Industrial Polyurethane Elastomer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

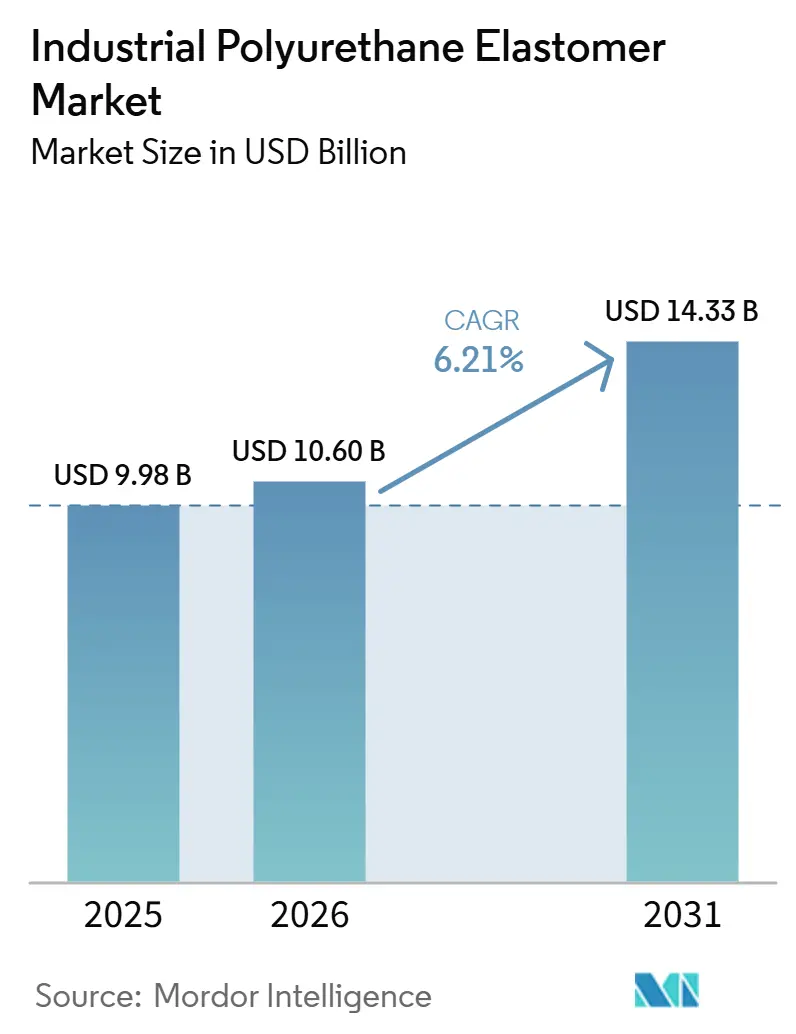

| Market Size (2026) | USD 10.60 Billion |

| Market Size (2031) | USD 14.33 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Polyurethane Elastomer Market Analysis by Mordor Intelligence

The Industrial Polyurethane Elastomer Market size was valued at USD 9.98 billion in 2025 and is estimated to grow from USD 10.60 billion in 2026 to reach USD 14.33 billion by 2031, at a CAGR of 6.21% during the forecast period (2026-2031). Robust demand for abrasion-resistant, high-load, and chemical-stable elastomers in mining, oil and gas, and automated-warehouse systems is driving consistent revenue growth. Thermoset castable grades remain critical for producing large, highly customized parts, while thermoplastic polyurethane (TPU) is gaining market share in applications where short cycle times, recyclability, and closed-loop processing are essential. Rapid automation across Asia-Pacific, the localization of elastomer supply chains in emerging economies, and ongoing lightweighting in transportation equipment are supporting revenue growth. The industrial polyurethane elastomer market continues to benefit from the material’s superior low-temperature flexibility and elastic memory, which outperform conventional rubber and many advanced thermoplastic elastomers in extreme service conditions.

Key Report Takeaways

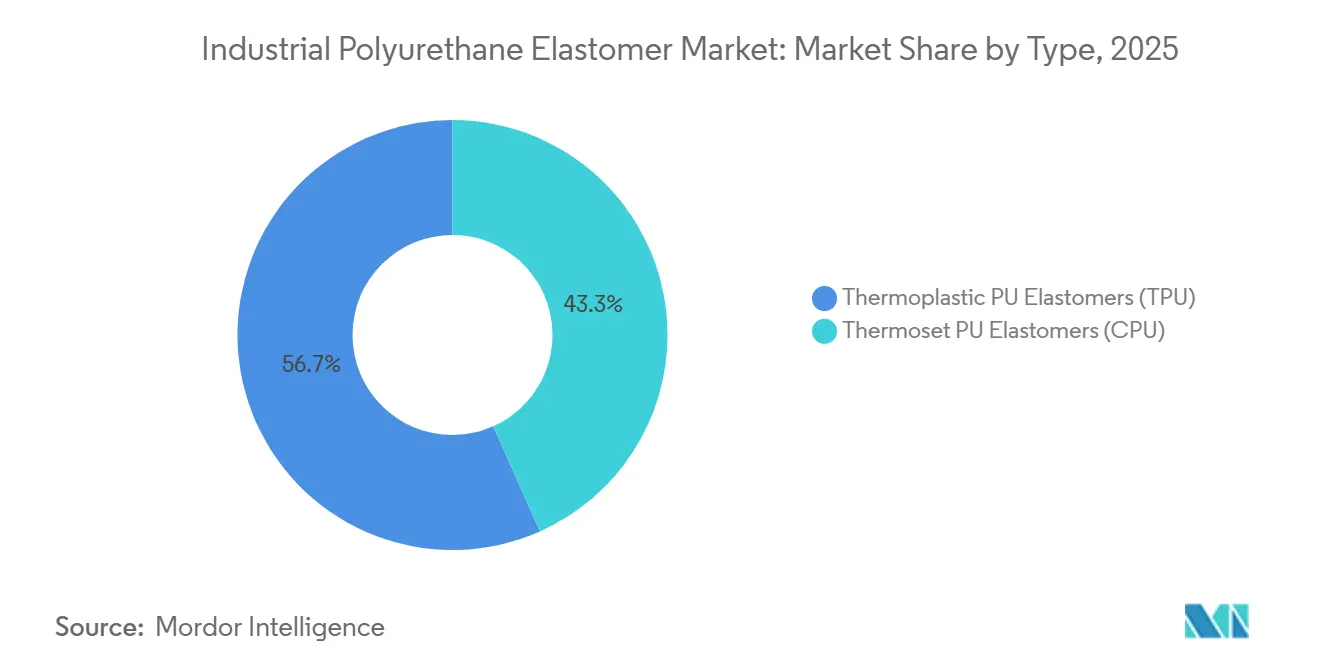

- By type, thermoplastic PU elastomers (TPU) held 56.67% of the industrial polyurethane elastomer market share in 2025 and are forecast to grow at a 6.89% CAGR through 2031.

- By processing technology, injection molding led with 39.66% of the industrial polyurethane elastomer market share in 2025, while other processing technologies (compression, blow, etc.) are projected to record the fastest 6.90% CAGR through 2031.

- By application, wheels and rollers dominated with 31.11% of the industrial polyurethane elastomer market share in 2025; vibration and shock-absorbing components are advancing at a 7.12% CAGR through 2031.

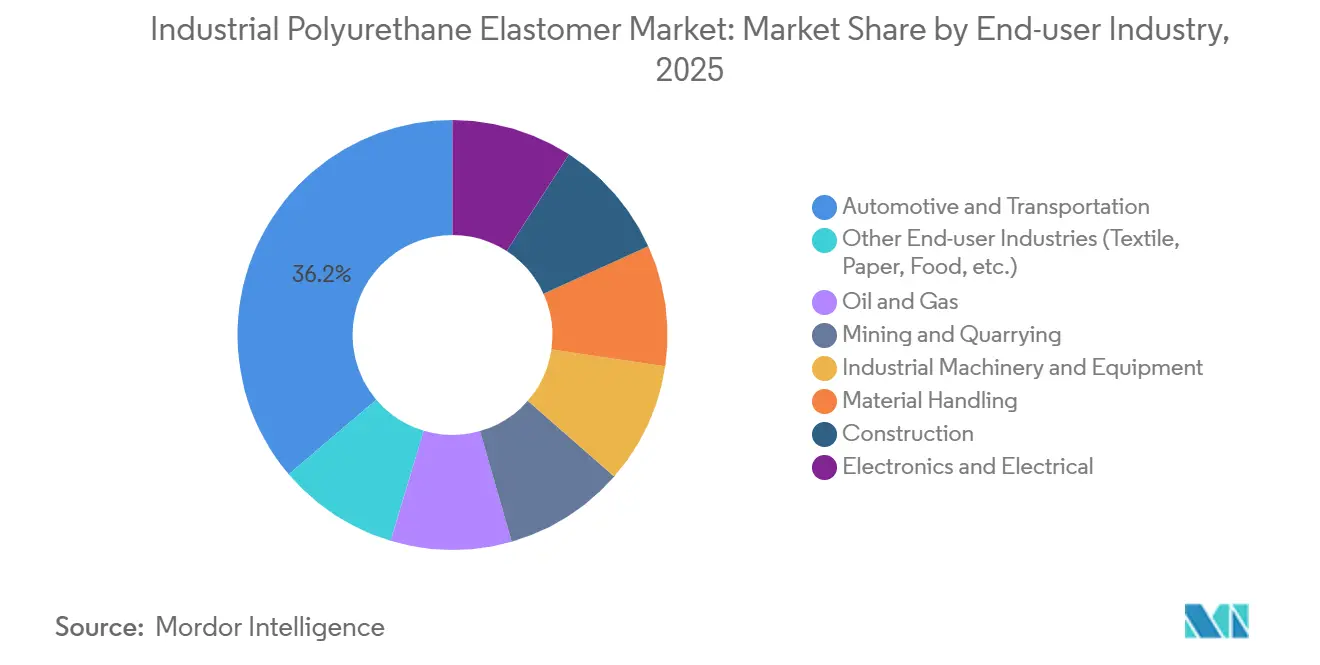

- By end-user industry, automotive and transportation contributed 36.21% of the industrial polyurethane elastomer market share in 2025, whereas electronics and electrical is the fastest-growing segment at a 7.23% CAGR through 2031.

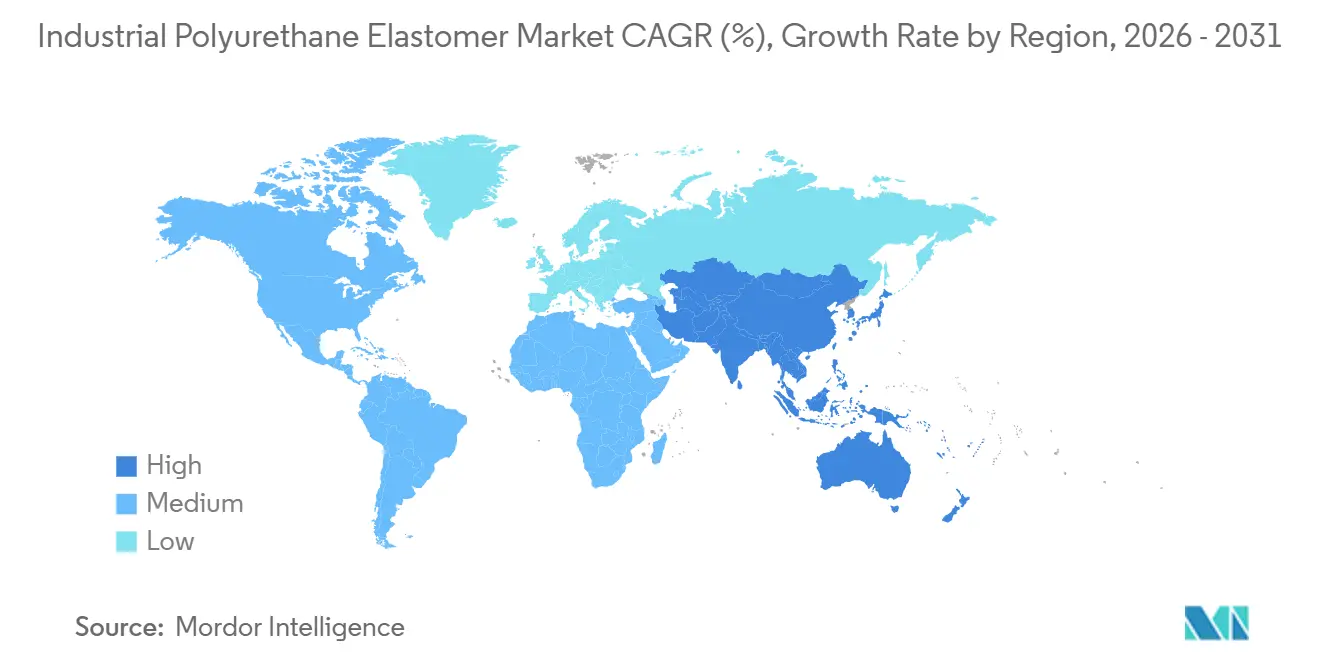

- By geography, Asia-Pacific generated 46.67% of the industrial polyurethane elastomer market share in 2025 and is forecast to register a 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Polyurethane Elastomer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of oil and gas exploration equipment using polyurethane parts | +1.2% | Global, with concentration in North America (Gulf of Mexico, Permian Basin), Middle-East (Saudi Arabia, UAE), and offshore Asia-Pacific (Malaysia, Australia) | Medium term (2-4 years) |

| Light-weighting via metal-PU hybrids in heavy machinery | +1.4% | North America and Europe (automotive, construction equipment), APAC core (China, India industrial machinery) | Long term (≥ 4 years) |

| Industrial automation needs high-load vibration damping | +1.5% | APAC core (China, South Korea electronics assembly), North America (warehouse automation), Europe (automotive robotics) | Short term (≤ 2 years) |

| 3D-printed PU elastomer tooling for rapid industrial prototyping | +0.8% | North America and Europe (aerospace, automotive RandD), emerging in APAC (China's additive manufacturing hubs) | Medium term (2-4 years) |

| On-site spray-elastomer linings for asset life extension | +1.0% | Global, with early adoption in mining regions (Australia, South America), oil and gas infrastructure (Middle-East, North America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Oil and Gas Exploration Equipment Using Polyurethane Parts

Polyurethane seals, pipeline pigs, and cable protectors exhibit excellent resistance to hydrocarbon immersion and temperatures below -40 °C, replacing nitrile and fluoroelastomers in subsea projects. Cast elastomers with Shore A 70-95 hardness ratings extend the service life of abrasive slurry pumps by up to 300%, reducing downtime for offshore operators.

Light-Weighting via Metal-PU Hybrids in Heavy Machinery

Bonding polyurethane sleeves to aluminum or steel cores reduces unsprung mass while maintaining the required stiffness for suspension bushings and cab mounts. BASF’s Cellasto components achieved a 2.4% improvement in NVH (noise, vibration, and harshness) performance during a 2024 test program, leading to a EUR 100 million investment in a new Cellasto plant in India, scheduled to begin operations in 2026[1]BASF, “Cellasto NVH Performance Results,” basf.com.

Industrial Automation Needs High-Load Vibration Damping

Automated-guided vehicles require wheels capable of sustaining loads above 500 kg while maintaining positional accuracy within ±2 mm. Polyurethane casters have been shown to reduce floor vibration by 35% compared to nylon alternatives, enabling continuous 24/7 operation in warehouse environments.

3D-Printed PU Elastomer Tooling for Rapid Industrial Prototyping

Additive manufacturing of TPU grades such as EPU 43 achieves tensile strengths of approximately 45 MPa and elongations exceeding 600%, significantly reducing fixture development lead times from weeks to days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU REACH restrictions on di-isocyanates | -0.9% | Europe (Germany, France, Italy, UK, NORDIC countries), with spillover compliance in export-oriented APAC and North America suppliers | Short term (≤ 2 years) |

| Advanced TPEs (PEBA, TPU alloys) as substitutes | -0.6% | Global, with concentration in North America and Europe, medical/automotive, APAC electronics | Medium term (2-4 years) |

| Insurance-driven flammability concerns in underground mining | -0.3% | Australia, South America (Chile, Peru, Brazil), South Africa, North America (coal regions) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU REACH Restrictions on Di-Isocyanates

Under EU REACH regulations effective August 2023, all European workers handling MDI or TDI must complete certified training, increasing compliance costs and encouraging OEMs to shift toward TPU, where injection molding can replace hand-cast CPU parts[2]ISOPA, “Di-isocyanate Training Requirements,” isopa.org.

Advanced TPEs (PEBA, TPU Alloys) as Substitutes

Advanced thermoplastic elastomers (TPEs), such as PEBA, provide superior performance, including flexibility at -40 °C and resistance to repeated steam sterilization, reducing polyurethane’s market share in premium medical tubing and performance footwear. Additionally, TPU alloys that optimize hard-segment ratios offer comparable damping properties with simpler processing, intensifying competition for conventional polyurethane suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Customizable Thermoset Grades Sustain Leadership

Thermoplastic polyurethane (TPU) elastomers accounted for 56.67% of the industrial polyurethane elastomer market share in 2025 and are projected to grow at a 6.89% CAGR through 2031. This segment leads in applications such as low-volume, heavy-duty screens, large rollers, and bespoke seals requiring tolerances exceeding ±5 mm. Cast processing enables shore hardness customization from 40A to 75D and facilitates the integration of fiber or microsphere fillers without shear-heating challenges. The growth of thermoplastic TPU is supported by recyclability mandates; Dow’s SPECFLEX CIR line, launched in 2025, incorporates up to 65% recycled TPU while maintaining tensile strength benchmarks.

Thermoplastic TPU benefits from injection molding efficiency and compliance with circular economy requirements, particularly in automotive trim and electronics housings. However, cast polyurethane (CPU) retains an advantage in applications requiring extreme abrasion resistance, oversized parts, and complex chemistries that demand on-site processing flexibility. The ISO 7425-1:2021 standardization of hardness and compression-set tests enhances cross-supplier comparability and mitigates risks in large-asset procurement for industries such as mining and offshore platforms.

By Processing Technology: Injection Molding Leads, Hybrid Methods Accelerate

Injection molding held a 39.66% market share in 2025 due to its ability to produce precise geometries with minimal finishing. A 2024 study demonstrated that increasing barrel temperatures from 190 °C to 210 °C improved tensile strength by 12%, underscoring the importance of process parameters in optimizing TPU performance. Casting remains essential for manufacturing parts exceeding typical press capacities and for rapid field repairs. Other processing technologies, including compression and blow molding, are expected to grow at a 6.90% CAGR through 2031, driven by advancements in multi-component molding that combine soft-touch skins with structural cores in a single process.

Continuous extrusion is widely used for belts and tubing, where market growth is linked to improved material homogeneity and uninterrupted production. Additionally, digital process controls and closed-loop metering are lowering barriers for small fabricators to adopt hybrid platforms, redistributing market share toward agile regional processors.

By Application: Wheels and Rollers Dominate, Damping Components Surge

Wheels and rollers accounted for 31.11% of the industrial polyurethane elastomer market size in 2025. Polyurethane casters offer a 40% longer service life compared to rubber alternatives in high-speed conveyors, reducing total ownership costs for food and electronics manufacturing facilities. Vibration and shock-absorbing components are projected to grow at the fastest CAGR of 7.12% through 2031, driven by applications in electric vehicle chassis and precision robotics, where damping coefficients are critical for electronics durability.

Other applications, including belts, couplings, seals, and gaskets, also contribute to demand. For example, Gates’ Poly Chain GT2 belts utilize polyurethane teeth to maintain timing accuracy over millions of cycles. High-pressure hydraulic seals made from TPU can withstand pressures of 45-55 MPa without extrusion, serving industries such as drilling and earth-moving equipment.

By End-user Industry: Transportation Dominates, Electronics Gains Momentum

The automotive and transportation industry accounted for 36.21% of demand in 2025, driven by the material’s effectiveness in noise, vibration, and harshness (NVH) isolation, suspension bushings, and timing belts that operate in temperature ranges from -40 °C to +120 °C. Electric vehicle drivetrains are intensifying these requirements, particularly for high-frequency damping. The electronics and electrical segment is expected to grow at a 7.23% CAGR through 2031, fueled by the demand for wearable sensors and flexible circuits that rely on biocompatible, sub-millimeter TPU housings.

Emerging technologies, such as MXene-reinforced waterborne polyurethane films with strain sensitivities of 12.5 over 10,000 cycles, are opening new opportunities in smart wearables. Meanwhile, oil and gas, mining, and industrial machinery continue to demand polyurethane for its abrasion and chemical resistance, while material-handling automation supports sustained volume growth in logistics hubs worldwide.

Geography Analysis

Asia-Pacific dominated with 46.67% revenue share in 2025 and is forecast to have the fastest 6.98% CAGR to 2031. Capacity expansions in China, such as Covestro’s Phase 1 Zhuhai TPU plant with a 30 kt/y capacity launched in 2026, are enabling local supply for industries including footwear, consumer electronics, and automotive. India’s increasing polyol consumption aligns with new Cellasto capacity expected to come online in 2026, strengthening vertical integration in South Asia. Japan and South Korea focus on supplying advanced electronics-grade TPU, while ASEAN nations capture demand for footwear and appliance assemblies relocating from coastal China.

North America maintains a strong market position, supported by automotive, oil and gas, and warehouse automation sectors. Dow’s 2025 expansion of propylene glycol production in Thailand secures upstream feedstock, complementing Huntsman’s planned increase in European systems capacity by 2026. Mexico’s near-shoring trend supports cast polyurethane NVH components for U.S. vehicle assembly lines.

In Europe, stringent REACH regulations on di-isocyanates are driving a shift toward TPU injection molding and pre-polymer systems with lower free-monomer content. Germany, France, and Italy anchor demand for advanced damping mounts and railway components, while Nordic countries emphasize bio-based polyols and halogen-free flame retardants for wind energy and cold-climate applications. Selected South American and Middle-Eastern markets utilize polyurethane in mining and petrochemical infrastructure, though growth is moderated by commodity cycle volatility.

Competitive Landscape

Five vertically integrated suppliers, including BASF, Covestro, Huntsman, Lanxess, and Dow, collectively held majority of the industrial polyurethane elastomer market share in 2025, leveraging captive MDI/TDI production and global formulation centers. Strategic initiatives, such as Wanhua’s 700 kt/y MDI line set to commence in Q2 2026, enhance cost efficiency and reduce lead times in Asia. BASF’s upcoming Indian Cellasto plant highlights the shift toward regional supply for NVH modules in automotive and industrial equipment.

Niche players like Era Polymers (Australia) and Herikon (Netherlands) secure contracts by offering on-site casting and rapid prototyping for offshore, mining, and marine projects where downtime costs are significant. UBE Corporation’s 2025 acquisition of LANXESS’s polyurethane business for USD 495 million expands its footprint in Europe and North America for specialty prepolymers. Innovations focus on bio-based polyols, self-healing matrices, and digitally enabled color matching, as OEMs prioritize lower carbon footprints and real-time quality monitoring. Patent activity in conductive, MXene-reinforced polyurethane dispersions indicates rising competition in the flexible electronics market.

With the top five suppliers holding 49% market share, the industry remains moderately concentrated, with opportunities for selective consolidation in commodity grades. Meanwhile, customization and application-specific engineering sustain a fragmented landscape of regional processors.

Industrial Polyurethane Elastomer Industry Leaders

BASF

Covestro AG

Dow

LANXESS

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Covestro AG strengthened its Cast Polyurethane (CPU) elastomers business network in Taiwan. The initiative targeted demand in automated equipment, smart logistics, offshore wind power, waterproofing for construction and infrastructure, and the pulp and paper industries, enhancing local service and sales support for advanced material systems and precision casting machines.

- October 2024: Lubrizol launched four biomass-balanced ESTANE RNW thermoplastic polyurethane (TPU) products, which aimed to reduce carbon footprints by up to 59% while retaining the performance characteristics of petroleum-based resins. Certified under the ISCC PLUS scheme, these materials supported sustainability in industrial applications without necessitating modifications to current production processes.

Global Industrial Polyurethane Elastomer Market Report Scope

Industrial polyurethane elastomers are durable and versatile materials available as thermoset or thermoplastic options. They provide superior load-bearing capacity, wear resistance, and elasticity compared to traditional materials like rubber, plastic, and metal. With excellent chemical and abrasion resistance, these elastomers are extensively utilized in heavy-duty applications, including molding, mining, automotive components, wheels, and protective industrial parts.

The Industrial Polyurethane Elastomers Market is segmented into type, processing technology, application, end-user industry, and geography. By type, the market is segmented into thermoplastic PU elastomers (TPU) and thermoset PU elastomers (CPU). By processing technology, the market is segmented into injection molding, casting, extrusion, and other processing technologies (compression, blow, etc.). By application, the market is segmented into wheels and rollers, belts and couplings, vibration and shock-absorbing components, seals and gaskets, machine components, mining screens and liners, and other applications. By end-user industry, the market is segmented into automotive and transportation, oil and gas, mining and quarrying, industrial machinery and equipment, material handling, construction, electronics and electrical, and other end-user industries (textile, paper, food, etc.). The report also covers the market size and forecasts for industrial polyurethane elastomers in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Thermoplastic PU Elastomers (TPU) |

| Thermoset PU Elastomers (CPU) |

| Injection Molding |

| Casting |

| Extrusion |

| Other Processing Technologies (Compression, Blow, etc.) |

| Wheels and Rollers |

| Belts and Couplings |

| Vibration and Shock-absorbing Components |

| Seals and Gaskets |

| Machine Components |

| Mining Screens and Liners |

| Other Applications |

| Automotive and Transportation |

| Oil and Gas |

| Mining and Quarrying |

| Industrial Machinery and Equipment |

| Material Handling |

| Construction |

| Electronics and Electrical |

| Other End-user Industries (Textile, Paper, Food, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Thermoplastic PU Elastomers (TPU) | |

| Thermoset PU Elastomers (CPU) | ||

| By Processing Technology | Injection Molding | |

| Casting | ||

| Extrusion | ||

| Other Processing Technologies (Compression, Blow, etc.) | ||

| By Application | Wheels and Rollers | |

| Belts and Couplings | ||

| Vibration and Shock-absorbing Components | ||

| Seals and Gaskets | ||

| Machine Components | ||

| Mining Screens and Liners | ||

| Other Applications | ||

| By End-user Industry | Automotive and Transportation | |

| Oil and Gas | ||

| Mining and Quarrying | ||

| Industrial Machinery and Equipment | ||

| Material Handling | ||

| Construction | ||

| Electronics and Electrical | ||

| Other End-user Industries (Textile, Paper, Food, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the industrial polyurethane elastomer market?

The industrial polyurethane elastomer market stands at USD 10.60 billion in 2026 and is expected to reach USD 14.33 billion by 2031, reflecting a 6.21% CAGR from 2026.

Which type of polyurethane elastomer is growing fastest through 2031?

Thermoplastic PU elastomers (TPU) are projected to expand at a 6.89% CAGR to 2031 due to their customization flexibility.

Why is Asia-Pacific growing fastest through 2031?

Localized TPU capacity expansions in China and India, combined with rapid automation and automotive production, drive a 6.98% CAGR for the region through 2031.

How do EU REACH rules affect polyurethane processors?

Mandatory di-isocyanate training raises compliance costs and encourages a shift toward TPU injection molding in European applications.

Page last updated on: