Senegal Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

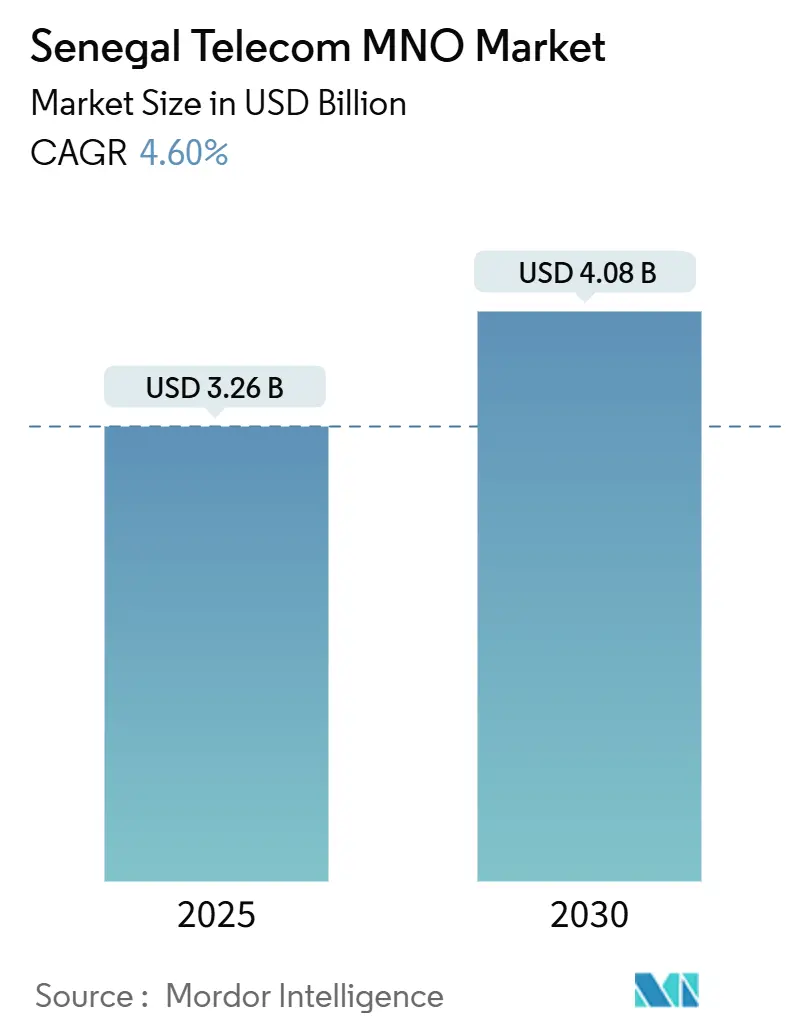

| Base Year Market Size (2025) | USD 3.26 Billion |

| Market Size (2025) | USD 3.26 Billion |

| Market Size (2030) | USD 4.08 Billion |

| Growth Rate (2025 - 2030) | 4.60% CAGR |

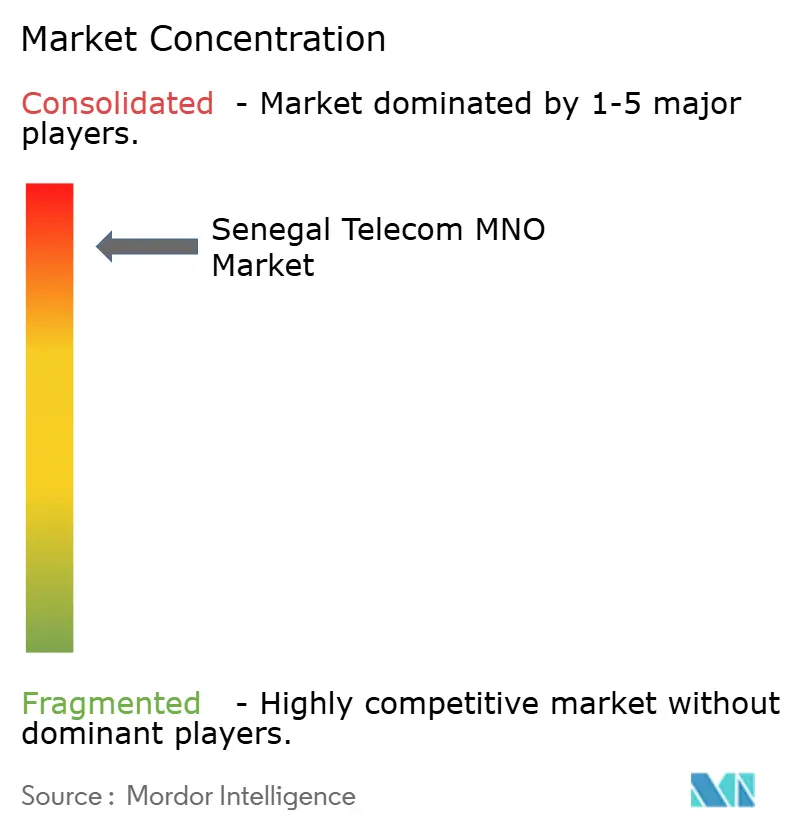

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Senegal Telecom MNO Market Analysis by Mordor Intelligence

The Senegal Telecom MNO Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 4.08 billion by 2030, at a CAGR of 4.60% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 22.32 million subscribers in 2025 to 28.04 million subscribers by 2030, at a CAGR of 4.66% during the forecast period (2025-2030).Mobile broadband demand, national fiber upgrades, and early 5G deployments underpin this expansion as the sector already contributes close to 10% of GDP. Operators are channeling capital into 4G+ densification and fixed-wireless access to monetize surging data traffic, while government-backed Digital Senegal 2025 programs lower rural coverage gaps. Competitive differentiation now hinges on AI-enabled local-language services, mobile-money ecosystems, and satellite backhaul that bring underserved communities into the digital economy. Spectrum reforms, cross-border roaming within UEMOA, and enterprise IoT in agriculture further broaden revenue levers as operators pursue diversified growth strategies.

Key Report Takeaways

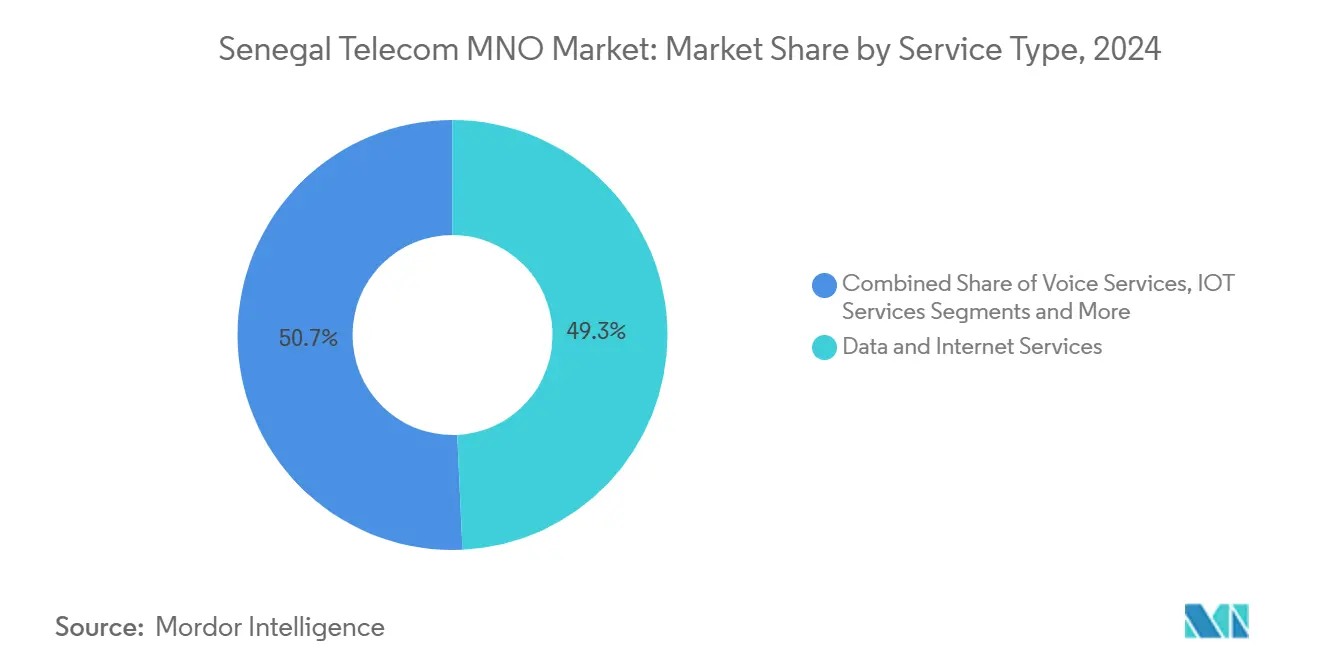

- By Service Type, data services captured 49.26% of the Senegal Telecom MNO market share in 2024, and are projected to have the highest CAGR at 5.12% through 2030.

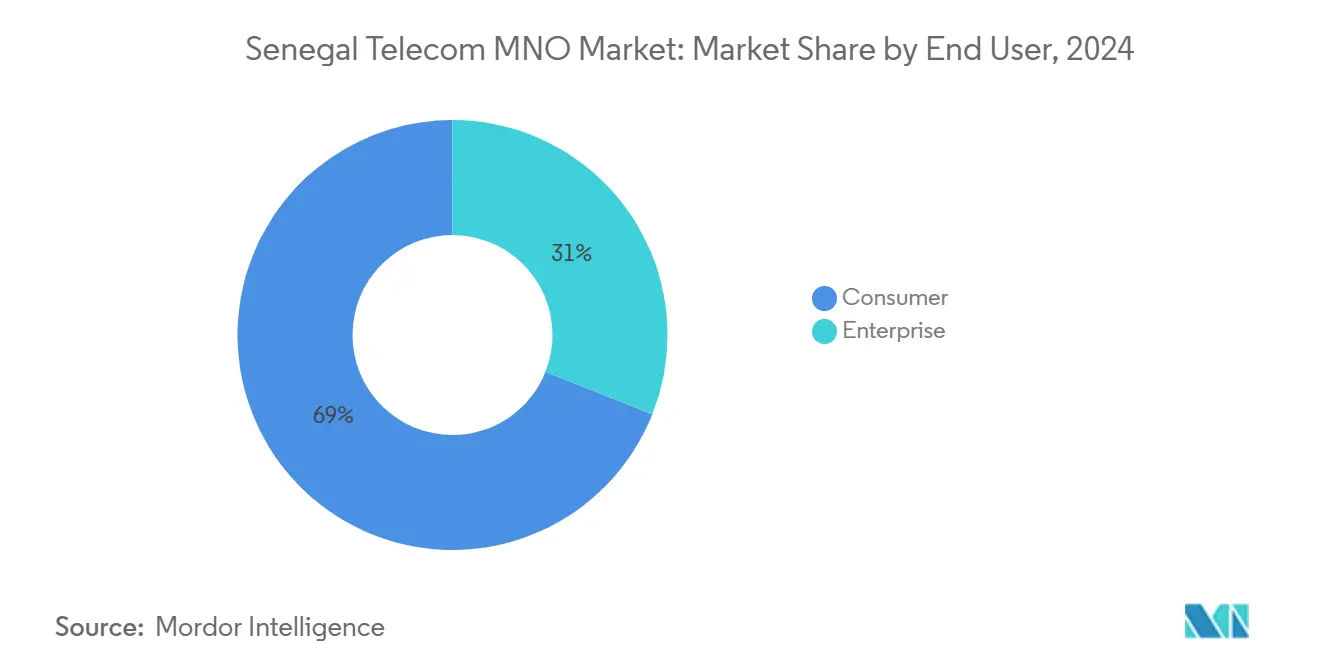

- By End-User, Consumers captured 68.99% of the Senegal Telecom MNO market share in 2024, and while Businesses are projected to have the highest CAGR at 4.93% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Senegal Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising 4G+ coverage and 5G readiness | +1.2% | Dakar and secondary cities | Medium term (2-4 years) |

| Surge in mobile data traffic from smartphone uptake | +1.5% | Nationwide | Short term (≤ 2 years) |

| Government Digital Senegal 2025 programs | +0.8% | Nationwide | Long term (≥ 4 years) |

| Fixed-wireless access demand outside Dakar | +0.4% | Secondary cities | Medium term (2-4 years) |

| Enterprise IoT in fisheries and agriculture | +0.3% | Coastal and farm regions | Long term (≥ 4 years) |

| UEMOA cross-border mobile-money growth | +0.5% | West African corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising 4G+ Coverage and 5G Readiness

Operators have lifted 4G population coverage above 95% in settlements over 500 inhabitants and secured 5G licenses worth USD 57 million combined. The roadmap prioritizes dense urban sites, allowing Sonatel to trial peak speeds of 2.1 Gbps. By reallocating 3G spectrum before its 2028 sunset, carriers release extra capacity for enhanced mobile broadband. Obligatory service-quality maps established by the regulator from 2025 compel transparency and encourage network upgrades that sustain the Senegal telecom MNO market growth.

Surge in Mobile Data Traffic from Smartphone Uptake

Smartphone penetration climbed to 60.6% of the population, lifting mobile internet users to 11.3 million and driving a double-digit jump in average monthly data usage. Video streaming dominates traffic as YouTube counts 5.01 million Senegalese viewers, pressuring operators to bundle zero-rating offers and bigger data allowances. Youthful demographics median age 19.6 years maintain upward momentum for the Senegal telecom MNO market.

Government Digital Senegal 2025 Programs

Public funding of USD 100 million, topped up by USD 150 million from the World Bank, accelerates backbone fiber rollouts and subsidizes rural BTS sites. The plan already delivered 140 000 jobs and elevates telecom’s GDP weight, cementing long-term demand for connectivity and cloud services. Regulatory reforms mandate infrastructure sharing, trimming duplicated capex and stabilizing tariffs that fortify the Senegal telecom MNO market.

Fixed-Wireless Access Demand Outside Dakar

Fixed broadband subscriptions climbed 25% to 741 000 in 2024, with 4G/5G radio links filling gaps where fiber trenching remains uneconomical. The ACE submarine cable’s 9 014 Gbps capacity feeds backhaul, letting operators market home-broadband packages that tap latent demand in secondary cities. These bundles diversify revenue beyond crowded mobile segments and uplift the Senegal telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High taxation and spectrum fees | -0.8% | Nationwide | Short term (≤ 2 years) |

| Limited submarine bandwidth capacity | -0.4% | Nationwide | Medium term (2-4 years) |

| Delayed local-content rules for Pay-TV | -0.2% | Nationwide | Long term (≥ 4 years) |

| Grid-power instability raising BTS OPEX | -0.6% | Rural zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Taxation and Spectrum Fees

Initial 4G auctions stalled when reserve prices equaled USD 50 million per block, a level the GSMA labeled unsustainable. Although concessions were reached, elevated levies still squeeze operator cash flows, delaying 5G radio deployments and tempering the Senegal telecom MNO market expansion.

Grid-Power Instability Raising BTS OPEX

Diesel back-up and hybrid solar kits raise site operating costs by up to 40% versus grid power. Tower company Helios Towers is testing on-site renewables to stabilize expenses, yet rural rollout economics remain tight, limiting coverage density and moderating the Senegal telecom MNO market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Accelerate Monetization

Data services represented 49.26% of Senegal telecom MNO market share in 2024 and will compound at 5.12% through 2030. In revenue terms, the segment accounted for USD 1 586 million of Senegal telecom MNO market size last year and will add more than USD 400 million by 2030. Social-media-driven video, mobile money usage, and cloud adoption raise bandwidth needs, prompting operators to bundle larger data plans and OTT content. Voice retains a sizeable 39.80% slice but is losing share to OTT calling, despite VoLTE upgrades that keep legacy minutes alive. IoT services, at 4.21% share, gather pace via agriculture moisture sensors and fisheries cold-chain trackers that run on narrow-band links. OTT & Pay-TV packages hold 2.97% share amid local-content bottlenecks, while other residual services take 3.76%.

Complementary investments in IP core, caching, and submarine capacity help contain unit data costs, letting carriers protect EBITDA. Tariff competition—daily micro-bundles and zero-rated social apps—sustains prepaid ARPU while expanding smartphone adoption enlarges the addressable base. The operator pivot to non-connectivity revenue aligns with the global trend where value-added services deliver 27% of sector turnover. Regulatory service-quality enforcement aims to maintain consumer confidence and underpin the Senegal telecom MNO market.

By End-User: Enterprise Uptake Outpaces Consumer Growth

Consumers remain dominant at 68.99% of 2024 revenue but rise more slowly than enterprises. Businesses, which already generate 31.01%, seek MPLS, SD-WAN, and IoT bundles, pushing a 4.93% CAGR to 2030 compared with 4.45% for households. Government digitization and fintech integrations catalyze enterprise connectivity, deepening the Senegal telecom MNO market penetration.

Geography Analysis

Dakar contributes roughly 55% of telecom revenue due to higher disposable incomes and fiber density. Secondary cities such as Thiès and Saint-Louis witness double-digit growth in fixed-wireless access, aided by government subsidies that cut last-mile costs. Rural coverage now spans 95% of villages over 500 residents, yet only two-thirds enjoy “good” or “very-good” signal under new ARTP mapping rules. Coastal regions attract IoT fisheries pilots that enhance cold-chain monitoring, while inland farming belts deploy smart irrigation meters to curb water waste. Cross-border corridors with Mali and Guinea host roaming and mobile-money traffic that lifts blended ARPU, broadening the Senegal telecom MNO market footprint. Satellite connectivity shores up backhaul in the far east, ending long-distance microwave dependence and enabling mobile data growth in sparsely populated zones.

Competitive Landscape

The Senegal telecom MNO market is moderately concentrated: Sonatel (Orange) holds 56.23%, Yas Senegal takes 24.47%, and Expresso carries 17.02%. Sonatel’s USD 4.1 billion market capitalization funds aggressive 5G rollout and AI-based Wolof and Pulaar chatbots that enhance customer care. Yas Senegal, rebranded by AXIAN Telecom, focuses on pan-African synergies and cheaper data packs to narrow the gap. Expresso stays price-led but leverages parent company Sudatel’s regional spectrum procurement to trim cost per MHz-pop. Infrastructure sharing via Helios Towers yields opex savings; its exploration of solar-hybrid power aims to cut fuel costs by 18%. Competitive dynamics intensify as Starlink starts rural broadband, forcing incumbents to expedite fixed-wireless rollouts and lobby for equalized licensing fees. Digital financial services remain a battleground, with Orange Money nearing 40 million users region-wide and Yas launching Mixx super-app in early 2025.

Senegal Telecom MNO Industry Leaders

Sonatel (Orange)

Free Senegal

Expresso

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Orange raised its 2025 organic cash-flow target to at least EUR 3.6 billion after 2024 revenue rose 1.2% to EUR 40.26 billion, with Africa & Middle East up 11.1%.

- November 2024: AXIAN Telecom rebranded Free Senegal to Yas Senegal, unifying operations across five African markets.

- November 2024: Orange partnered with OpenAI and Meta to create African-language AI models, starting with Wolof and Pulaar.

- January 2024: Yas Senegal secured a USD 22.4 million 5G license; Sonatel had obtained its license for USD 34.5 million in Jul 2023.

Senegal Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Senegal telecom MNO market today?

The market generated USD 3 220 million in 2024 and is on track to reach USD 4 085.7 million by 2030.

Which service type generates the most revenue?

Data services held 49.26% of 2024 revenue and will remain the largest contributor through the forecast period.

When will 5G be widely available?

Initial urban 5G launched in 2024; broader coverage is expected after 2026 as operators refarm 3G spectrum.

Why does rural coverage still lag?

High spectrum fees, unreliable grid power, and low ARPU make rural rollouts cost-intensive despite universal-service subsidies.

Page last updated on: