effective June 2026, imposes stringent VOC limits for interior coatings, compelling door-seal and skin suppliers to eliminate residual solvents. Similarly, the European Union’s formaldehyde limit of 0.062 mg/m³ for vehicle cabins, effective August 2027, is driving European converters to replace urea-formaldehyde adhesives in laminated trims. Nissan’s TailorFit polyurethane seating, launched in February 2026, exemplifies OEM preferences for low-odor synthetics that replicate leather textures without incurring premium costs. BASF and Hyundai Transys have jointly developed a modular seat using supercritical-fluid-foamed TPU, reducing VOC emissions and enabling full recyclability. Certification to ISO 12219 interior-air standards is now a contractual requirement for new programs, accelerating the adoption of low-emission elastomers in the automotive market.

3D-Printed Elastomer Gaskets Enabling Agile EV Niche Production

Research in 2025 demonstrated the feasibility of multi-material 3D printing for nitrile-butadiene interfaces that meet battery-pack sealing standards while bypassing traditional 12-16 week tooling cycles. Tier-two suppliers are integrating digital twin simulations with additive tooling to deliver prototypes within days, reducing design iteration times for EV cooling circuits. Freudenberg introduced an injection-moldable PFAS-free battery seal in April 2025, setting performance benchmarks for future printable compounds. Hutchinson’s EPDM grade, capable of withstanding temperatures from −40 °C to +165 °C, further expands operational capabilities. At the same time, additive manufacturing remains low-volume; its ability to produce customized geometries positions it for gradual growth in the automotive elastomer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU REACH and US EPA tightening on PAH limits | -0.6% | Europe, North America | Short term (≤ 2 years) |

| Elastomer recyclate quality inconsistency hampers closed-loop uptake | -0.5% | Global, with acute impact in Europe due to End-of-Life Vehicle Regulation | Medium term (2-4 years) |

| Skill scarcity in high-precision electric vehicle elastomer compounding | -0.3% | North America, Europe, emerging in China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU REACH and US EPA Tightening on PAH Limits

The European Chemicals Agency (ECHA) has capped polycyclic aromatic hydrocarbons (PAHs) in process oils at 3 ppm, requiring tire and non-tire EPDM compounders to adopt naphthenic alternatives. These alternatives increase raw material costs and reduce low-temperature flexibility. Similarly, the US EPA’s aligned regulation, effective 2024, has eliminated legacy aromatic extracts from the North American supply chain, raising EPDM input prices by 8-12%[2]United States Environmental Protection Agency, “Final Rule on PAHs,” epa.gov. Asian OEMs, including Panasonic, have also banned these substances, extending compliance testing timelines by up to six weeks. The EU’s microplastics ban further complicates the situation by restricting crumb-rubber use, accelerating research into devulcanization technologies that remain commercially unviable. Small compounders without ISO 17025-certified labs face challenges in certifying below-detection PAH levels, risking market share in the automotive elastomer market.

Elastomer Recyclate Quality Inconsistency Hampers Closed-Loop Uptake

A 2024 study revealed that 40% bumper recyclates exhibit ±15% melt-flow variability in thermoplastic elastomers, leading to increased scrap rates during molding. EPDM tests conducted in 2025 showed a 7% tensile strength loss at 80 phr crumb addition, which is acceptable for low-stress seals but unsuitable for door gaskets. Trinseo’s dissolution recycling modules, announced in March 2026, recover high-quality polycarbonate, but scalable devulcanization for crosslinked elastomers remains elusive. The draft End-of-Life Vehicle Regulation mandates 25% recycled content by 2030, but the absence of standardized quality grades hinders OEM approval for safety-critical components. As a result, only 100 million of the 1.5 billion waste tires generated annually are repurposed into new elastomer products, limiting progress toward circularity in the automotive elastomer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Thermoset Elastomers Lead Revenue, While Thermoplastic Elastomers Gain Traction

In 2025, thermoset elastomers accounted for 64.45% of the automotive elastomer market share, driven by their extensive use in tires and high-heat under-hood components. Meanwhile, thermoplastic elastomers are projected to grow at a CAGR of 6.49% through 2031. Cooper Standard’s FlexiCore body seal has replaced traditional metal-carrier EPDM with a fully recyclable combination of polyolefin elastomer and polypropylene, reducing vehicle weight by 44% and cutting plant energy consumption by 20%. Additionally, BASF and Hyundai Transys have introduced TPU seating foam using supercritical-fluid foaming, which aligns with End-of-Life targets and eliminates the need for chemical blowing agents.

Thermoset compounds are essential for applications requiring resistance to temperature cycling, fuel exposure, and compression set, such as tire sidewalls, brake hoses, and motor-mount bushings. However, rising feedstock costs led Celanese to increase Santoprene prices in April 2026, narrowing the cost gap with thermoplastic alternatives. Specialty styrene-based elastomers with improved scratch resistance are increasingly used in soft-touch interior panels, reducing the market share of crosslinked EPDM. To adapt to these changes, suppliers are dual-sourcing facilities to accommodate both chemistries, ensuring flexibility as the automotive elastomer market evolves.

By Application: EV Sealing Surges Ahead of Tires

In 2025, tires represented 51.22% of the automotive elastomer market. However, EV-specific sealing and thermal-management components are expected to grow at a CAGR of 6.89% through 2031, driven by the requirements of 800-volt battery packs for higher dielectric strength and flame-retardant properties. Freudenberg’s PFAS-free injection-moldable seal demonstrates this shift, offering a tenfold improvement in leakage resistance.

Interior applications face cost pressures as OEMs demand single-digit VOC limits and a leather-like finish. Supercritical-foamed TPU skins meet these requirements while reducing odor. On the exterior, frameless door weatherstrips enhance premium EV styling and require precise NVH control as powertrain masking diminishes. High-voltage wiring and connector seals are transitioning to silicone and fluoroelastomer grades capable of continuous operation at 165 °C, increasing value per vehicle even as combustion-engine mounts decline. These diverse requirements are driving differentiated growth across the automotive elastomer market.

Geography Analysis

In 2025, the Asia-Pacific region held 44.48% of the automotive elastomer market share and is expected to grow at a CAGR of 6.67% through 2031. China’s polyolefin elastomer production reached 60,000 tons in 2025 and is projected to exceed 300,000 tons by the end of 2026, supported by expansions at Dushanzi and other complexes. Multinational companies such as BASF and LANXESS are localizing Cellasto and additive production to mitigate feedstock volatility and leverage labor cost advantages. Additionally, China’s GB 30981 low-VOC regulation is driving the adoption of thermoplastic elastomers in mainstream interior trims.

North America is navigating the transition from internal combustion engines (ICE) to an expanding battery supply chain. Dow has delayed its planned polyolefin elastomer debottlenecking to 2029-2030 due to demand uncertainties. Meanwhile, EPA PAH caps have increased EPDM compound costs, accelerating the shift to paraffinic oil substitutes. The local assembly of battery packs, spanning the U.S. Midwest to Ontario, is reshaping logistics for just-in-time gasket deliveries in the automotive elastomer market.

Europe enforces some of the strictest chemical regulations globally. Formaldehyde caps will take effect in August 2027, while the End-of-Life Vehicle directive aims for 25% recycled polymer content by 2030. Restrictions on microplastics are also reducing the use of crumb-rubber fillers. SABIC is divesting its commodity olefins sites to AEQUITA and engineered thermoplastics to Mutares, signaling a shift away from lower-margin segments. Wacker is investing in a silicone specialty plant in Czechia to support EV and renewable energy systems, highlighting the market’s move toward specialty applications.

Competitive Landscape

In 2025, the market is moderately concentrated. Key strategies include: expanding regional capacities to reduce freight and tariff costs, upgrading specialty portfolios to achieve 20-30% price premiums, and emphasizing sustainability credentials verified through blockchain technology. Cooper Standard’s FlexiCore recyclable seal has replaced long-standing EPDM-metal designs in Tesla models, demonstrating the compatibility of lightweighting and circularity with cost objectives. BASF is scaling microcellular urethane production in India, Wacker is expanding silicone capacity in Japan and South Korea, and Mitsui is commissioning Tafmer elastomer production in Singapore to supply ASEAN tire manufacturers.

Technological advancements include digital twins for seal design, supercritical foaming techniques that eliminate VOC-emitting agents, and ceramifying silicones designed to insulate busbars at temperatures up to 1,000 °C. Goodyear’s sale of its chemical arm to Gemspring for USD 650 million highlights tire manufacturers’ retreat from upstream elastomers, creating feedstock opportunities for independent players. Suppliers with ISO 17025-certified in-house labs gain a competitive edge by self-certifying below 3 ppm PAH and meeting ISO 12219 VOC standards, reducing OEM approval timelines by six weeks and gaining a schedule advantage in the automotive elastomer market.

Automotive Elastomer Industry Leaders

BASF

Exxon Mobil Corporation

LANXESS

Dow

LG Chem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Hutchinson developed an elastomer compound specifically designed to address the sealing requirements of components used in electric vehicle heat pump applications utilizing the R744 refrigerant (CO₂). Its hardness rating of 80 Shore A enabled it to withstand high-pressure applications of up to 130 bar, enhancing system safety.

- February 2024: KRAIBURG TPE Pvt. Ltd launched a new range of automotive thermoplastic elastomers (TPEs) with a minimum recycled content of 73%, complying with stringent OEM standards for emissions and odor. The range featured hardness levels between 20 and 95 Shore A, making it suitable for soft-touch, interior, and exterior applications.

Global Automotive Elastomer Market Report Scope

Automotive elastomers are durable and flexible polymers, either natural or synthetic rubber, developed for high-performance automotive applications such as tires, seals, hoses, and weather stripping. These materials offer heat resistance, chemical compatibility, and durability. Commonly used polymers include EPDM, nitrile (NBR), and silicone, which are designed to endure harsh under-the-hood conditions and improve interior comfort.

The Automotive Elastomers Market is segmented into product type, application, and geography. By product type, the market is segmented into thermoset elastomers and thermoplastic elastomers. By application, the market is segmented into tires, interior components, exterior components, electrical and electronics, powertrain and chassis, EV-specific sealing and thermal-management parts, and other applications. The report also covers the market size and forecasts for automotive elastomers in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Thermoset Elastomers |

| Thermoplastic Elastomers |

| Tires |

| Interior Components |

| Exterior Components |

| Electrical and Electronics |

| Powertrain and Chassis |

| EV-Specific Sealing and Thermal-Management Parts |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Malaysia | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Product Type | Thermoset Elastomers | |

| Thermoplastic Elastomers | ||

| By Application | Tires | |

| Interior Components | ||

| Exterior Components | ||

| Electrical and Electronics | ||

| Powertrain and Chassis | ||

| EV-Specific Sealing and Thermal-Management Parts | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Malaysia | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Turkey | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the automotive elastomer market?

The automotive elastomer market stands at USD 40.50 billion in 2026 and is projected to reach USD 54.81 billion by 2031, recording a 6.24% CAGR during 2026-2031.

Which region is expanding fastest through 2031?

Asia-Pacific leads growth, expanding at a 6.67% CAGR through 2031 as China and India add tire and EV-related capacity.

What drives the shift toward thermoplastic elastomers?

Recyclability mandates, shorter molding cycles, and low-VOC compliance are steering OEMs toward thermoplastics that can be recovered at end-of-life.

Why are EV platforms important for elastomer suppliers?

Battery packs need advanced sealing, flame retardancy, and dielectric insulation, boosting elastomer content per vehicle despite declining ICE-related parts.

Page last updated on: