Liquid Silicone Rubber (LSR) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

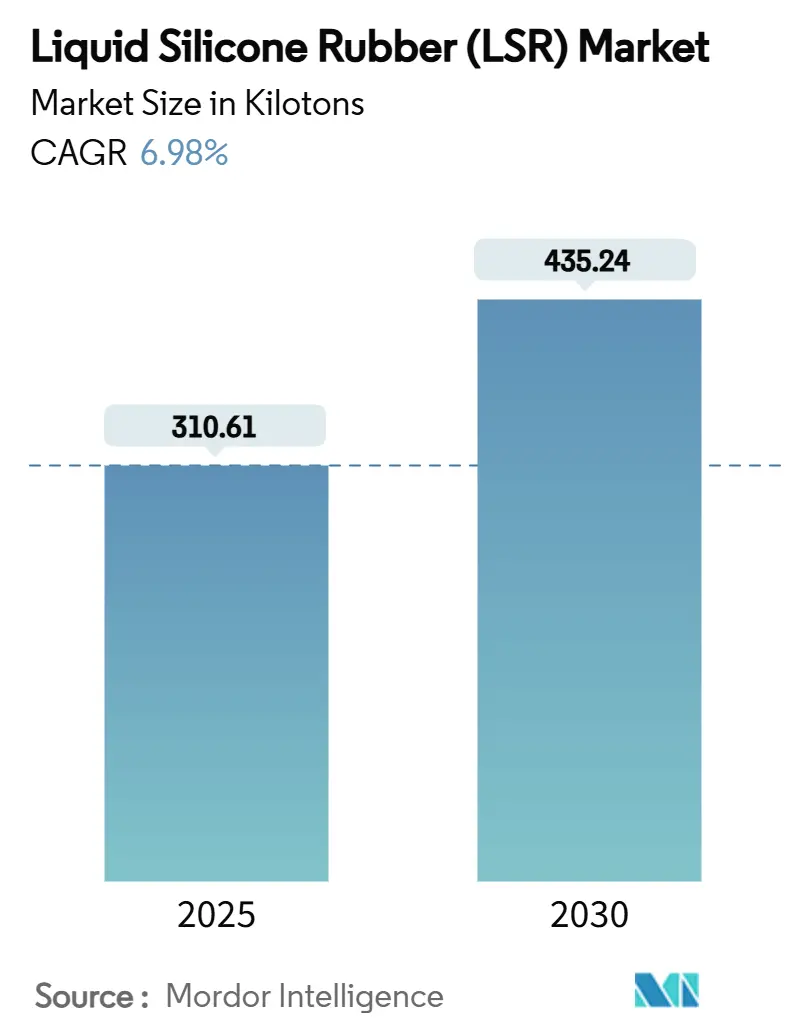

| Market Volume (2025) | 310.61 kilotons |

| Market Volume (2030) | 435.24 kilotons |

| Growth Rate (2025 - 2030) | 6.98% CAGR |

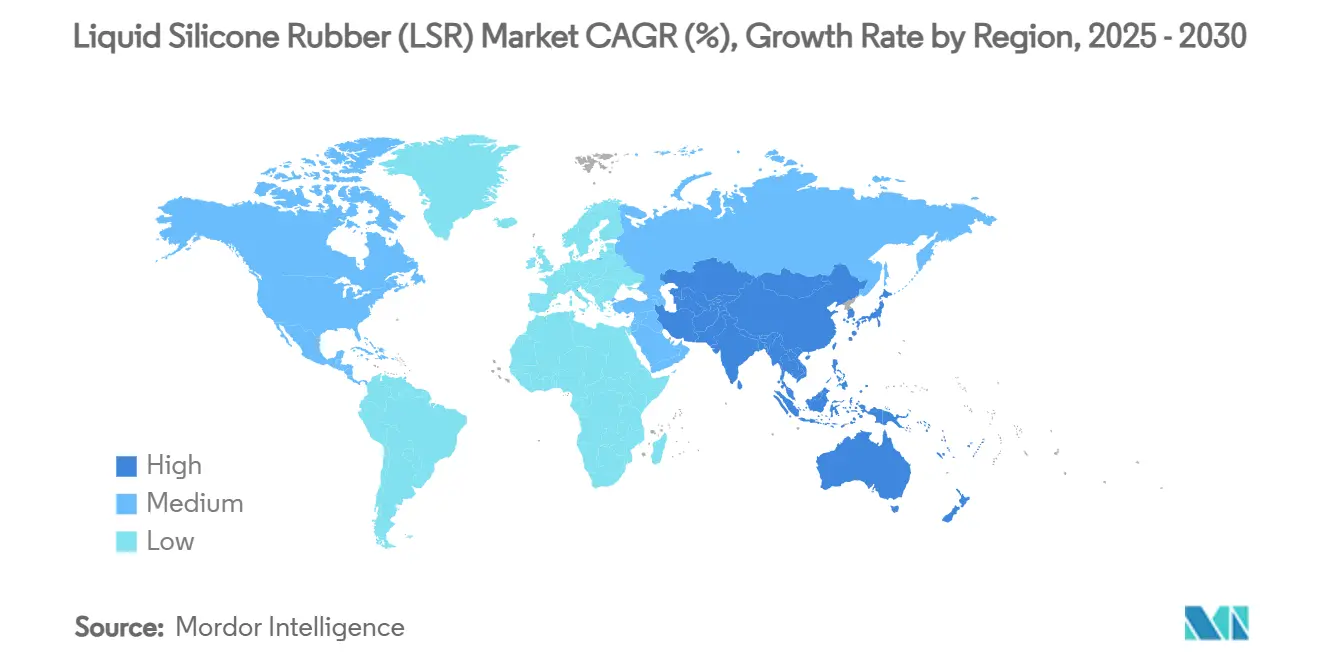

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Silicone Rubber (LSR) Market Analysis by Mordor Intelligence

The liquid silicone rubber market size reached 310.61 kilotons in 2025 and is projected to expand to 435.24 kilotons by 2030, reflecting a 6.98% CAGR over 2025-2030. Rising demand for biocompatible materials in medical devices, premium baby products, and ultra-high-voltage electric-vehicle (EV) battery packs sustains this growth trajectory. Asia-Pacific dominates current consumption on the back of electronics and automotive manufacturing, while healthcare innovation is accelerating adoption in North America and Europe. Liquid injection molding (LIM) remains the preferred processing technology because it delivers tight tolerances, minimal flash, and high output rates.

Key Report Takeaways

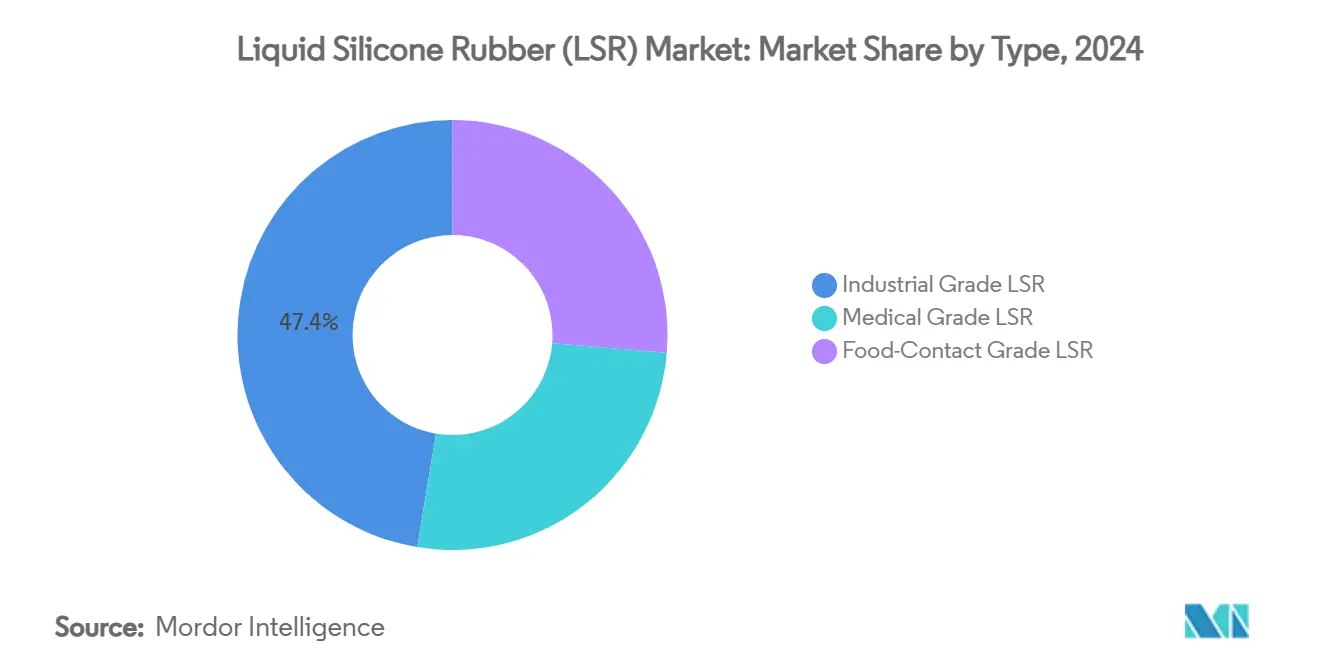

- By type, industrial grade commanded 47.38% of volume in 2024, whereas medical/implant grade will expand most rapidly at 7.15% CAGR on the back of long-term implant approvals.

- By processing method, liquid injection molding accounted for 69.19% of the liquid silicone rubber market size in 2024 and is projected to grow at 7.36% through 2030.

- By application, seals, gaskets & O-rings captured 45.18% of the liquid silicone rubber market share in 2024; wearable & implantable drug-delivery systems are advancing at a 7.04% CAGR to 2030.

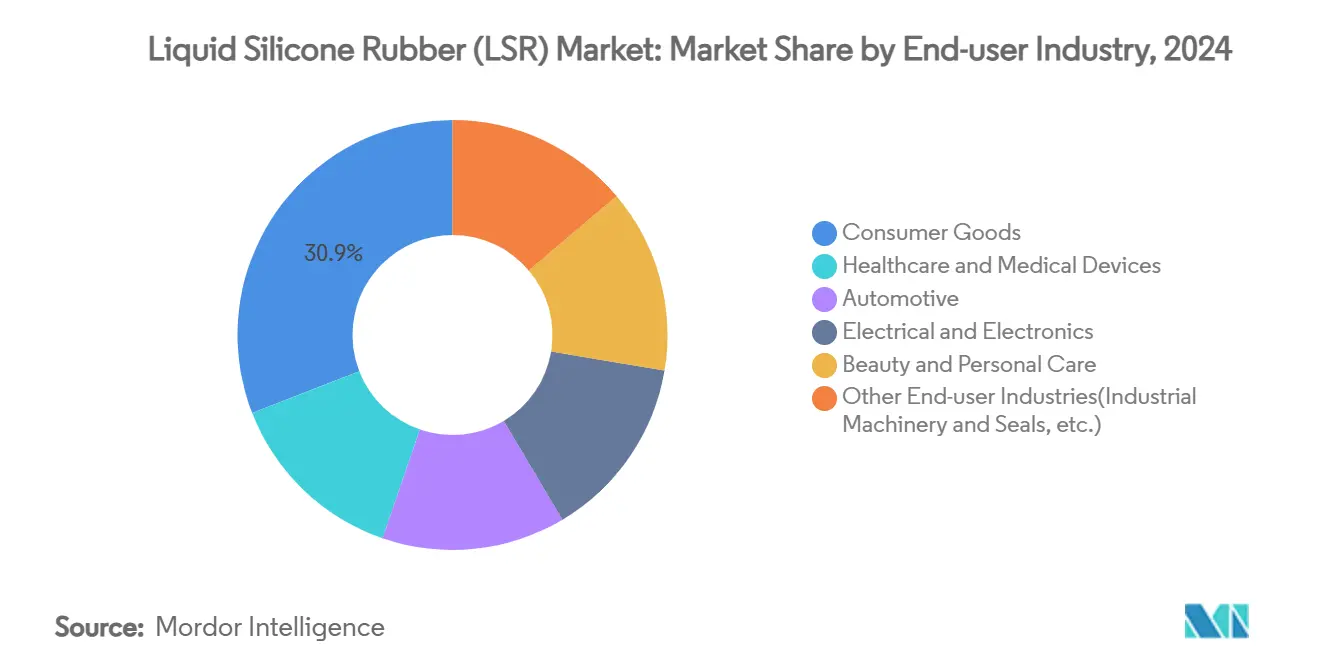

- By end-use industry, consumer goods led with 30.91% of the liquid silicone rubber market share in 2024, while healthcare & medical devices are forecast to post the fastest 7.15% CAGR to 2030.

- By region, Asia-Pacific controlled 53.96% of 2024 global volume and is set to climb at a 7.18% CAGR through 2030, supported by EV production hubs in China, Japan, and South Korea.

Global Liquid Silicone Rubber (LSR) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising healthcare demand | +1.2% | North America, Europe | Medium term (2-4 years) |

| Growth in baby-care products | +0.8% | North America, Europe | Short term (≤ 2 years) |

| EV battery sealing needs | +1.5% | Asia-Pacific, Europe | Long term (≥ 4 years) |

| Expanding electronics usage | +0.7% | Asia-Pacific, North America | Medium term (2-4 years) |

| Increasing Adoption in Aerospace | +0.3% | North America & Europe | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Increasing Demand From the Healthcare Industry

Hospitals and device makers specify medical-grade formulations because the material meets ISO 10993 cytotoxicity and USP Class VI criteria, resists gamma and steam sterilization, and supports complex geometries with undercuts. Recent breakthroughs enable multi-drug elution from a single implant, allowing physicians to tailor release profiles for oncology and pain-management therapies[1]Elkem, “Healthcare,” elkem.com. Compression-set resistance extends implant life, lowering revision-surgery risk and total cost of care. Clean-room LIM has become routine for catheter hubs and micro-valves, driven by FDA expectations for traceability and tighter particulate limits. These factors together lift global specification rates and help propel the liquid silicone rubber market toward higher-margin medical segments.

Rising Demand From the Baby Care Industry

Caregivers increasingly favor pacifiers, teething rings, and feeding bottles that contain no plasticizers, BPA, or latex proteins. Liquid silicone rubber maintains elasticity after hundreds of dishwasher or sterilization cycles, giving brands a clear durability advantage over TPE alternatives. Hypoallergenic and odor-neutral traits align with strict international toy-safety directives, while vibrant pigmentation options help premium lines stand out on retail shelves. Producer innovation—such as 100% food-grade infant toothbrushes—illustrates how this niche keeps expanding into everyday hygiene items. Together, these trends enlarge the consumer base and lift revenue density inside the liquid silicone rubber market.

Demand for EV Battery Sealing

Next-generation 800 V battery packs require gaskets that withstand rapid temperature cycling, high dielectric fields, and differential expansion across wide module footprints. Purpose-built gap fillers achieve thermal conductivities exceeding 3 W/m-K while maintaining softness for vibration dampening. As cell-to-pack designs gain acceptance, OEMs specify wide continuous seals that must remain compressed over 10-year service lives. LSR’s low VOC cure chemistry prevents contamination of sensitive electro-chemistry, a decisive quality for premium battery warranties. These attributes firmly embed the liquid silicone rubber market in the EV supply chain, underpinning double-digit demand growth in Asia-Pacific gigafactories.

Growing Utilization From the Electronics Industry

Miniaturized sensors, LED modules, and 5G-antenna housings require encapsulants that combine dielectric stability with heat dissipation. Formulations offering thermal conductivities above 1.5 W/m-K can now be processed in low-pressure over-mold systems, protecting fragile micro-chips from mechanical stress. UV-resistant grades ensure outdoor base-station gaskets maintain signal integrity despite high humidity and intense solar exposure[2]Dow, “Dow to Showcase Technologies for Safer, More Reliable EV Batteries at The Battery Show Europe,” corporate.dow.com. Because LSR cures without by-products, it eliminates corrosion risk on copper leads, supporting high-reliability electronics in automotive ADAS and industrial automation. These requirements solidify electronics as a long-term volume contributor to the liquid silicone rubber market.

Restraint Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product cost | -1.0% | Global | Short term (≤ 2 years) |

| Recycling challenges | -0.5% | Europe, North America | Medium term (2-4 years) |

| Competition from Novel TPEs | -0.6% | Global, with concentration in consumer goods applications | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

High Cost of Liquid Silicone Rubber Products

Dedicated dosing pumps, closed-loop temperature control, and plunger-type injection machines inflate capital outlays relative to thermoplastic molding. Added-value features—medical purity, food-contact certification, or flame-retardancy packages—increase formulation prices by 25%-60% versus commodity elastomers. Process‐integration sensors provide cycle-time savings and scrap reduction but require upfront investment in Industry 4.0 hardware. Budget-constrained segments such as personal-care dispensers sometimes switch to modified TPEs, dragging near-term growth. Producers are countering with higher cavity molds, predictive maintenance platforms, and expanded regional compounding to shrink freight costs, gradually easing this brake on the liquid silicone rubber market.

Recycling Challenges for Liquid Silicone Rubber

Cross-linked network chemistry prevents remelting, limiting conventional mechanical recycling routes. End-of-life incineration creates regulatory pressure, especially under Europe’s waste-framework directives. A pilot chemical-recycling pathway that depolymerizes silicone backbones into reusable siloxanes promises a 60% cut in carbon footprint relative to virgin feedstock. Technology awaits commercial scale-up, leaving OEMs with few short-term disposal solutions. Sustainability departments are beginning to factor cradle-to-grave impacts into material selection, which may divert some demand toward advanced TPEs until circular models for LSR mature. The issue therefore taps the brakes on long-range growth within the liquid silicone rubber market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Medical Adoption Drives Premium Formulations

Industrial grade maintained the lion’s share at 47.38% in 2024, delivering cost-effective performance for seals, grommets, and keypad housings across diverse industries. High tear strength and oil resistance underpin its suitability for under-hood automotive parts and consumer-electronics buttons, ensuring stable baseline demand inside the liquid silicone rubber market.

Medical/implant grade is advancing at a 7.15% CAGR as minimally invasive therapies gain traction globally. United States FDA approvals for cardiac leads and neuromodulation implants frequently cite low extractables data and stable compression-set values made possible by platinum-cured LSR. This premium pricing tier improves overall liquid silicone rubber market size profitability, with top suppliers scaling ISO 13485–certified production cells to meet stringent traceability requirements. Food-contact grade forms a niche growth pocket anchored in reusable baking molds and baby utensils; performance parity after repeated sterilizations positions it as an eco-friendly alternative to single-use plastics.

By Processing Method: Liquid Injection Molding Dominates Manufacturing

Liquid Injection Holding held 69.19% in 2024, stemming from fully automated mixing, short cure cycles, and minimal post-processing. Multi-component LIM integrates hard-plastic substrates with soft LSR over-molds in a single shot, cutting assembly time for medical valves and smart-watch straps. These advantages are critical as OEMs chase takt-time reductions and repeatable high yields, reinforcing LIM’s status in the liquid silicone rubber market.

Transfer and compression molding retain relevance for very large parts such as industrial diaphragms, where press tonnage rather than cavity count dictates economics. Early additive-manufacturing pilots demonstrate how 3D-printed LSR lattices can tune cushioning in custom prosthetics, hinting at a future bridge between prototype agility and mass-production quality.

By Application: Specialized Uses Shape Demand Patterns

Seals, gaskets & O-rings delivered 45.18% share in 2024, with battery-pack perimeter seals topping growth charts due to the EV surge. LSR’s low volatility protects lithium-ion chemistry from contamination and extends module life, making this application a cornerstone of the liquid silicone rubber market.

Wearable & implantable drug-delivery systems are forecast at a 7.04% CAGR, supported by continuous glucose monitors and contraceptive rings that rely on long-term skin compatibility. Catheters & medical tubing maintain a robust pipeline as minimally invasive surgery becomes standard care. Electrical connectors and housings capture synergy between dielectric strength and moisture resistance for outdoor telecom hardware. Premium infant teats and soothers round out a portfolio that underscores LSR’s versatility across safety-critical and lifestyle-driven products alike.

By End-Use Industry: Consumer Goods Lead Diverse Applications

Consumer goods comprised 30.91% volume in 2024, leveraging soft-touch aesthetics, non-stick behavior, and vibrant colorability in kitchenware, wearables, and baby-care lines. Premium-segment brands tout dishwasher-cycle durability up to 200 cycles, amplifying perceived value for price-sensitive shoppers and enlarging the liquid silicone rubber market.

Healthcare & medical devices record the next-largest share, propelled by point-of-care diagnostic cartridges and wearable infusion pumps. Automotive demand is shifting toward battery-pack seals and radar-sensor over-molds, while beauty & personal-care brands use LSR applicators for hygienic skin contact. These diverse vectors create a balanced revenue mix that buffers cyclical risk within the liquid silicone rubber industry.

Segment Analysis: End-User Industry

Consumer Goods Segment in Liquid Silicone Rubber Market

The Consumer Goods segment dominates the global liquid silicone rubber market, commanding approximately 30% market share in 2024. This segment, which includes food contact products and baby care products, has established itself as both the largest and fastest-growing segment with a projected growth rate of around 7% from 2024-2029. The segment's leadership position is primarily driven by the increasing demand for food-grade LSR in storage containers, kitchen appliances, and baby care products like pacifiers and bottle dispensers. The growing focus on food safety and hygiene has led to increased adoption of LSR in food contact applications, while the expanding baby care industry, particularly in emerging economies, continues to drive demand. The material's non-toxic nature, resistance to bacteria, and ease of sterilization make it particularly suitable for these applications, further cementing its position as the market leader.

Remaining Segments in End-User Industry

The liquid injection molding companies within the LIM market are significantly impacting the liquid silicone rubber market by serving several other significant end-user segments, including Healthcare and Medical Devices, Automotive, Electrical and Electronics, and Beauty and Personal Care. The Healthcare and Medical Devices segment represents the second-largest market share, driven by increasing applications in medical devices, surgical equipment, and implants. The Automotive sector utilizes LSR in various components, including gaskets, seals, and electrical connectors, while the Electrical and Electronics industry employs LSR for its excellent insulating properties and thermal stability. The Beauty and Personal Care segment, though smaller, maintains steady demand for LSR in packaging solutions and personal care products. Each of these segments contributes uniquely to the market's growth, leveraging LSR's versatile properties such as biocompatibility, chemical resistance, and thermal stability for their specific applications.

Geography Analysis

Asia-Pacific held 53.96% of global volume in 2024, with China accounting for more than half of regional consumption. Expansions by Wynca Tinyo and Jiangsu Tianchen signal a shift toward local upstream integration that lowers feedstock costs and secures supply continuity. Government incentives for new-energy vehicles elevate LSR demand in battery cooling pads and cell-module gaskets, cementing the region’s influence on the liquid silicone rubber market.

North America ranks second, anchored by high-purity medical-device production clusters in Minnesota, California, and Mexico’s Bajío corridor. Recent capacity additions—such as Datwyler’s two-component molding lines—shorten lead times for U.S. and Canadian OEMs while shielding them from freight volatility. Aerospace tier-ones in Washington and Alabama specify flame-retardant grades for cabin and engine seals, tapping LSR’s broad thermal window to meet weight-saving goals.

Europe maintains leadership in process innovation and sustainability. German machine builders continuously refine dosing precision to shrink scrap rates, and Italian mold-makers pioneer conformal-cooling layouts that lower cycle times. The European Commission’s focus on circularity spurs R&D into chemical recycling ventures like New Dawn Silicones, foreshadowing a future where closed-loop systems unlock additional growth channels for the liquid silicone rubber market.

Mordor Intelligence provides coverage of the liquid silicone rubber (lsr) market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The liquid silicone rubber market is partially fragmented in nature. KCC’s full takeover of Momentive in March 2024 enlarged its product portfolio and geographic reach, strengthening its grip on advanced formulations for medical and mobility customers [3]Momentive, “KCC Corporation Enters into Agreement to Fully Acquire Momentive Performance Materials Group,” momentive.com. Innovation serves as the prime differentiator. Elkem’s Silicone range targets controlled-release drug implants, while Wacker’s heat-shrinkable LSR grades address wire-harness miniaturization. Players are securing quartz-feedstock contracts, establishing regional compounding hubs, and deploying digital twins for predictive maintenance. These moves aim to stabilize lead times and quality, providing customers with confidence as volumes accelerate, particularly in EV and medical verticals.

Liquid Silicone Rubber (LSR) Industry Leaders

Dow

Wacker Chemie AG

Shin-Etsu Chemical Co., Ltd.

Elkem ASA

Momentive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: WACKER Chemie AG announced the launch of its new “eco” grade ELASTOSIL eco LR 5003, which will be featured in its sustainability zone. This non-post cure liquid silicone rubber is designed for large-scale production in the food industry and other sensitive sectors.

- May 2024: WACKER Chemie AG announced the launch of industrial-grade silicone rubber compounds made from plant-based raw materials, advancing sustainable manufacturing practices while conserving fossil resources. The product portfolio includes one liquid grade, six solid silicone rubber grades, and a range of SILMIX silicone rubber compounds.

Global Liquid Silicone Rubber (LSR) Market Report Scope

Liquid silicone rubber (LSR) is a silicone-based rubber made from a liquid compound that consists mainly of silicone polymer and possesses various superior characteristics such as non-toxic, temperature resistant, pourable consistency, physical and electrical stability, and others. A liquid silicone rubber material is a type of elastomer that is two-part platinum-cured that can be injected into different types of mold cavities to manufacture various parts serving from consumer products to medical devices industries.

The Liquid Silicone Rubber (LSR) Market is segmented by Type (Food Grade LSR, Industrial Grade LSR, and Medical Grade LSR), End-user Industry (Healthcare and Medical Devices, Automotive, Electrical and Electronics, Consumer Goods, Beauty and Personal Care, and Other End-user Industries), The report also covers the market size and forecasts for the market in 17 countries across the globe. The report offers market size and forecasts in terms of volume (Tons) for all the above segments.

| Industrial Grade LSR |

| Medical Grade LSR |

| Food-Contact Grade LSR |

| Liquid Injection Molding |

| Transfer and Compression Molding |

| Seals, Gaskets and O Rings |

| Catheters and Medical Tubing |

| Electrical Connectors and Housings |

| Teats, Soothers and Infant Feeding |

| Wearable and Implantable Drug Delivery Systems |

| Healthcare and Medical Devices |

| Automotive |

| Electrical and Electronics |

| Consumer Goods |

| Beauty and Personal Care |

| Other End-user Industries(Industrial Machinery and Seals, etc.) |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Industrial Grade LSR | |

| Medical Grade LSR | ||

| Food-Contact Grade LSR | ||

| By Processing Method | Liquid Injection Molding | |

| Transfer and Compression Molding | ||

| By Application | Seals, Gaskets and O Rings | |

| Catheters and Medical Tubing | ||

| Electrical Connectors and Housings | ||

| Teats, Soothers and Infant Feeding | ||

| Wearable and Implantable Drug Delivery Systems | ||

| By End-use Industry | Healthcare and Medical Devices | |

| Automotive | ||

| Electrical and Electronics | ||

| Consumer Goods | ||

| Beauty and Personal Care | ||

| Other End-user Industries(Industrial Machinery and Seals, etc.) | ||

| By Geography | Asia Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the liquid silicone rubber market?

The liquid silicone rubber market size reached 310.61 kilotons in 2025 and is forecast to climb to 435.24 kilotons by 2030.

Which region leads global consumption?

Asia-Pacific leads with 53.96% of 2024 volume and maintains the fastest 7.18% CAGR thanks to strong electronics and EV production bases.

Why is liquid silicone rubber preferred for medical devices?

Biocompatibility, resistance to multiple sterilization methods, and stable mechanical properties make it suitable for long-term implants and disposable surgical tools.

How does the automotive sector use liquid silicone rubber?

EV manufacturers specify specialized LSR grades for battery pack gaskets, gap fillers, and high-voltage connector seals that withstand extreme temperatures and vibration.

Which processing method dominates LSR manufacturing?

Liquid injection molding holds 69.19% of output because it delivers high precision, automated production, and low reject rates.

Page last updated on: