Sierra Leone Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

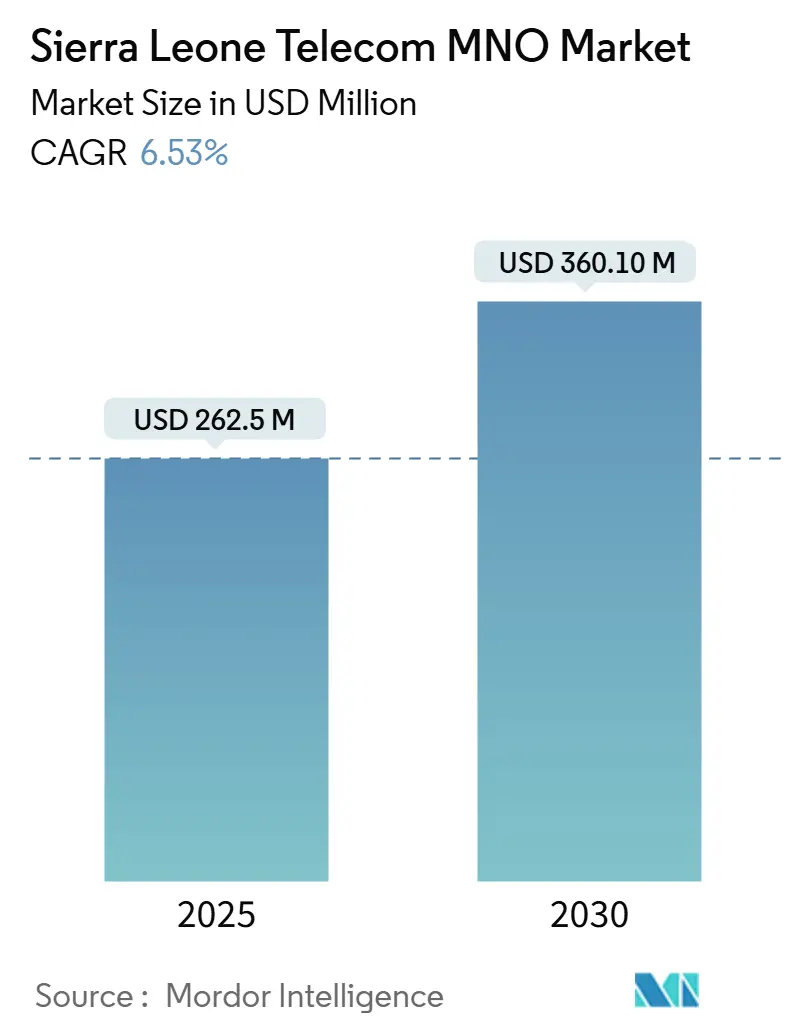

| Market Size (2025) | USD 262.5 Million |

| Market Size (2030) | USD 360.10 Million |

| Growth Rate (2025 - 2030) | 6.53% CAGR |

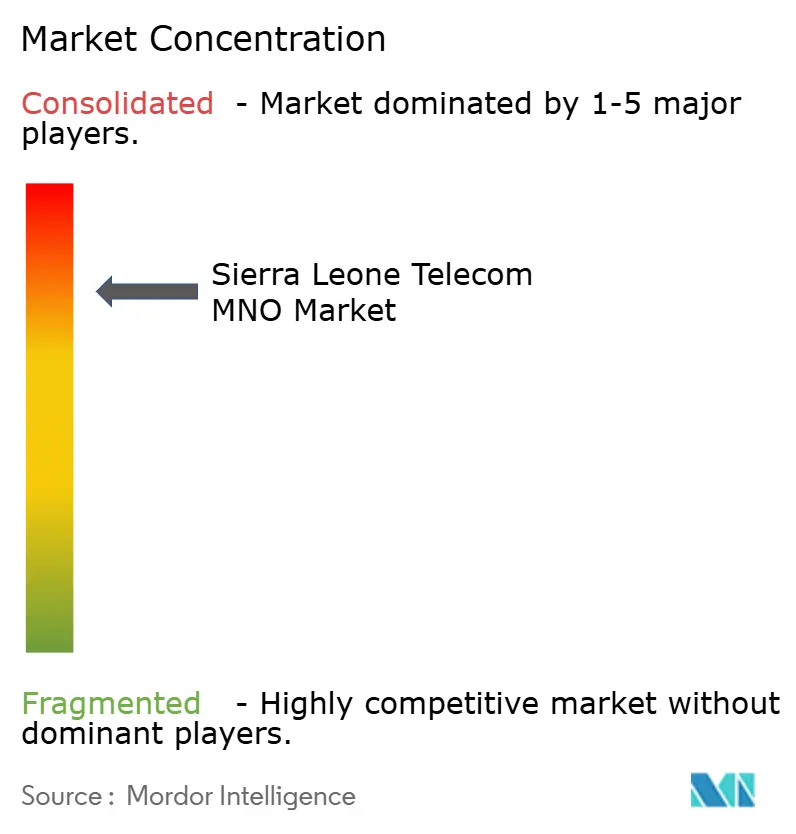

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sierra Leone Telecom MNO Market Analysis by Mordor Intelligence

The Sierra Leone telecom MNO market size is valued at USD 262.5 million in 2025 and is forecast to reach USD 360.1 million by 2030, reflecting a 6.53% CAGR. Growth is driven by rapid 4G coverage, falling smartphone prices, and government-backed digital programs, yet it remains moderate because operators still contend with severe power and foreign-exchange constraints. Network quality has become the main competitive lever, pushing mobile network operators (MNOs) toward tower upgrades, renewable power solutions, and spectrum refarming. Consumer demand for mobile data, mobile money, and value-added digital services is expanding faster than voice traffic, leading firms to prioritize ARPU optimization rather than subscriber acquisition. Enterprise connectivity is beginning to scale on the back of national e-government platforms and data-center rollouts, shifting revenue mix away from pure retail to blended B2B offerings.

Key Report Takeaways

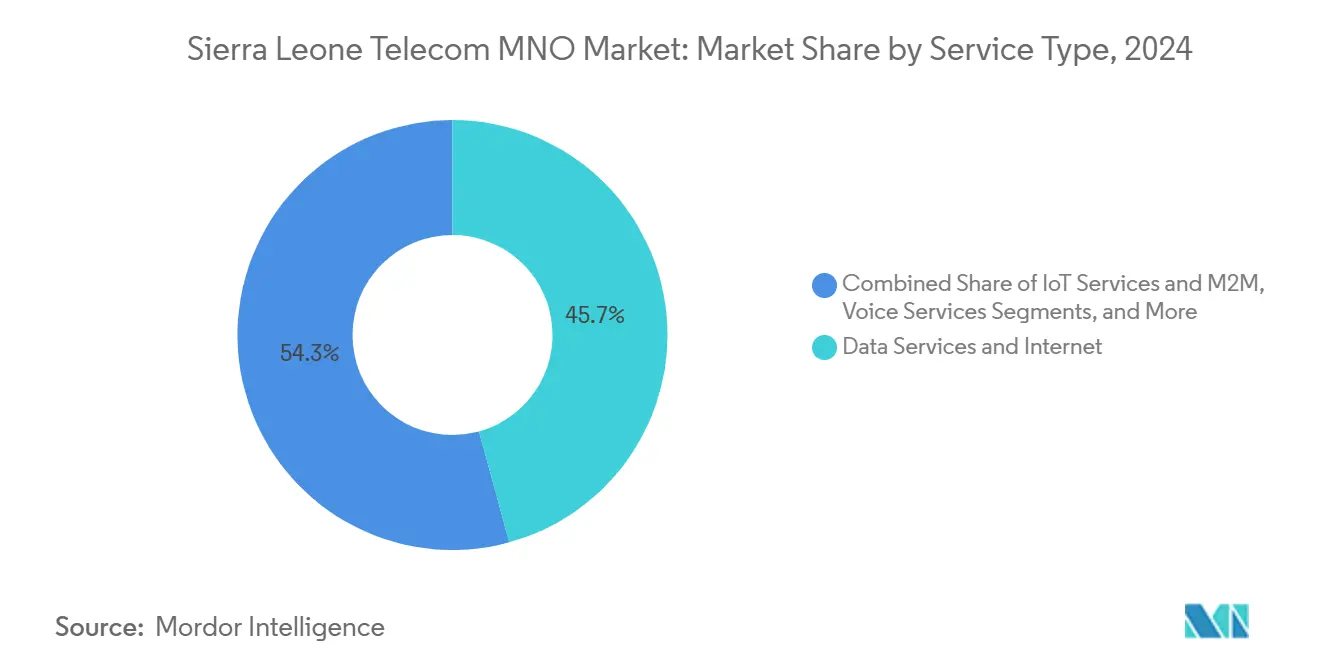

- By service type, data and internet services led with 45.74% revenue share in 2024, while IoT and M2M services is projected to expand at a 6.78% CAGR through 2030.

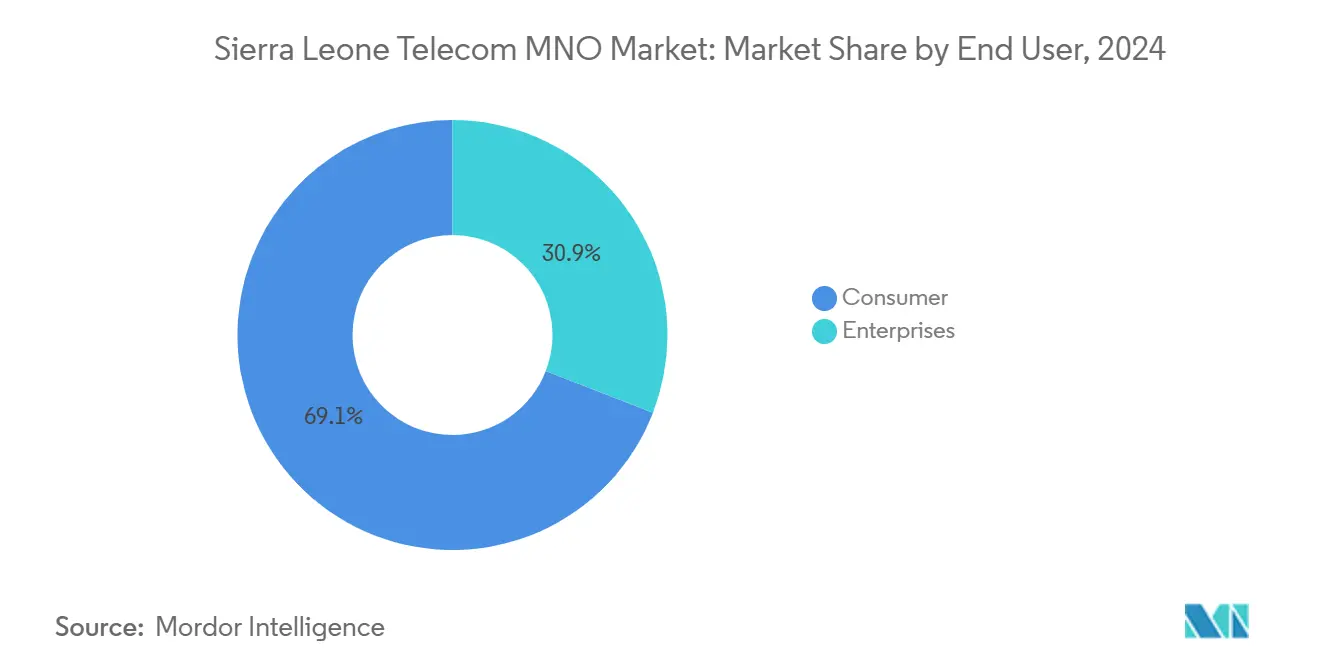

- By end user, the consumer segment captured 69.19% revenue share in 2024; the enterprise segment is poised for the fastest 6.87% CAGR to 2030.

Sierra Leone Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone-driven surge in mobile data usage | +0.8% | National, concentrated in Freetown and Bo | Medium term (2-4 years) |

| Rapid 4G roll-outs by Africell and Orange | +0.6% | National, prioritizing urban centers | Short term (≤ 2 years) |

| Falling smartphone and data-bundle prices | +0.4% | National, greatest impact in rural areas | Medium term (2-4 years) |

| Government e-services and Digital ID push | +0.3% | National, government-led initiatives | Long term (≥ 4 years) |

| ACE cable capacity upgrade | +0.2% | National, wholesale cost reduction | Short term (≤ 2 years) |

| Mobile-money cross-sell of micro-credit | +0.5% | National, rural inclusion focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smartphone-Driven Surge in Mobile Data Usage

Rapid smartphone adoption is lifting average data-bundle consumption despite earlier price barriers. Operators now offer promotional off-peak bundles, such as Orange Sierra Leone’s unlimited night browsing plan, to stimulate traffic and smooth network load. As affordability improves, data-user numbers outpace general mobile subscriber growth, forcing MNOs to accelerate capacity upgrades and spectrum refarming. Higher usage volumes help offset falling effective MB pricing, enabling steadier revenue even in a low-ARPU environment. Network planners are shifting capex toward additional 4G sectors, small-cells, and backhaul resilience to meet video-streaming demand in Freetown, Bo, and emerging provincial hubs.

Rapid 4G Roll-outs by Africell and Orange

Africell and Orange deployed nationwide 4G layers faster than expected after securing USD 100 million and USD 33 million funding, respectively. Their simultaneous expansion created a “coverage race” that closed service gaps in diamond-mining corridors and tourist areas, reducing churn and raising customer satisfaction indices. Enhanced 4G capacity enables VoLTE, low-latency fintech apps, and video-rich educational content, setting the stage for the country’s first renewable-powered 5G pilot activated in 2025. Competitors QCell and Sierratel are now forced to accelerate their own modernization plans, which collectively improve national service reliability.

Government E-services and Digital ID Push

The Medium-Term National Development Plan 2024-2030 targets 50% internet penetration by 2030, doubling current levels and requiring sizeable wholesale bandwidth additions.[1]Ecofin Agency, “Sierra Leone signs USD 50 million Smart project,” ecofinagency.com Projects such as the USD 50 million Smart Sierra Leone program and the USD 150 million Tech City hub are building data centers, public Wi-Fi spots, and cloud-ready workloads that depend on local carrier interconnects. Digital ID rollouts and a cashless-payments mandate formalize new authentication traffic for MNOs, while long-term contracts for government networks anchor predictable B2B revenue.

Mobile-Money Cross-sell of Micro-Insurance and Credit

Orange Money and Africell Money are transforming ARPU through fintech products that sit on top of core connectivity. Orange’s micro-loan feature offers Le 15–Le 200 with 12% interest, creating fee streams independent of voice or data consumption. Partner programs adding 2,000 female agents have enlarged merchant acceptance points and deepened financial inclusion. Operators benefit from higher daily log-ins and reduced churn as subscribers treat the SIM as a transactional identity. Incremental micro-insurance and merchant-QR services are expected to lift combined fintech revenue share of the Sierra Leone telecom MNO market to low double-digits by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power unreliability inflating tower OPEX | -0.4% | National, acute in rural areas | Long term (≥ 4 years) |

| Leone depreciation raising import CAPEX | -0.3% | National, equipment procurement | Medium term (2-4 years) |

| Fiber vandalism along mining corridors | -0.2% | Regional, mining areas focus | Short term (≤ 2 years) |

| Proposed 2024 VAT on data services | -0.1% | National, regulatory implementation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Power Unreliability Inflating Tower OPEX

Fewer than 40% of citizens have reliable grid access, forcing MNOs to depend on diesel or solar hybrid power at more than 1,300 active cell sites. Diesel logistics raise operating expenses, especially during rainy-season road disruptions. Health-facility mapping revealed 82% of clinics lack institutional internet, signaling broader energy deficits that also stunt rural broadband plans. Renewable energy pilots for 5G are lowering fuel costs, but rollout remains slow outside Freetown. The USD 412 million Western Area Power Generation Project promises future relief, yet will not meaningfully cut tower OPEX until after 2027. [2]YAME, “Western Area Power Generation Financing,” yame.media

Leone Depreciation Raising Import CAPEX

Every radio node, fiber pair, and handset is priced in foreign currency, so Leone weakness immediately inflates procurement budgets. The Finance Act 2024 raised withholding tax on management fees to 15% and introduced new digital levies, compounding cash-flow stress. Economic growth cooled to 4.3% in 2024 amid iron-ore volatility, pressuring the exchange rate. MNOs now hedge currency risk or stagger orders, but delayed deliveries slow 4G densification. Tariff adjustments partly compensate, yet they heighten the affordability tension among low-income users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and Internet Services Drive Revenue Transformation

Data and Internet Services accounted for 45.74% share of 2024 revenue, making them the largest slice of the Sierra Leone telecom MNO market. Operators see this category as the chief growth engine because video streaming, social media, and fintech apps rely on robust downlink speeds. The Sierra Leone telecom MNO market size linked to data and internet services is projected to rise in line with the overall 6.96% CAGR as greater spectrum efficiency and new fiber backhaul support higher traffic loads. IoT and M2M Services remains small today, yet has one of the steepest 6.78% CAGR, buoyed by smart-city pilots and industrial monitoring contracts in diamond mines.

Usage trends place sustained pressure on backbone capacity, so Africell and Orange invest in carrier-grade routers and content-delivery caches. Operators concurrently design tiered data bundles to monetize heavier users while keeping entry-level packs affordable. Partnerships with streaming platforms and education portals add value without large capex. By 2030, analysts expect data lines to eclipse 50% of total service revenue, confirming the shift away from legacy voice.

By End User: Consumer Market Drives Volume, Enterprise Accelerates Growth

The consumer base generated 72.88% of 2024 revenue, reflecting the prepaid, low-ARPU nature of the Sierra Leone telecom MNO market. Rural SIM proliferation and handset financing schemes sustain subscriber additions, even though voice minutes per user trend down. Cross-selling digital loans and insurance lift effective ARPU, which otherwise remains in single-digit USD terms.

Enterprises are growing at a 3.88% CAGR, benefiting from foreign-investor incentives such as duty-free machinery imports and zero-stamp-duty land leases. Banks, mining firms and BPO centers seek symmetrical bandwidth and managed security, stimulating higher-margin B2B lines. MNOs bundle cloud storage, cybersecurity, and M2M connectivity, deepening wallets beyond simple leased lines. As public-sector data availability rises, telcos can monetize hosting and edge-compute nodes for provincial government offices.

Geography Analysis

Western Area, led by Freetown, generates an estimated 65% of the Sierra Leone telecom MNO market’s 2025 service revenue. Dense population, higher spending power, and better power supply mean 4G population coverage already exceeds 98% in the capital. Bo, Kenema, and Makeni represent emerging mid-tier clusters where Africell and Orange continue to swap 3G sites for LTE, targeting school and hospital data-traffic corridors.

Rural districts still struggle with fewer than 45% electrification levels. Operators lean on solar-hybrid base stations and satellite backhaul to bridge gaps. Starlink’s 2024 entry introduced competition in deep rural zones; however, its price points limit adoption to NGOs and agribusiness customers techpoint.africa. Cross-border fiber deals with Guinea and Liberia aim to provide redundancy and slash wholesale rates, reducing reliance on the single ACE landing station.[3]Developing Telecoms, “Guinea-Sierra Leone Fibre Link,” developingtelecoms.com

Regional growth potential lies in mining concessions that demand always-on connectivity for safety telemetry. Fiber vandalism along haul roads remains a risk, so carriers deploy buried ducts and microwave rings as backups. Coastal tourism corridors from Bureh to Tokeh gain new small-cell coverage that supports mobile money acceptance by guesthouses. By 2030, nationwide LTE population coverage is expected to surpass 95%, narrowing the urban-rural digital divide and unlocking new content consumption patterns.

Competitive Landscape

Four main MNOs dominate the Sierra Leone telecom MNO market. Africell holds leadership by subscriber count through rapid rural footprint expansion and a robust mobile money ecosystem. Orange leverages superior 4G quality, brand strength, and international group resources to win high-value urban customers. QCell positions itself as an affordable alternative with niche data packs, while state-owned Sierratel focuses on enterprise voice links and wholesale capacity sales. Comium operates as a small fifth player targeting youth segments with price-led promos.

Competitive intensity now revolves around network quality, fintech breadth, and customer-experience digitization rather than headline tariffs. Orange is collaborating with OpenAI and Meta to develop Wolof and Pulaar language models that will enable chatbots and IVR in local dialects from 2025. Africell plans to inject private-equity funds into 5G and fiber rings, aiming to defend its mass-market stronghold. Smaller ISPs such as NetPage and Afcom pursue fixed-wireless and VSAT in hard-to-reach villages, complementing MNO footprints.

Tower-sharing is rising as operators seek capex efficiency. Independent towercos pilot solar and lithium battery solutions that cut diesel usage by up to 40%, an attractive proposition in a high-fuel-cost setting. The regulatory authority encourages infrastructure sharing to avoid duplicate sites and accelerate rural coverage. Market consolidation risk remains low because each player services distinct micro-segments, but spectrum renewal fees in 2027 could prompt joint bids or network-sharing alliances to lower cost burdens.

Sierra Leone Telecom MNO Industry Leaders

Africacell

Orange

QCell

Sierratel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sierra Leone launched its first renewable-powered 5G network, delivering sustainable capacity growth and mitigating grid-power risks.

- May 2025: Orange and the International Finance Corporation unveiled a pan-African digital initiative that includes improved Sierra Leone connectivity

- January 2025: The Finance Act 2025 introduced duty-free plant and machinery imports for investments of at least USD 10 million, benefiting telco infrastructure rollouts

- June 2024: A USD 150 million Tech City hub was announced within a 130-acre special economic zone, backed by Africell and Orange

Sierra Leone Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumers |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumers |

Key Questions Answered in the Report

What is the current size of the Sierra Leone telecom market?

The Sierra Leone telecom MNO market is valued at USD 262.5 million in 2025 and is projected to reach USD 360.1 million by 2030.

Which service generates the highest revenue in the Sierra Leone telecom market?

Data and internet services account for the largest revenue share at 45.74% as of 2024.

How quickly is the enterprise segment growing?

Enterprise connectivity revenue is expanding at a 6.87% CAGR through 2030, the fastest among end-user segments.

What is the main operational challenge for network expansion?

Grid-power unreliability inflates tower operating costs, reducing profitability and slowing rural coverage growth.

How are operators improving ARPU?

They are bundling mobile money products such as micro-credit and micro-insurance, which create transaction-based fee income in addition to core connectivity revenue.

When is nationwide LTE population coverage expected to reach 95%?

Population-wide 95% LTE coverage is anticipated by 2030 as ongoing tower builds and fibre links close remaining rural gaps.

Page last updated on: