Morocco Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.73 Billion |

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Morocco Telecom MNO Market Analysis by Mordor Intelligence

The Morocco Telecom MNO Market size was valued at USD 3.73 billion in 2025 and estimated to grow from USD 3.87 billion in 2026 to reach USD 4.64 billion by 2031, at a CAGR of 3.72% during the forecast period (2026-2031).

This expansion reflects a gradual shift from pure subscriber growth toward revenue optimization through 5G-enabled services, fiber backhaul, and enterprise-grade solutions. Network modernization, strategic infrastructure-sharing ventures, and an accelerating government fiber program affect operator strategies, while near-parity market shares among Inwi, Maroc Telecom, and Orange Maroc create an aggressive pricing environment that compresses margins. Regulatory oversight intensifies with sizable anticompetitive penalties and mandatory local-loop unbundling, pushing incumbents to collaborate on neutral FiberCo and TowerCo vehicles to cut capital outlays. Youth-driven data demand and foreign direct investment in industrial corridors underpin medium-term traffic growth, whereas OTT substitution for voice and messaging restrains legacy revenues. Overall, the Morocco telecom MNO market has entered a maturation phase centered on quality-of-service differentiation rather than headline subscriber additions.

Key Report Takeaways

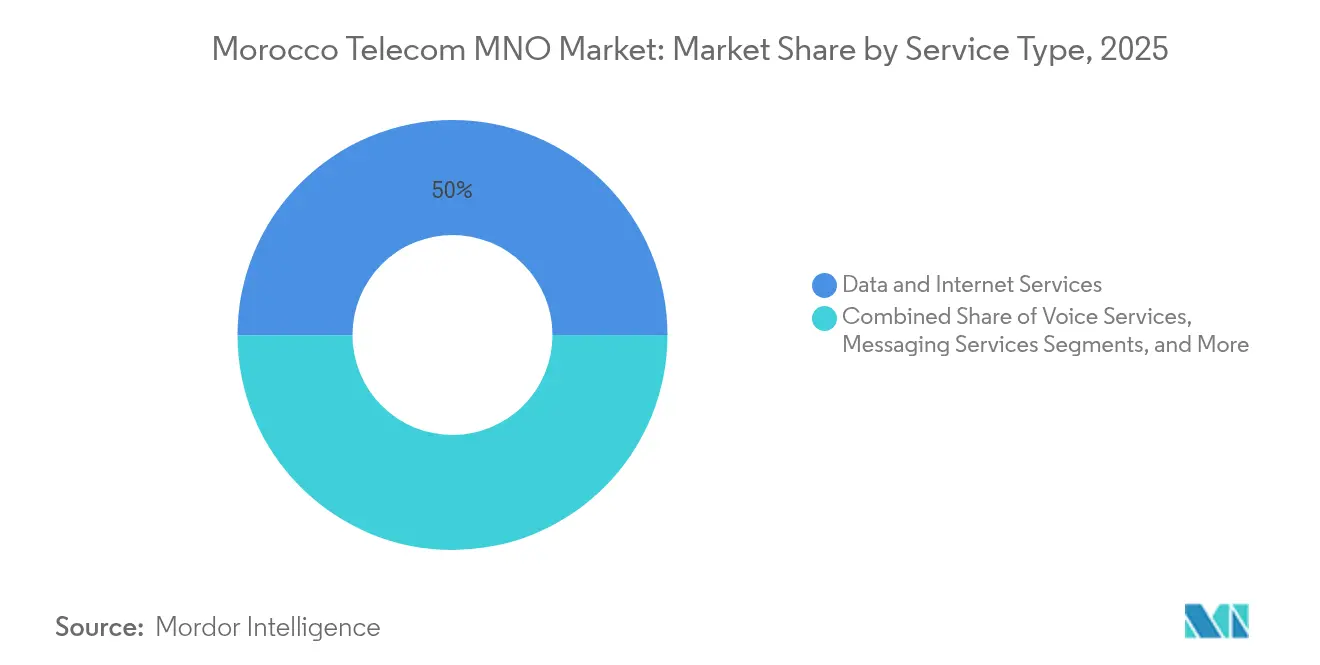

- By service type, data and internet services led with 50.02% of Morocco telecom MNO market share in 2025, while IoT and M2M services are positioned to expand at a 3.84% CAGR to 2031.

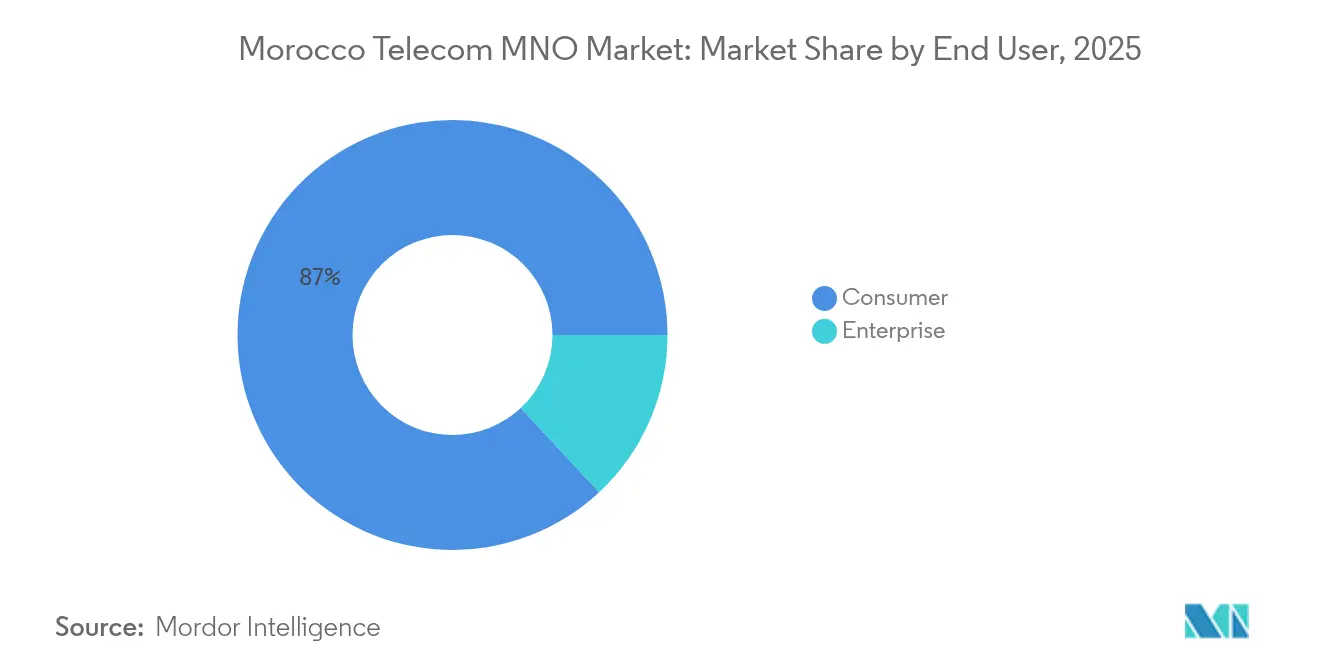

- By end user, the consumer segment accounted for 86.95% of the Morocco telecom MNO market size in 2025; the enterprise segment is projected to grow at a 4.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G spectrum auctions and rollout 2025-2030 | +1.2% | Casablanca, Rabat, Marrakech first | Medium term (2-4 years) |

| Surging mobile data consumption among Morocco’s <30 population | +0.8% | Urban centers nationwide | Short term (≤ 2 years) |

| Government “Digital Morocco 2030” fiber investment program | +0.6% | Rural and underserved areas | Long term (≥ 4 years) |

| Urban uptake of converged quad-play bundles | +0.4% | Primary and secondary cities | Medium term (2-4 years) |

| Enterprise demand for private LTE/5G at industrial zones | +0.3% | Tangier, Casablanca, Kenitra | Medium term (2-4 years) |

| Near-shoring FDI boosting international wholesale traffic | +0.2% | Coastal data-center hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Spectrum Auctions Drive Network Modernization

The scheduled November 2025 5G auction represents a strategic inflection point for the Morocco telecom MNO market. Licenses in the 3.5 GHz and 700 MHz bands are expected to accelerate coverage to 25% of the population by 2026 and 70% by 2030, creating capacity for industrial IoT, smart-city platforms, and immersive consumer applications [1]Paula Gilbert, “Morocco to launch 5G in November 2025,” Connecting Africa, connectingafrica.com. Nokia’s innovation centers will supply local operators with advanced radio and core solutions that shorten time-to-market. ANRT rules now oblige infrastructure sharing, opening premium spectrum bands to smaller licensees and curbing redundant deployment costs. Joint ventures such as Maroc Telecom-Inwi TowerCo illustrate how carriers pool passive assets to support faster rollout while protecting cash flow. As a result, capital intensity is anticipated to decline by nearly 200 basis points from 2024 levels, lifting free cash that can be redirected toward enterprise service development and customer-experience tools.

Digital Morocco 2030 Accelerates Fiber Infrastructure

Digital Morocco 2030 targets 5.6 million household fiber links by 2030, more than doubling the existing 2.5 million fixed-broadband lines recorded in September 2024. Government subsidies, streamlined permits, and new duct-sharing rules underpin the program, enabling power utilities and rail companies to lease dark fiber at discounted rates to mobile operators. Inwi and Orange increasingly challenge Maroc Telecom’s legacy copper dominance by piggybacking on electricity-distribution rights-of-way. Median nationwide upload speeds reached 31.86 Mbps in early 2025, the highest in North Africa, meeting the latency and symmetry requirements of data-center colocation, cloud migration, and advanced analytics workloads.

Enterprise Demand Transforms Revenue Mix

Private LTE and 5G networks in industrial parks symbolize a pivot from consumer connectivity toward enterprise digital-transformation enablement. The April 2025 Vodafone-Maroc Telecom memorandum of understanding bundles SD-WAN, MEC, cloud orchestration, and cybersecurity into a single SLA-backed offering for automotive, logistics, and aerospace plants clustered around Tangier Med and Casablanca free-trade zones [2]Jasdip Sensi, “Vodafone expands in Africa with Maroc Telecom MoU,” Capacity Media, capacitymedia.com. RedCap chipsets, priced close to LTE Cat-1 yet firmware-upgradable to 5G, lower the total cost of ownership for asset tracking, smart metering, and predictive-maintenance solutions. As regional headquarters relocate to Morocco to exploit cross-Mediterranean supply chains, operators stand to monetize wholesale IP transit, multi-cloud interconnect, and managed security offerings, cushioning the decline in traditional roaming and international voice.

Youth Demographics Fuel Data Consumption

Roughly two-thirds of Morocco’s 38 million citizens are under 30, and this cohort accounts for 78% of total mobile data traffic. Unlimited social-media bundles and video-streaming add-ons now comprise 41% of prepaid ARPU, while traditional voice and SMS revenue fell 8% year-on-year in 2024. The surge forces operators to densify LTE grids in densely populated districts and deploy content-delivery nodes at edge data centers to stave off congestion. To preserve monetization, carriers have introduced tiered Quality of Service packs that charge premium rates for gaming-grade latency or advertisement-free video. Partnerships with local e-learning and fintech platforms further embed the operator brand into youth digital lifestyles, contributing incremental service revenue that partially offsets price dilution in baseline access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense price competition driving ARPU erosion | -0.9% | Urban markets nationwide | Short term (≤ 2 years) |

| Heavy regulatory fines and compliance costs on incumbents | -0.6% | Incumbent-focused | Medium term (2-4 years) |

| Protracted rural fiber ROW approvals | -0.3% | Interior provinces | Long term (≥ 4 years) |

| OTT substitution of international voice and SMS revenue | -0.4% | Youth-centric urban segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Competition Intensifies ARPU Pressure

Near-parity shares, Inwi 35.3%, Maroc Telecom 32.5%, Orange Maroc 32.3%, have ignited an endless cycle of headline discounts, unlimited bundles, and loyalty giveaways that dragged blended mobile ARPU to USD 4.8 in Q2 2025, a 6% sequential drop [3]Africa Intelligence staff, “Maroc: Moov Africa à la rescousse de Maroc Telecom,” Africa Intelligence, africaintelligence.fr. Maroc Telecom’s domestic revenue contracted 3.9% in H1 2024, compelling the group to rely on Moov Africa subsidiaries for top-line stability. Regulatory nudges such as instant number portability and SIM-registration kiosks have lowered switching barriers, amplifying churn and inflating acquisition costs. Operators counter by cross-selling home-fiber, OTT-TV, and micro-insurance add-ons, yet elevated content-licensing fees blunt margin relief. Persistent price aggression could shave almost USD 120 million in sector revenue by 2027, limiting funds for 5G core upgrades and rural backhaul expansion.

Regulatory Enforcement Escalates Compliance Costs

ANRT’s punitive framework has reached new severity, a USD 635 million damages award to Inwi plus a USD 333 million local-loop fine against Maroc Telecom together exceeded the latter’s full-year 2023 net profit of USD 615 million. Operators must now ring-fence 5% of annual capex for mandated Quality-of-Service audits, cybersecurity drills, and universal-service contributions. Compliance extends to shared-spectrum management portals and real-time consumer complaint dashboards, systems that impose ongoing opex without immediate monetization upside. While the measures foster a fairer competitive arena and protect consumer welfare, the cumulative cash-flow impact could trim the effective Morocco telecom MNO market size growth by 30 basis points over the forecast horizon unless offset by efficiency gains or tariff rationalization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Lead Revenue Transformation

Data and internet services captured 50.02% of the Morocco telecom MNO market share in 2025. This dominance arises from rising smartphone adoption, the rollout of carrier aggregation on 4G networks, and the imminent 5G launch that promises sub-10 ms latency and gigabit throughput. Meanwhile, the Morocco telecom MNO market size for IoT and M2M services is forecast to climb at a 3.84% CAGR as RedCap standards slash module costs. Operators are bundling edge-compute mini-clusters with private-network slices to capture industrial automation, smart-agriculture, and smart-grid use cases.

Voice revenue continues to slide as OTT voice grows mainstream, even among mid-income users. Messaging faces a steeper drop given the ubiquity of WhatsApp and Telegram. To re-anchor relevance, carriers package zero-rated social platforms into tiered plans and leverage RCS business messaging to court enterprise advertising budgets. PayTV and OTT bundles are witnessing early traction within converged quad-play offers. International wholesale, roaming, and value-added services round out the portfolio, boosted by Morocco’s rising status as a North-South connectivity hub via the Medusa subsea cable landing at Nador West Med.

By End-User: Enterprise Segment Drives Premium Growth

The enterprise segment is projected to grow at a robust 4.43% CAGR through 2031. Sales cycles center on managed SD-WAN, unified-communications-as-a-service, and secure cloud interconnects, all supported by SLAs that guarantee <20 ms round-trip latency on domestic routes. Manufacturing plants in Tangier Automotive City and free-trade zones near Casablanca increasingly request 5G private slices to automate robotics, quality-assurance cameras, and AGV fleets.

The consumer segment remains numerically dominant, capturing 86.95% of the Morocco telecom MNO market share in 2025. Operators aim to stabilize consumer ARPU by bundling fiber-to-the-home, linear TV, SVOD, mobile, and device financing into single invoices. Loyalty apps that exchange points for e-commerce vouchers support churn reduction. High-usage youth customers are targeted with fair-usage-capped unlimited plans featuring premium network tiers during peak gaming hours, generating marginal ARPU uplift without compromising network economics.

Geography Analysis

Casablanca-Rabat-Temara and Marrakech-Safi corridors together account for 42.58% of Morocco telecom MNO market revenue, underpinned by high population density, advanced LTE-Advanced networks, and an early 5G rollout slated for November 2025. Coastal provinces attract data-center builds by international hyperscalers, amplifying wholesale backhaul demand and international IP transit volumes.

Interior provinces such as Fes-Meknes and Drâa-Tafilalet lag in fiber penetration, constrained by protracted right-of-way approvals that inflate deployment costs. Digital Morocco 2030 earmarks USD 429 million in subsidies to bridge this divide, allowing operators to extend fiber backhaul and fixed-wireless access to remote communes. Median downlink speeds of 35.57 Mbps already outpace regional peers, but rural clusters still average under 18 Mbps, indicating headroom for quality-of-service uplift. Operators combine microwave and low-band 5G NR for cost-efficient wide-area coverage, capitalizing on universal-service fund incentives to defray tower builds.

Internationally, Morocco’s north-south location provides a strategic shortcut for Europe-West Africa cables. The 8,760 km Medusa system will link Nador West Med to Marseille, Barcelona, and Lisbon, positioning the country as a neutral peering point and fueling carrier-neutral data-center growth. For operators, wholesale leasing of spectrum on these routes offers a counter-cyclical revenue stream that mitigates domestic price erosion. Cross-border roaming agreements with Mauritania and Senegal further diversify income.

Competitive Landscape

The Morocco telecom MNO market operates as a balanced oligopoly in which Inwi, Maroc Telecom, and Orange Maroc split shares within a 3-percentage-point band, triggering aggressive promotional warfare. Market-share stability masks under-the-surface churn, as each carrier swaps customers chasing initial discount periods.

Collaborative infrastructure strategies mark a second competitive axis. The joint Maroc Telecom-Inwi FiberCo controls 16,400 km of metropolitan fiber; its TowerCo arm expects to reach 4,500 macro sites by 2027, leasing slots to rivals at regulated rates. These neutral platforms reduce duplication, freeing capital for service differentiation. International alliances also shape positioning: Maroc Telecom leverages Vodafone’s cloud and security stack, while Orange taps its Middle East and Africa wholesale division to resell capacity on European routes.

Regulatory actions continue to redefine tactics. ANRT’s hefty fines against Maroc Telecom elevate compliance risk and force board-level attention to fair-competition practices. Mandatory quarterly quality of service disclosures create reputational stakes, pushing operators to publish real-time network dashboards. As IoT and M2M become critical growth vectors, carriers race to lock ecosystem partners, from module vendors to analytics startups, into exclusive or preferential agreements, aiming to carve defensible niches before commoditization sets in.

Morocco Telecom MNO Industry Leaders

-

Maroc Telecom

-

Orange Maroc (Méditel)

-

Inwi (Wana Corporate S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ANRT confirmed the commercial 5G launch for November 2025, targeting 25% national coverage by 2026 and 70% by 2030.

- April 2025: Vodafone Business and Maroc Telecom signed an MoU to deliver SD-WAN, mobile private networks, cloud and cybersecurity services across Morocco.

- July 2024: The Casablanca Commercial Court of Appeal upheld Maroc Telecom’s USD 635 million compensation to Inwi for anticompetitive practices.

Morocco Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The telecom market includes in-depth trend analysis of connectivity, such as fixed networks, mobile networks, and telecom towers. Several factors, including the increasing demand for 5G, are likely to drive the adoption of telecom services.

The Moroccon telecom market is segmented by services (voice services (wired and wireless), data and messaging services, OTT, and PayTV services). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the forecast revenue for Morocco’s mobile-network-operator segment by 2031?

The Morocco telecom MNO market size is projected to reach USD 4.64 billion by 2031.

When will 5G services become commercially available in Morocco?

ANRT has scheduled the commercial 5G launch for November 2025, with plans to reach 25% national coverage by 2026 and 70% by 2030.

Which operator currently leads Morocco in subscriber share?

Inwi held the largest subscriber share at 35.3% at the end of 2024.

How fast is the enterprise customer segment growing?

Enterprise service revenue is expected to expand at a 4.43% CAGR through 2031, outpacing the consumer segment.

What government initiative underpins national fiber rollout?

Digital Morocco 2030 aims to connect 5.6 million households to fiber networks by 2030, accelerating broadband expansion.

How are fines affecting operator investment capacity?

Significant penalties, such as Maroc Telecom’s combined USD 968 million in damages and fines, constrain capital available for 5G and fiber projects.

Page last updated on: