Sheet Face Masks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

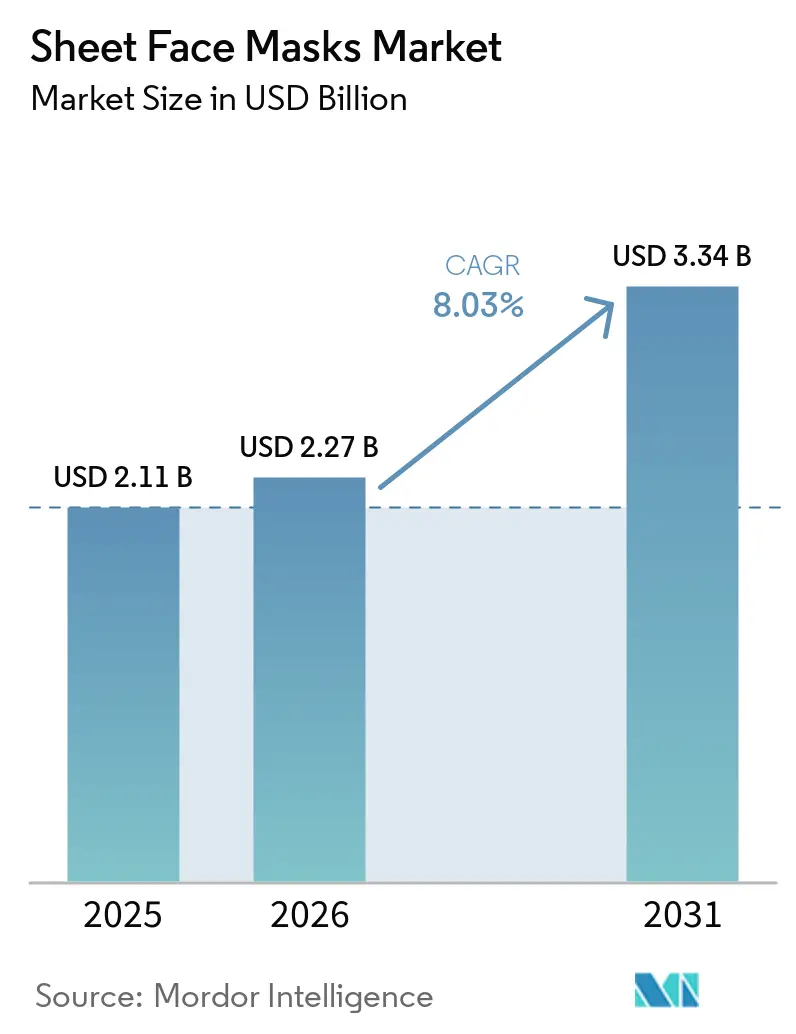

| Market Size (2026) | USD 2.27 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sheet Face Masks Market Analysis by Mordor Intelligence

The sheet face masks market size was valued at USD 2.1 billion in 2025 and is projected to reach USD 3.3 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031. The sheet face masks market is being supported by the wider spread of South Korean skincare routines, and that support became more visible when South Korean cosmetics exports rose, and the United States became the largest export destination. This shift is widening the retail base for the sheet face masks market in North America and Europe, where premium beauty chains and online storefronts now give Korean and Japanese brands better access to first-time users and repeat buyers. The sheet face masks market is also gaining from faster discovery through social commerce, because digital channels shorten the path between product awareness, trial, and refill, especially for smaller brands that do not depend on long retail listing cycles. At the same time, the sheet face masks market is moving toward better ingredients, clearer claims, and stronger format differentiation, which supports trade-up behavior even though mass products still account for most demand. Competitive conditions remain balanced, but brands that do not address packaging waste, counterfeit exposure, and traceability requirements are likely to lose pricing power as buyer scrutiny becomes more demanding.

Key Report Takeaways

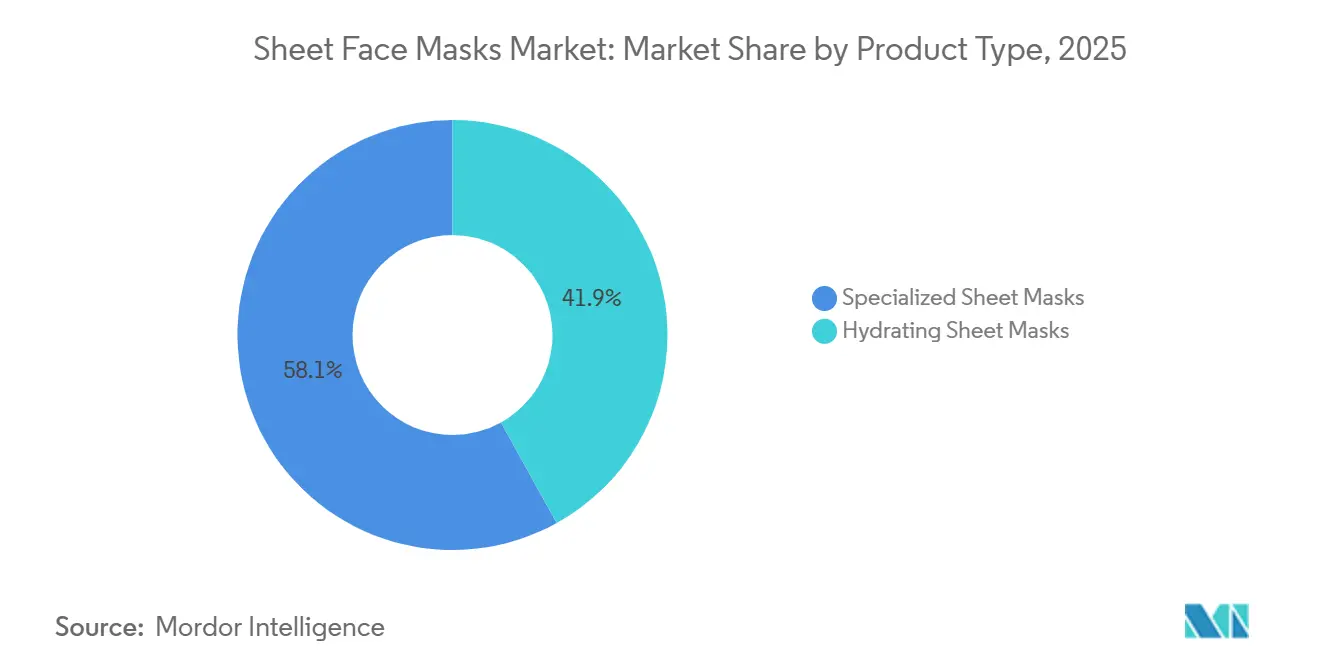

- By product type, specialized sheet face masks held 58.04% of revenue in 2025, while hydrating sheet face masks are projected to grow at an 8.41% CAGR through 2031.

- By price, mass products accounted for 68.32% of revenue in 2025, while premium products are projected to expand at a 9.13% CAGR through 2031.

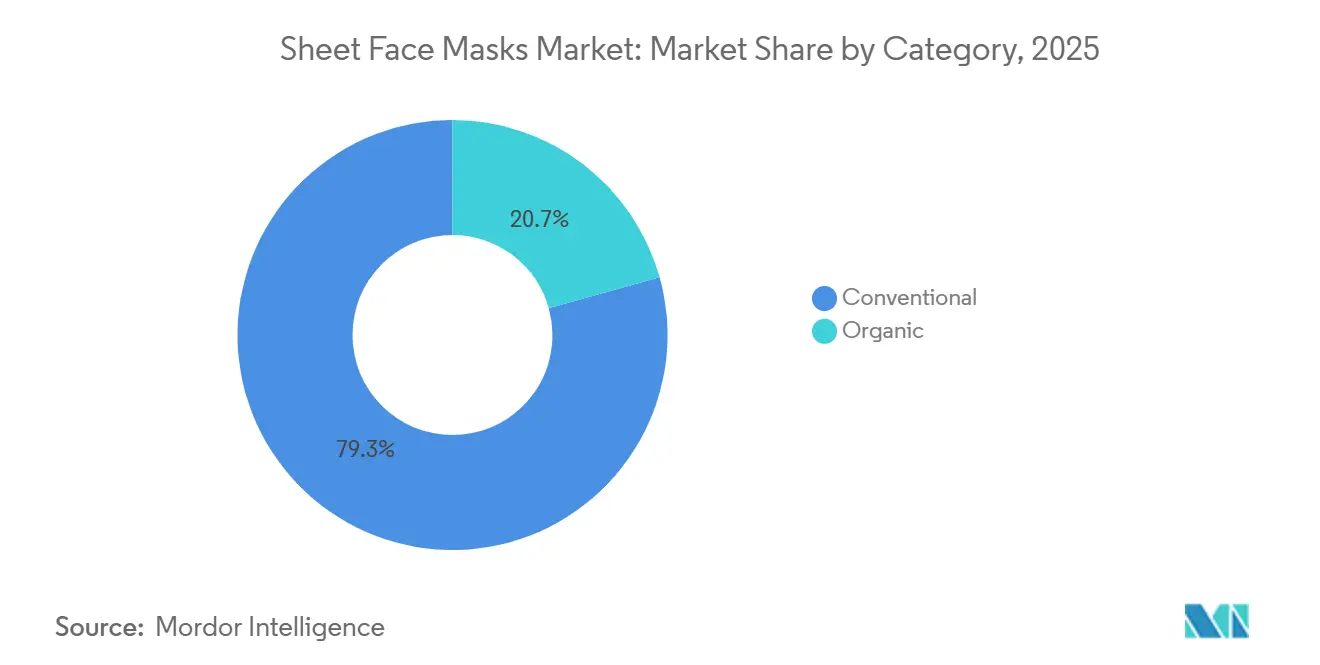

- By category, conventional products represented 79.32% of revenue in 2025, while organic products are forecast to grow at a 10.26% CAGR through 2031.

- By end-user, women held 82.66% of the sheet face masks market share in 2025, while men are projected to advance at a 9.57% CAGR through 2031.

- By distribution channel, beauty and health stores captured 57.83% of revenue in 2025, while online retail stores are projected to grow at an 8.79% CAGR through 2031.

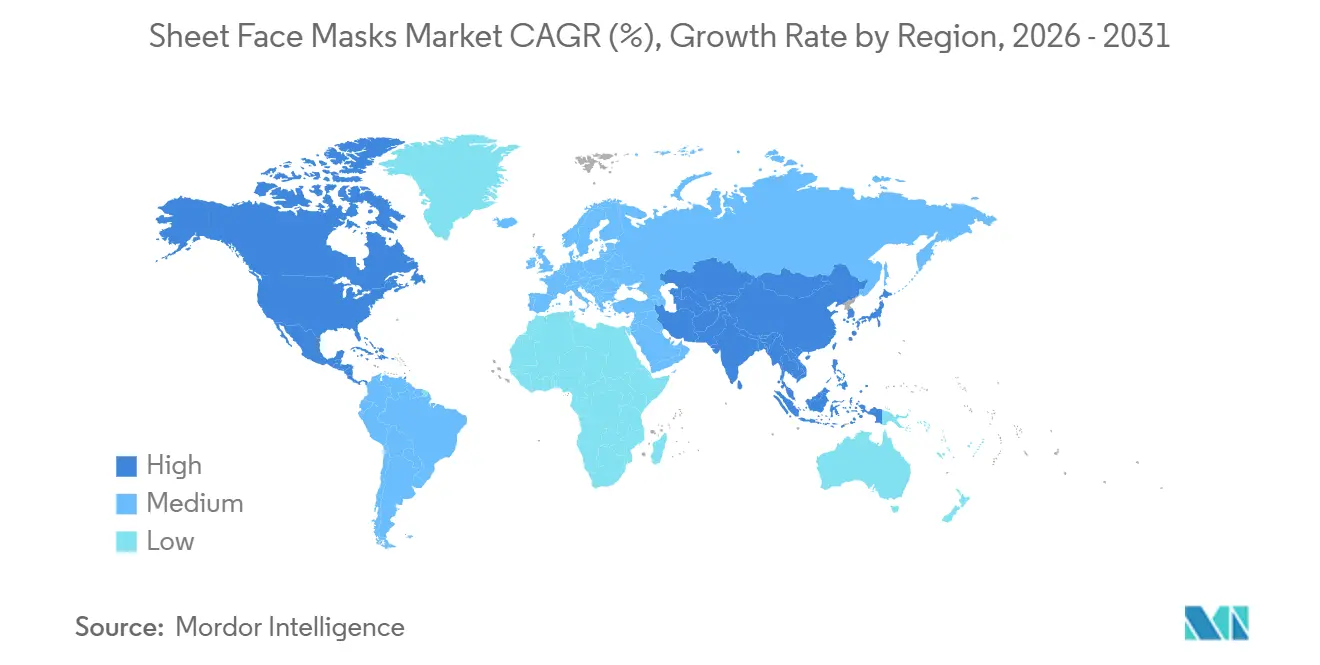

- By geography, Asia-Pacific held 46.57% of the sheet face masks market share in 2025, while the region is projected to expand at an 8.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sheet Face Masks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Influence of K-Beauty Skincare Trends | +2.1% | Global, with concentrated acceleration in North America and Europe | Short term (≤ 2 years) |

| Expansion of E-Commerce Beauty Product Sales | +1.5% | Global, led by China, North America, and Southeast Asia | Short term (≤ 2 years) |

| Growing Adoption of Vegan and Cruelty-Free Skincare | +1.2% | North America and Europe | Medium term (2-4 years) |

| Product Innovations with Multifunctional Skincare Benefits | +0.9% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of Men's Skincare and Grooming Routines | +0.8% | Asia-Pacific core, with spillover to North America and Europe | Medium term (2-4 years) |

| Celebrity and Influencer Driven Product Promotion | +0.7% | Global, with highest impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Influence of K-Beauty Skincare Trends

The sheet face masks market is closely tied to the international spread of South Korean skincare culture, because product education, format familiarity, and ingredient trust tend to move together once Korean brands gain shelf presence in a new country. Korean sheet face mask exports rose in the first quarter of 2026, and the United States moved ahead of China as the largest destination, which signals a broader westward shift in where premium demand is building. This matters for the sheet face masks market because Western buyers often compare premium masks with higher-priced skincare treatments rather than low-cost daily-use items, and that comparison supports higher average selling prices for brands with clinical or ingredient-led positioning. The momentum also appears durable rather than short-lived, because annual Korean sheet face mask exports were reported to be on pace for a record year in 2026, which suggests the current K-Beauty cycle is being reinforced by broader distribution and repeat purchase behavior.

Expansion of E-Commerce Beauty Product Sales

The sheet face masks market is seeing a structural benefit from online selling because the format is easy to explain, easy to sample in small basket sizes, and easy to replenish through repeat digital orders. Online retail stores are the fastest-growing distribution channel in the sheet face masks market, with an 8.8% CAGR projected through 2031, which shows that channel expansion is not a side trend but a central part of category growth. Social commerce is changing how buyers enter the category, because short videos, influencer demonstrations, and skin concern-based recommendations can move a shopper from curiosity to purchase within minutes. This matters most for smaller Korean and Japanese brands, since digital channels reduce their dependence on traditional retail gatekeepers and let them scale through content rather than through a long physical rollout. The same pattern is also shifting marketing budgets inside the sheet face masks market, as brands now place more importance on product storytelling, review velocity, and creator partnerships than on broad-based shelf promotions. As online assortments deepen, the brands that combine credible efficacy claims with clear visuals, accessible pack sizes, and steady content output are likely to capture repeat sales faster than brands that rely only on store visibility.

Growing Adoption of Vegan and Cruelty-Free Skincare

The sheet face masks market is also moving toward cleaner and more ethically positioned products, and that shift is shaping both product development and premium pricing. Demand for vegan and cruelty-free claims is increasingly linked with material choice, so brands are using bio-cellulose, bamboo fiber, and cotton-based substrates to align ethical messaging with visible product quality. This change is also affecting serum formulation, because brands are looking for alternatives to ingredients that were once tied to animal sourcing and are replacing them with plant-derived or biotechnology-based versions where possible. Mediheal’s Rose PDRN Essential Sheet Mask, launched nationwide across more than 1,400 Ulta Beauty stores in February 2026, is a good example because it paired vegan PDRN from rose with a clinical efficacy message rather than treating vegan claims as a separate niche. This supports the faster rise of organic products in the sheet face masks market, since buyers are rewarding products that combine better ingredient transparency with performance claims they can understand at the shelf.

Expansion of Men’s Skincare and Grooming Routines

The sheet face masks market is widening beyond its traditional female base, and the clearest sign of that shift is the stronger growth outlook for male end users. Men are projected to be the fastest-growing end-user group in the sheet face masks market, with a 9.6% CAGR through 2031, which is well above the overall category rate. This growth is being shaped first by South Korea and Japan, where multi-step grooming routines are already normalized, and then by urban consumers in India, North America, and Southeast Asia who are becoming more comfortable with targeted skincare. Demand from men is centered on practical concerns such as hydration, oil control, post-shave recovery, and visible anti-aging support, which makes the format easier to position as a treatment step instead of a cosmetic indulgence. That distinction matters because it reduces stigma around use and allows gender-neutral or minimalist branding to perform better than overly decorative packaging. The brands that adapt quickly to this broader demand pool are likely to gain a durable advantage in the sheet face masks market, while brands that remain narrowly focused on the historical female core may miss the category’s fastest-moving consumer cohort.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit Apparel Products Reducing Consumer Trust | -0.6% | Global, peak impact in North America and Europe | Short term (≤ 2 years) |

| Size And Fit Uncertainties In Online Purchases | -0.5% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Data Privacy And Cybersecurity Concerns Among Shoppers | -0.4% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Growing Concerns Over Sustainability And Packaging Waste | -0.3% | Europe, North America, and consumer-driven parts of Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Affecting Consumer Trust Levels

The sheet face masks market faces a direct trust problem from counterfeit goods, especially because these products are widely sold online and are often purchased by consumers who cannot verify authenticity before use. Marqvision identified more than 1.1 million suspected counterfeit K-Beauty listings across 1,500 platforms in 80 countries during 2024, which shows how wide the exposure has become for legitimate brands[1]Source: Information Technology & Innovation Foundation, "Protecting Authenticity in the Global K-Beauty Market", itif.org. The same review noted that Korean beauty firms lost USD 362 million in revenue to counterfeit consumer goods between January and May 2025, which means the problem is affecting both brand equity and realized sales. The damage goes beyond price pressure, because counterfeit masks may contain undisclosed ingredients or weak formulations, and poor user experiences can easily be blamed on the original brand rather than on the fraudulent seller. This risk is especially serious for premium and clinical-positioned products in the sheet face masks market, since their value depends on trust, repeat use, and ingredient credibility. As online expansion continues, brands will need stronger traceability, seller control, and consumer education if they want growth in digital channels without a parallel loss in confidence.

Environmental Concerns Over Single-use Sheet Waste

The sheet face masks market also faces pressure from the single-use nature of the format, because most conventional masks combine synthetic sheets with multilayer packaging that is difficult to recycle through standard municipal systems. That concern is becoming more important in Europe and North America, where retailers and consumers are paying closer attention to packaging materials, waste intensity, and the broader environmental cost of frequently used items. Suppliers are responding with product and packaging changes rather than by stepping away from the category entirely, which suggests the issue is reshaping competition instead of removing demand. This creates a split inside the sheet face masks market, where brands that invest in better substrates and more recyclable formats can use sustainability as a premium lever, while low-cost brands that do not adapt face a higher risk of listing pressure. The issue is unlikely to reverse category growth on its own, but it will make innovation quality and packaging execution more important to long-term brand survival.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clinical Specialization Anchors Value While Hydration Drives Volume Entry

Specialized sheet face masks held 58.04% of product type revenue in 2025, which made them the largest product group in the sheet face masks market and reflected strong demand for targeted skin treatment rather than occasional use. Buyers are increasingly treating these masks as a delivery format for specific concerns such as anti-aging, acne care, soothing, and barrier support, which has raised the importance of actives and visible product claims. This has helped specialized formats capture higher value, since consumers often accept a higher per-use price when the mask is positioned as part of a focused routine instead of a casual beauty add-on. The segment also benefits from the migration of ingredients once associated with clinic-led or premium topical care into more accessible sheet formats, which makes the category easier to trade up within. As a result, the sheet face masks market is moving away from a narrow pampering image and toward a more treatment-oriented product logic.

Hydrating sheet face masks are projected to grow at an 8.41% CAGR through 2031, and the sheet face masks market size for hydrating formats is expanding because these products remain the easiest entry point for new users. Hydration is the most straightforward benefit to communicate, which helps brands reach younger shoppers, male users, and first-time K-Beauty buyers with less education than a specialized treatment product would require. The growth outlook also reflects how the line between hydration and clinical benefit is becoming less rigid, because brands now build moisture focused products around stronger actives and more premium textures. Innisfree’s Green Tea PDRN Exosome Gel Mask, introduced in 2026 with a claim of improving skin moisture by 108% after a single use, illustrates how a hydration product can also support a higher efficacy image. That overlap should keep hydrating products important for volume growth in the sheet face masks market, even as specialized products continue to anchor the higher-value end of the assortment.

By Price: Mass Volume Meets Premium Trade-up Dynamics

Mass-priced products accounted for 68.32% of revenue in 2025, which shows that affordability still gives the sheet face masks market its broadest base of regular use. These products perform well in convenience stores, supermarkets, hypermarkets, and value-oriented online channels, where basket size is smaller but repurchase is more frequent. Mass demand is also supported by the fact that sheet face masks remain one of the easiest beauty items to buy on impulse, since the ticket size is small and the use case is widely understood. In many countries, that combination of low-friction purchase and visible self-care value keeps the mass tier central to the category’s scale. The mass tier, therefore, remains essential to the sheet face masks market, even though competitive intensity is higher and product differentiation is often weaker in this part of the assortment.

Premium products are projected to grow at a 9.13% CAGR through 2031, and the sheet face masks market size for the premium tier is being lifted by ingredient-led positioning and stronger clinical language. Western buyers often compare premium masks with higher-priced serums or treatment products, which makes a single-use premium mask feel more acceptable than it would in markets where the category is still seen as purely promotional. This trade-up pattern is also being reinforced by clinical actives, hydrogel formats, bio-cellulose materials, and tighter targeting around concerns such as elasticity, tone, and recovery. At the same time, some brands continue to defend the mass middle with structured derma positioning, as seen in Tony Moly’s 2024 launch of the Dermatician brand for E-Mart. These opposite strategies show that the sheet face masks market is stretching at both ends, with stronger premium momentum and continued mass importance rather than convergence around a single middle price point.

By Category: Organic Growth Outpaces Conventional Despite Lower Current Share

Conventional sheet face masks represented 79.32% of category revenue in 2025, which left them firmly in the lead within the sheet face masks market because they benefit from lower costs, established formulation systems, and the broadest shelf coverage. Their strength also reflects manufacturing familiarity, since most established producers can scale conventional materials and formulas more easily than certified organic alternatives. In high-volume channels, this gives conventional products a practical advantage because price points stay accessible while assortment breadth remains wide. Conventional products are therefore likely to keep leading absolute sales for the foreseeable period, especially in markets where entry price matters more than certification language. This scale advantage continues to give the sheet face masks market its largest pool of everyday purchases and first-time trials.

Organic products are projected to grow at a 10.26% CAGR through 2031, and the sheet face masks market size for this category is rising faster because buyers increasingly want cleaner sourcing, more transparent labeling, and materials that feel less wasteful. Growth is not limited to Western natural beauty niches, since South Korean brands are also developing certified or nature-forward versions to meet the expectations of import markets with tighter claim scrutiny. In practice, organic positioning in the sheet face masks market covers both the sheet substrate and the serum, which means credibility depends on how well the product’s material and ingredient story fit the certification standards of each target country. Brands that do not align claims with local frameworks risk consumer skepticism and retail pushback, especially where ingredient transparency is becoming more central to category curation. That makes the organic segment smaller today, but more strategically important for future premium growth and brand trust.

By End-user: Women Drive Scale, Men Define the Growth Trajectory

Women accounted for 82.66% of end-user revenue in 2025, which kept them as the core demand base for the sheet face masks market across Asia-Pacific and Europe. This position reflects long-established skincare routines in which sheet face masks already fit naturally as a regular or occasional treatment step. Women also remain the group most familiar with the format, the claims language, and the broader K-Beauty ritual that has supported category development for many years. Because of that, most existing assortment depth, promotional timing, and retail education in the sheet face masks market still speak most directly to female buyers. This foundation gives the category a stable scale, even as the growth story gradually broadens into new user groups.

Men are projected to grow at a 9.57% CAGR through 2031, which makes them the fastest-moving end-user group in the sheet face masks market and an increasingly important source of incremental demand. Male uptake is being supported by grooming normalization in South Korea, stronger social acceptance in urban markets, and content platforms that present skincare in a practical and results-focused way. Products tied to oil control, anti-aging, post-shave care, and fast hydration are especially well placed, because they solve visible concerns without asking buyers to adopt highly decorative beauty routines. In Western markets, the channel mix also matters, since male shoppers are still more likely to buy through pharmacy, grocery, or broad online platforms than through specialty beauty stores alone. The brands gaining fastest traction in this part of the sheet face masks market are often those using minimalist packaging and gender-neutral language, because that lowers barriers without forcing a separate male-only brand identity.

By Distribution Channel: Physical Retail Holds Share, Digital Channels Set Trajectory

Beauty and health stores captured 57.83% of distribution revenue in 2025, which kept them as the largest route to market in the sheet face masks market because they support product education, sampling, and assisted selling. For a format where fit, texture, and perceived skin compatibility matter, physical retail still plays an important role in helping shoppers try a new product with less uncertainty. These stores also help premium and treatment-led products communicate value more clearly, because trained staff and in-store displays can connect a mask to a broader regimen. Supermarkets and hypermarkets continue to matter for everyday and mass-priced purchases, while pharmacy, duty-free, and other channels serve narrower needs. Physical retail, therefore, remains central to the sheet face masks market, even as growth is shifting toward digital platforms.

Online retail stores are projected to grow at an 8.79% CAGR through 2031, and this makes them the most important growth channel in the sheet face masks market over the forecast period. The online advantage is not only about convenience, because digital channels also support broader assortments, faster product launches, bundled subscriptions, and direct feedback through ratings and reviews. This model particularly benefits brands that move quickly on content and packaging, since strong visuals and short education cycles are often enough to drive a first purchase. It also helps newer entrants compete with larger companies, because a product can gain national visibility through creator content or platform promotions before it wins major shelf space. As a result, the sheet face masks market is likely to see a more blended channel structure, with stores still leading absolute sales while online platforms shape trial speed and brand momentum.

Geography Analysis

Asia-Pacific accounted for 46.57% of revenue in 2025, and the sheet face masks market size in the region is projected to expand at an 8.79% CAGR through 2031, which keeps it as both the largest and the fastest-growing regional block. South Korea and Japan remain the category’s main innovation centers, since they continue to shape ingredient language, format upgrades, and consumer expectations that later spread into other regions. China still matters greatly for volume, but the local demand pattern is becoming more selective as buyers move away from bulk low-cost purchases toward more premium and clinically positioned products. This change was visible when the top 10 Tmall sheet face mask brands saw sales volume fall from around 500,000 units in April 2025 to around 360,000 units in April 2026. At the same time, Korean sheet face mask exports to China rose 94.3% year over year in April 2026, which suggests that premium cross-border brands are still capturing value even as lower-end local volume softens.

North America is one of the most important expansion zones for the sheet face masks market, because premium retail partnerships and wider consumer familiarity with Korean skincare are lowering entry barriers for imported brands. Europe is following a similar path, with Korean cosmetics exports to the region rising 60% year over year through April 2026 to USD 820 million, which shows how quickly the category is scaling beyond its original base [2]Source: Younhap News Agency, "K-beauty's 2nd boom: How indie brands, manufacturing powerhouses are rewriting the industry", en.yna.co.kr. The Netherlands has become a meaningful logistics node for this growth, ranking first among European destinations for Korean sheet face mask exports in April 2026 at USD 16.3 million. These two regions are especially important for the sheet face masks market because they reward premium positioning, support broader omnichannel distribution, and are placing greater emphasis on ingredient transparency and packaging quality. That mix makes North America and Europe attractive not only for sales growth, but also for margin expansion and brand building.

South America and the Middle East and Africa remain smaller in total size, but they offer meaningful white space for the sheet face masks market as import access, online beauty shopping, and premium self-care habits continue to widen. Brazil leads South American demand because of its large beauty engaged consumer base, while Argentina, Colombia, Chile, and Peru are adding incremental opportunities through urban middle-income spending and better product availability. In the Middle East and Africa, the strongest immediate value pools are in the United Arab Emirates and Saudi Arabia, where premium retail infrastructure and strong beauty spending make premium imported brands easier to place. Africa is still a longer-cycle opportunity, but better anti-counterfeit systems and formal retail development could improve the environment for the sheet face masks market over time.

Competitive Landscape

The sheet face masks market has a moderately concentrated structure, where Korean and Japanese companies still shape much of the technical agenda, while Western multinationals provide global scale, broader distribution, and stronger portfolio diversification. Companies such as Amorepacific, Shiseido, Mediheal, and Kao remain important because they are closely tied to the routines, materials, and ingredient stories that built the category in the first place. Global beauty groups such as L'Oréal, Estée Lauder, and Unilever remain relevant because they can absorb new formats into wider skincare portfolios and place them across more countries and channels. The result is a market where no single competitive model dominates, since innovation leadership and distribution leadership are often held by different players. That balance keeps the sheet face masks market open enough for new entrants, but it also raises the execution bar for smaller brands that want to move from viral visibility to stable repeat demand.

A major pattern in 2025 and 2026 has been selective retail expansion by Asian brands, especially in North America, where partnerships with Sephora, Ulta Beauty, and OLIVE YOUNG create visibility without forcing immediate competition with every mass channel at once. Mediheal expanded its U.S. retail presence in June 2026 through OLIVE YOUNG’s first U.S. store in Pasadena, which reinforced the brand’s effort to grow both in-store and online access while keeping a premium K-Beauty context around the brand. Amorepacific also pushed further into North America, and IOPE’s March 2026 Sephora debut reflected a deliberate move to frame Korean skincare around clinical grade positioning rather than novelty. L'Oréal completed the acquisition of Kering Beauté in March 2026, which showed that large groups still prefer to deepen premium beauty capabilities through acquisition when they see room for stronger prestige positioning. These moves suggest that the sheet face masks market is being shaped by access strategy, brand framing, and portfolio quality as much as by product count alone.

Competitive differentiation is also moving further upstream into materials, packaging, and technology, which makes the supply chain more important to long-term brand positioning in the sheet face masks market. Kolmar Korea’s recyclable paper pouch development is one example, because a supplier-led packaging improvement can help many customer brands close the sustainability gap without redesigning the full product concept. At the same time, personalization tools and device linked skincare concepts are pushing brands to think beyond a standalone sheet format and toward a wider care system. That means the next phase of the sheet face masks market is likely to reward companies that connect product efficacy, digital engagement, and packaging credibility in a single proposition rather than relying on shelf presence alone.

Sheet Face Masks Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies Inc.

-

Unilever PLC

-

Shiseido Company, Limited

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Mediheal expanded its US retail presence through a partnership with OLIVE YOUNG at its first-ever US store in Pasadena, Los Angeles, offering both in-store and online distribution; the launch introduced several of Mediheal's newest product innovations including upgraded toner pad collections and new sun care formats.

- June 2026: Rael launched two science-backed K-Beauty hydrogel masks, the Cryo Soothing Hydrogel Mask and the Glutathione + Vitamin C Brightening Hydrogel Mask, exclusively at Ulta Beauty and on its direct-to-consumer site, bringing cutting-edge South Korean sheet face mask ingredient technology to US mainstream retail at accessible price points of USD 4.99 per single mask.

- March 2026: L'Oréal completed its acquisition of Kering Beauté, which includes the House of Creed and 50-year exclusive licences for Bottega Veneta and Balenciaga beauty and fragrance, strengthening L'Oréal's luxury division and signaling the conglomerate's commitment to premium beauty investment.

Global Sheet Face Masks Market Report Scope

It includes the production, sale, and distribution of these masks designed to deliver concentrated, targeted ingredients to the skin for hydration, anti-aging, acne control, and brightening. The Sheet Face Masks Market Report is Segmented by Product Type (Specialized Sheet Masks, Hydrating Sheet Masks), Price (Premium, Mass), Category (Organic, Conventional), End-User (Men, Women), Distribution Channel (Supermarkets/Hypermarkets, Online Retail Stores, and Other Distribution Channels), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Specialized Sheet Masks |

| Hydrating Sheet Masks |

| Premium |

| Mass |

| Organic |

| Conventional |

| Men |

| Women |

| Beauty and Health Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Specialized Sheet Masks | |

| Hydrating Sheet Masks | ||

| Price | Premium | |

| Mass | ||

| Category | Organic | |

| Conventional | ||

| End-User | Men | |

| Women | ||

| Distribution Channel | Beauty and Health Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retail Stores | ||

| Other Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for sheet face masks?

The sheet face masks market is projected to reach USD 3.3 billion by 2031 from USD 2.1 billion in 2025, with an 8% CAGR from 2026 to 2031.

Which region is leading demand and growth for sheet face masks?

Asia-Pacific led with 46.6% of 2025 revenue and is also the fastest growing region, with an 8.5% CAGR projected through 2031.

Which product type is growing fastest in sheet face masks?

Hydrating sheet face masks are projected to grow at an 8.4% CAGR, while specialized products still held the largest 2025 revenue share at 58%.

Why are premium sheet face masks gaining traction?

Premium products are growing at a 9.1% CAGR because buyers are responding to stronger ingredient stories, clinical positioning, and better format differentiation, especially in Western retail channels.

Page last updated on: