Papua New Guinea Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

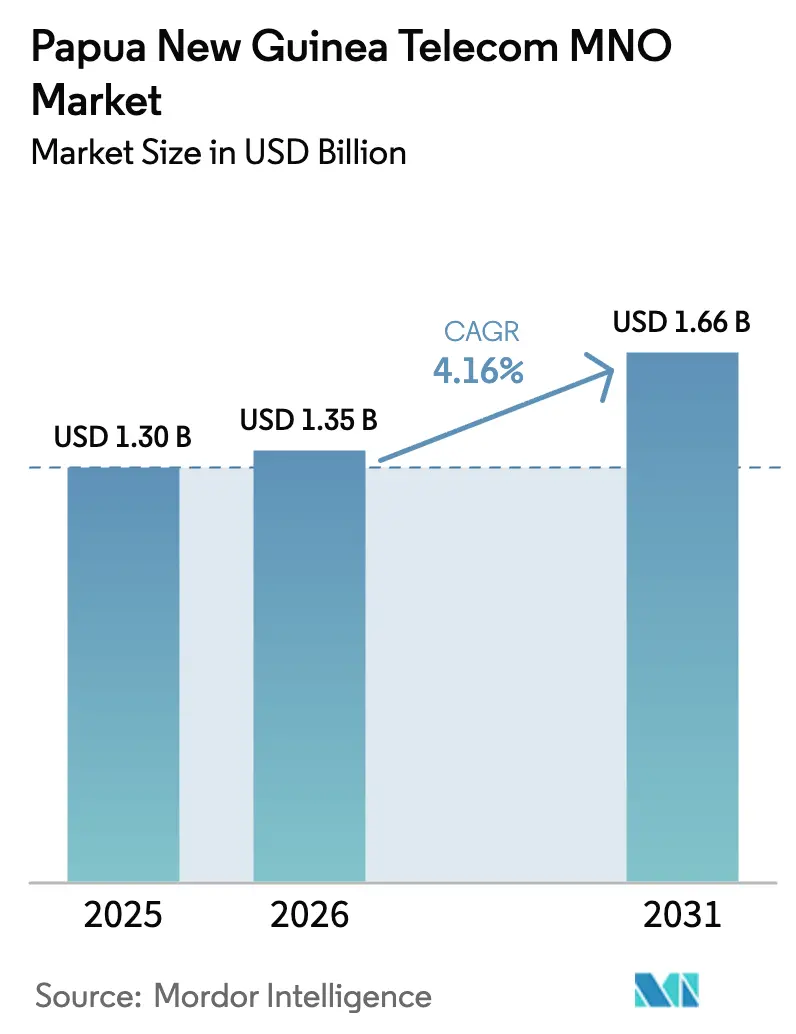

| Base Year Market Size (2025) | USD 1.30 Billion |

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Papua New Guinea Telecom MNO Market Analysis by Mordor Intelligence

The Papua New Guinea Telecom MNO Market size is expected to grow from USD 1.30 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 1.66 billion by 2031 at 4.16% CAGR over 2026-2031.

Demand is being propelled by submarine-cable capacity upgrades, rising mobile-data adoption, and expanding enterprise connectivity needs. [1]Coral Sea Cable Company, “The System,” coralseacablecompany.comReforms that clarify spectrum policy and mandate infrastructure sharing are prompting strategic investment, while satellite licensing widens reach to remote islands. [2]National Information and Communication Technology Authority, “Official Statement on the Licensing of Starlink,” nicta.gov.pg The Papua New Guinea telecom MNO market also benefits from universal-service subsidies that de-risk rural roll-outs and from a youthful population that is embracing digital services at pace. Competitive intensity is high but largely confined to three national operators plus one wholesale backbone provider, keeping price wars in check yet spurring coverage expansion.

Key Report Takeaways

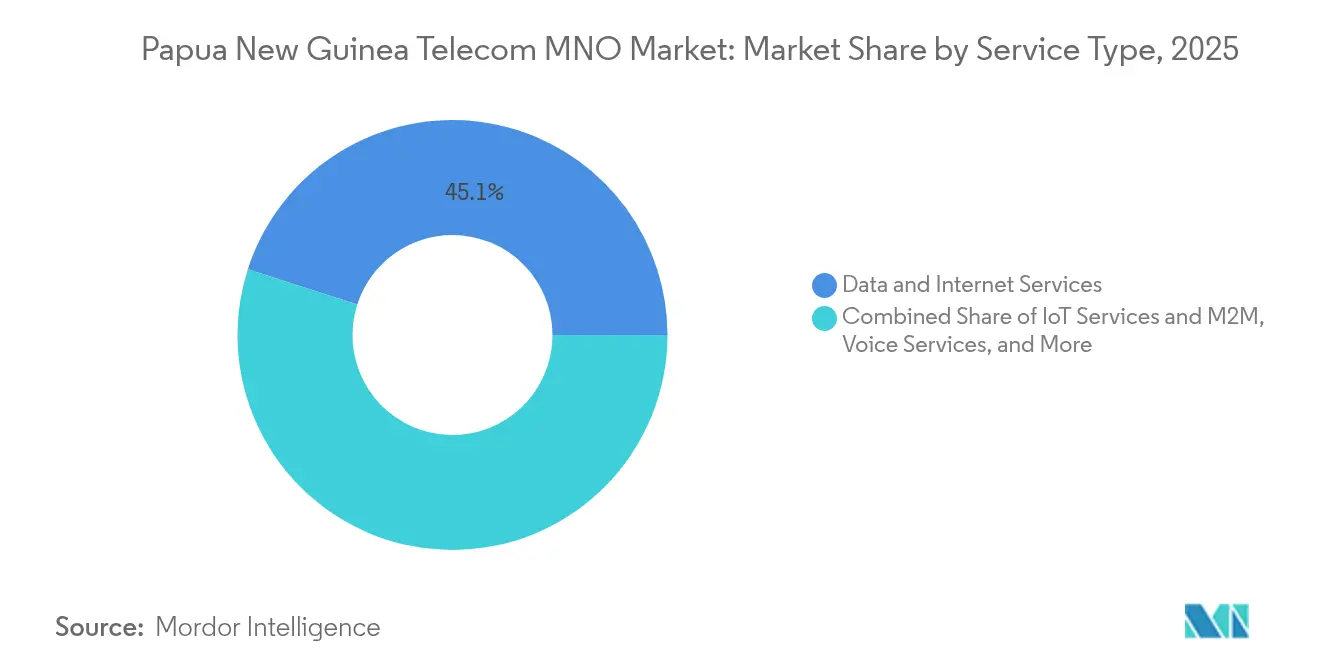

- By service type, data services led with 45.05% revenue share in 2025. IoT and M2M solutions are forecast to post the fastest 4.23% CAGR through 2031.

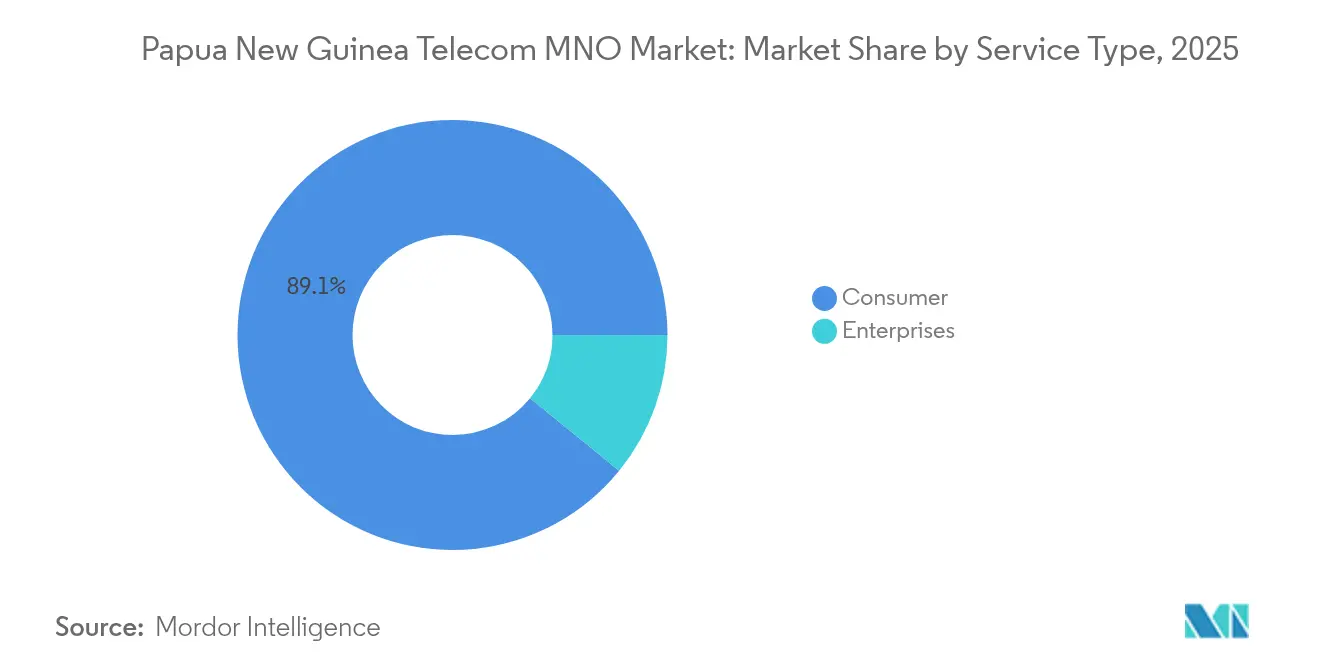

- By end user, consumer connections held 89.12% of the Papua New Guinea telecom MNO market share in 2025. Enterprise demand is projected to expand at a 5.03% CAGR to 2031 on the back of cloud adoption targets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Papua New Guinea Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding mobile-data consumption | +1.2% | Port Moresby, Lae, Mount Hagen | Medium term (2-4 years) |

| Government USO and rural-connectivity projects | +0.8% | Highlands and island provinces | Long term (≥4 years) |

| 4G expansion and 5G-ready spectrum roadmap | +0.7% | Urban hubs and provincial capitals | Medium term (2-4 years) |

| Coral Sea Submarine Cable boosts backhaul | +0.5% | National | Short term (≤2 years) |

| Mobile-money led digital-financial inclusion | +0.4% | Rural and unbanked areas | Long term (≥4 years) |

| LEO satellite gateways for remote islands | +0.3% | Outlying islands and mountains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exploding Mobile-Data Consumption

Average monthly mobile-data use now mirrors Pacific peers as affordable smartphones flood the market and youth under 25 comprise 63% of the population. Digicel’s March 2025 tariff revamp introduced bundles up to 307 GB with rollover, accelerating uptake. [3]Digicel Pacific, “Data Plans,” digicelpacific.com Progress on the cloud-first government program—40% of public services already online—adds institutional traffic and normalizes digital workflows. These trends raise revenue per gigabyte even as unit prices fall, translating directly into sustained growth for the Papua New Guinea telecom MNO market.

Government USO and Rural-Connectivity Projects

The USD 1.2 billion Connect PNG launch targets 78% coverage and links 13 economic corridors, guaranteeing long-term demand for wholesale bandwidth and retail voice-data products. Parallel goals to bring 70% of citizens online by 2030 channel predictable capital into towers, fiber spurs, and power back-up systems. Asian Development Bank funding of USD 675 million for infrastructure and health increases indirect telecom usage as e-services become embedded. Collectively, the initiatives remove coverage white spots and enlarge the addressable base for the Papua New Guinea telecom MNO market.

4G Expansion and 5G-Ready Spectrum Roadmap

NICTA’s modernized licensing paves the way for seamless 5G migration while ensuring fair access to the 700 MHz and 3.5 GHz bands. Vodafone PNG’s 4G+ network already delivers 60 Mbps downlink across five cities, setting performance benchmarks that catalyze rival upgrades. Lessons from Fiji’s 5G pilots shorten learning curves and promote regional vendor collaboration. As coverage widens, smartphone users migrate from 3G, lifting ARPU and supporting verticals such as video streaming and agritech IoT—all incremental tailwinds for the Papua New Guinea telecom MNO market.

Coral Sea Submarine Cable Boosts Backhaul

The 4,700 km Coral Sea system supplies 40 Tbps into Port Moresby, cutting wholesale capacity costs by up to 80% and boosting speeds 100-fold over legacy links. Economic impact studies forecast USD 5 billion in added Pacific GDP by 2040 as latency-sensitive services become viable. Complementary inland fiber from PNG DataCo connects 14 cities to this gateway, aligning national traffic flows with international routes and strengthening the resilience of the Papua New Guinea telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and challenging topography | -0.9% | Highlands and outer islands | Long term (≥4 years) |

| Limited disposable income curbing ARPU | -0.6% | Rural and low-income urban | Medium term (2-4 years) |

| Opaque spectrum pricing deterring entrants | -0.3% | National | Short term (≤2 years) |

| Rising cyber-security breaches in SMEs | -0.2% | Business hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Challenging Topography

PNG’s 600 islands and rugged mountains force operators to rely on helicopters, satellite backhaul, and hybrid power, making tower builds up to 35% costlier than in Southeast Asia. Digicel’s 945 sites cover 85% of citizens but only 53% of landmass, illustrating the diminishing returns of incremental reach. Earthquake-related outages underline the need for hardened infrastructure, further pressuring capital budgets. The resultant expenditure suppresses free cash flow and may slow rural roll-outs in the Papua New Guinea telecom MNO market.

Limited Disposable Income Curbing ARPU

GDP per capita sits at USD 2,600, while mobile-data baskets still absorb 11.3% of GNI per capita—well above the 2% affordability target. Only 17% of residents hold bank accounts, constraining uptake of value-added and post-paid plans. Operators therefore prioritize volume-driven prepaid models with slim margins, limiting near-term ARPU expansion within the Papua New Guinea telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Growth

Data connections generated 45.05% of 2025 revenue, confirming that bandwidth rather than voice fuels the Papua New Guinea telecom MNO market. OTT bundles and video-friendly rates accelerated usage during 2024-25. The Papua New Guinea telecom MNO market size for IoT and M2M is projected to climb 4.23% annually to 2031 as mining, logistics, and utilities digitize operations. Voice retains cultural relevance for remote communities, yet its share continues to recede. Messaging revenue erodes under social-media cannibalization, but operators offset the slide by monetizing SMS for enterprise alerts. Mobile-money gateways such as CellMoni and MiCash add low-fee transfer revenue and deepen stickiness, powering data-led ecosystems that sustain lifetime value.

IoT adoption remains low today but early pilots in smart-metering and cold-chain tracking highlight latent opportunity. Submarine backhaul ensures the latency required for industrial telemetry, while NICTA’s spectrum plan ring-fences 80 MHz in the 3.5 GHz band for future 5G massive-machine-type deployments. As businesses scale sensor networks, the Papua New Guinea telecom MNO market size attributed to IoT services could represent a double-digit share of incremental revenue post-2028.

By End User: Enterprise Segment Accelerates Growth

Consumers delivered 89.12% of 2025 revenue on the back of 5.03 million SIMs, yet enterprise lines record the quicker 5.03% CAGR to 2031. Managed WAN, cloud connect, and cybersecurity packages appeal to banks, mining majors, and government agencies migrating to SaaS. PNG DataCo’s 7,000 km fiber gives MNOs wholesale options to craft SLA-backed services that capture corporate ICT budgets. Sprint Networks’ secure-edge roll-outs in 2025 signal growing demand for zero-trust architectures among SMEs.

On the consumer side, mobile-first households use smartphones for everything from school assignments to micro-payments, ensuring steady SIM growth even as ARPU stays flat. Facebook’s March 2025 blackout exposed platform dependence but also validated MNO network resilience when traffic shifted to alternative apps. As macro conditions improve, the Papua New Guinea telecom MNO market share of enterprise revenue is expected to widen, giving operators a hedge against consumer price sensitivity.

Geography Analysis

Urban centers dominate infrastructure allocation; Port Moresby and Lae enjoy contiguous 4G and fixed-fiber footprints that support premium bundles and corporate VPNs. The Coral Sea landing station and the national subsea loop create dual paths that buttress uptime for business districts, anchoring a disproportionate chunk of the Papua New Guinea telecom MNO market size.

Second-tier provincial capitals receive phased 4G upgrades financed by Connect PNG and tower-sharing directives. These cities exhibit surging smartphone penetration once coverage arrives, rapidly narrowing the digital divide. IoT pilot zones in mining towns of the Highlands illustrate demand beyond traditional hubs, providing the next layer of growth for the Papua New Guinea telecom MNO market.

Remote islands and mountainous interiors remain underserved. Starlink’s five-year licence and Telikom-Lynk’s Sat2Phone SMS service furnish lifelines where towers are uneconomic. With Universal-Service funds subsidising satellite OPEX, operators can break even faster while building brand equity among dispersed communities.

Competitive Landscape

The Papua New Guinea telecom MNO market is oligopolistic. Digicel controls roughly 91% of subscribers, leveraging 945 sites and Deep Blue One’s subsea redundancy to market uptime guarantees to enterprises. Vodafone PNG differentiates on aggressive 4G+ speeds and youth-oriented bundles, while Telikom PNG pivots to satellite-mobile convergence to capture far-flung users.

Regulation has begun to temper dominance: a USD 29 million market-concentration levy and mandatory infrastructure-sharing rules lowered Digicel’s pricing flexibility in 2024. Yet high CAPEX keeps new foreign entrants cautious, leaving spectrum reforms and wholesale fibre to foster quasi-competition. Starlink’s licence invalidates the historical tower monopoly for outer islands, compelling terrestrial MNOs to bundle satellite capacity into enterprise SLAs.

Corporate activity underscores strategic repositioning. Digicel’s 2025 prepaid overhaul added rollover and micro-credit features to shore up retention. Telikom PNG signed multi-satellite capacity leases to cover disaster-prone areas. Vodafone PNG pilots e-SIMs and fintech tie-ups to seize mobile-money flows previously cornered by banks. These moves collectively maintain momentum in the Papua New Guinea telecom MNO market.

Papua New Guinea Telecom MNO Industry Leaders

Digicel PNG Limited

Bemobile Limited

Telikom PNG Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Digicel launched refreshed prepaid data catalogue up to 307 GB with rollover.

- June 2024: Digicel switched on Deep Blue One cable using Infinera GX gear for 400G wavelengths

- January 2024: Telikom PNG and Lynk Global activated commercial Sat2Phone SMS service .

- January 2024: NICTA issued a five-year operating licence to Starlink.

Papua New Guinea Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How big is the Papua New Guinea telecom MNO market in 2026?

It generated USD 1.35 billion in 2026 and is on track for USD 1.66 billion by 2031 at a 4.16% CAGR.

Which service brings in the most revenue for operators?

Mobile data leads with 45.05% share, far ahead of voice and messaging

What is driving enterprise demand for connectivity?

Cloud adoption across government and mining plus rising cybersecurity requirements are lifting enterprise lines at a 5.03% CAGR.

How is backhaul capacity improving?

The Coral Sea and Deep Blue One subsea cables now supply 40 Tbps into the country, cutting wholesale costs and boosting speed.

Who dominates PNG’s mobile market today?

Digicel holds roughly 91% of subscribers, followed by Vodafone PNG and Telikom PNG.

Are satellite services available for remote islands?

Yes, Starlink received a five-year licence in 2024 and Telikom PNG offers Sat2Phone SMS through Lynk Global.

Page last updated on: