Plastic Extrusion Machine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

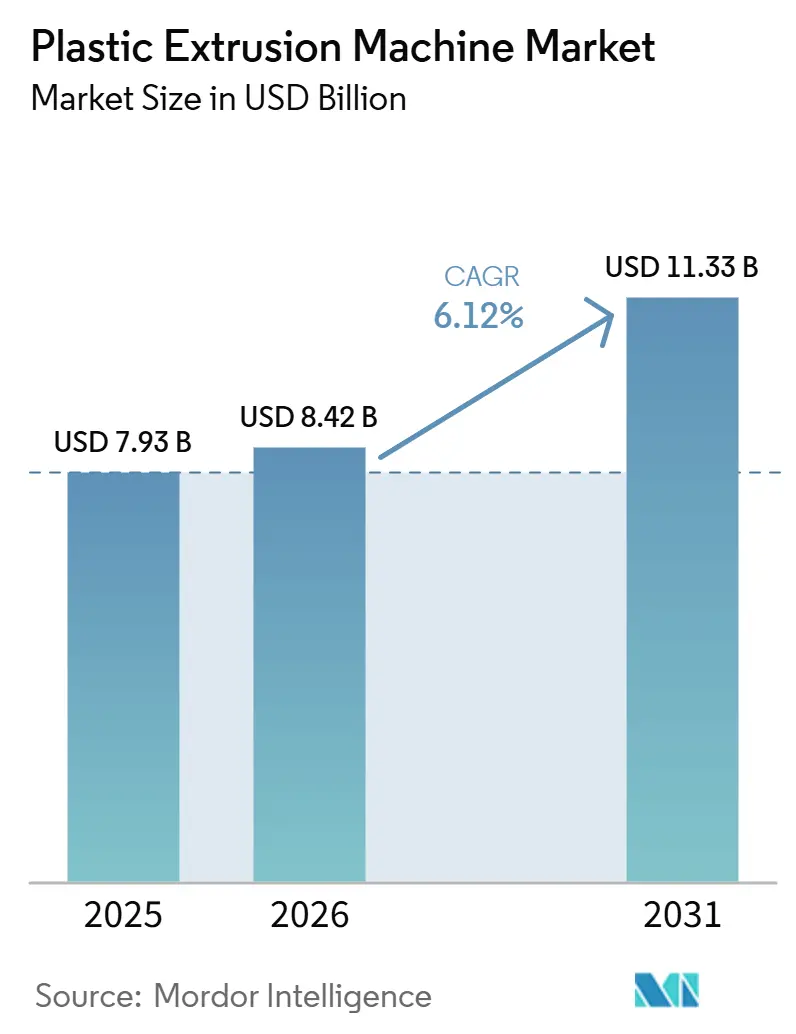

| Market Size (2026) | USD 8.42 Billion |

| Market Size (2031) | USD 11.33 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

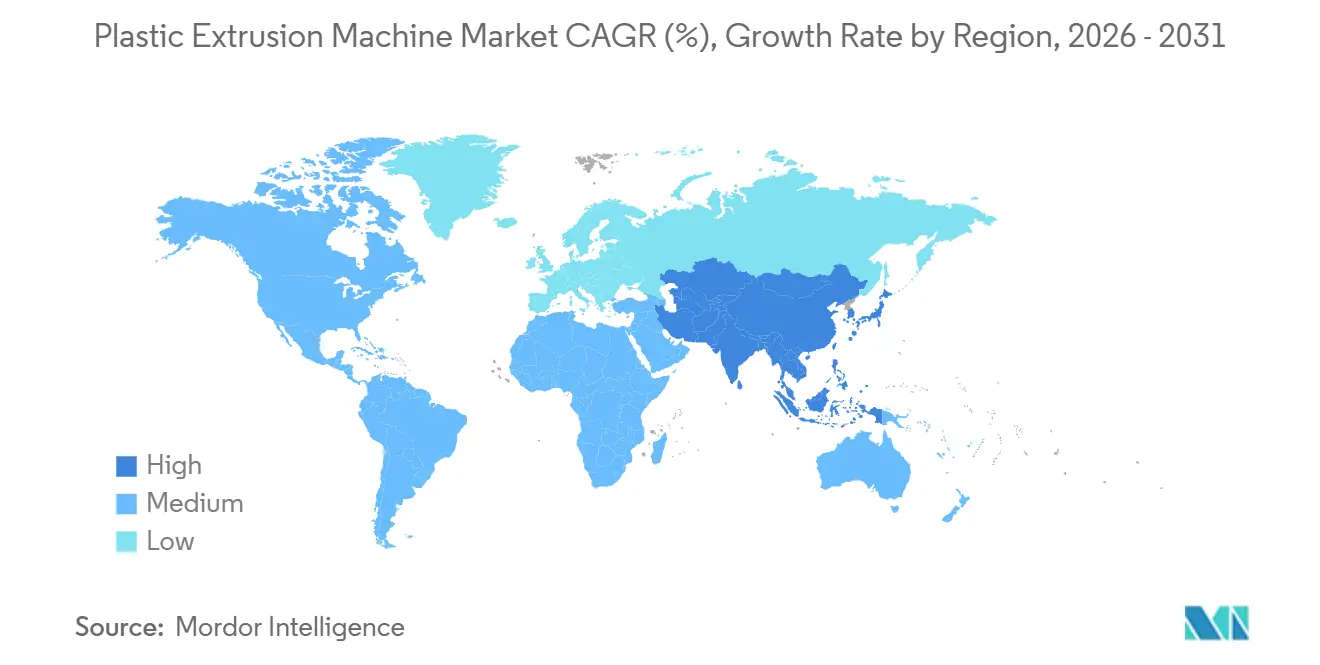

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

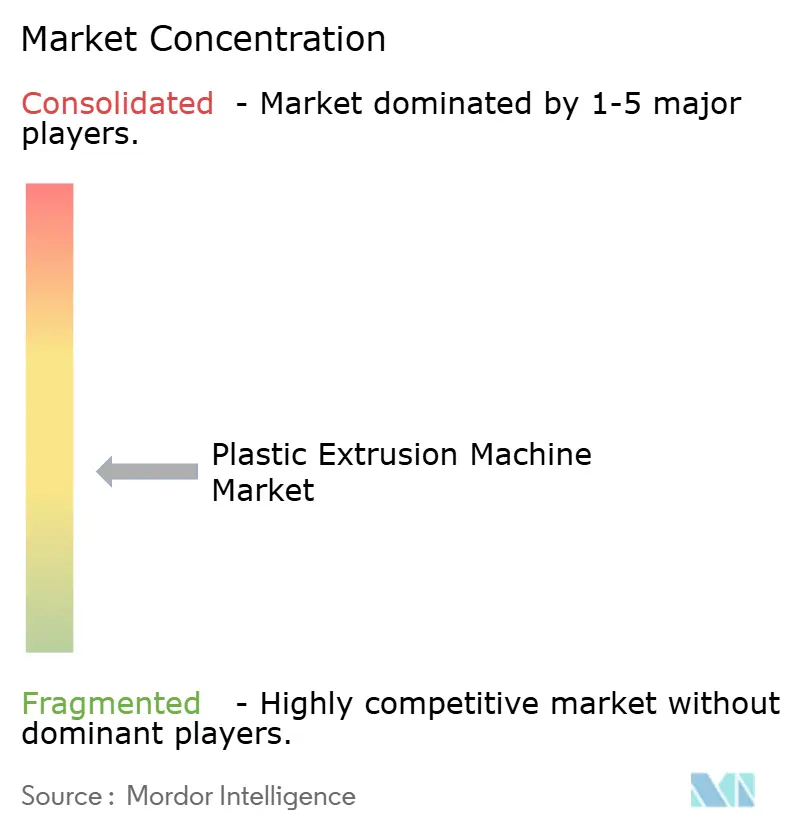

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Extrusion Machine Market Analysis by Mordor Intelligence

The Plastic Extrusion Machine Market size is projected to be USD 7.93 billion in 2025, USD 8.42 billion in 2026, and reach USD 11.33 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031. In Europe and North America, stricter mandates on recycled content are encouraging converters to update older single-screw lines. In the Asia-Pacific region, particularly in China, India, and ASEAN countries, increasing production capacities are contributing to the global rise in throughput. While single-screw units maintained a cost advantage in 2025, twin-screw machines are experiencing higher growth due to their improved mixing capabilities for regrind and engineering polymers. Packaging accounted for the largest share of end-use demand, but micro-extrusion for medical devices is growing, supported by personalized hospital care and the demand for sterile, single-use items. In Europe, rising electricity costs are driving the adoption of energy-efficient drives to protect margins. Additionally, converters are focusing on AI-driven predictive controls to achieve defect-free output.

Key Report Takeaways

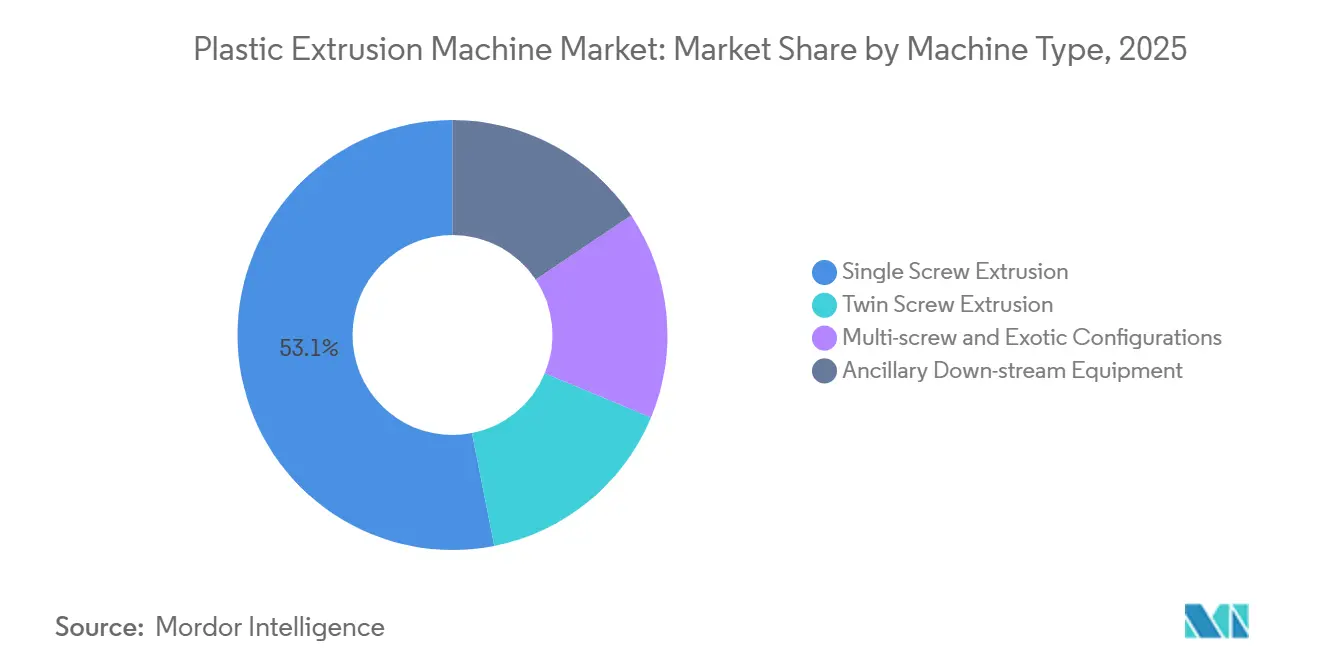

- By machine type, single-screw extrusion led with 53.11% of the plastic extrusion machine market share in 2025; twin-screw extrusion is projected to post the fastest 6.21% CAGR from 2026 to 2031.

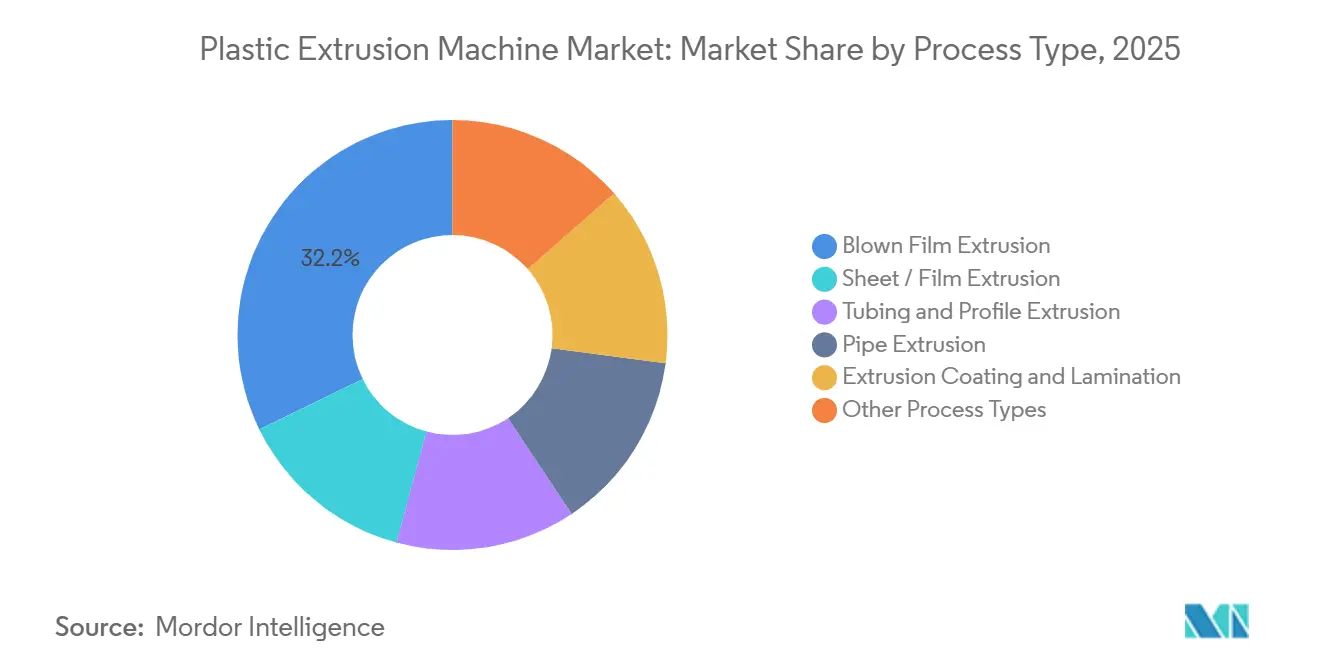

- By process type, blown-film extrusion held 32.24% revenue share in 2025; extrusion coating and lamination is poised to expand at a 6.42% CAGR from 2026 to 2031.

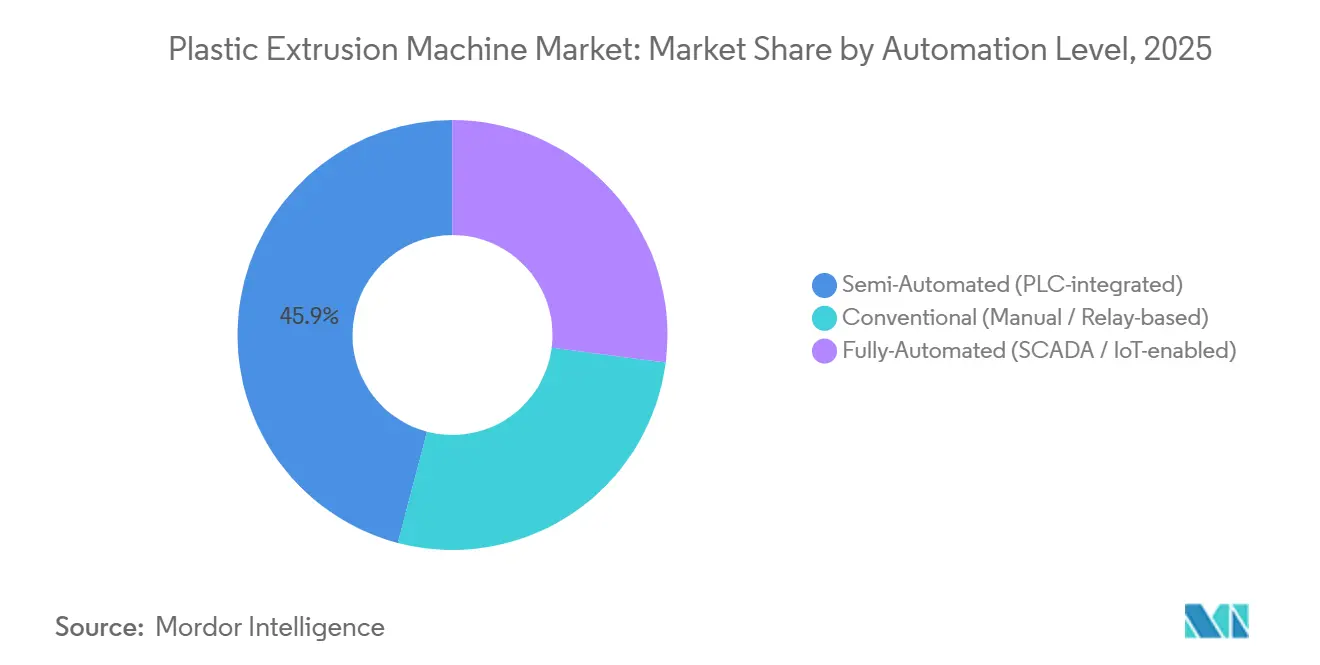

- By automation level, semi-automated (PLC-integrated) commanded 45.89% of the plastic extrusion machine market size in 2025, whereas fully automated SCADA/IoT configurations are advancing at a 6.56% CAGR from 2026 to 2031.

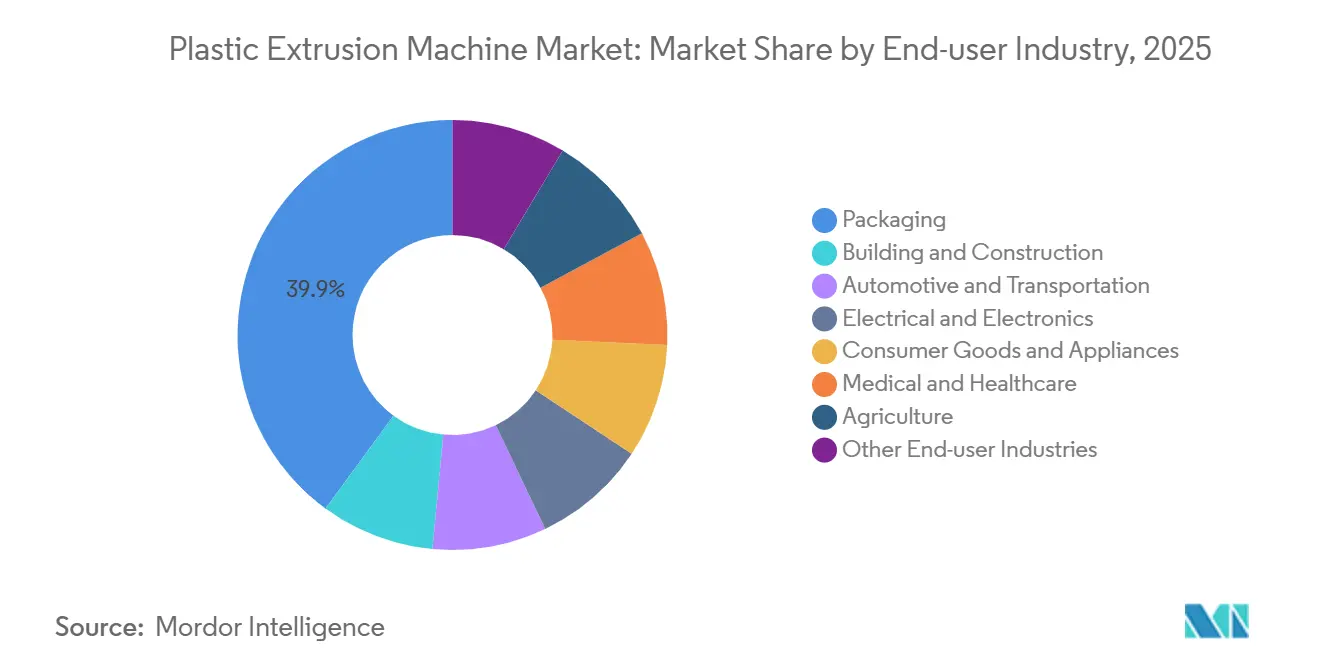

- By end-user industry, packaging secured 39.91% share of the plastic extrusion machine market size in 2025; medical and healthcare is accelerating at a 6.93% CAGR from 2026 to 2031.

- By geography, Asia-Pacific accounted for 48.22% of 2025 revenue and is progressing at a 6.88% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plastic Extrusion Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in automation and energy-efficient machinery | +1.2% | Global, with early adoption in Germany, United States, Japan | Medium term (2-4 years) |

| Rising demand for recycled and biodegradable polymer extrusion | +1.5% | EU core, North America, spillover to ASEAN | Long term (≥ 4 years) |

| Government incentive schemes for circular-economy equipment | +0.9% | Australia (Victoria, NSW), Netherlands, United States (EPA SWIFR) | Short term (≤ 2 years) |

| AI-enabled predictive process control for zero-defect output | +0.8% | North America & EU, pilot deployments in China, India | Medium term (2-4 years) |

| On-site micro-extrusion for personalized medical implants | +0.6% | North America, Western Europe, select metro hubs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advancements in Automation and Energy-Efficient Machinery

Centralized control platforms, such as Bausano’s ORQUESTRA 4.0, collect live operating data and organize maintenance events. This approach reduces unscheduled downtime, helping converters manage margins amid rising power prices in Europe. In 2026, SML introduced a twin-screw system that achieved a 10-15% reduction in specific energy input and a 20% decrease in gels on cast-film lines. This development highlights the growing focus on energy efficiency and quality improvements. Coperion’s C-Beyond lifecycle suite monitors gearbox vibrations and provides alerts to prevent catastrophic failures. This feature supports asset-life extensions, addressing challenges posed by the retirement of skilled technicians. Germany and the U.S. are leading early adoption, with the reduced total cost of ownership driving automation as a critical factor in purchase decisions.

Rising Demand for Recycled and Biodegradable Polymer Extrusion

The EU Packaging and Packaging Waste Regulation mandates 30-65% recycled content between 2030 and 2040, prompting a wave of line retrofits that favor twin-screw starve-feeding of dusty flake streams[1]European Parliament, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” europa.eu . Coperion’s STS 35 Mc 11 boosts throughput by 27% on contaminated regrind because intermeshing screws self-clean and control melt temperature. California’s requirement that all packaging be recyclable or compostable by 2032 lifts interest in bio-based PLA extrusion lines. Manufacturers respond with abrasion-resistant screws, tighter residence-time control, and low-shear melting zones that protect recycled polymer integrity, reshaping value propositions across the plastic extrusion machine market.

AI-Enabled Predictive Process Control for Zero-Defect Output

In a 2024 study published in the Journal of Manufacturing Processes, researchers found that neural-network models predict dimensional accuracy with an R² score above 0.9. When integrated into machine control, this development reduced scrap by 20%. Extru-Tech’s EXPRO AI has optimized formulation trials, cutting the time from days to hours by recommending screw-speed profiles based on historical data. NetFIELD's edge gateways support predictive maintenance by buffering data during outages and deploying containerized anomaly-detection applications within two hours. This functionality enables smaller converters, including those without dedicated IT teams, to adopt predictive maintenance practices. To meet the demands of medical and automotive contracts, which impose strict recall penalties, early adopters in North America and Europe are leveraging zero-defect certifications as a competitive advantage.

On-Site Micro-Extrusion for Personalized Medical Implants

Micro-extruders in operating rooms efficiently produce custom PCL bone scaffolds and EVA ocular implants, addressing sterilization logistics and reducing inventory waste. Hospital networks in the U.S. and Germany are evaluating benchtop twin-screw units, designed for Class 7 cleanrooms, that can achieve sub-millimeter tolerances as needed. FDA clearances are granted on a case-by-case basis, while reimbursement frameworks supporting patient-specific devices are encouraging equipment manufacturers to explore this specialized niche. Although compact lines involve higher costs per kilogram compared to industrial units, surgeons prioritize speed over volume. This trend is creating a new profit opportunity for OEMs capable of miniaturizing screws, barrels, and control hardware without compromising validation traceability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental regulations on virgin-plastic use | -0.7% | EU core, California, Canada (British Columbia, federal), spillover to ASEAN | Short term (≤ 2 years) |

| Scarcity of high-torque gearbox suppliers lengthening lead-times | -0.4% | Global, acute in large-diameter twin-screw (>90 mm) segments | Medium term (2-4 years) |

| Skilled operator shortage amid demographic shift | -0.5% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Regulations on Virgin-Plastic Use

Canada's prohibition on single-use plastics, along with California's SB 54, is requiring retailers and restaurants to transition from virgin materials to recycled or compostable options[2]Government of Canada, “Single-Use Plastics Prohibition Regulations Overview,” canada.ca. This regulatory compliance has increased demand for food-grade rPET, which is priced 25% higher than its virgin counterpart. Additionally, converters are working within tight deadlines to validate new formulations. In Europe, a 2030 recyclability mandate will restrict multilayer laminates that cannot be easily delaminated. Converters unable to modify their production lines may lose contracts, as brand owners increasingly prefer suppliers that provide traceable recycled content.

Scarcity of High-Torque Gearbox Suppliers Lengthening Lead Times

A limited number of firms globally can provide case-hardened gears rated for 2,000 Nm per shaft, a requirement for twin-screw extruders exceeding 90 mm in diameter. Neugart USA can dispatch small servo gearboxes within two days. However, there is a backlog for planetary and parallel-shaft units used in high-output compounding, with waits ranging from six to twelve months. While Asian capacity additions exceed the domestic supply of gearboxes, European heat-treat lines face occasional gas curtailments, further delaying deliveries. OEMs operating their own gearbox shops maintain a pricing advantage, as converters are paying a premium for guaranteed commissioning dates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Twin-Screw Accelerates on Compounding Versatility

Twin-screw units are projected to grow faster than the broader plastic extrusion machine market, with a 6.21% CAGR through 2031. This growth is observed across various regions, even though single-screw machines accounted for 53.11% of the plastic extrusion machine market share in 2025. The market size for laboratory twin-screw systems in plastic extrusion remains relatively small today, but it is expanding at a notable rate. This trend is driven by converters in different geographies running trial batches of recycled or bio-based formulations before scaling to production.

Modular screw elements allow operators to adjust kneading, conveying, and devolatilizing sections, which improves pigment dispersion at 0.1% loadings and helps prevent thermal degradation in hygroscopic polymers. Capital investment increases with screw diameter, but throughput grows with the square of that diameter, reducing cost per kilogram for high-volume plants. Single-screw machines continue to dominate the pipe and profile sector due to their simpler maintenance requirements. However, their market share is gradually declining in regions where converters are qualifying high-regrind recipes that only twin-screw machines can process consistently.

By Process Type: Coating Lines Benefit from Recyclability Rules

In 2025, blown film accounted for 32.24% of the revenue share. However, extrusion coating and lamination are anticipated to grow at a CAGR of 6.42%, reflecting the increasing preference among brand owners for mono-material barrier structures. The plastic extrusion machine market, particularly for nine-to-eleven-layer coating lines, is expanding as food brands transition from mixed laminate pouches to all-PE alternatives that align with upcoming grade-A recyclability labels.

Energy audits indicate that co-extrusion consumes less than 2.6 kWh per square meter, which is approximately half the energy usage of solvent-based laminate production. This allows converters to reduce energy expenses and compliance costs related to solvent emissions. While pipe, tubing, and profile lines continue to meet infrastructure demands in India and ASEAN, investments are gradually shifting toward barrier-film lines. These lines are designed to support contracts requiring extended shelf life for products such as fresh meat and ready-to-eat meals.

By Automation Level: SCADA and IIoT Secure Premium Margins

In 2025, semi-automated PLC lines accounted for 45.89% of the market share. Fully automated SCADA and IoT-enabled systems are projected to grow at a 6.56% CAGR, driven by the increasing focus of converters on achieving zero-defect certifications and optimizing predictive maintenance. The plastic extrusion machine market is experiencing notable growth in regions with elevated energy tariffs and limited labor availability, highlighting the importance of maintaining operational uptime.

Edge gateways with embedded Docker containers analyze real-time trends in torque, melt pressure, and temperature, providing alerts to prevent specification deviations from escalating into scrap. Entry-level cloud tiers are now included with new machines at no additional cost, reducing financial barriers for smaller converters. Manual relay lines remain prevalent in Vietnam and parts of Africa, where low labor costs continue to outweigh the expenses of automation. However, these facilities are increasingly pressured by export customers requiring certified logged process data.

By End-User Industry: Healthcare Demand Surpasses Growth of Packaging

In 2025, packaging contributed 39.91% of revenue, growing in line with the market average. Medical and healthcare applications are anticipated to grow at a CAGR of 6.93% during the forecast period, representing the fastest growth among segments. The market size for plastic extrusion machines associated with catheter, stent, and scaffold production remains limited. However, the increasing adoption of personalized medicine is driving higher equipment orders from hospital networks.

Micro-extruders designed for cleanroom environments incorporate stainless frames, HEPA-filtered enclosures, and rapid-change screws that can be sanitized in under 30 minutes. The automotive and construction segments experience cyclical demand but continue to support the need for fuel-tank barrier sheets and pipes made from PVC or HDPE. In the electronics segment, low-smoke, halogen-free compounds are being used for insulation in EV wires and cables, contributing to incremental demand across Asia and North America.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 48.22% of global revenue and is projected to achieve a CAGR of 6.88% through 2031, supported by capacity expansions in China, India, and ASEAN nations. Thailand, with its 3,200 converters and 34.6 million tonnes of petrochemical capacity, shows room for improvement in recycling. Growth opportunities may arise if policymakers implement stricter circular-economy targets.

In North America, retrofitting facilities is prioritized over constructing new ones, particularly with regulations such as California’s SB 54 and Canadian bans becoming more stringent. However, low mechanical-recycling rates have led to a reliance on importing certified rPET from Europe, which continues to drive investments in twin-screw reclamation lines. Mexico is attracting near-shoring investments, particularly in EV wiring and food-contact films, facilitating cross-border supplies to U.S. OEMs under the USMCA agreement.

Europe operates under some of the most stringent regulations in the industry. The PPWR's focus on recycled content and recyclability grades is encouraging converters to adopt advanced five-to-eleven-layer coextruders equipped with online quality analytics. Germany and Italy are leading in automation adoption, while Eastern Europe and the Nordics are testing chemical-recycling feedstock preparation, which requires high-vacuum devolatilization extruders. In South America and the Middle East, growth remains uneven: Brazil is investing in silage-film lines despite currency fluctuations, and Saudi Arabia is increasing its HDPE pipe capacity to address water infrastructure needs.

Competitive Landscape

The plastic extrusion machine market remains moderately fragmented, with KraussMaffei, JWELL Extrusion Machinery, Davis-Standard, Reifenhäuser Group, and Hillenbrand (Milacron) holding significant positions.

Technology continues to drive competition. KraussMaffei’s Continuous Fiber Pelletizing system removes a compounding step and reduces fiber breakage, aiming to secure contracts in automotive lightweighting. Coperion’s RF400 roller feeder expands its presence into battery-separator film lines, reflecting a strategic move into adjacent markets. SML’s twin-screw technology reports 10-15% energy savings, highlighting the increasing focus on low kilowatt-hours per kilogram in Europe’s energy-sensitive environment.

Edge-computing providers like Hilscher are enabling broader adoption of IIoT integration. Machine builders can now incorporate predictive maintenance capabilities without requiring dedicated software teams. Opportunities for growth exist in pharmaceutical micro-extruders and high-vacuum devolatilizers for chemical recycling. These segments are marked by limited competition from players with both process expertise and the engineering capabilities for cleanroom or corrosion-resistant applications.

Plastic Extrusion Machine Industry Leaders

KraussMaffei

Hillenbrand

Reifenhäuser Group

Davis-Standard Corporation

JWELL Extrusion Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: SML launched a co-rotating twin-screw extruder delivering 10-15% lower energy draw and 20% fewer gels than single-screw peers.

- September 2025: Hillenbrand, Inc completed sale of its majority interest in the Milacron injection molding and extrusion business (“Milacron”), within the Molding Technology Solutions segment, to Bain Capital for USD 287 million. Bain Capital now owns an approximate 51% share and has full operational control of Milacron, while Hillenbrand maintains an ownership stake of approximately 49%.

Global Plastic Extrusion Machine Market Report Scope

A plastic extrusion machine is a manufacturing device that converts raw thermoplastic materials (pellets, granules, or powder) into continuous, uniform shapes. It works by heating and melting plastic inside a barrel using a rotating screw, then forcing the molten material through a shaped die to form products like pipes, tubing, sheets, and films.

The market is segmented by machine type, process type, automation level, end-user industry, and geography. By machine type, the market is segmented into single screw extrusion, twin screw extrusion, multi-screw and exotic configurations, and ancillary downstream equipment. By process type, the market is segmented into blown film extrusion, sheet/film extrusion, tubing and profile extrusion, pipe extrusion, extrusion coating and lamination, and other process types. By automation level, the market is segmented into semi-automated (PLC-integrated), conventional (manual/relay-based), and fully-automated (SCADA/IoT-enabled). By end-user industry, the market is segmented into packaging, building and construction, automotive and transportation, electrical and electronics, consumer goods and appliances, medical and healthcare, agriculture, and other end-user industries. The report also covers the market size and forecasts for Plastic Extrusion Machine in 17 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Single Screw Extrusion |

| Twin Screw Extrusion |

| Multi-screw and Exotic Configurations |

| Ancillary Down-stream Equipment |

| Blown Film Extrusion |

| Sheet / Film Extrusion |

| Tubing and Profile Extrusion |

| Pipe Extrusion |

| Extrusion Coating and Lamination |

| Other Process Types |

| Semi-Automated (PLC-integrated) |

| Conventional (Manual / Relay-based) |

| Fully-Automated (SCADA / IoT-enabled) |

| Packaging |

| Building and Construction |

| Automotive and Transportation |

| Electrical and Electronics |

| Consumer Goods and Appliances |

| Medical and Healthcare |

| Agriculture |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Machine Type | Single Screw Extrusion | |

| Twin Screw Extrusion | ||

| Multi-screw and Exotic Configurations | ||

| Ancillary Down-stream Equipment | ||

| By Process Type | Blown Film Extrusion | |

| Sheet / Film Extrusion | ||

| Tubing and Profile Extrusion | ||

| Pipe Extrusion | ||

| Extrusion Coating and Lamination | ||

| Other Process Types | ||

| By Automation Level | Semi-Automated (PLC-integrated) | |

| Conventional (Manual / Relay-based) | ||

| Fully-Automated (SCADA / IoT-enabled) | ||

| By End-user Industry | Packaging | |

| Building and Construction | ||

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Consumer Goods and Appliances | ||

| Medical and Healthcare | ||

| Agriculture | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the plastic extrusion machine market?

It stands at USD 8.42 billion in 2026 and is projected to reach USD 11.33 billion by 2031.

Which machine type is growing fastest?

Twin-screw extruders are forecast to post a 6.21% CAGR through 2026-2031, the quickest among machine types.

Why are extrusion coating lines attracting investment?

Mono-material coating lines help converters meet EU recyclability grades while using half the energy of solvent laminators.

How are regulations shaping buying decisions in North America?

Mandates such as California’s SB 54 push converters to retrofit lines for recycled feedstocks rather than build greenfield plants.

Page last updated on: