Guinea Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

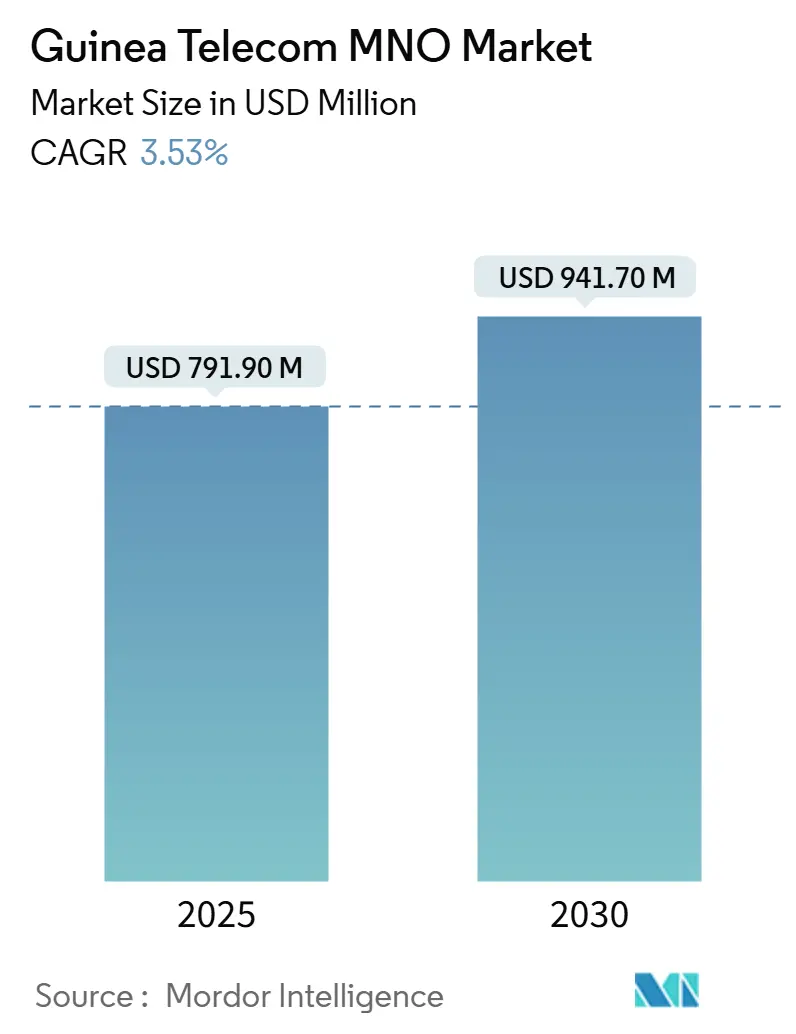

| Market Size (2025) | USD 791.90 Million |

| Market Size (2030) | USD 941.70 Million |

| Growth Rate (2025 - 2030) | 3.53% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Guinea Telecom MNO Market Analysis by Mordor Intelligence

The Guinea Telecom MNO Market size is estimated at USD 791.90 million in 2025, and is expected to reach USD 941.70 million by 2030, at a CAGR of 3.53% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 14.5 million subscribers in 2025 to 17.90 million subscribers by 2030, at a CAGR of 4.22% during the forecast period (2025-2030).

This muted trajectory reflects the transition from network roll-out to operational consolidation after MTN Group divested its local subsidiary to the State of Guinea in December 2024. [1]IT News Africa Staff, “MTN Sells Guinea Unit to State,” IT News Africa, itnewsafrica.com Growth is sustained by rising data demand, low-cost smartphones, and government-backed fiber projects, yet tempered by chronic power deficits and limited submarine-cable redundancy. Competitive intensity is increasing as Orange, Telecel (ex-MTN) and Africell strengthen 4G coverage while preparing for satellite-based disruption. Monetization prospects hinge on mobile money expansion, enterprise cloud adoption in the mining corridor, and cross-border fiber links that lower wholesale bandwidth pricing—factors that together underpin the long-run outlook for the Guinea telecom MNO Market.

Key Report Takeaways

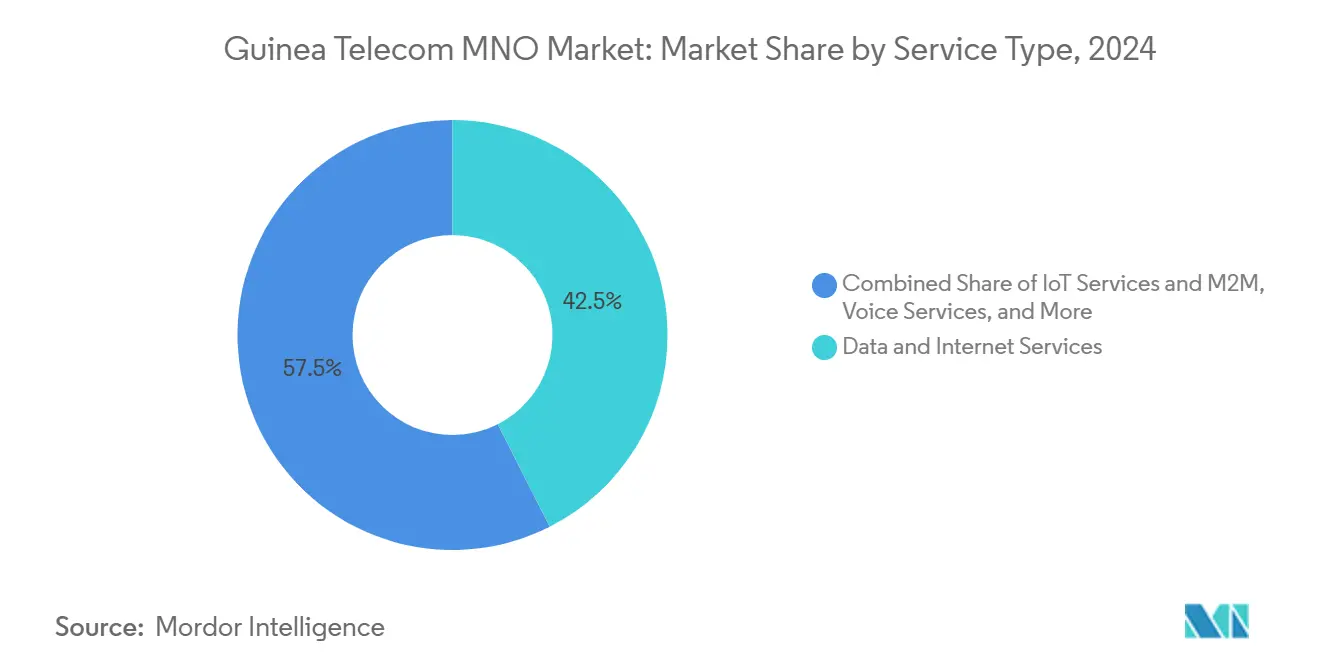

- By service type, data and internet services held 42.53% of Guinea telecom MNO Market share in 2024, and IoT services are projected to grow at a 3.39% CAGR to 2030.

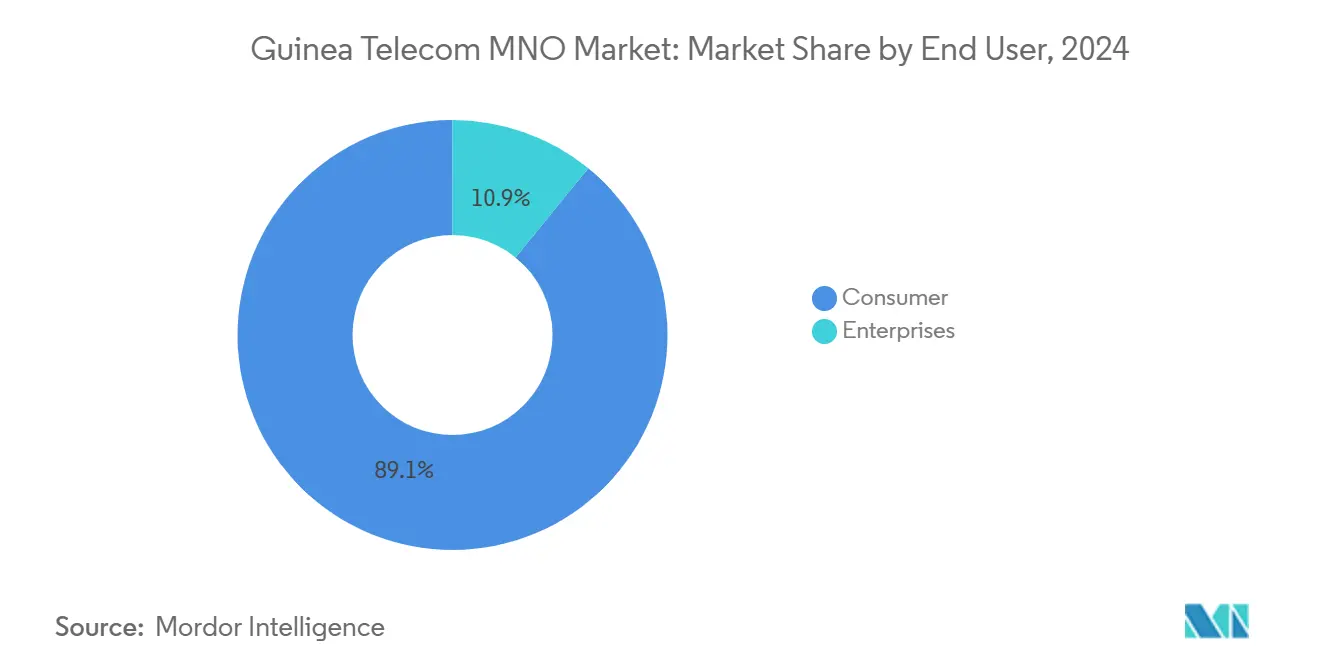

- By end user, the consumer segment generated 89.13% of 2024 revenue, whereas enterprise lines are poised for the fastest growth at a 5.10% CAGR over the forecast horizon.

Guinea Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 4G/4.5G network densification in Conakry and regional corridors | +0.3% | Conakry, Kankan and Labé corridors | Medium term (2-4 years) |

| Government-backed National Backbone fiber expansion (WB PADESCE project) | +0.2% | National | Long term (≥ 4 years) |

| Surge in mobile money transactions driving data traffic monetization | +0.4% | Nationwide, urban-led | Short term (≤ 2 years) |

| Planned entrance of Starlink and other LEO constellations | +0.1% | Rural and underserved regions | Medium term (2-4 years) |

| Multicloud adoption by mining exporters | +0.2% | Boké, Kindia, Forécariah | Medium term (2-4 years) |

| Low-priced Chinese smartphones (< USD 50) accelerating 4G handset uptake | +0.3% | National, rural bias | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

4G/4.5G network densification in Conakry and regional corridors

Operators are adding radios on 1800 MHz, 2600 MHz and 700 MHz layers to relieve congestion in the capital as data usage climbs. Orange launched LTE-A using carrier aggregation in 2019, reinforcing the commercial argument for deeper site grids along the Conakry-Kindia-Mamou logistics axis. Denser cells improve user throughput and reduce churn, spurring average revenue per user uplift that supports the Guinea telecom MNO Market. [2]Powertec Editorial, “Orange Guinea Activates LTE-A,” Powertec, powertec.com.au

Government-backed National Backbone fiber expansion (WB PADESCE project)

The World Bank’s PADESCE program channels USD 34 million into a 4,000 km optical backbone that interconnects interior cities and links to Mali and Côte d’Ivoire. The rollout addresses the single-cable vulnerability of the ACE landing station and introduces wholesale competition that gradually lowers bandwidth prices. Enhanced backhaul capacity enables reliable fixed and mobile broadband, underpinning the long-term growth of the Guinea telecom MNO Market. [3]World Bank Project Team, “Guinea – PADESCE,” World Bank Group, worldbank.org

Surge in mobile money transactions driving data traffic monetization

Orange Money adoption accelerates because fewer than 5% of Guineans hold bank accounts, pushing cashless payment volumes over EUR 2 billion across Africa in 2024, with Guinea a material contributor. Every transaction triggers SMS or USSD confirmations, nudging customers toward heavier data use via balance checks and in-app services. The virtuous cycle increases blended ARPU and stabilizes revenue in the Guinea telecom MNO Market.

Low smartphone ASPs from Chinese OEMs accelerating 4G handset penetration

Tecno, Itel and Infinix offer dual-SIM 4G smartphones retailing for less than USD 50, a price point aligned with local purchasing power. Transsion brands captured 48.2% of Africa’s smartphone shipments in Q4 2020, confirming the potency of ultra-low pricing. Affordable devices unlock latent demand for video streaming and social media, boosting data volumes that sustain the Guinea telecom MNO Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic electricity deficits inflating tower OPEX | -0.2% | Nationwide, rural intensification | Long term (≥ 4 years) |

| GNF volatility raising capex financing costs | -0.1% | National | Medium term (2-4 years) |

| Limited international fiber redundancy causing outages | -0.2% | Nationwide | Medium term (2-4 years) |

| SIM-tax hikes dampening multi-SIM uptake | -0.1% | Low-income segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic electricity deficits inflating tower OPEX

Less than half of Guinean mobile sites enjoy stable grid power, compelling operators to run diesel generators that raise operating costs by up to 50% compared with grid-fed sites. Elevated OPEX squeezes margins and slows rural network rollout, restraining the Guinea telecom MNO Market.

Limited international fiber redundancy creating frequent outages

The ACE cable is Guinea’s single international gateway. Outages or maintenance events reduce throughput nation-wide, disrupting enterprise traffic and mobile data sessions. Government initiatives to join the Cap Amílcar Cabral cable and to light cross-border fiber with Côte d’Ivoire aim to alleviate this risk, but redundancy remains limited until 2027. Intermittent latency spikes undermine user experience and temper revenue momentum across the Guinea telecom MNO Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and internet services reshape revenue composition

Data and internet services generated 42.53% of total revenue in 2024, underscoring the pivot from voice toward bandwidth-centric products. The Guinea telecom MNO Market size attributable to data is forecast to climb in line with smartphone penetration and fiber backhaul upgrades. IoT connectivity, though nascent, is expanding at 3.29% CAGR. Voice remains meaningful, yet over-the-top calling erodes minutes, nudging operators to bundle data-heavy apps. Mobile money integration adds stickiness, giving carriers cross-sell leverage in the Guinea telecom MNO Market.

A broader service stack that blends OTT video, cloud storage and gaming positions operators for incremental revenue per subscriber. The outlook assumes continued subsidy of entry-level smartphones to unlock rural demand. As data monetization deepens, contribution from SMS and traditional VAS will decline, but tailored enterprise solutions for remote SCADA and telemetry feed higher-margin growth inside the Guinea telecom industry.

By End User: Enterprise momentum overtakes consumer saturation

Consumers generated 89.13% of 2024 service revenue, but SIM saturation and unit-price erosion mean growth is flattening. Enterprise lines expand at 5.10% CAGR as miners, banks and tech start-ups procure capacity for ERP, IoT and cybersecurity. The Guinea telecom MNO Market share weighted toward enterprise will rise as operators carve tiered service-level agreements and edge-cloud nodes near industrial clusters.

Public-sector digitization amplifies demand through e-tax, health-information systems and biometric ID databases, each requiring resilient IP connectivity. Meanwhile, rural micro-SMEs embrace USSD-linked inventory apps, a sign that data-lite solutions extend enterprise revenue beyond large accounts. Consumer ARPU gains depend on bundling streaming music and local language video—services that ride on the broader network improvements funded in part by enterprise contracts, closing a virtuous investment loop within the Guinea telecom MNO Market.

Geography Analysis

Commercial returns concentrate inside the Conakry urban footprint, where disposable incomes and smartphone ownership are highest. International capacity lands at Kaporo beach, enabling lower latency and fostering a vibrant digital-services scene. Yet the Guinea telecom MNO Market can no longer rely solely on coastal demand. Corridor investment along the Conakry-Kindia-Mamou-Kankan axis pushes fiber deeper, piggy-backing on highway and rail upgrades that serve the mining belt.

Interior prefectures such as Labé and N'Zérékoré exhibit double-digit traffic growth off small bases, catalyzed by education portals and diaspora video calls. The Guinea telecom MNO Market size extracted from these regions remains modest in 2025, but share of new base-station deployments is rising as tower-cos sign build-to-suit deals subsidized by energy-as-a-service contracts. World Bank funding encourages operators to extend open-access fiber to community e-centers, narrowing the digital gap.

Cross-border links to Mali and Côte d’Ivoire create a budding role for Guinea as a regional transit hub, opening wholesale revenue streams that diversify operator balance sheets. Frontier zones abutting Sierra Leone and Liberia remain under-served, constrained by terrain and intermittent security. Satellite service could leapfrog some bottlenecks, but policy clarity on licensing and landing rights will determine uptake. Overall, geography continues to dictate cost curves and competitive behavior within the Guinea telecom MNO Market.

Competitive Landscape

Market leadership rests with Orange Guinée, followed by Telecel Guinée (the re-branded ex-MTN asset) and Africell. Orange leverages brand equity, 4G spectrum depth and the Orange Money platform, helping it capture premium subscribers and enterprise accounts. Telecel is navigating post-acquisition integration while evaluating capital-expenditure commitments amid uncertain forex conditions. Africell positions on value pricing and youth-oriented campaigns, banking on agile marketing rather than scale economies.

Technology investment centers on LTE-Advanced features and IP-MPLS backbones. Fiber joint-ventures reduce duplication, but operators differentiate through urban small-cell density and rural coverage reach. Starlink’s imminent entry injects disruptive potential: service quality independent of terrestrial grids reshapes benchmarks in remote prefectures, forcing incumbents to revisit pricing and retention strategies.

Strategic partnerships expand beyond telecom: Orange teams with Ecobank on digital-wallet interoperability, while Telecel explores edge-cloud collaborations with mining majors. Tower-co carve-outs remain on the agenda as operators hunt for balance-sheet flexibility to fund 5G trials expected post-2028. Despite consolidation, the Guinea telecom MNO Market still allows niche MVNO models tied to diaspora calling cards or sector-specific data plans, although regulatory clarity on wholesale access remains pending.

Guinea Telecom MNO Industry Leaders

-

Orange Guinea

-

Telecel Guinea

-

Cellcom Guinea

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: MTN completed the sale of its Guinean subsidiary to the State of Guinea, realigning competitive dynamics.

- September 2024: Guinea’s telecom ministry agreed to link its optical backbone with Côte d’Ivoire to enhance redundancy.

- July 2024: Cross-border fiber between Guinea and Mali was commissioned, lowering backhaul latency for mining operations.

- March 2024: MTN revealed plans to sell its Guinea stake to Telecel as part of its Ambition 2025 portfolio review.

Guinea Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current size of the Guinea telecom MNO Market?

The Guinea telecom MNO Market size stands at USD 791.9 million in 2025 and is projected to reach USD 941.7 million by 2030.

Which service type generates the most revenue?

Data and internet services lead with 42.53% revenue share, reflecting user migration toward bandwidth-intensive applications.

Why is enterprise demand increasing faster than consumer demand?

Cloud adoption in bauxite mining and government digitization programs are driving enterprise connectivity at a 5.10% CAGR.

What are the main obstacles to network expansion in rural Guinea?

Chronic electricity shortages inflate operating costs, and the reliance on a single submarine cable limits international capacity.

Could satellite broadband disrupt the market?

Yes. Starlink’s planned launch offers high-throughput coverage to remote areas, pressuring incumbent operators to improve rural service quality.

Page last updated on: