Lip and Face Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.54 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

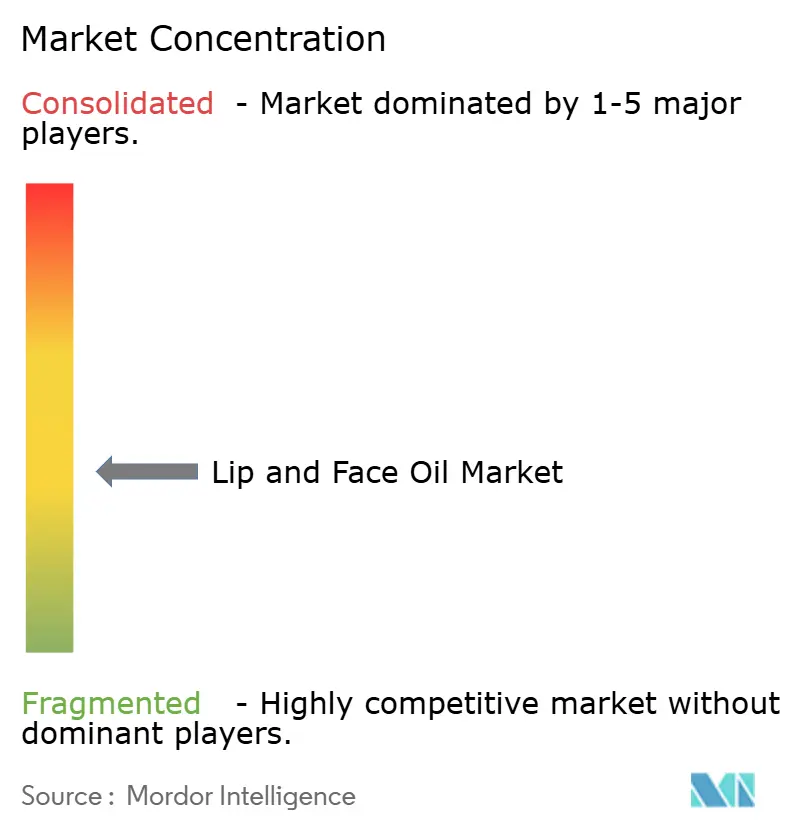

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lip and Face Oil Market Analysis by Mordor Intelligence

The global lip and face oil market was valued at USD 6.32 billion in 2025 and is estimated to grow from USD 6.54 billion in 2026 to USD 8.09 billion by 2031, registering a CAGR of 4.35% during 2026–2031. Market growth is driven by increasing consumer preference for skincare solutions focused on hydration, nourishment, and overall skin maintenance. The rising shift toward ingredient-conscious beauty has encouraged the adoption of oil-based formulations containing botanical extracts, essential fatty acids, and skin-supporting ingredients. Growing awareness regarding skin barrier protection and the role of oils in maintaining a healthy-looking complexion continues to strengthen demand globally.

Key Report Takeaways

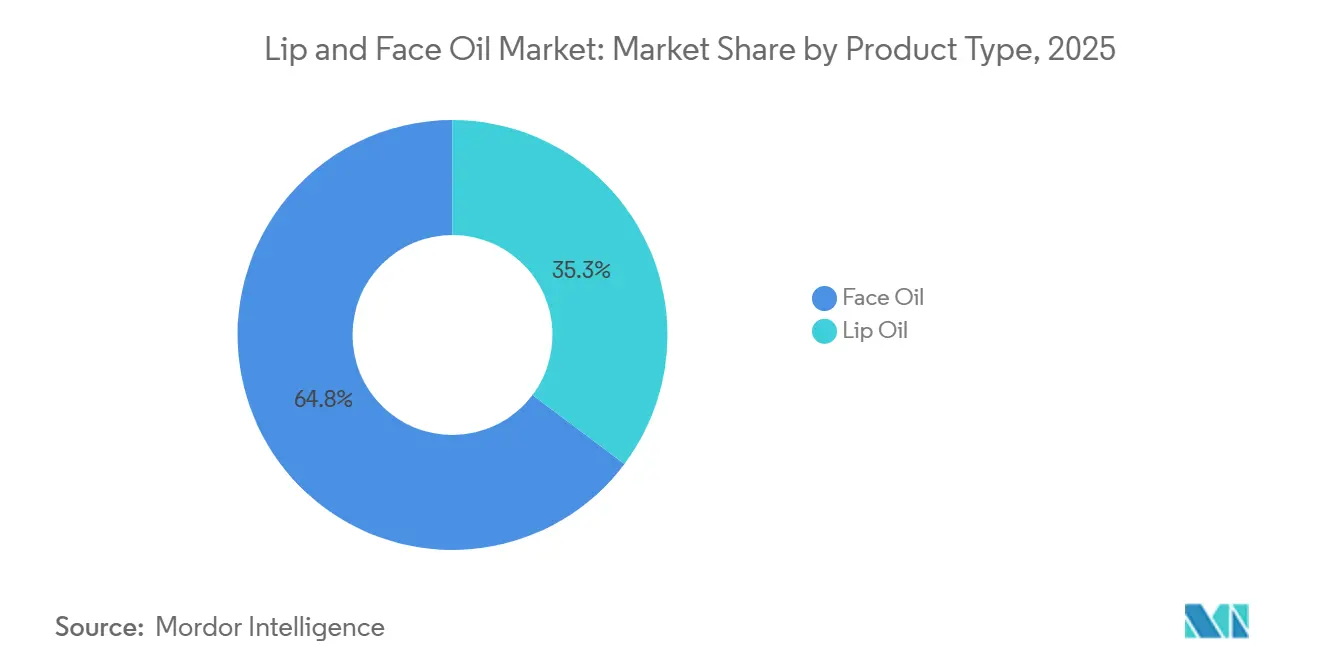

- By product type, face oil held 64.75% of the lip and face oil market share in 2025, while lip oil is forecast to grow at a 5.07% CAGR through 2031.

- By oil type, jojoba oil accounted for 32.45% of the lip and face oil market size in 2025, while squalane is projected to expand at a 5.69% CAGR through 2031.

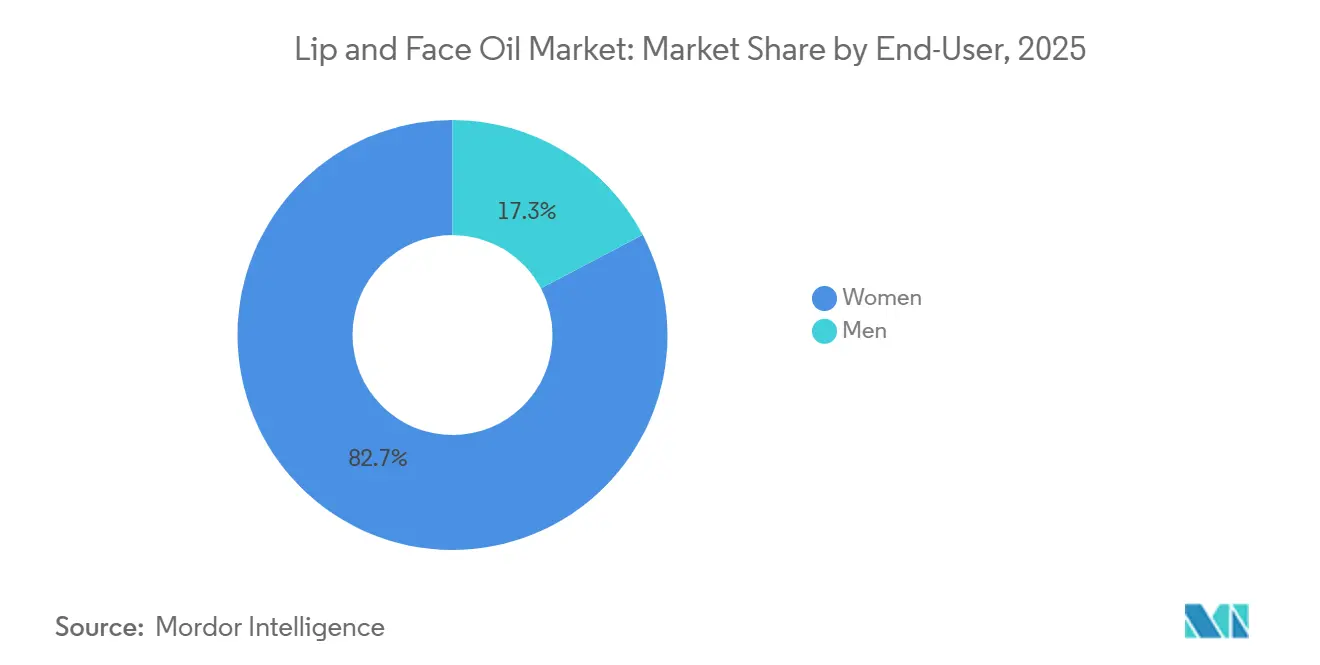

- By end-user, women represented 82.73% share in 2025, while men recorded the highest projected CAGR at 5.81% through 2031.

- By distribution channel, specialty stores held 39.63% share in 2025, while online retail stores are advancing at a 6.23 CAGR through 2031.

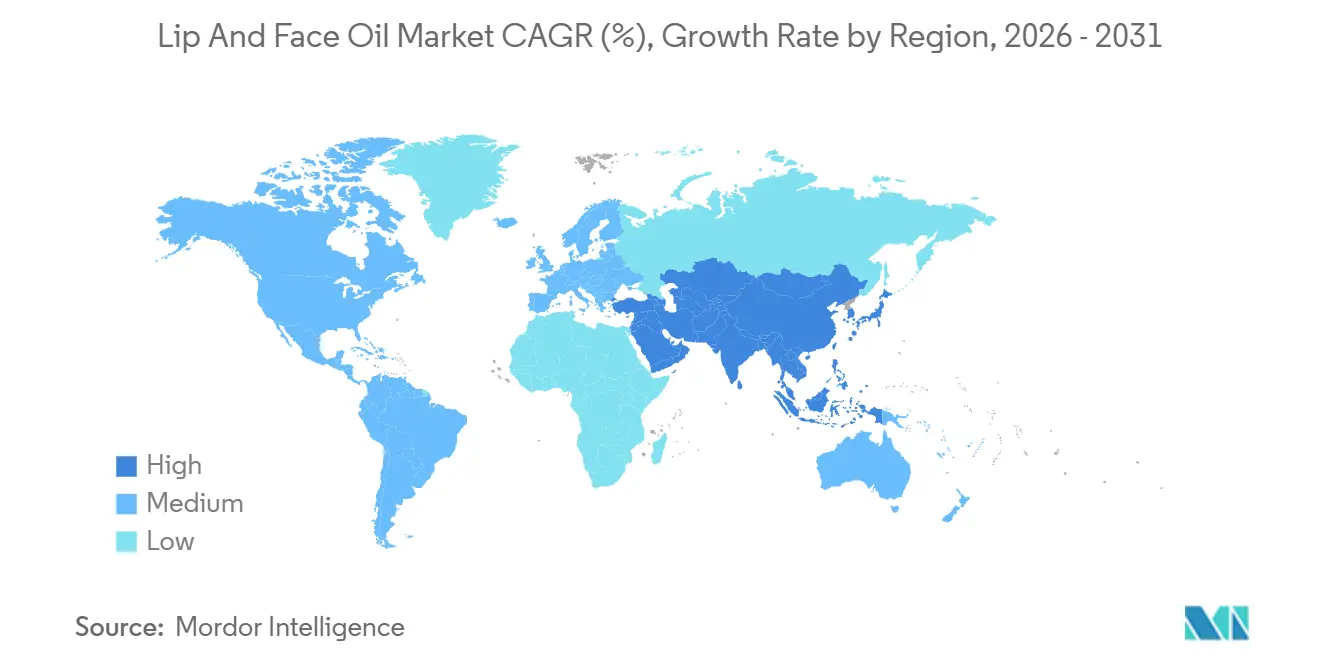

- By geography, North America held 33.25% of the lip and face oil market share in 2025, while Asia-Pacific is forecast to expand at a 5.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lip and Face Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for natural and plant-based beauty products | +0.8% | Global, concentrated in North America, Europe, and Asia-Pacific | Medium term (2–4 years) |

| Demand for anti-aging and preventive skincare solutions | +0.7% | North America, Europe, Asia-Pacific (Japan, South Korea) | Long term (≥ 4 years) |

| Rising adoption of premium and luxury skincare products | +0.6% | North America, Europe, China, Middle East | Medium term (2–4 years) |

| Influence of social media and beauty content creators | +0.7% | Global, strongest in North America, South Korea, Southeast Asia | Short term (≤ 2 years) |

| Popularity of clean beauty and chemical-free formulations | +0.5% | North America, Western Europe | Medium term (2–4 years) |

| Expansion of multi-functional skincare products | +0.6% | Global, fastest adoption in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Consumer preference for natural and plant-based beauty products

The increasing consumer preference for natural and plant-based beauty products is driving growth in the global lip and face oil market. Individuals are seeking formulations made with botanical ingredients and minimal synthetic additives. This trend toward ingredient-conscious beauty has heightened demand for oils derived from natural sources that offer nourishment, hydration, and skin-conditioning benefits, while meeting clean beauty standards. Consumers are prioritizing products with transparent ingredient lists, cruelty-free claims, and formulations free from harsh chemicals, prompting brands to develop plant-based lip and facial oils. For example, La Mior provides lip oil products with a vegan composition that are paraben-free and sulfate-free, catering to the rising demand for cleaner, naturally positioned beauty solutions. The increasing adoption of nature-inspired formulations continues to drive innovation and expansion within the lip and face oil market.

Demand for anti-aging and preventive skincare solutions

The demand for anti-aging and preventive skincare solutions is increasing as consumers prioritize maintaining skin health, improving firmness, and reducing visible signs of aging through targeted beauty formulations. Face oils containing antioxidants, vitamins, essential fatty acids, and skin-conditioning ingredients are becoming more popular due to their ability to enhance elasticity, improve moisture retention, and promote overall skin appearance. Additionally, the growing aging population is driving demand for products tailored to mature skincare needs. For example, according to the World Bank, Monaco had the highest proportion of people aged 65 years and above in 2024, accounting for 36% of its population, followed by Japan at approximately 30% [1]Source: World Bank, "Countries with the highest share of people aged 65 years", worldbank.org . This expanding older demographic is fostering the development and adoption of nourishing lip and facial oil products aimed at long-term skincare maintenance.

Rising adoption of premium and luxury skincare products

The increasing demand for premium and luxury skincare products is driving growth in the global lip and face oil market. Consumers are prioritizing high-performance formulations, superior textures, and exclusive ingredient profiles in their beauty routines. Luxury oils are gaining popularity due to their emphasis on advanced extraction methods, premium botanical ingredients, and enhanced user experience through lightweight textures, appealing fragrances, and attractive packaging. In response, brands are launching sophisticated oil-based products that combine skincare benefits with a luxury image. For example, Chanel offers Huile de Jasmin Revitalizing Facial Oil, which features jasmine extract and camellia-derived ingredients for nourishment and comfort. Similarly, Guerlain’s Abeille Royale Advanced Youth Watery Oil incorporates Ouessant black bee honey and royal jelly technology to address skin repair and visible signs of aging. These premium innovations are increasing the appeal of high-value lip and face oil products among consumers seeking luxury skincare solutions.

Influence of social media and beauty content creators

The global lip and face oil market is experiencing significant growth, driven by the increasing influence of social media and beauty content creators. Digital platforms have emerged as essential channels for introducing consumers to innovative skincare routines, highlighting product benefits, and promoting beauty trends. Influencers, dermatologists, and beauty creators are playing a pivotal role in boosting awareness of oil-based products by demonstrating application techniques, sharing detailed reviews, and showcasing visible results through engaging tutorials and short-form content. The rising popularity of trends such as glossy lips, glass skin, and skin nourishment routines has further encouraged consumers to experiment with lip and face oils. Platforms like TikTok, Instagram, and YouTube are proving instrumental in rapidly building product awareness, shaping consumer preferences, and driving the global adoption of these products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of skin irritation and allergic reactions | -0.4% | Global, heightened in Europe and North America (sensitive skin focus) | Medium term (2–4 years) |

| Concerns regarding clogged pores and acne breakouts | -0.3% | North America, Asia-Pacific (high humidity, oily skin prevalence) | Short term (≤ 2 years) |

| Competition from alternative skincare products | -0.5% | Global, strongest in Europe and North America | Medium term (2–4 years) |

| Concerns over synthetic additives and ingredient transparency | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Risk of skin irritation and allergic reactions

The risk of skin irritation and allergic reactions poses a challenge to the global lip and face oil market. Some consumers may experience sensitivity due to certain botanical extracts, essential oils, fragrances, and active ingredients commonly used in oil-based formulations. Given the high sensitivity of lip and facial areas, issues such as redness, clogged pores, itching, or irritation can deter consumers from trying new products, particularly those containing concentrated natural ingredients. Variations in individual skin tolerance necessitate that brands prioritize extensive safety testing, hypoallergenic formulations, and clear ingredient labeling, which adds complexity to product development. These concerns may reduce adoption among consumers with sensitive or reactive skin, impacting the overall acceptance of lip and face oil products.

Concerns regarding clogged pores and acne breakouts

Concerns about clogged pores and acne breakouts are limiting the growth of the global lip and face oil market. Many consumers are hesitant to use oil-based formulations on facial skin due to fears of excessive oil buildup and blemishes. Heavier oils or unsuitable formulations can contribute to the perception that face oils may exacerbate skin congestion, particularly for individuals with oily or acne-prone skin. Additionally, a lack of understanding regarding the differences between various oil types and their compatibility with specific skin needs further hinders adoption. To address these challenges, manufacturers need to focus on creating lightweight, non-comedogenic formulations to build consumer confidence and encourage wider use of lip and face oil products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lip Oil Gains Share as Skincare-Cosmetic Hybrids Mature

In 2025, Face Oil accounted for 64.75% of the global lip and face oil market, fueled by the growing integration of facial oils into daily skincare routines. This trend is attributed to their capacity to deliver deep nourishment, enhance skin smoothness, and provide long-lasting hydration. The segment has achieved significant consumer acceptance as innovative formulations have improved absorption, minimized greasy textures, and made face oils appropriate for a broader spectrum of skin types. Increased awareness of the importance of maintaining the skin's natural moisture barrier and enhancing overall skin appearance has further promoted their use.

Lip Oil is experiencing the fastest growth among product types, with a CAGR of 5.07% projected through 2031. This surge is fueled by a rising preference for products that offer both lip care benefits and an enhanced aesthetic. The segment is gaining popularity as consumers increasingly opt for lightweight alternatives that provide hydration, a smooth texture, and a glossy finish, all without the sticky sensation often found in traditional products. The growing desire for healthier-looking lips and the demand for comfortable, everyday formulations have further accelerated this trend. Innovations in tinted oils, nourishing ingredients, and long-lasting moisture technologies are enhancing product attractiveness, allowing lip oils to gain significant growth momentum in the global lip and face oil market.

By Oil Type: Jojoba Dominates, Squalane Reshaping Premium Formulations

Jojoba Oil leads with 32.45% of the global lip and face oil market share in 2025, driven by its close similarity to the skin’s natural sebum, which supports better absorption and makes it suitable for regular skincare routines. Its lightweight consistency, hydrating properties, and suitability for various skin types have made it a favored choice among consumers looking for gentle yet effective oil-based products. Additionally, the segment benefits from the oil's natural stability, extended shelf life, and its rich blend of vitamins, minerals, and fatty acids that contribute to improved skin softness and a healthy look. The rising demand for beauty solutions with minimal ingredients and naturally sourced components has further bolstered the incorporation of jojoba oil in lip and face care products, allowing it to maintain its dominant market position.

Squalane is the fastest-growing oil type, with a CAGR of 5.69% projected through 2031. This growth is driven by its increasing use as an emollient ingredient that meets modern consumer preferences for effective and comfortable skincare solutions. The segment benefits from squalane's formulation flexibility, as it is highly resistant to oxidation and enhances product texture, consistency, and performance. Its transparent, odorless, and lightweight properties make it a preferred choice in premium lip and facial oil formulations, where sensory appeal is critical. Furthermore, the transition from traditional oil ingredients to science-backed, bio-engineered alternatives, such as plant-derived squalane from sugarcane and olives, is boosting its adoption and contributing to the segment's expansion.

By End-User: Women Lead Demand, Male Grooming Opens New Frontiers

Women accounted for 82.73% of the market share in 2025, driven by their strong engagement with structured skincare and beauty routines. Facial nourishment and lip treatment products are frequently incorporated into daily self-care practices. This segment benefits from increased awareness of ingredient benefits, product experimentation, and a preference for specialized solutions targeting hydration, radiance, and overall skin maintenance. Additionally, the growing participation of women in professional environments has heightened attention toward personal grooming and beauty care. According to the United States Bureau of Labor Statistics, the number of employed women in the United States reached approximately 80.3 million in 2025, representing a significant consumer base actively engaging with personal care categories [2]Source: United States Bureau of Labor Statistics, "Civilian female labor force in the United States", bls.gov.

The men's end-user segment is the fastest-growing category, with a CAGR of 5.81% projected through 2031. This growth is driven by the evolution of male grooming habits from basic personal care to dedicated skincare routines. Increasing acceptance of skincare among men has encouraged the use of targeted products addressing concerns such as dryness, rough texture, and maintaining a well-groomed appearance. The segment is further supported by the rise of gender-neutral beauty trends and shifting perceptions around male self-care, leading to greater experimentation with oil-based formulations. The growing availability of products tailored to men’s preferences, including simple routines, lightweight textures, and functional benefits, continues to drive adoption and support the segment’s rapid growth in the global lip and face oil market.

By Distribution Channel: Specialty Stores Retain Share but Online Retail Accelerates

Specialty stores accounted for 39.63% of the global lip and face oil market channel share in 2025. This dominance is attributed to their ability to offer a curated beauty shopping experience, allowing consumers to explore a wide range of skincare-focused products and compare formulations before making a purchase. These stores provide personalized assistance, product demonstrations, and expert recommendations, enabling customers to select oils tailored to their preferences and skin needs. The availability of premium, niche, and ingredient-specific beauty products further enhances customer engagement within specialty retail formats. Additionally, in-store consultations, sampling opportunities, and immersive beauty experiences build trust, positioning specialty stores as a preferred channel for purchasing lip and face oil products.

Online retail stores are the fastest-growing distribution channel, with a CAGR of 6.23% projected through 2031. This growth is driven by the increasing shift toward digital beauty discovery and the convenience of accessing a broader range of lip and face oil products via e-commerce platforms. The segment benefits from detailed product information, ingredient transparency, customer reviews, and comparison tools, which help consumers make informed purchasing decisions. Digital channels also provide faster visibility for emerging beauty brands and offer access to niche formulations that may not be widely available in physical stores. Features such as virtual beauty tools, subscription models, personalized recommendations, and social commerce platforms further support the adoption of online retail in the global lip and face oil market.

Geography Analysis

North America is projected to account for 33.25% of the global lip and face oil market in 2025. This dominance is driven by the region's well-established beauty and personal care industry, where consumers increasingly prioritize advanced skincare routines and ingredient-focused formulations. The market benefits from strong acceptance of oil-based products that provide targeted benefits such as nourishment, skin comfort, and improved texture. Additionally, growing interest in clean-label beauty, dermatologist-inspired formulations, and premium personal care experiences has encouraged wider adoption of lip and face oils. The presence of advanced retail ecosystems, beauty-focused digital platforms, and evolving consumer preferences for high-performance skincare solutions further supports the region's leading position.

Asia-Pacific is the fastest-growing regional market, with a CAGR of 5.91% projected through 2031. This growth is driven by the rapid evolution of skincare habits and increasing adoption of beauty routines that emphasize prevention, maintenance, and ingredient efficacy. Consumer interest in lightweight textures, naturally derived ingredients, and multifunctional beauty formats aligns with changing skincare expectations, supporting market expansion. The rising influence of beauty trends, product experimentation, and a preference for innovative formulations have further accelerated demand for lip and facial oils, positioning Asia-Pacific as a key growth contributor during the forecast period.

Europe, South America, and the Middle East & Africa represent evolving markets influenced by regulatory standards, ingredient preferences, and changing beauty behaviors. Europe offers a differentiated landscape, supported by strict cosmetic safety and transparency requirements. For example, by July 31, 2026, Regulation (EU) 2023/1545 mandates individual labeling of fragrance allergens on cosmetic product packaging, requiring brands to declare an expanded list of fragrance allergens and improve ingredient visibility [3]Source: European Union, "Regulation (EU) 2023/1545", european-union.europa.eu .

South America is gaining traction due to growing interest in botanical and nature-derived beauty formulations. Meanwhile, the Middle East & Africa market is supported by increasing consumer preference for nourishing skincare products and expanding awareness of specialized lip and facial care routines.

Competitive Landscape

The global lip and face oil market is moderately fragmented, with established beauty companies and emerging specialized brands competing through product innovation, ingredient quality, and differentiated positioning. Prominent global players such as L'Oréal S.A., The Estée Lauder Companies Inc., Shiseido Company, Limited, Unilever PLC, and Beiersdorf AG leverage their competitive advantages through extensive formulation capabilities, multi-geography distribution networks, and the ability to integrate premium face oil launches into their broader skincare portfolios. These companies continue to enhance their market presence by expanding oil-based product ranges that cater to consumer preferences for improved textures and advanced ingredients.

Competition in the market is increasingly driven by advancements in formulation, clean beauty positioning, and growing consumer demand for transparency. Companies are focusing on developing high-performance oil blends, incorporating naturally derived ingredients, creating lightweight textures, and offering multifunctional formulations to differentiate their products. Additionally, brands are prioritizing sustainable sourcing, responsible ingredient procurement, and premium packaging to foster consumer trust and strengthen brand loyalty in a market that values ingredient-conscious beauty solutions.

Technology is becoming a critical factor in differentiating offerings within the lip and face oil market. Companies are exploring innovations such as blockchain-based ingredient traceability for supply chains involving jojoba and squalane to enhance transparency from raw material sourcing to finished products. Digital innovation, data-driven product development, and advanced testing technologies are enabling brands to improve formulation precision and adapt swiftly to evolving skincare trends. These technology-driven initiatives, combined with sustainability efforts and ongoing product innovation, are expected to intensify competition and influence market strategies during the forecast period.

Lip and Face Oil Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies Inc.

-

Shiseido Company, Limited

-

Unilever PLC

-

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Clarins launched the Cryo-Plumping Lip Oil and Balm. The Cryo-Plumping Oil features Cryo-Active Technology, which provides an instantly plumped appearance, a clear and glossy finish, and a cooling, mint sensation.

- April 2026: Bath & Body Works launched new pH Lip Oils, designed to provide customers with a customized tint. The lip oils are lightweight and nourishing, and are available in three shades, Acai Berry Jam, Pucker Punch, and Pink Pout, with flavor notes of caramelized sugar, strawberry nectar, and crème brûlée.

Global Lip and Face Oil Market Report Scope

Lip oils and face oils are liquid skincare treatments rich in botanical extracts and fatty acids designed to intensely hydrate, nourish, and protect the skin. The lip and face oil market is segmented by product type, oil type, end-user, distribution channel, and geography. Based on product type, the market is segmented into lip oil and face oil. Based on oil type, the market is segmented into jojoba oil, argan oil, rosehip oil, squalane, and others. Based on end-user, the market is segmented into men and women. Based on distribution channel, the market is segmented into supermarkets and hypermarkets, specialty stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Lip Oil |

| Face Oil |

| Jojoba Oil |

| Argan Oil |

| Rosehip Oil |

| Squalane |

| Others |

| Men |

| Women |

| Supermarkets and Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Lip Oil | |

| Face Oil | ||

| By Oil Type | Jojoba Oil | |

| Argan Oil | ||

| Rosehip Oil | ||

| Squalane | ||

| Others | ||

| By End-User | Men | |

| Women | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 value forecast for lip and face oils?

The category is forecast to reach USD 8.09 billion by 2031, rising from USD 6.5 billion in 2026 at a 4.35% CAGR.

Which product type is larger, lip oil or face oil?

Face oil remained the larger product type, with 64.75% share in 2025, supported by its role in barrier care and routine-based skincare use.

Which ingredient category is growing the fastest?

Squalane is the fastest-growing oil type, with a projected 5.69% CAGR through 2031, helped by wider use of fermentation-based supply.

Why is online retail gaining ground so quickly?Online retail stores are projected to grow at 6.23% CAGR through 2031 because social commerce now combines discovery, content, and checkout in one path.

Online retail stores are projected to grow at 6.23% CAGR through 2031 because social commerce now combines discovery, content, and checkout in one path.

Page last updated on: