Silicone Fluids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

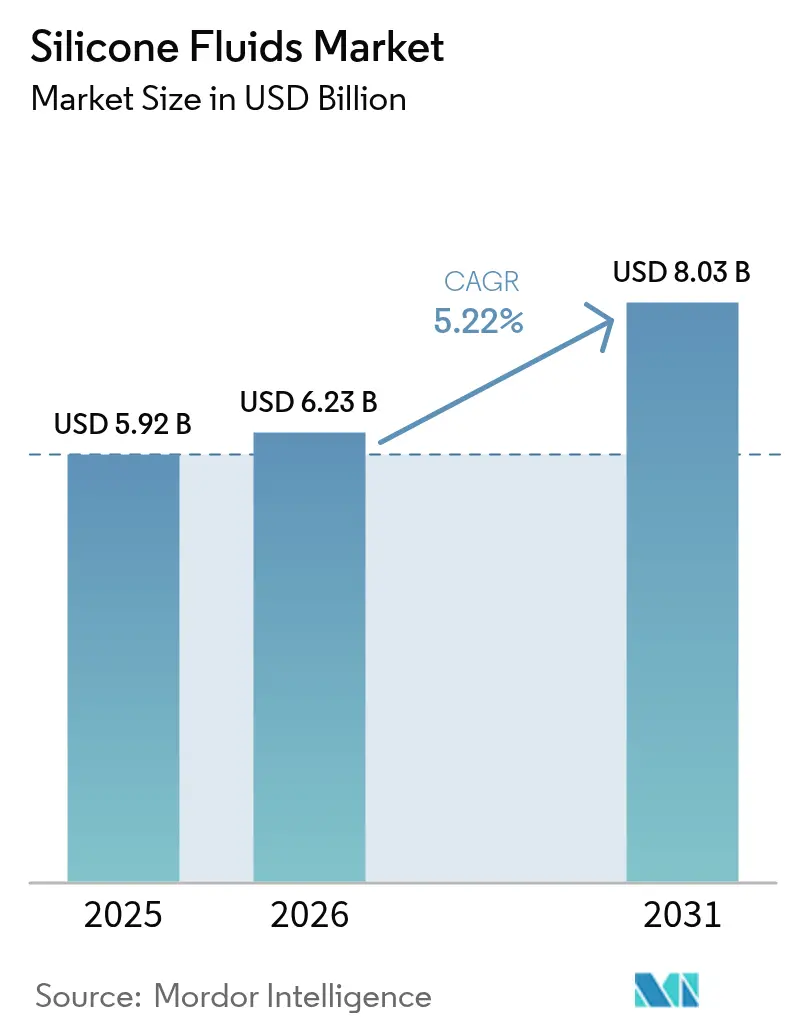

| Market Size (2026) | USD 6.23 Billion |

| Market Size (2031) | USD 8.03 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicone Fluids Market Analysis by Mordor Intelligence

Silicone Fluids market size in 2026 is estimated at USD 6.23 billion, growing from 2025 value of USD 5.92 billion with 2031 projections showing USD 8.03 billion, growing at 5.22% CAGR over 2026-2031. Demand for these high-performance polymers is climbing as OEMs and formulators look for fluids that stay stable under extreme temperatures, resist oxidation, and insulate electronics—capabilities that conventional mineral or synthetic hydrocarbons cannot match. Growth is further reinforced by the accelerating shift to electric mobility, the rise of hyperscale data centers, and regulatory moves that push manufacturers toward safer, more sustainable chemistries. Although raw-material volatility and tightening environmental standards temper momentum, the silicone fluids market continues to benefit from vertical integration initiatives, recycling investments, and niche-application innovation. Collectively, these forces position the silicone fluids market for steady mid-single-digit expansion over the next five years.

Key Report Takeaways

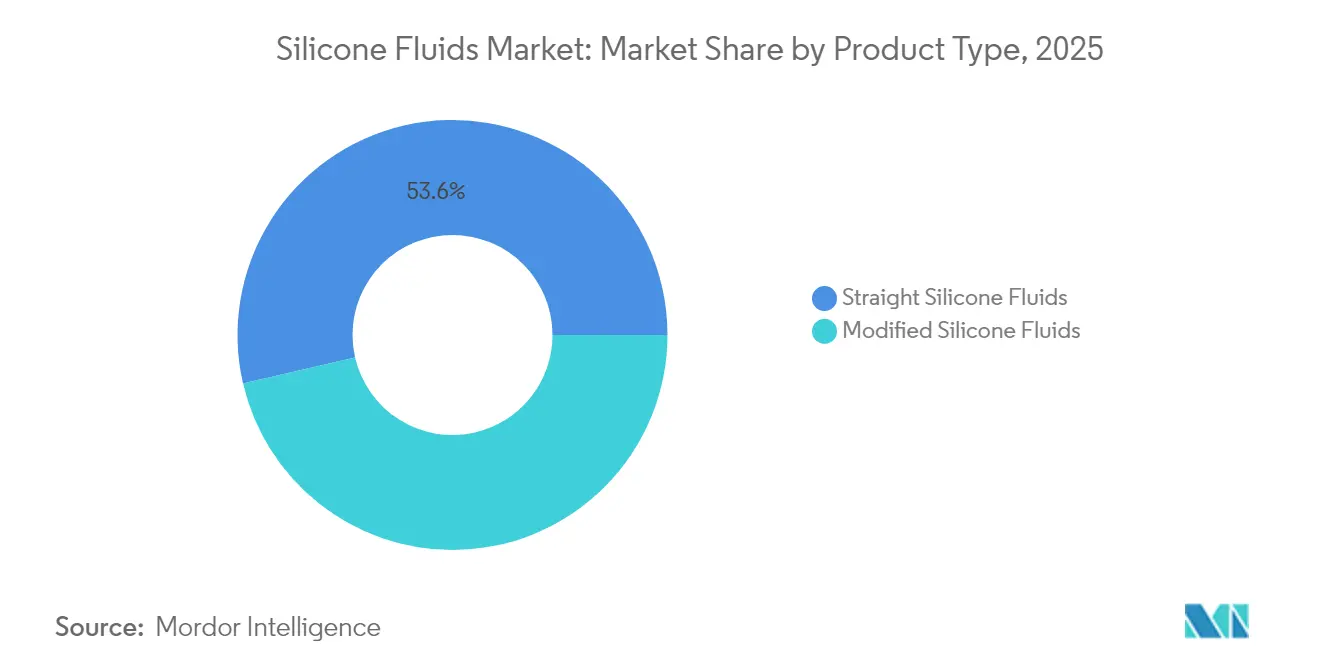

- By product type, straight fluids held 53.62% of the silicone fluids market share in 2025, while modified fluids are on track to post the fastest 6.72% CAGR through 2031.

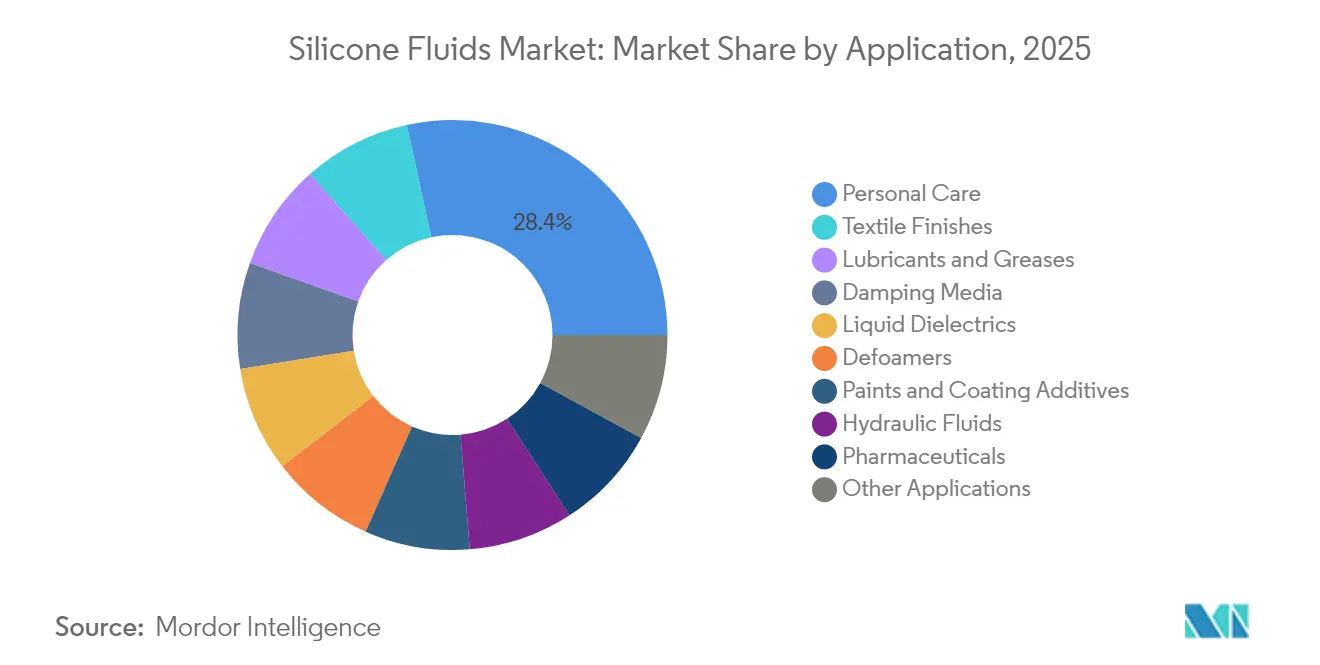

- By application, personal care commanded 28.41% share of the silicone fluids market size in 2025; textile finishes are projected to lead growth at 6.54% CAGR between 2026-2031.

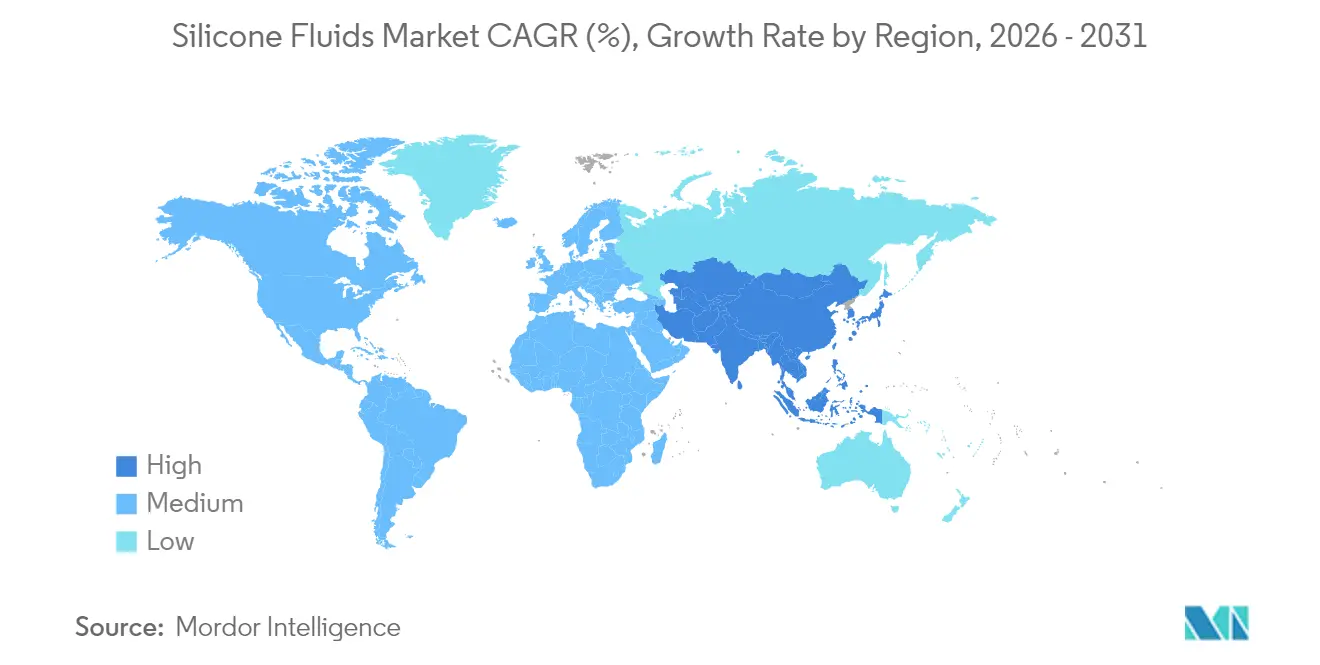

- By geography, Asia-Pacific accounted for 44.10% revenue share in 2025, and the region is forecast to expand at a 6.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicone Fluids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from personal care and cosmetics | +1.2% | Global, with EU regulatory shift driving innovation | Medium term (2-4 years) |

| Increasing adoption in electric vehicle thermal-management fluids | +0.8% | North America and APAC core, spill-over to EU | Long term (≥ 4 years) |

| Growth in high-performance lubricants for industrial automation | +0.6% | APAC manufacturing hubs, expanding to Americas | Medium term (2-4 years) |

| Liquid-immersion cooling of hyperscale data centres | +0.7% | Global, concentrated in major cloud regions | Short term (≤ 2 years) |

| Precision agriculture anti-foam agents for biostimulant mixtures | +0.4% | Americas and EU agricultural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Personal Care and Cosmetics

Formulators are moving quickly to replace restricted cyclic silicones with next-generation materials that marry sensory appeal and sustainability. Bio-based alkyl dimethicones from Siltech improve spreadability while cutting reliance on virgin fossil feedstocks. CHT Group’s BeauSil RE-AMO 919 EM incorporates over 94% recycled monomers to meet circular-economy targets without sacrificing emolliency. Expanding middle-class populations in Asia-Pacific are embracing premium multifunctional skin- and hair-care products, spurring demand for silicone fluids that deliver conditioning, barrier, and gloss benefits in a single blend. As brands tighten product portfolios, multifunctionality becomes a critical differentiator, and suppliers able to document lower carbon footprints gain preferred-supplier status.

Increasing Adoption in Electric Vehicle Thermal-Management Fluids

Liquid-cooled battery packs need dielectric fluids that suppress thermal runaway yet transfer heat efficiently. Lubrizol’s lifetime-fill silicone coolant exemplifies this shift by remaining stable for the full service life of an EV battery pack[1]Lubrizol, “Lifetime EV Battery Immersion Cooling Fluids,” lubrizol.com. China’s forthcoming GB 29743.2 conductivity threshold sets a high bar that conventional glycol-water blends cannot meet, steering automakers toward silicone-based formulations. Beyond batteries, wide-bandgap inverters, e-motors, and charging systems also benefit from the broad operating-temperature band of silicone fluids. Upstream, silicon metal demand tied to EV growth is rising 4.56% annually through 2030, rewarding vertically integrated producers that can secure raw supply.

Growth in High-Performance Lubricants for Industrial Automation

Servo-driven equipment and precision robotics require lubricants whose viscosity does not drift when plant temperatures swing. Silicone fluids deliver a flat viscosity–temperature curve and inherent dielectric protection, enabling in-line sensors to operate reliably within gearboxes. Food-processing and pharma plants—where PFAS restrictions are tightening—are migrating from fluorinated lubricants toward silicone alternatives that satisfy incidental-contact standards. Predictive-maintenance programs value the much longer drain intervals achievable with silicone fluids, lowering total cost of ownership despite higher per-litre pricing.

Liquid-Immersion Cooling of Hyperscale Data Centres

Next-generation AI servers push power densities above 100 kW per rack, forcing operators to abandon air cooling. Single-phase immersion systems built around silicone fluids achieve Power Usage Effectiveness as low as 1.02, while simplifying heat-capture architectures. Equipment makers collaborating with cloud leaders now design boards and connectors for full-time fluid contact, eliminating bulky heat sinks. With datacenter operators pledging net-zero roadmaps, the recyclability and low-toxicity profile of silicone fluids offers a compelling alternative to PFAS-based chemistries removed from the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicon metal and monomer prices | -1.1% | Global, with China price volatility affecting supply chains | Short term (≤ 2 years) |

| Stringent VOC and REACH compliance costs | -0.7% | EU primary impact, expanding to other regions | Medium term (2-4 years) |

| High supplier concentration in raw siloxanes | -0.5% | Global, with APAC manufacturing concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicon Metal and Monomer Prices

China controls roughly three-quarters of the world’s silicon metal output, creating a single-country risk that cascades through the silicone fluids market. Energy-price spikes, production curbs, and geopolitical frictions swing spot quotes, disrupting budgeting for downstream formulators. The United States is incentivizing domestic smelter projects under the Inflation Reduction Act, yet new capacity will not meaningfully come onstream before 2030. In the meantime, producers hedge with long-term supply contracts and evaluate backward integration, actions that demand capital many mid-sized players cannot muster.

Stringent VOC and REACH Compliance Costs

The European Chemicals Agency continues to tighten exposure limits for siloxanes, obliging manufacturers to invest in abatement systems, greener solvents, and extensive toxicological testing. Fragmented global standards compound complexity: a formulation cleared in the EU may still face new dossier requirements in Korea or Canada. Producers responding with low-VOC grades often accept higher synthesis cost or slightly reduced performance, squeezing gross margins until learning curves offset initial penalties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Modified Fluids Drive Innovation

Modified grades are expanding faster than unmodified counterparts, charting a 6.72% CAGR as formulators specify siloxanes with tailored side-chains, reactive sites, or crosslinkable groups. These custom molecules bond selectively to substrates, boost adhesion, or create hydrophobic surfaces, letting end-users hit performance targets without over-engineering. Demand is prominent in EV potting, conformal coatings, and high-flex textile inks. Straight polydimethyl-silicone grades nevertheless maintain volume leadership due to cost efficiency and broad spec inclusion. Their supply chains are mature, and continuous-process debottlenecking further reduces unit cost.

Competition is intensifying around sustainable production. Dow’s joint venture with Circusil brings a recycling loop able to cut PDMS carbon footprint by more than 50%. Wacker commissioned new Chinese fluid and emulsion lines in May 2025, adding high-purity capacity aimed at next-gen electronics. KCC’s 2024 purchase of Momentive broadens vertical reach from upstream siloxane monomers to downstream specialty fluids. As circular-economy targets harden, producers with closed-loop capabilities gain supply-award preference from global OEMs keen to certify Scope 3 reductions.

By Application: Personal Care Leadership Faces Textile Challenge

The personal-care domain represents the largest value pool, underpinned by skin- and hair-care brands that leverage silicone fluids for sensory and conditioning effects. EU restrictions on D5/D6 accelerate the switch to linear, branched, or bio-derived alternatives, raising formulation complexity yet opening premium-price niches. Asian consumers’ appetite for lightweight, non-sticky textures drives continuous new-product flow, keeping personal care at the front of the order book for many suppliers.

Textile finishing now posts the strongest growth, propelled by performance stretch fabrics, athleisure wear, and on-garment printing. Silicone-ink bases such as SILASTIC LCF 9600 M enable vibrant, crack-resistant elastomeric prints on high-elongation garments. Sustainability mandates also favor silicones because they cure at lower temperatures than PVC or plastisol systems, saving energy and mitigating worker exposure to phthalates. As fashion brands publicize restricted-substance lists, silicone formulations gain share across moisture-management coatings, durable water repellents, and soft-touch finishes.

Geography Analysis

Asia-Pacific dominates the silicone fluids market, leveraging integrated supply chains that begin with silicon metal smelting and culminate in finished formulations. China’s cost advantage and 75% raw-material control anchor the region’s leadership, while Japan and South Korea champion miniaturized electronics and memory semiconductors that require ultra-pure dielectric fluids. Southeast Asia is emerging as a manufacturing hedge, with Vietnam and Thailand courting foreign direct investment for specialty-chemical complexes. India, supported by domestic automotive build-out and an expanding personal-care sector, records double-digit local sales increases.

North America presents a different dynamic. The United States orchestrates supply-chain onshoring for critical minerals, while datacenter and EV build-outs propel specialty-fluid demand. Dow’s capacity expansion for silicone elastomers in Michigan supports regional customers seeking short lead times. ExxonMobil added high-viscosity synthetic base-stock capacity in Texas, signaling wider industrial acceptance of premium functional fluids. Canada supplies hydro-based metallurgical-grade silicon, and Mexico’s maquiladora corridor pulls in fluids for electronics assembly and automotive wiring harness production.

Europe contends with the strictest regulatory hurdles yet remains an innovation epicenter. Wacker forecasts 10% revenue growth in its Silicones division for 2025 as specialty grades offset lower commodity volumes. Germany’s engineering companies specify silicone damping media for machine tools, while France’s cosmetic houses pioneer upcycled silicone ingredients to meet imminent packaging and carbon-footprint rules. Nordic utilities’ green-power matrices lend credibility to circular-manufacturing claims, helping silicone fluid makers sell environmental value alongside technical performance.

Regulatory Landscape

Regulation for siloxanes is tightening across major end markets, increasing the compliance burden for silicone-fluid and silicone-based formulations. In the European Union, restrictions on cyclic siloxanes are extending into downstream products: the European Commission adopted a REACH amendment (EU) 2026/1289 on July 14, 2026 that sets a 0.1% (w/w) combined concentration limit for D4/D5 in silicone sealants placed on the EU market from January 1, 2027. South Korea also moved to lower volatile methyl siloxane thresholds, with the Ministry of Food and Drug Safety (MFDS) Notice No. 2026-11 (published May 3, 2026) reducing the combined D4/D5 limit in silicone sealants from 500 ppm to 350 ppm, effective October 1, 2026.

In the United States, oversight is progressing through both pesticide and industrial chemicals frameworks. Effective March 25, 2026, the US EPA finalized an exemption from tolerance requirements for methyl end-capped polydimethylsiloxane when used as an inert ingredient in pesticide formulations under 40 CFR 180.960, supporting continued use of PDMS-type silicone fluids in select agrochemical formulations. Separately, EPA released the Science Advisory Committee on Chemicals (SACC) final report on June 12, 2026 for the draft TSCA risk evaluation of D4, keeping scrutiny on cyclic siloxanes and reinforcing the shift by formulators toward high-purity, linear, and application-tailored silicone fluids to maintain market access under evolving labeling and exposure expectations.

Value Chain Analysis

The silicone fluids value chain starts with energy-intensive upstream inputs, particularly silicon metal (from quartz/silica reduction) and methyl chloride, alongside copper catalyst systems. These feedstocks are used in the Rochow-Muller direct process to produce methylchlorosilanes (notably dimethyldichlorosilane), followed by hydrolysis/condensation and polymerization to produce base polydimethylsiloxane (PDMS) fluids. Two manufacturing routes are common downstream: hydrolysis-condensation for high-volume industrial grades, and catalytic equilibrium polymerization for tighter molecular-weight control required in electronics, dielectric, and specialty formulations.

Midstream, producers and compounders upgrade base fluids into modified silicone fluids (reactive and non-reactive), emulsions, and application-specific packages, including thermal management fluids, defoamers, textile finishes, and personal care ingredients. Cost and availability risks concentrate around siloxane intermediates and silicon metal, with operating economics highly sensitive to monomer costs and supply stability, which strengthens the advantage of integrated players and long-term contracting. Downstream routes to market typically run through direct OEM and key-account supply for electronics, mobility, and industrial lubricants, while specialty distributors and formulators serve personal care, coatings, and agriculture, where documentation, purity control, and compliance data increasingly influence supplier selection.

Competitive Landscape

Industry concentration sits in the mid-range. The top five suppliers hold under 60% combined revenue, leaving room for regional specialists and integrated formulators. KCC’s Momentive acquisition consolidates R&D talent in structural silicones and optical fluids, potentially pressuring smaller independents that lack scale. Wacker and Dow lean into circular-economy messaging, unveiling recycling alliances and bio-based pilot plants that resonate with OEMs tracking Scope 3 emissions. Elkem capitalizes on Norway’s hydropower to differentiate its carbon footprint, marketing SILCOLAPSE and BLUESIL lines into agriculture and pharmaceuticals.

Technology is the chief battleground. PFAS exit paths, ultra-low-VOC coatings, and immersion-cooling chemistries demand polymer science and application testing that deter fast-follower copycats. Digital twins and AI-guided formulating accelerate customer co-development, shrinking lab iterations and winning sticky, multi-year supply contracts. Price competition persists in legacy straight-fluid grades, but specialized modified fluids command double-digit margins, shielding innovators from raw-material whipsaw.

Smaller players carve niches in localized supply or single-application mastery, such as anti-foam concentrates or optically clear encapsulants. These firms become acquisition targets once growth validates the niche, perpetuating a steady consolidation drumbeat that is likely to continue across the decade.

Silicone Fluids Industry Leaders

Dow Inc.

Wacker Chemie AG

Shin-Etsu Chemical Co., Ltd.

Momentive Performance Materials

Elkem ASA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is expanding where regulatory pressure and performance requirements intersect, pushing end users toward higher-purity and reformulated silicone fluid systems. The EU restriction on D5/D6 in 2024 has already accelerated substitution work in personal care, creating premium niches for linear, bio-based, and recycled-content silicone fluids such as Siltech bio-based alkyl dimethicones and CHT Group’s BeauSil RE-AMO 919 EM (over 94% recycled monomers). A parallel whitespace sits in low-VOC and low-VMS formulations across sealants, coatings, and inks as jurisdictions tighten siloxane limits, favoring suppliers that can provide validated impurity control and compliance documentation.

Industrial and electronics-led demand is being reinforced by investments and targeted product platforms rather than commodity expansion. Dow announced a USD 100 million program (June 2026) to expand specialty silicones manufacturing and innovation capabilities across the United States, China, and Japan through 2027, aligning capacity with engineered materials and electronics-adjacent applications. On the supply side in China, Inner Mongolia Hengxing Chemical completed registration (April 2026) for a high-performance organosilicon polymer expansion designed to add 20,000 tons of specialty silicone oil annually, illustrating continued build-out of specialty silicone oil capacity close to regional manufacturing clusters. In parallel, hyperscale data center immersion cooling and EV thermal management are creating qualification-driven demand for dielectric and thermal-interface silicone fluid systems, with product introductions such as Dow’s DOWSIL TC-3120 Thermal Gel for high-speed optical modules signaling expanding silicone use cases tied to dense electronics and heat management.

Recent Industry Developments

- June 2026: Dow announced a USD 100 million set of targeted investment projects through 2027 to expand specialty silicones manufacturing and innovation capabilities across the United States, China, and Japan. The program includes additions aligned to engineered materials and regional supply resilience, supporting shorter lead times for high-spec silicone materials used in electronics, mobility, and industrial applications.

- May 2025: Wacker commissioned new plants for silicone fluids in China to produce high-purity functional and non-functional silicone fluids, along with silicone emulsions. The added capacity supports electronics and specialty formulation demand, strengthening local supply in Asia-Pacific where integrated silicone value chains are concentrated.

- May 2024: KCC completed its acquisition of Momentive Performance Materials, expanding its silicone portfolio and vertical reach from upstream intermediates into downstream specialty materials. The combination strengthens scale in specialty silicone technologies and broadens the platform for application-focused silicone fluids and related formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers silicone fluids sold for industrial and consumer uses where the material stays in fluid form, including straight silicone fluids and modified silicone fluids, and measured as manufacturer level and channel level revenues in USD.

Scope exclusions: Silicone elastomers, silicone resins, and non-silicone substitute fluids are not counted, even if they serve similar end uses.

Segmentation Overview

- By Product Type

- Straight Silicone Fluids

- Poly-dimethyl Silicone Fluid

- Methylphenyl Silicone Fluid

- Methylhydrogen Silicone Fluid

- Other Straight Silicone Fluids

- Modified Silicone Fluids

- Reactive Silicone Fluid

- Non-reactive Silicone Fluid

- Straight Silicone Fluids

- By Application

- Lubricants and Greases

- Damping Media

- Liquid Dielectrics

- Hydraulic Fluids

- Defoamers

- Personal Care

- Paints and Coating Additives

- Textile Finishes

- Pharmaceuticals

- Other Applications

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the drivers behind silicone fluid demand in specific end uses, then linking those drivers back to measurable indicators. Public sources such as UN Comtrade trade statistics, USGS minerals and materials data, Eurostat industrial indicators, and OECD manufacturing series were reviewed to understand production and consumption direction in key regions.

Technical references were also used to sense check typical use rates, performance requirements, and substitution limits in applications like lubricants, dielectrics, defoamers, and personal care. NIST chemistry resources and peer reviewed journal articles were referenced for chemistry and performance context, while company filings, investor presentations, and reputable press were used to validate capacity additions, product mix commentary, and regional revenue exposure. Where available, a paid subscription for company financials and an import export shipment level database were used selectively to support cross checks on trade flows and supplier footprints. These sources are indicative and not exhaustive, and other public materials were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with manufacturers, distributors, formulators, and downstream users across major consuming industries. Because this is a global market, we covered APAC, EMEA, and the Americas to confirm regional demand shape, typical pricing movement, and the share of demand by application, and then revisited a few respondents when model outputs showed unusual jumps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | APAC: 46% |

| Mid tier: 53% | Functional/Unit leaders: 36% | EMEA: 29% |

| Smaller Players: 20% | Managers: 50% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where production and trade data were used to reconstruct the addressable silicone fluid pool by region and then split by product and application using interview validated shares. To keep totals realistic, selective bottom-up approximations were also run using supplier roll ups, sampled average selling price ranges, and volume checks for a few high visibility applications.

The model is anchored on market fingerprints that can be tracked consistently, such as regional manufacturing output trends, cosmetics and personal care production indicators, automotive and electronics output signals (linked to dielectrics and thermal management demand), and construction and coatings activity (linked to additives demand). Pricing direction was monitored through feedstock and energy signals plus supplier commentary, since silicone fluid pricing tends to move in steps rather than smoothly. Where data gaps exist for smaller countries, we used proxy indicators like import dependence, downstream industry size, and neighbor market ratios, and then adjusted with interview feedback.

For forecasting, scenario analysis was used with a base case as the main view, and then high and low cases were tested around variables like regional manufacturing growth, personal care demand resilience, and the speed of adoption in specialty applications. Assumptions were reviewed with market participants so the slope of demand and the pace of price change did not drift away from what practitioners expect.

Data Validation & Update Cycle

Outputs were validated through triangulation across application shares, regional totals, and independent signals such as trade movements and downstream production indicators. Variance checks were run when regional growth looked out of pattern, and those points were pushed back into the model only after the driver and the math were rechecked by another analyst.

If a major event occurs, such as a large capacity change, regulation impact, or a sharp input cost swing, we re contact sources and revisit assumptions so the time series remains internally consistent. Reports are refreshed annually, and before delivery we run a final update pass so clients receive the most recent view that fits the same definition and measurement logic.

Mordor Intelligence's Silicone Fluids Market Size Compared With Other Published Estimates

Published market sizes for silicone fluids can look different even when the topic name is the same, mainly because each publisher draws the scope lines in its own way and uses different price and volume assumptions. Differences also show up when base years do not match, or when growth is pushed by aggressive scenarios rather than a single base case.

The key gap drivers usually come from what is counted as silicone fluids versus adjacent silicone materials, how applications are mapped (for example, whether all personal care silicone ingredients are included), and how average selling prices are carried forward each year. Currency conversion timing and how quickly assumptions get refreshed after price shocks can also shift the reported USD value by a noticeable amount.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.23 B (2026) | |

| Industry Publisher A | USD 5.70 B (2024) | Uses an earlier baseline year and is typically read as a 2024 valuation, so later capacity additions and post-2024 pricing shifts are not reflected in the stated number. |

| Global Publisher B | USD 5.90 B (2025) | Often applies a different mapping of product scope and demand drivers, which can shift the application split and the implied ASP progression used to extend the series. |

The benchmark table shows a spread that is largely explained by base year alignment and what gets counted inside the silicone fluids bucket, and in Mordor Intelligence's model the total is built only from straight and modified silicone fluids across defined applications, with silicone elastomers and resins kept outside the calculation. When those choices are kept consistent year to year, the final value stays traceable to clear inputs and can be repeated with the same steps during updates.

Key Questions Answered in the Report

What is the current valuation of the silicone fluids market?

The silicone fluids market size is valued at USD 6.23 billion in 2026 and is on course to reach USD 8.03 billion by 2031.

Which segment leads the silicone fluids market by application?

Personal care holds the largest 28.41% share, thanks to widespread use in skin- and hair-care formulations.

Why are silicone fluids preferred for EV battery cooling?

Their wide operating-temperature window and excellent dielectric properties prevent thermal runaway while delivering reliable heat transfer.

How is regulation affecting silicone fluids in cosmetics?

The EU restricted cyclic silicones D5 and D6 in 2024, prompting formulators to switch to linear or bio-based alternatives.

Which region dominates the silicone fluids market growth through 2031?

Asia-Pacific leads with a 44.10% share and is forecast to grow at a 6.34% CAGR, driven by integrated supply chains and expanding manufacturing bases.

Page last updated on: