Market Overview

| Study Period | 2020 - 2031 |

|---|---|

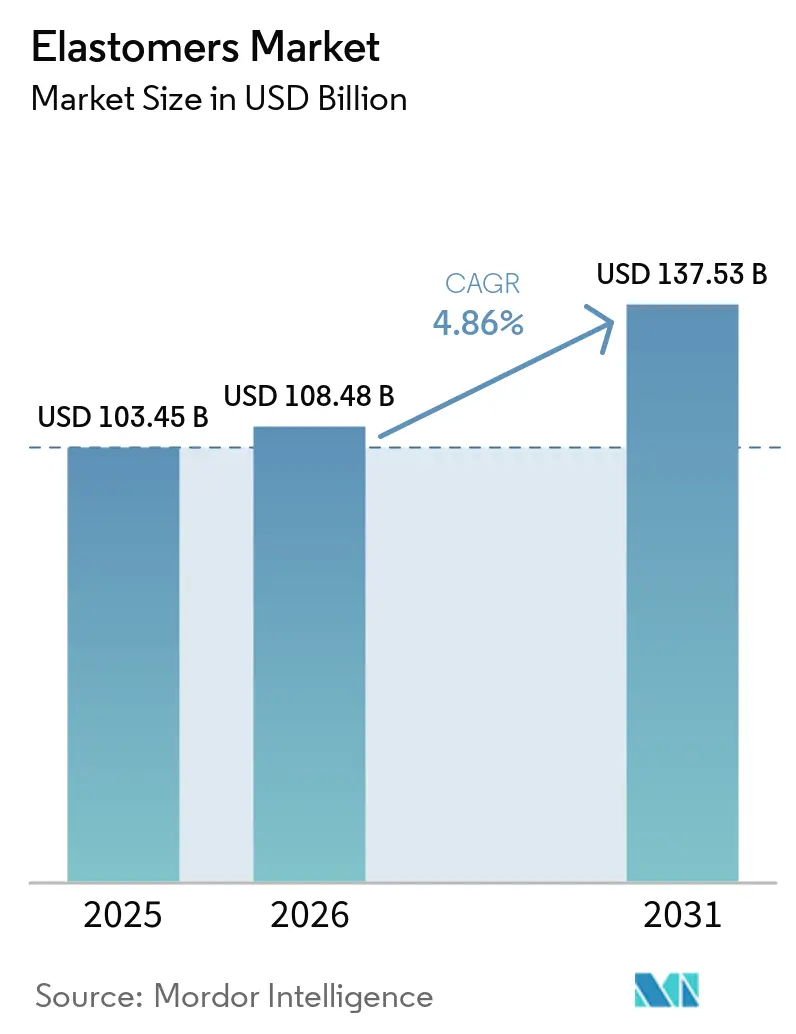

| Market Size (2026) | USD 108.48 Billion |

| Market Size (2031) | USD 137.53 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Elastomers Market Analysis by Mordor Intelligence

The Elastomers market size is expected to grow from USD 103.45 billion in 2025 to USD 108.48 billion in 2026 and is forecast to reach USD 137.53 billion by 2031 at 4.86% CAGR over 2026-2031. The upward trajectory of the Elastomers market is tied to the material’s ability to deliver weight reduction in automotive platforms, extend electric-vehicle range, and meet circular-economy expectations without sacrificing durability. Thermoplastic grades are displacing conventional rubbers because they melt-process on standard plastics equipment, cut cycle times, and enable closed-loop re-grind streams that lower scrap rates. Rapid urbanization in Asia Pacific and the push for energy-efficient buildings keep construction demand elevated, while medical device makers accelerate the shift away from PVC tubing toward biocompatible TPEs that survive sterilization.

Key Report Takeaways

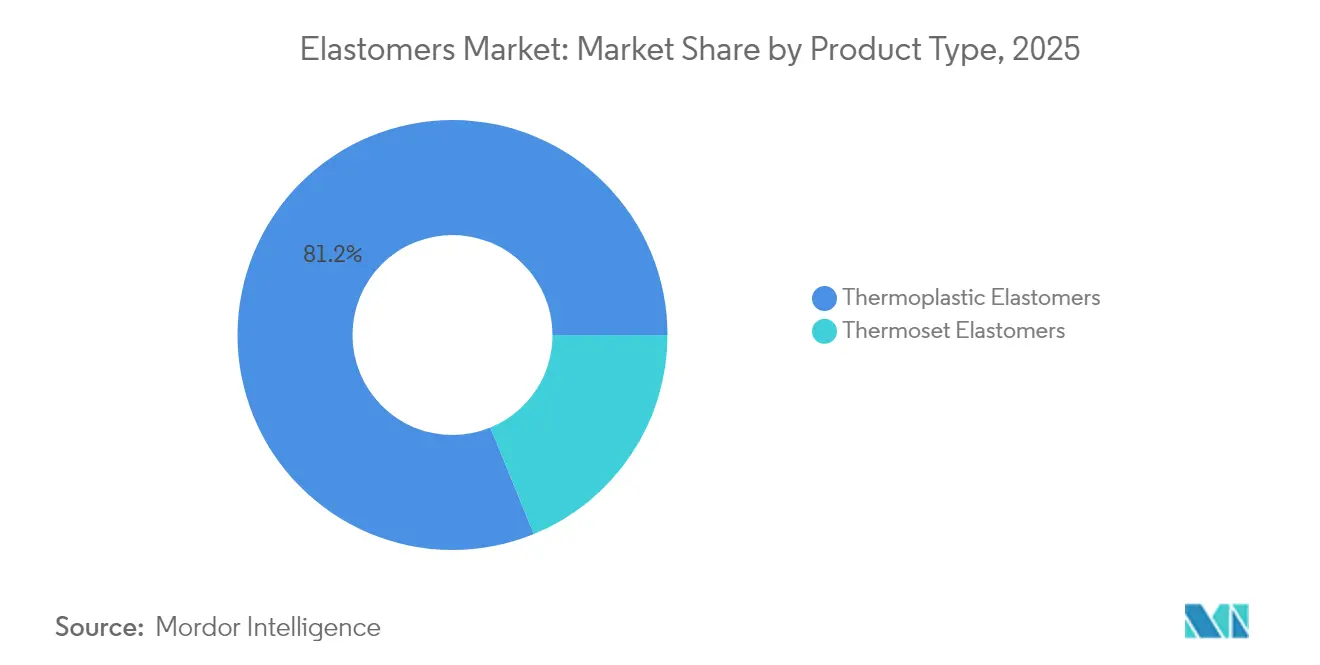

- By product type, thermoplastic elastomers led with 81.18% Elastomers market share in 2025; the segment is also projected to expand at 5.18% CAGR through 2031.

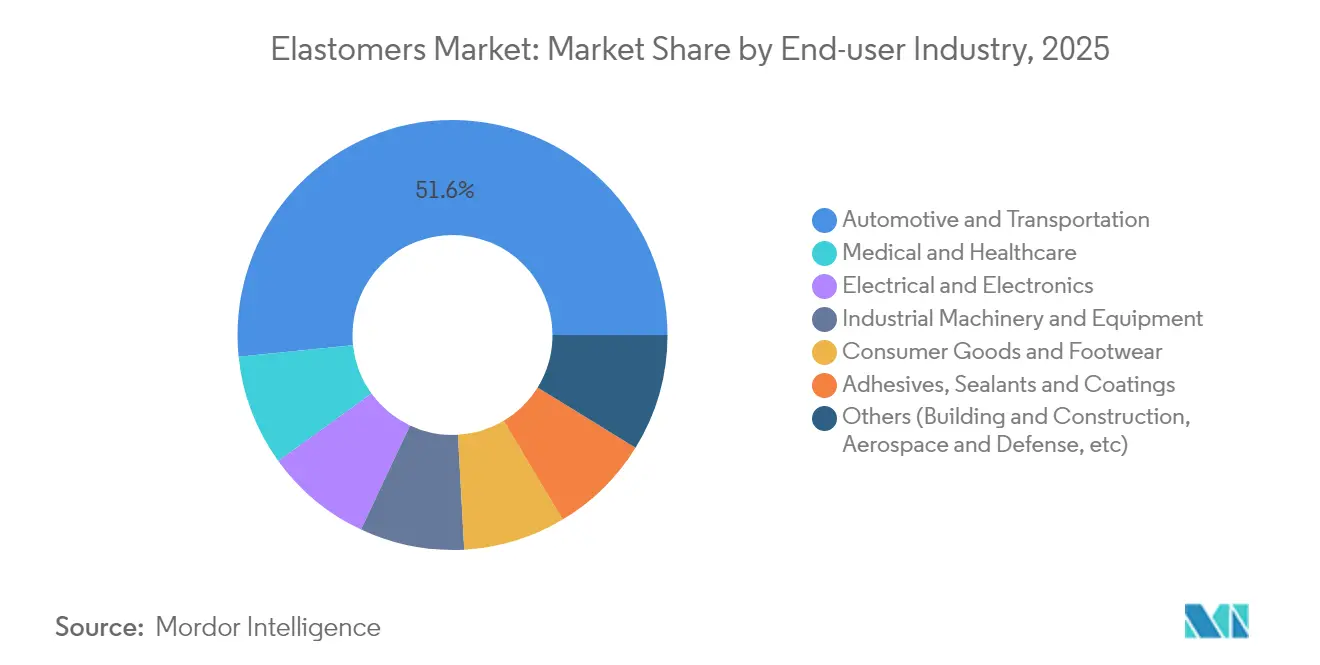

- By end-user industry, automotive and transportation captured 51.62% of the Elastomers market size in 2025, while medical and healthcare applications are advancing at the fastest 5.82% CAGR to 2031.

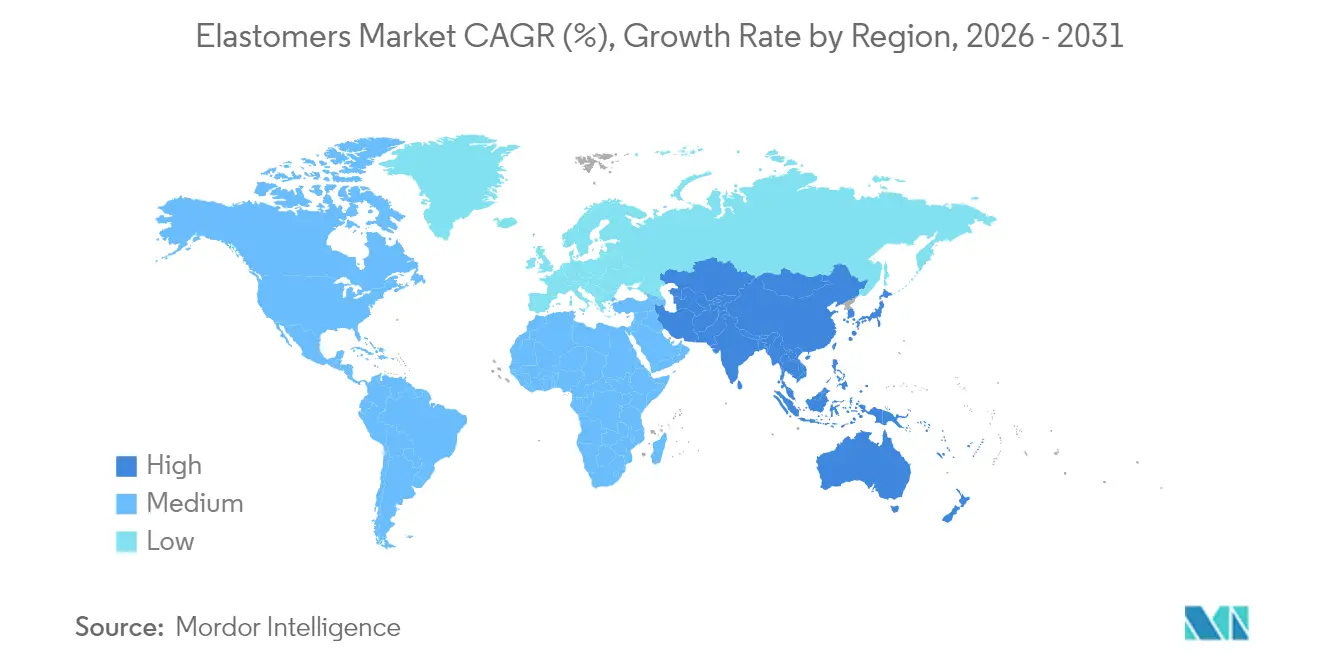

- By geography, Asia Pacific commanded 42.15% revenue share of the Elastomers market in 2025 and is projected to post the highest 6.27% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Elastomers Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for lightweighting and EV parts in automotive | +1.8% | Global, led by North America, Europe, and China | Medium term (2–4 years) |

| Expansion of construction and infrastructure in the Asia Pacific | +1.2% | Asia Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Rapid penetration of thermoplastic elastomers in flexible consumer electronics | +0.9% | Global, led by Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Surge in medical-grade PVC-free tubing applications | +0.7% | North America and EU regulatory markets | Medium term (2–4 years) |

| Emergence of recycling-compatible circular TPE grades | +0.4% | Europe and North America are sustainability-focused markets | Long term (≥ 4 years) |

| Additive manufacturing demand for elastomeric filaments | +0.2% | Global, early uptake in aerospace and medical | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Lightweighting and EV Parts in Automotive

Electric-vehicle makers rely on advanced elastomers to shave kilograms from battery housings, suspension boots, and fluid-handling lines, which directly boosts driving range. Materials such as Hytrel TPC LCF cut carbon footprints by 50% compared with incumbent polymers, yet keep flexibility under low-temperature shock. Commercial fleet owners echo the same need in heavy-duty packs, fueling multi-year programs for high-temperature gaskets and vibration isolators. Even in a year when global light-vehicle sales slipped, OEMs funneled research and development budgets toward lightweight sealing solutions, creating a counter-cyclical lift for the Elastomers market. Cooper Standard’s Fortrex platform highlights the trend with a 53% mass reduction versus EPDM while extending service life. Charging-station manufacturers add to demand because elastomeric over-mold parts must tolerate thermal cycling during fast charging.

Expansion of Construction and Infrastructure in Asia-Pacific

High-rise projects and mega-transport corridors across China, India, and Southeast Asia use elastomeric sealants to enable movement joints, glazing systems, and waterproof membranes that maintain building envelope integrity under seismic loads. Government green-building codes reward the use of low-VOC, energy-saving materials, turning high-performance TPE and PU sealants into default specifications. Covestro’s recent capacity ramp-up in Taiwan for cast polyurethane elastomers is aimed at equipment used in automated factories and wind-turbine components, reinforcing regional self-sufficiency. Smart-city investments generate incremental pulls from sensor housings and air-quality monitors that require UV-stable elastomer skins. Contractors favor locally compounded grades to avoid shipping delays, giving global suppliers a reason to co-locate with end-markets in the Elastomers market.

Rapid Penetration of Thermoplastic Elastomers in Flexible Consumer Electronics

Device brands exploring foldable displays, soft wearables, and haptic feedback surfaces need stretchable yet optically clear polymers. Transparent SEBS-based composites record 182% crack-onset strain while preserving 95% light transmission, paving the way for skin-like electronics. TPEs also solve EMI-shielding challenges through conductive filler packages engineered for micro-molding. KRAIBURG TPE’s skin-contact grades underscore convergence between consumer tech and medical wearables by meeting ISO 10993 biocompatibility norms. As component sizes shrink, designers value the shot-to-shot consistency of TPE over liquid silicone, giving the Elastomers market a fresh pipeline of high-margin applications.

Surge in Medical-Grade PVC-Free Tubing Applications

Health-care providers in North America and Europe are phasing out DEHP-plasticized PVC due to leaching risks, turning to thermoplastic elastomer tubing that withstands gamma, e-beam, and steam sterilization cycles. Teknor Apex reports its Medalist TPEs expand peristaltic pump life while resisting aggressive cleaning chemistries. Single-use bioprocess bags, IV sets, and catheter components benefit from consistent bonding to PP and PE connectors, avoiding adhesives. Shore 00 ultra-soft TPEs introduced by KRAIBURG TPE enable patient-friendly prosthetic liners that distribute pressure more evenly. Regulatory approvals move swiftly because TPEs are halogen-free, accelerating penetration in the Elastomers market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude oil and feedstock prices | -1.4% | Global, higher impact where the feedstock is imported | Short term (≤ 2 years) |

| Stricter micro-plastic and tire-wear regulations | -0.8% | Europe and North America first movers | Medium term (2–4 years) |

| Performance gap of bio-based elastomers at high temperature | -0.6% | Global, affects auto and industrial uses | Long term (≥ 4 years) |

| Supply-chain concentration of specialty monomers | -0.4% | Global, high vulnerability in Asia Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude Oil and Feedstock Prices

Producers such as BASF implemented 8–10 cents per pound surcharges on key diols to maintain margins. Tight supply obliges converters to balance inventories carefully, and some shift sourcing to bio-based feedstocks, although volumes remain limited. The volatility clouds budgeting and can postpone capital expenditure, dampening near-term expansion of the Elastomers market.

Stricter Micro-Plastic and Tire-Wear Regulations

The EU’s proposed Euro 7 rules include tire abrasion limits, forcing compounders to measure wear rates under harmonized UN tests[1]European Rubber Journal, “Euro 7 Proposal Tightens Tire Wear Limits,” european-rubber-journal.com. Studies attribute over 35% of marine microplastics to tire particles, triggering international calls for reformulated tread polymers. In the United States, EPA standards set particulate ceilings that compel upgrades to capture systems by 2027[2]Federal Register, “NESHAP for Rubber Tire Manufacturing,” federalregister.gov . Complying with these frameworks adds research and development, and capital costs, which can temporarily slow project launches in the Elastomers market until new grades clear validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Thermoplastic Grades Reinforce Circular Economy Gains

Thermoplastic elastomers not only own 81.18% share of the Elastomers market but also log the fastest 5.18% CAGR to 2031, thanks to closed-loop reprocessability that helps OEMs hit recycling targets. This dominance means every major automotive window seal, wire harness grommet, and wearable band increasingly relies on TPE, often replacing cross-linked rubber to shorten molding cycles.

Thermoset elastomers maintain footholds where temperatures exceed 150 °C, for instance, in turbocharger hoses and oil-field packers. Yet even in these niches, hybrid concepts mix TPE outer layers with vulcanized cores to marry chemical resistance with recyclability. Research investment, therefore, centers on nucleating agents, block-copolymer design, and catalyst systems that lift the service temperature of TPE beyond 180 °C without eroding fatigue life. Such advances are expected to channel additional revenue into the Elastomers market while helping processors meet take-back mandates.

By End-User Industry: Medical Overtakes Consumer Electronics in Growth Velocity

Automotive and transportation still accounts for 51.62% of the Elastomers market in 2025 because every vehicle contains more than 200 sealing, NVH, and fluid-handling parts made from the material class. The segment adds incremental volume through EV battery packs where dielectric strength and puncture resistance matter. At the same time, the medical and healthcare vertical expands at a 5.82% CAGR, the fastest within the Elastomers industry, supported by global regulatory bans on DEHP-plasticized PVC in infusion systems. This growth shifts the revenue mix toward higher-margin specialty grades that must secure USP Class VI and ISO 10993 clearance.

Geography Analysis

Asia Pacific captures 42.15% of the Elastomers market and outpaces all other regions with a 6.27% CAGR. China remains the centerpiece, channeling elastomers into high-speed rail gaskets, appliance seals, and tire plants clustered along the Yangtze River Delta. India’s state-sponsored industrial corridors likewise lift demand for vibration-dampening mounts used in capital equipment, while Southeast Asia’s electronics clusters consume heat-resistant over-mold compounds for smartphones and tablets.

North America sustains the Elastomers market through its integrated supply chain for light vehicles, medical devices, and shale-gas infrastructure. Policy incentives for domestic EV battery plants intensify the procurement of flame-retardant TPE gaskets that seal cell enclosures. Europe pivots heavily toward sustainability, driving the adoption of bio-attributed EPDM and TPE blends verified under ISCC PLUS mass-balance systems.

South America, the Middle-East, and Africa post steady gains in infrastructure spending. Brazil’s polyurethane output ranks fourth globally, while Gulf energy projects need sour-gas-resistant elastomer seals. Although smaller in absolute terms, these regions provide long-run upside as supply-chain localization continues.

Competitive Landscape

The market is highly fragmented. Specialists carve growth by solving niche pain points. Competitive intensity now revolves around ESG credentials as much as cost. Early movers in chemical recycling forge brand partnerships with consumer-electronics giants eager to publicize circular-material stories. Meanwhile, tire makers race to meet Euro 7 wear limits by combining silica-rich tread recipes with functionalized SSBR that cuts rolling friction and particle shedding. Such demands keep the Elastomers market focused on high-performance, specialty applications rather than pure volume growth.

Elastomers Industry Leaders

Dow

ARLANXEO

BASF

Covestro AG

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: LANXESS has sold its Urethane Systems business to UBE Corporation, marking a strategic shift. This move completes LANXESS’s transition toward a stronger focus on specialty additives.

- April 2025: Kuwait Petroleum’s subsidiary took a 25% stake in Wanhua Chemical Group in China, expanding combined reach in isocyanate and elastomer value chains.

- February 2025: Dow launched bio-based NORDEL REN EPDM produced via ISCC PLUS-certified mass-balance feedstocks, targeting automotive seals and infrastructure gaskets.

Global Elastomers Market Report Scope

The elastomer is a high-molar-mass polymeric material with elasticity characteristics, allowing it to regain its original shape after deformation. Thermoset elastomers are widely used in the production of tire rubbers, and thermoplastic elastomers are used in manufacturing sealants, hoses, and tubes by injection molding. The elastomers market is segmented by product type, application, and geography. By product type, the market is segmented into thermoset elastomers and thermoplastic elastomers. By application, the market is segmented into automotive, sports, electronics, industrial, adhesives, and other applications. The report also covers the market size and forecasts for the market in 15 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

By Product Type

| Thermoplastic Elastomers |

| Thermoset Elastomers |

By End-user Industry

| Automotive and Transportation |

| Electrical and Electronics |

| Medical and Healthcare |

| Industrial Machinery and Equipment |

| Consumer Goods and Footwear |

| Adhesives, Sealants and Coatings |

| Others (Building and Construction, Aerospace and Defense, etc) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Thermoplastic Elastomers | |

| Thermoset Elastomers | ||

| By End-user Industry | Automotive and Transportation | |

| Electrical and Electronics | ||

| Medical and Healthcare | ||

| Industrial Machinery and Equipment | ||

| Consumer Goods and Footwear | ||

| Adhesives, Sealants and Coatings | ||

| Others (Building and Construction, Aerospace and Defense, etc) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global Elastomers market?

The Elastomers market size is USD 108.48 billion in 2026.

How fast will the Elastomers market grow through 2031?

Market value is projected to rise to USD 137.53 billion by 2031 at a 4.86% CAGR.

Which product segment leads the Elastomers market?

Thermoplastic elastomers hold 81.18% share and also record the quickest 5.18% CAGR.

Why is Asia Pacific pivotal for elastomer demand?

The region combines large manufacturing hubs with booming construction, giving it 42.15% share and the fastest 6.27% CAGR.

What regulatory trends are shaping elastomer innovation?

Stricter limits on microplastic emissions and mandates for circular materials push suppliers to develop low-wear, recyclable and bio-based grades.

Page last updated on: