Honduras Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

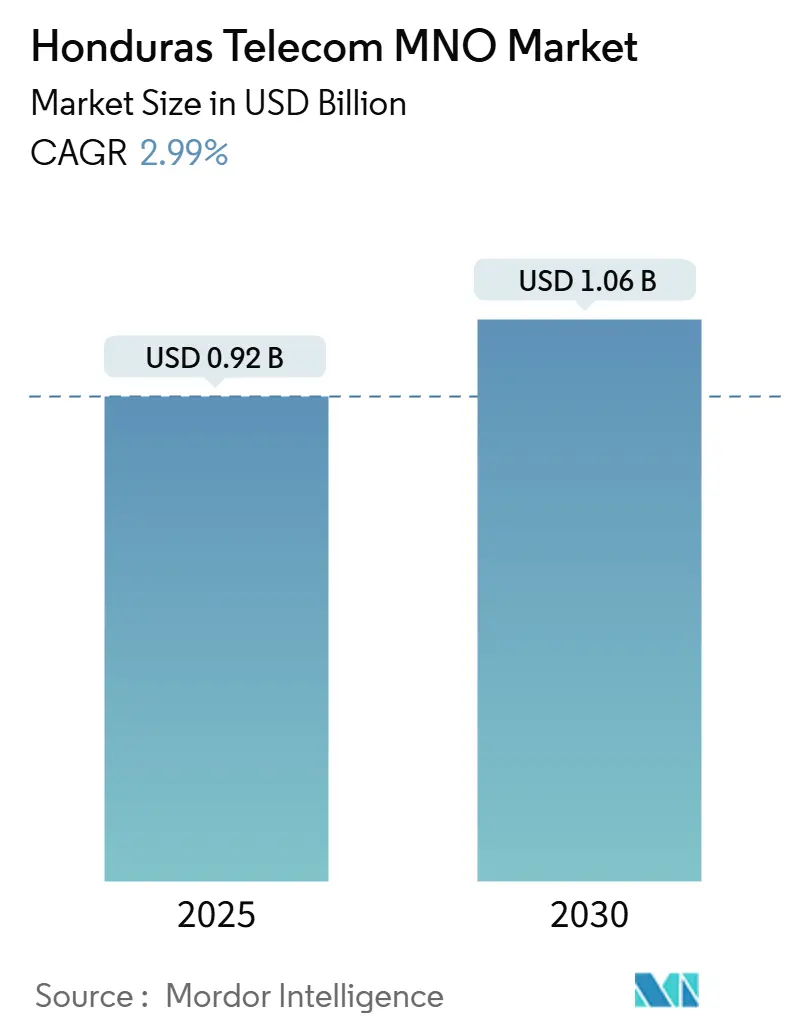

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.06 Billion |

| Growth Rate (2025 - 2030) | 2.99% CAGR |

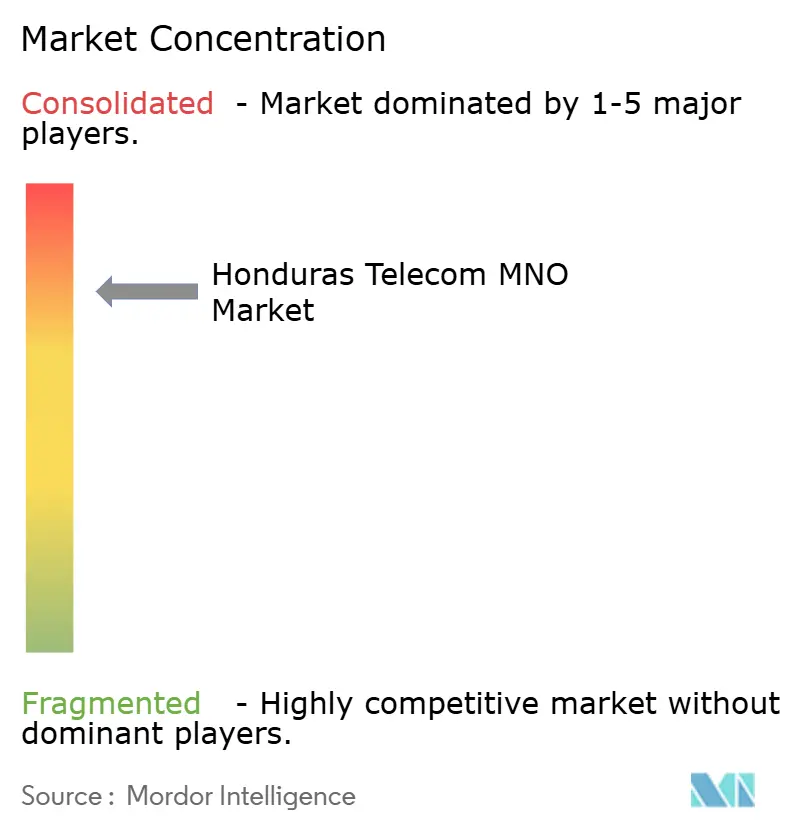

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Honduras Telecom MNO Market Analysis by Mordor Intelligence

The Honduras Telecom MNO Market size is estimated at USD 0.92 billion in 2025, and is expected to reach USD 1.06 billion by 2030, at a CAGR of 2.99% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 7.70 million subscribers in 2025 to 8.80 million subscribers by 2030, at a CAGR of 2.63% during the forecast period (2025-2030).

Honduras Telecom MNO market momentum rests on high mobile penetration of 87.57%, expanding 4G coverage that already serves 80% of the population, and sizable operator investment programs targeting capacity upgrades and rural build-outs. Demand shifts from voice toward digital services are reinforced by rising smartphone penetration, diaspora-driven mobile money usage and the government’s Digital Republic program, all of which encourage data-centric revenue streams. Operator tower-sharing deals, notably Millicom’s USD 975 million sale-and-lease-back agreement with SBA Communications, further lower deployment costs and support quality of service gains.

Key Report Takeaways

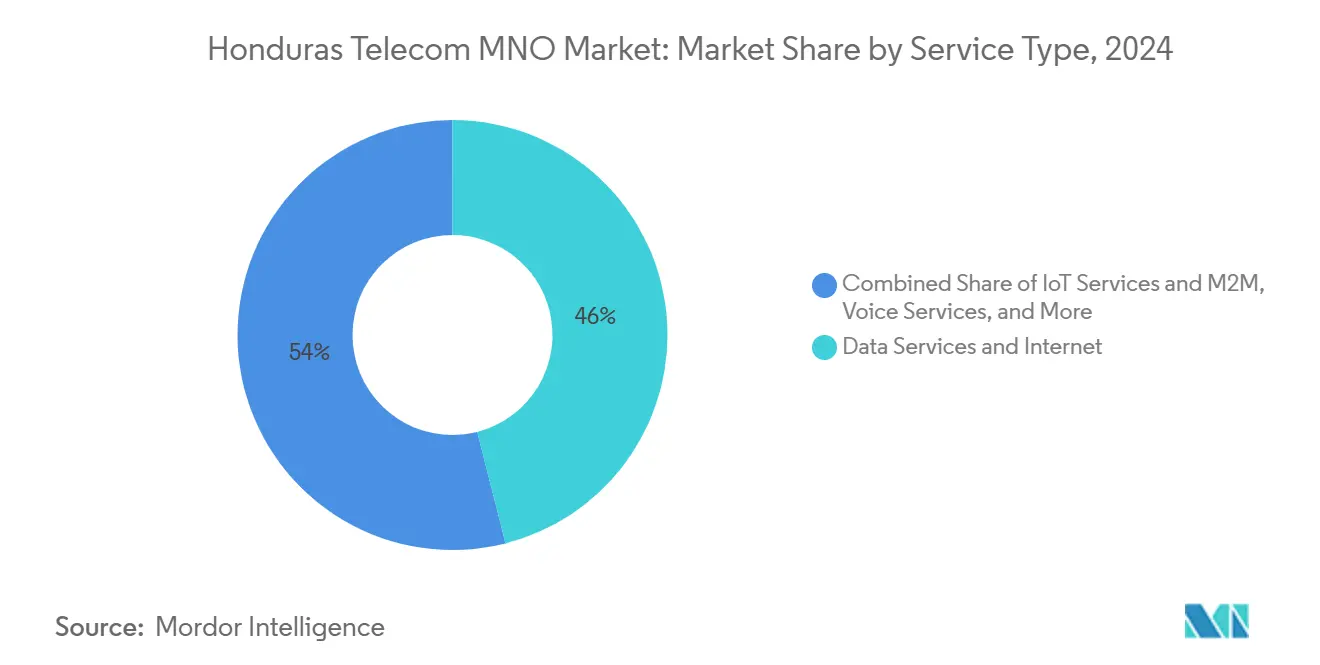

- By service type, data services led with 46.04% revenue share in 2024; IoT and M2M are forecast to expand at a 3.43% CAGR through 2030.

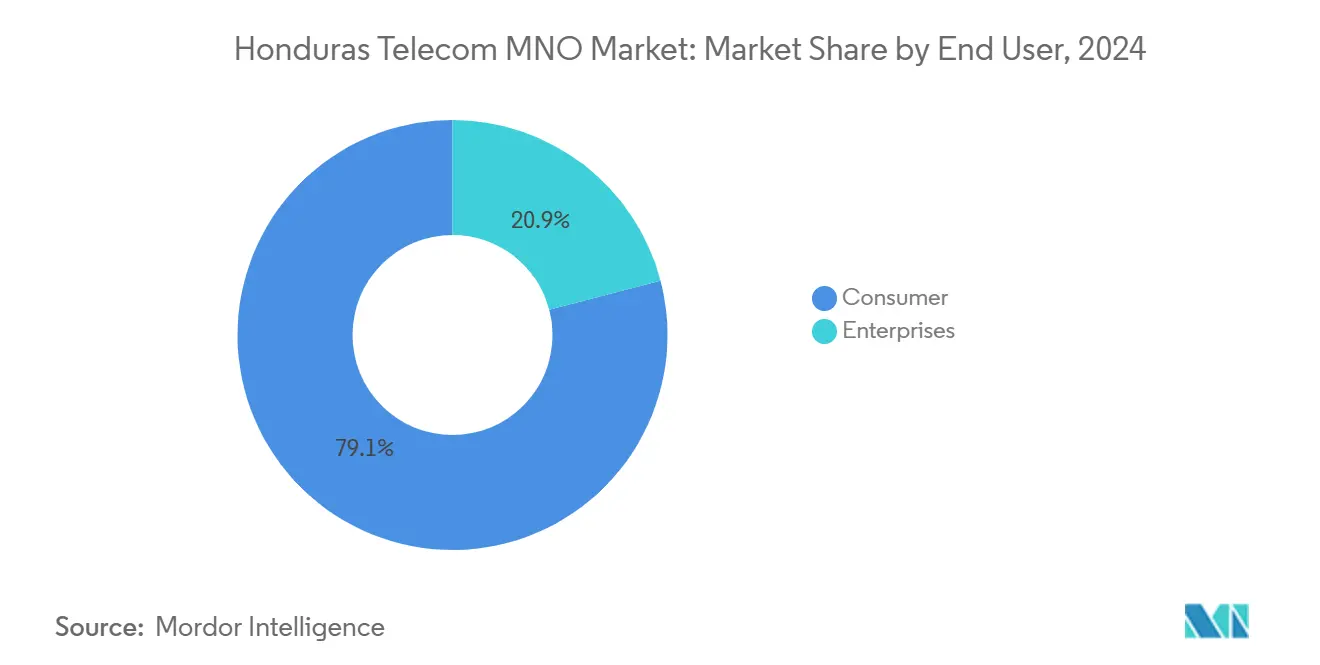

- By end user, consumer accounts for 79.06% of 2024 revenue; enterprise is advancing at a 4.15% CAGR to 2030.

Honduras Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded 4G LTE coverage in rural regions | +0.8% | National (rural municipalities) | Medium term (2-4 years) |

| Growing mobile data consumption per capita | +0.7% | Urban centers with rural spillover | Short term (≤ 2 years) |

| Government spectrum allocations for 5G readiness | +0.4% | National, beginning with Tegucigalpa and San Pedro Sula | Long term (≥ 4 years) |

| Increasing smartphone penetration via affordable Chinese handsets | +0.6% | National | Short term (≤ 2 years) |

| Diaspora-backed demand for digital financial services | +0.5% | Remittance-receiving communities | Medium term (2-4 years) |

| Rapid SME adoption of fixed-wireless access | +0.3% | Urban and semi-urban business districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanded 4G LTE Coverage in Rural Regions

Rural build-outs narrow the connectivity gap that still leaves more than one-third of Honduran villages underserved, despite national 4G availability now topping 80% of residents. CONATEL’s National Frequency Allocation Plan incentivizes coverage obligations, while Millicom’s and SBA Communications’ 7,000-site agreement underwrites tower density in low-ARPU areas. Additional network reach is critical because mobile broadband adoption shows a positive correlation with GDP per capita rise, making rural connectivity a shared policy and commercial priority. [1]Comisión Nacional de Telecomunicaciones, “Plan Nacional de Atribución de Frecuencias,” conatel.gob.hn

Growing Mobile Data Consumption Per Capita

Median download speeds have surpassed 35 Mbps, enabling video streaming, social networking and cloud usage at scale. Data already provides 46.04% of operator turnover, and rising smartphone penetration—propelled by low-cost Chinese models and device-financing plans—keeps traffic expanding faster than subscriber growth. Competitive differentiation has therefore shifted toward content delivery quality and bundled digital services. [2]International Trade Administration, “Honduras – Telecommunications,” trade.gov

Government Spectrum Allocations for 5G Readiness

Although Honduras Telecom MNO market participants do not expect commercial 5G before 2028, CONATEL is clearing mid-band blocks, aligning with Digital Republic targets and World Radiocommunications Conference outcomes. Predictable spectrum roadmaps lower investment risk and allow operators to plan migration strategies that reuse existing infrastructure where possible, improving long-run return on invested capital.

Increasing Smartphone Penetration via Affordable Chinese Handsets

Aggressive unit pricing by Chinese OEMs has lifted smartphone ownership well above 60% of total mobile connections, including many first-time rural adopters. Higher device capability expands engagement with data plans and mobile financial services such as Tigo Money, supporting new revenue layers beyond connectivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High poverty levels limiting ARPU growth | -0.4% | National (rural focus) | Long term (≥ 4 years) |

| Limited national backbone fiber infrastructure | -0.3% | National, strongest in rural zones | Medium term (2-4 years) |

| Persistent electricity outages affecting tower uptime | -0.2% | National | Short term (≤ 2 years) |

| Complex municipal right-of-way fees slowing fiber rollout | -0.2% | Urban and semi-urban corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Poverty Levels Limiting ARPU Growth

While Honduras Telecom MNO market penetration is high, disposable income remains constrained. Household telecom spend represents a higher proportion of earnings than in OECD economies and keeps prepaid uptake above 90%. Tiered bundles help protect volumes, yet limit ARPU expansion potential over the forecast horizon. [3]U.S. Department of State, “Investment Climate Statement: Honduras 2024,” state.gov

Limited National Backbone Fiber Infrastructure

Honduras still ranks low on fixed broadband speed tests, with only 28.84 Mbps median uploads. Insufficient domestic fiber backbone elevates backhaul costs and curbs network capacity, especially in dense urban foot-prints where 4G traffic growth is steepest. Ongoing multilateral loans are extending reach, but last-mile fiber rollouts remain subject to municipal red-tape that postpones monetization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and internet services produced 46.04% of Honduras Telecom MNO market size in 2024 and are forecast to remain the dominant revenue pillar through 2030. Voice still yields substantial cash flow but faces gradual substitution by OTT messaging. IoT and M2M, today a low-base line of business, is the fastest growing segment at a 3.43% CAGR, benefiting from smart city pilots and fleet telematics deployments. Honduras Telecom MNO market share for data-led bundles is reinforced by median download speeds exceeding 35 Mbps and tower upgrades that enable advanced modulation, while OTT video and PayTV add upselling headroom. Millicom’s multi-play mix—about one-third cable, half mobile, and 10% financial services—illustrates the structural shift operators are pursuing for margin resilience.

Spanish-language content partnerships, zero-rated social media packs and progressive data rollover schemes further lift customer lifetime value. Fixed-wireless access over 4G also expands addressable broadband markets where copper loops are absent, supporting service diversification.

By End User: Consumer Dominance with Enterprise Growth Potential

Consumer users contributed 79.06% of Honduras Telecom MNO market size in 2024. Strong diaspora remittances—USD 7.5 billion annually—finance handset purchases and top-ups, sustaining prepaid volumes even during macro volatility. However enterprise revenue is forecast to expand at a 4.15% CAGR as SMEs adopt cloud storage, cybersecurity and FWA broadband. Government Digital Republic mandates also encourage ministries and municipalities to migrate to e-procurement and tele-health platforms, widening institutional data demand. Honduras Telecom MNO market share for enterprise connectivity remains modest but rising as service catalogs extend to SD-WAN, IoT SIM management and mobile money payroll disbursement.

Bundled mobile plus fixed capacity, service-level agreements and dedicated account management now feature in operator offers, positioning carriers as strategic ICT partners rather than pure connectivity suppliers. This trend is likely to accelerate once backbone fiber constraints ease, enabling higher-value SLAs.

Geography Analysis

Urban-rural divides shape investment priorities. Tegucigalpa and San Pedro Sula account for a disproportionate share of GDP and generate the highest ARPU profiles, helped by near-ubiquitous 4G and ongoing fiber densification. San Pedro Sula’s Technology District project, backed by a USD 11 million Inter-American Development Bank loan, exemplifies municipal-level smart city ambitions that stimulate enterprise connectivity and public Wi-Fi demand. Rural areas still lag, with 4G availability reaching 50.7% in isolated districts, but tower sharing and universal-service subsidies are shrinking the coverage gap. Indigenous Mosquitia Hondureña communities remain underserved, yet community mesh networks demonstrate that low-cost solutions can extend service footprint where classic return on investment is weak.

Geographic spectrum maps indicate that fresh 700 MHz blocks will prioritize sparsely populated corridors, providing better propagation and lowering site counts per square kilometer. The same bands support FWA, a compelling broadband option for rural SMEs lacking copper or fiber. Honduras Telecom MNO market growth therefore hinges on balancing densification in wealth-concentrated cities with disciplined capital allocation in low-density zones.

Remittance inflows concentrate in western departments, catalyzing uptake of mobile money and micro-insurance, while Caribbean coastal regions benefit from port activity that demands reliable IoT tracking for logistics chains. Weather-related risks, especially hurricane-induced outages, underscore the strategic importance of diversified backhaul paths and battery backup at tower sites.

Competitive Landscape

Honduras Telecom MNO market structure is highly concentrated: two multinational subsidiaries hold 99% combined share, resulting in a market concentration score of 8. Tigo Honduras leads with about 60%, leveraging superior rural footprint and recognized 4G coverage leadership. Claro Honduras commands roughly 39%, differentiating through higher average content-streaming throughput and a USD 200 million Latin American fiber program that increases backbone scale. Hondutel’s sub-1% share reflects prolonged under-investment and historical cash outflows that eroded competitiveness.

Service competition centers on bundling rather than price wars. Tigo pushes quad-play packages—mobile, PayTV, fixed broadband and mobile money—to lift household share-of-wallet. Claro emphasizes post-paid loyalty programs and device subsidies. Both giants lock customers via zero-interest handset financing, prepaid bonuses and unlimited social media passes. Network quality is used as the primary competitive lever, supported by tower-sharing to reduce overlapping capital spend.

Strategic partnerships underpin efficiency. Millicom’s USD 975 million tower sale to SBA Communications grants long-term leases at lower cost of capital, directing freed cash toward 4G capacity and future 5G preparations. Claro benefits from América Móvil’s regional procurement scale for core equipment and fiber. Enterprise solution portfolios expand into IoT, cybersecurity and cloud interconnect, while rural coverage obligations become a reputational differentiator aligning operators with national inclusion goals.

Honduras Telecom MNO Industry Leaders

Tigo Honduras (Millicom)

Claro Honduras (America Movil)

Hondutel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: CONATEL updated its National Frequency Allocation Plan to optimise spectrum for evolving telecom demand Vlex.

- October 2024: Millicom (Tigo) and SBA Communications agreed on a USD 975 million tower sale-and-lease-back covering 7,000 sites BNamericas.

- September 2024: Claro confirmed a USD 200 million regional fiber investment to support AI-ready infrastructure BNamericas.

- August 2024: Honduras reached 80% 4G population coverage, supported by a 6.5% CAGR in tower count Telecom Advisory Services.

Honduras Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Honduras Telecom MNO market in 2025?

Honduras Telecom MNO market size stands at USD 918.39 million in 2025.

What is the expected CAGR for Honduran mobile network operator revenue through 2030?

Total revenue is projected to advance at a 2.99% CAGR during 2025-2030.

Which operator holds the highest subscriber share in Honduras?

Tigo Honduras leads with around 60% Honduras Telecom MNO market share.

Which service type is growing fastest?

IoT & M2M posts the highest forecast growth at 3.43% CAGR to 2030.

What initiatives are preparing Honduras for 5G?

CONATEL’s spectrum roadmap and Digital Republic projects align spectrum, fiber and e-government demand to enable future 5G launches.

Why is enterprise revenue expected to outpace consumer revenue growth?

SMEs and public agencies are accelerating digital transformation, boosting demand for cloud, cybersecurity and fixed-wireless access services at a 4.15% CAGR through 2030.

Page last updated on: