Uganda Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.52 Billion |

| Market Size (2030) | USD 1.96 Billion |

| Growth Rate (2025 - 2030) | 5.24% CAGR |

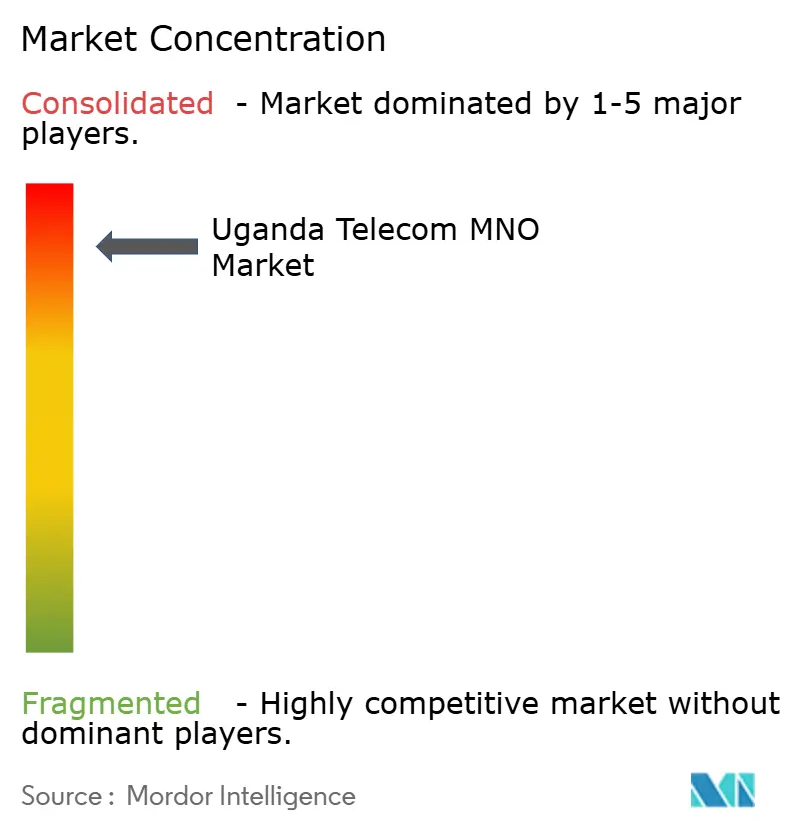

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uganda Telecom MNO Market Analysis by Mordor Intelligence

The Uganda Telecom MNO Market size is estimated at USD 1.52 billion in 2025, and is expected to reach USD 1.96 billion by 2030, at a CAGR of 5.24% during the forecast period (2025-2030).

Demand is accelerating as data-centric consumption, 4G densification, and early 5G launches offset rural infrastructure gaps. Operators gain pricing flexibility from mobile-money ecosystems that lift average revenue per user, while Google-backed fiber projects signal lower international capacity costs ahead. A landmark network-sharing pact between MTN Uganda and Airtel Uganda in March 2025 reshapes cost structures and speeds rural coverage. At the same time, private LTE and 5G contracts tied to Uganda’s oil and mining projects unlock fresh enterprise revenue streams. These dynamics collectively sustain investment appetite despite elevated spectrum fees and foreign-exchange cost pressures.

Key Report Takeaways

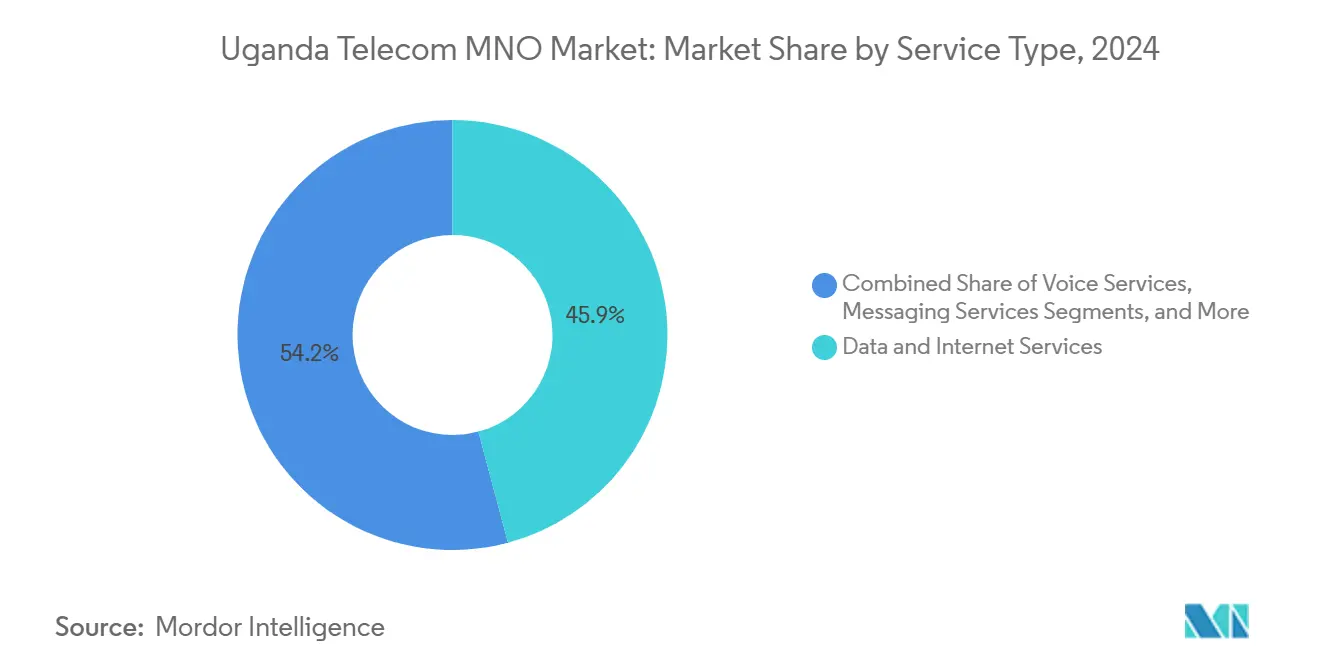

- By service type, data and internet services led with 45.85% revenue share in 2024 and are expanding at a 5.27% CAGR through 2030.

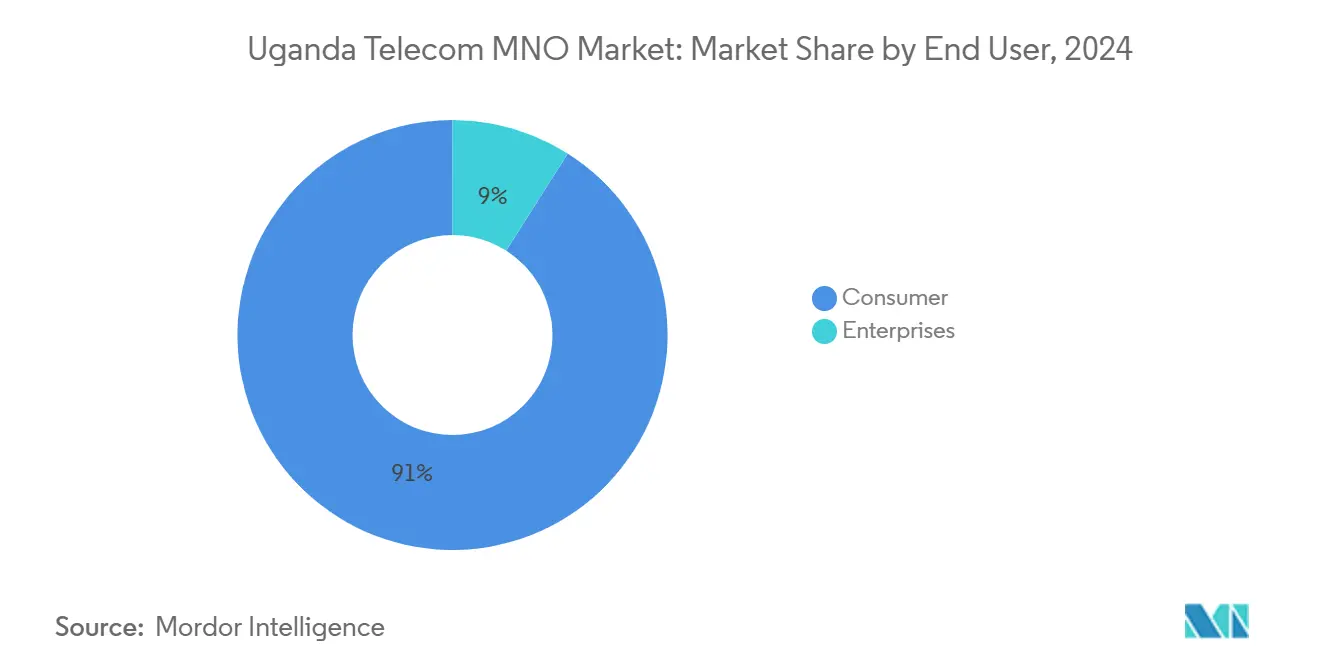

- By end user, the consumer segment held 90.99% of the Uganda telecom MNO market share in 2024, while enterprise connections posted the fastest growth at a 6.36% CAGR to 2030.

Uganda Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 4G rollout and 5G trial licensing | +1.2% | National, concentrated in Kampala and major urban centers | Medium term (2-4 years) |

| Surge in mobile data consumption via smartphones | +0.9% | National, with higher intensity in urban areas | Short term (≤ 2 years) |

| National broadband fiber-backbone expansion | +0.8% | National, prioritizing rural and underserved regions | Long term (≥ 4 years) |

| Mobile-money led ARPU uplift | +0.7% | National, with strongest adoption in rural areas | Medium term (2-4 years) |

| Private LTE/5G demand from oil and mining projects | +0.4% | Western Uganda oil regions, mining corridors | Long term (≥ 4 years) |

| Uganda acting as cross-border fiber transit hub | +0.3% | Border regions, international gateway points | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 4G rollout and 5G trial licensing

The July 2023 spectrum auction enabled Uganda’s first commercial 5G launches by MTN and Airtel, each targeting full Kampala coverage by end-2024. [1]Catherine Sbeglia Nin, “MTN delivers Uganda’s first 5G network,” RCR Wireless News, rcrwireless.com The partners’ 2025 network-sharing accord reduces duplication and releases capital for deeper rural builds. Early 5G performance supports 1 million devices per km², a capacity essential for industrial automation in the emerging oil economy. These deployments enhance user experience and underpin the Uganda telecom MNO market’s pivot from voice to data revenue. Nationwide 4G densification proceeds in parallel, ensuring affordable smartphone access as device prices fall.

Surge in mobile data consumption via smartphones

Cellular lines reached 38.6 million by early 2025, equal to 76.2% population penetration, while internet users climbed to 14.2 million. MTN posted 32.4% data-revenue growth in Q1 2025 on the back of 19.4% daily active user gains. Promotional bundles such as Airtel’s Mega4Dayzz cut effective gigabyte prices and stimulate usage. Strong data appetite aligns with Uganda’s tech-sector goal of contributing 8% to GDP by 2025. Intensifying competition keeps tariffs low, reinforcing data elasticity, and boosting volumes.

National broadband fiber-backbone expansion

Government-backed projects extend the National Backbone Infrastructure to underserved districts, supported by the World Bank’s Regional Communications Infrastructure Program. Liquid Intelligent Technologies upgraded the East Africa Fiber Ring to 100G capacity, improving regional latency and cost baselines. Nevertheless, Uganda’s average USD 2.67 cost per GB remains the highest in East Africa due to landlocked dependence on coastal gateways. The Uganda Internet Exchange Point mitigates outage risk by localizing traffic flows, as proved during the 2024 submarine cable disruptions. Expanded backbone reach, therefore, remains central to equitable service affordability.

Mobile-money led ARPU uplift

MTN’s MoMo handled USD 36 billion worth of transactions in 2023 across 13 million monthly active users. [2]MTN Group, “Mobile Money in Uganda – 15 years young,” mtn-investor.com Fintech revenue rose 18.4% in Q1 2025, underlining the model’s contribution to blended ARPU growth. Mobile money now spans merchant payments, micro-loans, and bank linkages, widening stickiness for rural customers excluded from formal banking. Plans to spin MoMo into a standalone fintech by 2025 underscore its strategic weight. High cash usage, still 95% of all transactions, signals further upside as digitization deepens.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High spectrum license and renewal fees | -0.6% | National, affecting all licensed operators | Short term (≤ 2 years) |

| Rural electrification gaps for tower rollout | -0.8% | Rural areas, particularly northern and eastern regions | Long term (≥ 4 years) |

| Lingering OTT-tax elasticity effects | -0.3% | National, with higher impact on social media usage | Medium term (2-4 years) |

| FX-driven capex inflation on imported gear | -0.4% | National, affecting equipment procurement cycles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High spectrum license and renewal fees

The 2023 5G auction imposed heavy up-front commitments on MTN and Airtel, while annual levies into the Universal Service and Access Fund add to recurring obligations. MTN alone paid UGX 42.5 billion in 2024, squeezing capital earmarked for rural towers. Sector taxes totaled UGX 1.1 trillion in the latest fiscal year, reinforcing the burden on profitability. [3]Nobert Atukunda, “Telecom sector contributes Shs1.1 trillion in taxes – Govt,” AllAfrica, allafrica.com Smaller operators such as Uganda Telecom struggle to fund competitive network upgrades, limiting market rivalry and constraining innovation diffusion.

Rural electrification gaps for tower rollout

Only 30% of Uganda’s population has grid electricity, forcing operators and tower-cos to deploy solar-battery hybrids at higher opex. [4]Christopher Greaves, “The big challenges impacting Africa’s telecom tower ecosystem,” Capacity Media, capacitymedia.com Ubuntu Towers raised USD 40 million to build 400 green-energy sites, illustrating the extra capital intensity of off-grid rollouts. Grid uncertainty worsens as Umeme’s concession expires and asset transfer plans progress, potentially delaying rural power reliability improvements. Persistent energy hurdles, therefore, lengthen pay-back periods and deter investment in low-ARPU zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services drive revenue transformation

Data and internet services accounted for 45.85% of the Uganda telecom MNO market in 2024 and are tracking a 5.27% CAGR to 2030. Voice revenue growth slowed to 1.5% during MTN’s Q1 2025 results, underscoring a structural pivot towards bandwidth-centric offerings. Smartphone subsidies, zero-rating promotions, and OTT partnerships keep gigabyte demand elevated. Messaging faces cannibalisation from social platforms, while IoT and M2M connections rise in oil-field automation. OTT and PayTV bundles ride on strategic content tie-ups, adding upsell avenues. Wholesale and enterprise circuits grow as Uganda acts as a regional transit hub, benefiting from recent 100G fiber upgrades. Rising spectrum efficiency through network sharing further supports margin preservation.

The evolving mix enhances the Uganda telecom MNO market size outlook, as elastic data usage offsets unit price declines. By 2030, data services are projected to capture more than half of sector value, confirming their role as the core growth engine. Higher-value fixed-wireless broadband also gains traction where fiber-to-home remains uneconomic. Continuous re-farming of legacy 2G bands into LTE ensures spectral headroom for sustained capacity expansion.

By End-User: Enterprise growth accelerates despite consumer dominance

Consumers contributed 90.99% of 2024 revenue, but enterprise lines deliver a 6.36% CAGR through 2030, outpacing mass-market growth. Oil projects such as the USD 10 billion East African Crude Oil Pipeline require mission-critical connectivity that leans on private LTE and 5G systems. Banking, manufacturing, and mining add IoT demand for asset tracking and predictive maintenance. Government cloud migration and e-services programs intensify bandwidth needs at ministries and district hubs.

Enterprise adoption boosts the Uganda telecom MNO market size for dedicated circuits, managed security, and edge data-center services. Raxio’s Tier III neutral facility in Kampala widens colocation options for corporates and Hyperscalers. As spectrum costs pressure retail pricing, business-grade solutions offer margin resilience. Consequently, operators bundle SD-WAN, IoT dashboards, and mobile money payroll integrations to capture share in a still-fragmented corporate segment.

Geography Analysis

Urban areas, home to 26% of the population, enjoy near-universal 4G and early 5G availability, anchoring roughly 70% of Uganda telecom MNO market revenue. Kampala’s Lugogo and Bugoloobi districts were the first to receive live 5G in 2023, with full-city coverage slated for late 2024. Data ARPU in the capital remains 30% above the national mean, reflecting premium plan uptake. In contrast, northern and eastern districts lag on both coverage and disposable income, underlining the digital divide.

The Uganda telecom MNO market size benefits from cross-border traffic as the country evolves into a regional transit hub. Google’s Umoja subsea cable will connect Mombasa to Australia and anchor a terrestrial link into Uganda, promising lower international transit costs. Concurrently, the upgraded East Africa Fibre Ring elevates redundancy for links to Kenya, Rwanda, and Tanzania. Local hosting of high-traffic content at the Uganda Internet Exchange Point limits exposure to future submarine outages.

Rural expansion relies on Universal Service and Access Fund disbursements, solar-powered tower models, and the fresh network-sharing regime between MTN and Airtel that halves site replication. Renewable-powered base stations enable modest opex savings despite high capex. As oil exploitation zones in western Uganda demand low-latency links for pipeline control, operators extend microwave backhaul and deploy private LTE grids. These investments progressively enlarge the Uganda telecom MNO market, even where household ARPU is subdued.

Competitive Landscape

The market operates as a duopoly: MTN Uganda and Airtel Uganda control a major share of the market. March 2025 network-sharing introduced joint passive and active infrastructure use, unlocking 15-20% opex efficiencies while preserving retail brand competition. MTN differentiates through loyalty propositions such as its Prestige program for high-value users. Airtel targets price-sensitive segments with aggressive bundle pricing, including 5 GB for UGX 7,000 under its Mega4Dayzz offer.

Technology leadership remains crucial. Both majors launched nationwide VoLTE in 2024, and each plans stand-alone 5G core upgrades by 2026. Uganda Telecom’s pending 60% stake sale to Rowad Capital for USD 225 million could reinvigorate competition if fresh capital funds 4G expansion. Satellite challenger Starlink signaled its intent to enter Uganda, appealing to remote enterprises and affluent households. Tower companies, led by American Tower and Ubuntu Towers, provide neutral hosting that lowers entry barriers for niche MVNOs, potentially widening service diversity.

Enterprise penetration presents the next battleground. MTN and Airtel pursue oil majors, banks, and logistics firms with private network proofs of concept. Bundled IoT, cloud connect, and mobile money payroll solutions offer stickier revenue. As wholesale cross-border capacity prices fall, both incumbents eye regional transit sales to operators in South Sudan and eastern DR Congo. Overall, high combined shares sustain significant bargaining power with vendors, yet regulatory scrutiny over pricing and quality remains.

Uganda Telecom MNO Industry Leaders

MTN Uganda

Airtel Uganda

Uganda Telecommunications Corporation Limited (UTel)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Rowad Capital completed negotiations to acquire a 60% stake in Uganda Telecommunications Corporation Limited for USD 225 million, aiming to revitalize the National Backbone Infrastructure and restore UTel’s competitive position in the market.

- March 2025: MTN Group and Airtel Africa signed a landmark network-sharing agreement covering Uganda and Nigeria, enabling infrastructure cost reduction and accelerated coverage expansion while maintaining service competition.

- December 2024: MTN Uganda launched the MTN Prestige premium loyalty program targeting high-value customers with monthly spending exceeding UGX 100,000, offering lifestyle benefits, exclusive discounts, and priority support services.

- December 2024: Google joined a USD 90 million investment into Cassava to strengthen Africa’s digital infrastructure, with implications for Uganda’s regional connectivity through enhanced fiber-optic networks.

- November 2024: MTN Uganda enhanced its WakaNet home broadband service with new pricing structures, faster internet speeds, and improved service offerings to compete in the fixed-broadband market.

- October 2024: The Uganda Parliament passed legislation providing for the mainstreaming of NITA-U into the Ministry of ICT after a three-year transition period, enabling implementation of the USD 200 million Uganda Digital Acceleration Project and USD 150 million National Backbone Infrastructure Phase V Project.

- May 2024: MTN Uganda contributed UGX 42.5 billion to the Uganda Communications Commission’s Universal Service and Access Fund, supporting rural connectivity expansion and digital inclusion initiatives.

Uganda Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is mobile money’s contribution to telecom revenue in Uganda?

Fintech income grew 18.4% year-on-year in Q1 2025, with MTN’s MoMo platform processing USD 36 billion in 2023, highlighting its rising share of operator earnings.

Which segment is expanding fastest within Ugandan telecom services?

Data and internet services, holding 45.85% revenue in 2024, are growing at a 5.27% CAGR to 2030 as smartphone use soars.

What drives enterprise demand for private networks?

Oil and mining projects such as the East African Crude Oil Pipeline require secure LTE/5G connectivity for real-time monitoring across remote sites.

Why are Uganda’s internet costs still high?

Landlocked dependence on coastal submarine cables and limited domestic backbone coverage keep average prices at USD 2.67 per GB, the highest in East Africa.

How does network sharing alter market economics?

The 2025 MTN–Airtel agreement cuts duplicate infrastructure spend by up to 20%, freeing capital for rural coverage while preserving brand competition.

What role will the Umoja cable play?

The Google-backed link will connect Uganda to the Mombasa–Australia corridor, lowering transit costs and improving international resilience.

Page last updated on: