Face Wash Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

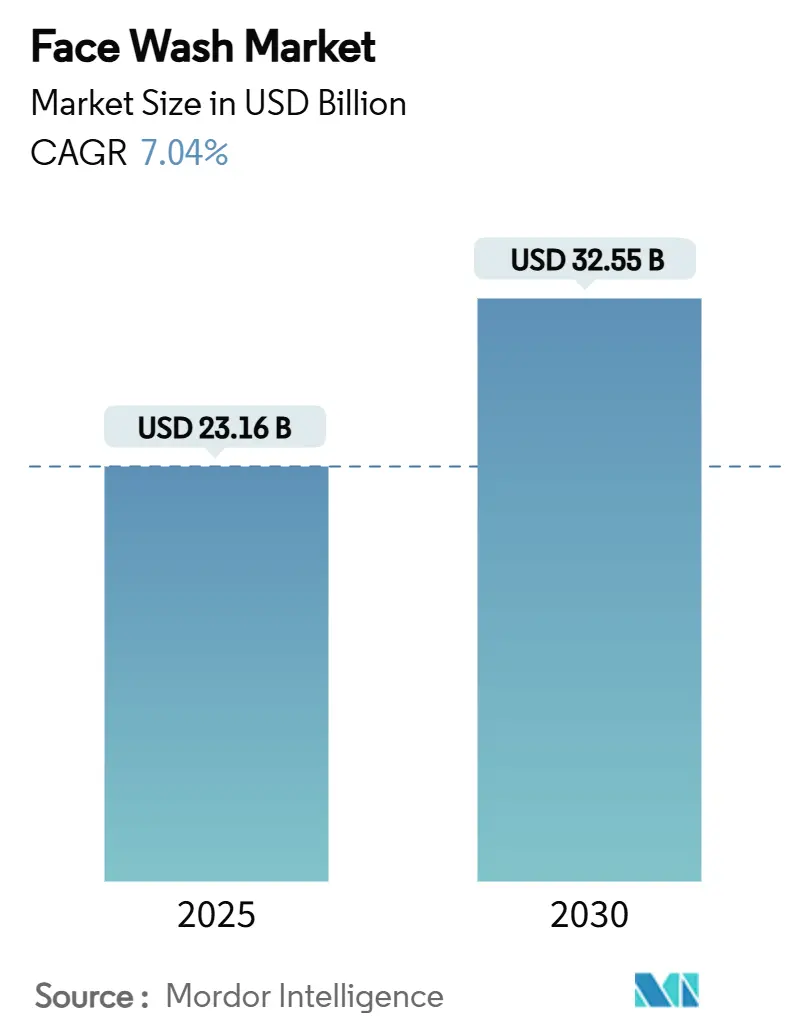

| Market Size (2025) | USD 23.16 Billion |

| Market Size (2030) | USD 32.55 Billion |

| Growth Rate (2025 - 2030) | 7.04% CAGR |

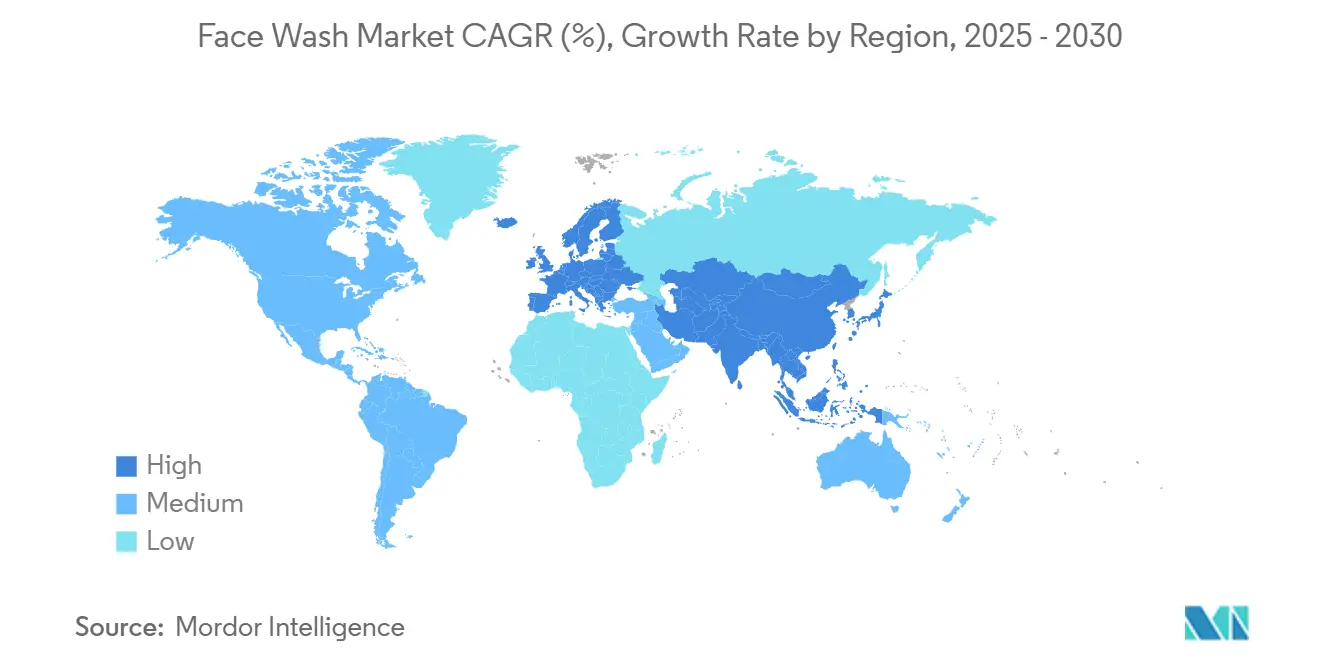

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Face Wash Market Analysis by Mordor Intelligence

The global face wash market size is valued at USD 23.16 billion in 2025 and is projected to reach USD 32.55 billion by 2030, growing at a CAGR of 7.04% during the forecast period. This market is evolving, influenced by changing consumer preferences, regulatory shifts, and innovative formulations. There's a noticeable shift from traditional, generic products to personalized solutions that emphasize efficacy. Today's consumers, prioritizing skin health, are gravitating towards face washes enriched with scientifically-backed ingredients like niacinamide, probiotics, and plant-based actives. This trend underscores a broader movement towards functional skincare. In Europe, tightening regulations are prompting brands to reformulate their products, pushing them towards cleaner and compliant alternatives. This shift not only highlights the importance of transparent ingredient sourcing but also carves out a niche for brands that prioritize it. Brands are leveraging technology to stand out, as seen with L’Oréal’s Cell BioPrint, which provides hyper-personalized skincare diagnostics. In response to rising concerns over ingredient safety and counterfeit products, the market is increasingly emphasizing premium, natural, and organic offerings that align with both performance and regulatory standards.

Key Report Takeaways

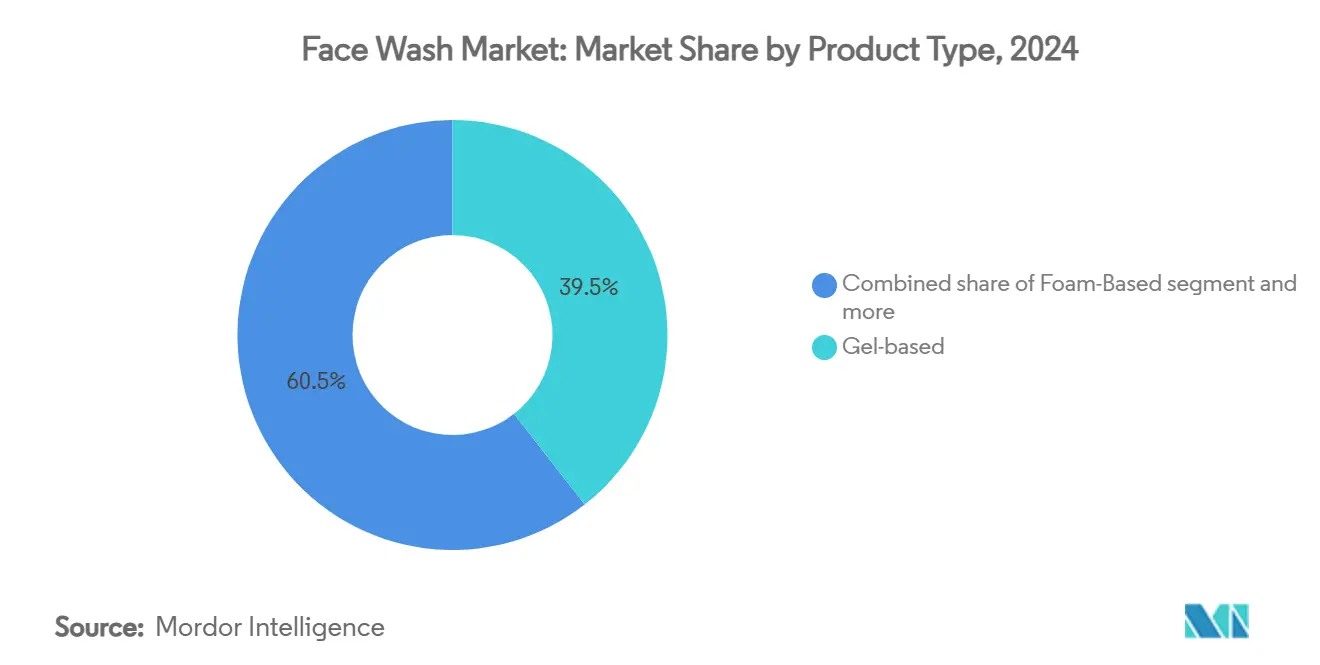

- By product type, gel-based cleansers held 39.45% of face wash market share in 2024, while foam products are projected to expand at a 7.49% CAGR to 2030.

- By skin type, normal skin products commanded 31.34% share of the face wash market size in 2024; sensitive-skin variants are advancing at a 9.72% CAGR through 2030.

- By end user, women’s formulations accounted for 62.25% of revenue in 2024, but men’s products are forecast to record the fastest 8.74% CAGR to 2030.

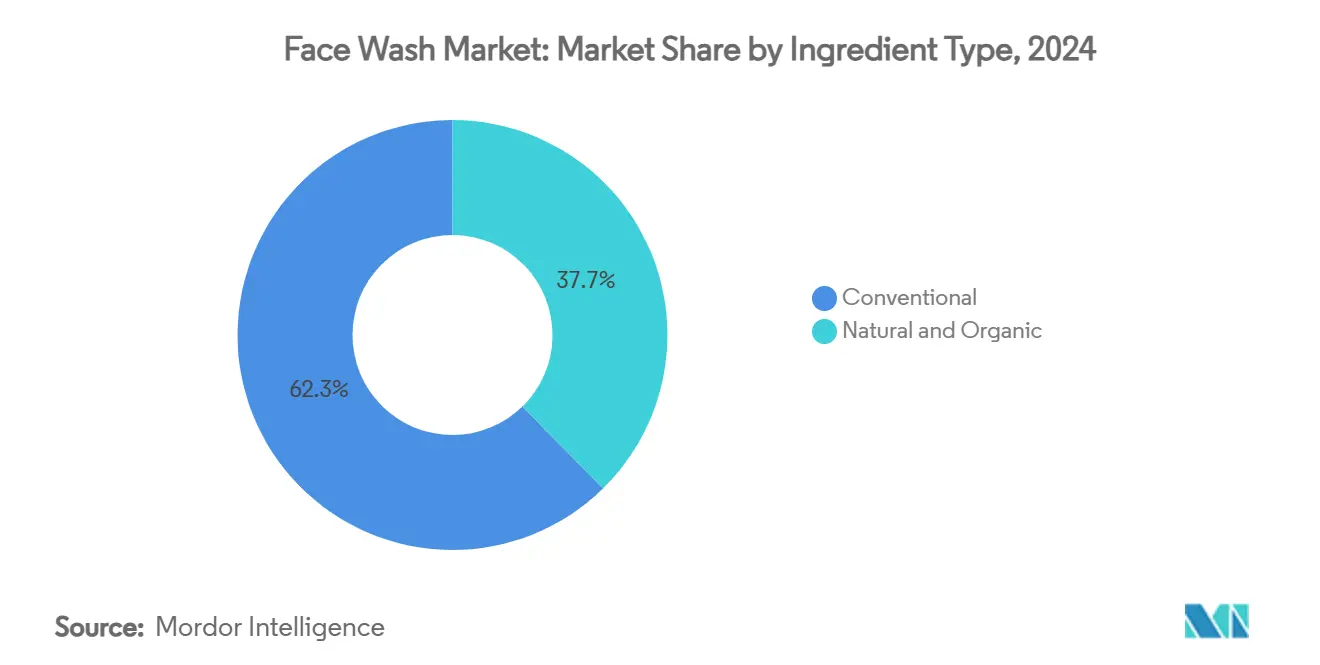

- By ingredient type, conventional formulations retained 62.34% share in 2024, whereas natural and organic offerings are set for an 8.22% CAGR in the face wash market.

- By distribution channel, online retail led with 28.79% share in 2024 and will also post the highest 9.55% CAGR over the forecast period.

- By price tier, mass-market lines held 66.61% share in 2024, yet premium cleansers are on track to deliver a 9.78% CAGR through 2030.

- By geography, Europe dominated with 37.65% share in 2024, while Asia-Pacific is projected to grow the fastest at a 9.98% CAGR to 2030

Market Trends and Insights

Drivers Impact Analysis of Face Wash Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising busy lifestyle and on the go snacking | +2.3% | Global, with highest impact in urban centers across North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Expansion of cloud-kitchen networks | +1.8% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Attractive discounts, loyalty programs, and subscription models | +1.5% | Global, with regional variations in discount sensitivity | Short term (≤ 2 years) |

| Integration of AI and data analytics for personalized offerings | +1.2% | North America and Europe leading, Asia-Pacific rapid adoption | Medium term (2-4 years) |

| Growing smartphone and internet penetration | +0.8% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Innovative loyalty programs and discounts | +0.7% | Global, with emphasis on mature markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Natural and Organic Skincare

As consumers increasingly prioritize transparency, safety, and ingredient integrity, the face wash market is pivoting decisively towards natural and organic skincare. Urban consumers, especially in premium markets, are shunning synthetic additives, harsh chemicals, and artificial fragrances, opting instead for gentle, plant-based alternatives. A March 2025 study by NSF, a prominent global public health and safety organization, revealed that 74% of consumers deem organic ingredients crucial in personal care products, highlighting the momentum behind the clean beauty movement [1]Source: NSF International, “Global Consumer Insights on Organic Personal Care,” nsf.org. In response, brands are reformulating and repositioning their products. Established names like Weleda and Dr. Hauschka are championing trusted botanical ingredients, while newer entrants are carving a niche with minimalist formulations and certifications like COSMOS and NATRUE. Today's skincare consumers are discerning, scrutinizing product labels, demanding ingredient transparency, and delving into digital content to grasp sourcing and efficacy. Ingredients such as aloe vera, chamomile, green tea, and coconut-derived surfactants are gaining popularity, especially among those with sensitive skin. With clean beauty becoming mainstream, natural and organic face washes have transitioned from niche offerings to essential components of contemporary skincare routines.

Face Wash Innovations Cater to Changing Consumer Tastes

Consumer demand for targeted skincare solutions is reshaping the face wash market. Today's consumers are increasingly seeking products that address specific concerns, from sensitivity and dullness to environmental stress. Active ingredients like niacinamide, hyaluronic acid, and vitamin C have taken center stage in formulations, offering benefits such as barrier repair, hydration, and brightening. According to Aveeno’s 2024 State of Skin Sensitivity report, 71% of global consumers now report skin sensitivity, driving demand for gentle yet effective formulations that avoid harsh surfactants and allergens [2]Source: Kenvue Inc., “Aveeno State of Skin Sensitivity 2024,” aveeno.com . Brands like The Ordinary and Minimalist are rising to the occasion with science-backed, low-irritation formulas focused on transparency and performance. Emerging players like Plum and Deconstruct are carving out their niche with fragrance-free, dermatologist-tested cleansers targeting acne, redness, and barrier damage. Innovation is also extending into multifunctional products, such as Dot & Key’s Cica and Niacinamide Face Wash with SPF 20, merging cleansing with UV protection. These trends highlight how brands are evolving to meet the needs of a discerning, ingredient-conscious audience that values personalization, protection, and simplicity in their skincare routines.

Expansion of Men's Grooming Segment

Men's grooming is undergoing a significant transformation, with face wash products now central to male self-care routines. This evolution is fueled by shifting views on masculinity, a heightened emphasis on skin health, and the burgeoning impact of social media platforms, notably TikTok and Instagram, where male skincare content flourishes. Today's male consumers are proactive and discerning, actively seeking face washes tailored to combat issues like acne, excess oil, and skin damage from pollution. In response, brands are crafting face washes with specialized formulations and distinctly masculine branding. For example, Garnier's Men's OilClear and AcnoFight ranges are tailored to address men's unique skincare needs. Likewise, brands like Beardo and The Man Company are resonating with urban males by infusing high-performance ingredients like salicylic acid, menthol, and activated charcoal into their products, all while sporting bold, gender-specific packaging and messaging. Instead of merely adapting products aimed at women, these brands are offering solutions that genuinely cater to men's skincare aspirations.

Influencer-Led Digital Marketing and Consumer Engagement

Influencer-led digital marketing is reshaping the landscape of face wash sales, revolutionizing how consumers discover and trust skincare brands. Platforms like TikTok, Instagram, and YouTube have become the epicenters of beauty content, with influencers steering product perceptions and routines. Their ability to demystify ingredient functions, share personal experiences, and craft relatable narratives has resonated deeply, particularly in the face wash segment. A 2024 survey from the University of Portsmouth revealed that 60% of consumers trust influencer recommendations, with nearly half of all purchasing decisions swayed by these endorsements [3]Source: University of Portsmouth, “Influencer Impact on Consumer Skincare Choices,” port.ac.uk. Brands are keenly tapping into this trust. Minimalist surged ahead with creator-led tutorials and ingredient breakdowns, while Dot & Key collaborates with dermatologists and micro-influencers to spotlight solutions like niacinamide- and salicylic acid-infused face washes. On the global stage, CeraVe's meteoric rise on TikTok, fueled by dermatologists and influencers championing its hydrating cleanser, underscores the potency of educational, community-centric content in driving sales. These campaigns not only elevate brand visibility but also cultivate deeper engagement and loyalty, particularly among Gen Z and millennials who prioritize authenticity and clarity in their skincare journey.

Restraints Impact Analysis of Face Wash Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ingredient-sensitisation and stricter bans | -0.6% | EU leading, followed by North America and Asia-Pacific | Medium term (2-4 years) |

| Concerns Over Harmful Chemicals in Conventional Products | -0.4% | Global, with highest impact in developed markets | Short term (≤ 2 years) |

| Rise of Counterfeit Products Impacting Trust and Safety | -0.8% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Consumer Shift to DIY Solutions | -0.5% | North America and Europe, limited impact in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ingredient-Sensitisation and Stricter Bans

Face wash manufacturers, especially in Europe, grapple with tightening cosmetic regulations. These regulations, driven by concerns over ingredient sensitization and safety, are prompting significant changes in product formulations. Highlighting this shift, the EU has restricted retinol to a maximum of 0.3% and limited kojic acid to 1%. These moves are part of a broader ban on nine cosmetic ingredients, signaling a heightened focus on ingredient risk mitigation. Effective September 2025, an amendment by the European Commission to Regulation (EC) No 1223/2009 bans substances deemed carcinogenic, mutagenic, or toxic to reproduction. Furthermore, compliance challenges are amplified by new mandates requiring labeling for 81 fragrance allergens, especially at trace thresholds (0.01% for rinse-off products). While major players with robust regulatory frameworks can navigate these changes, smaller brands might struggle with the associated costs and necessary reformulations. Yet, this regulatory landscape also fosters innovation; brands that can quickly devise safe, effective, and compliant alternatives are poised for success. With a transition period extending to July 2026, companies face the challenge of balancing regulatory investments with the need to maintain market presence, especially in crucial European markets.

Rise of Counterfeit Products Impacting Trust and Safety

Counterfeit face wash products are eroding consumer trust and jeopardizing health safety worldwide. Many of these fakes harbor harmful agents, such as mercury, leading to severe dermatological and systemic issues. The rise of online marketplaces has exacerbated the situation, with beauty products now constituting 31% of globally intercepted counterfeit goods, often snagged by unsuspecting bargain hunters. In response, regulatory bodies are intensifying their efforts: the U.S. FDA’s Modernization of Cosmetics Regulation Act (MoCRA) enforces product registration and bolsters actions against unverified sellers. Concurrently, recent executive orders have tightened customs checks, curbing tariff loopholes exploited by counterfeiters. Yet, enforcement measures alone fall short. To combat this, premium brands are channeling investments into AI-driven label authentication, QR-code verification, and blockchain supply chain tracking. While these advanced solutions promise long-term security, they come with hefty investments and necessitate consumer awareness initiatives. While discount retailers with secure sourcing might see short-term gains, the pervasive issue of counterfeits poses a significant threat to high-trust, premium skincare brands, jeopardizing their reputation and diminishing consumer confidence in the face wash segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Face Wash Market Segment Analysis

By Product Type:

Foam-Based Formulations Drive InnovationIn 2024, gel-based face washes command the market with a 39.45% share, thanks to their versatility and deep cleansing prowess. These gels excel at removing makeup and excess oil without causing dryness, making them essential for daily skincare, especially for those with oily or combination skin. Trusted products like Neutrogena's Oil-Free Acne Wash and CeraVe's Foaming Gel Cleanser blend performance with dermatologist-favored ingredients, including salicylic acid and ceramides. Meanwhile, micellar and water-based cleansers cater to consumers desiring gentle, no-rinse options, especially those with sensitive skin. Oil-based cleansers are gaining traction in double-cleansing routines, a trend notably strong in Asian markets with their multi-step skincare rituals.

Foam-based cleansers are the rising stars, set to grow at a CAGR of 7.49% from 2025 to 2030. This surge is fueled by consumers' preference for lightweight, luxurious textures. Younger audiences, swayed by social media, are captivated by the visual allure and gentle touch of foaming cleansers. Brands like Innisfree, The Face Shop, and Plum are pioneering sulfate-free surfactants and biodegradable components, ensuring a rich lather while prioritizing safety and sustainability. Innovations in surfactant chemistry, like plant-based heptyl glucoside, enhance cleansing efficacy while minimizing irritants, resonating with eco-conscious consumers in the premium skincare arena.

By Skin Type:

Sensitive Skin Segment Accelerates GrowthIn 2024, face washes for normal skin captured 31.34% of the global market share, underscoring a widespread consumer preference for gentle, maintenance-oriented products. These face washes prioritize balance, hydration, and daily freshness, appealing to a diverse audience. Brands like Neutrogena’s Hydro Boost Cleanser and Cetaphil Gentle Skin Cleanser epitomize this trend, offering dermatologist-recommended solutions that safeguard skin health without compromising its natural barrier. Their extensive distribution through pharmacies and mass retail channels amplifies their market presence.

Meanwhile, the sensitive skin segment is set to expand at a 9.72% CAGR from 2025 to 2030. This growth is fueled by heightened awareness of skin barrier health and an increasing number of consumers reporting skin sensitivity, attributed to factors like pollution, climate change, and lifestyle stresses. Consequently, there's a surge in demand for hypoallergenic and fragrance-free products. Brands such as Avene, La Roche-Posay, and Bioderma are capitalizing on this trend, utilizing clinical research and dermatological endorsements to bolster consumer confidence. Their offerings often incorporate calming ingredients like thermal spring water, niacinamide, and panthenol, directly addressing concerns of irritation and redness.

By End User:

Men's Segment Transforms Market DynamicsIn 2024, women command a significant 62.25% share of the global face wash market. This enduring demand is bolstered by a deep-rooted skincare culture, where women diligently follow multi-step routines encompassing cleansing, treatment, and protection. Brands respond with diverse formulations addressing hydration, anti-aging, acne, and pigmentation concerns. Products such as Neutrogena Deep Clean, Cetaphil Gentle Cleanser, and L'Oréal Paris Revitalift Cleanser have secured their status as essentials, thanks to their targeted claims, dermatological endorsements, and widespread presence in both retail and e-commerce.

Meanwhile, the men's segment is on a rapid ascent, with projections indicating a CAGR of 8.74% from 2025 to 2030. This growth underscores a shift in consumer behavior, as more men embrace skincare, focusing on challenges like oil control and acne. Brands like Garnier Men, Beardo, and The Man Company are seizing this opportunity, offering face washes infused with active ingredients such as charcoal, salicylic acid, and menthol. Their triumph is rooted in blending product effectiveness with branding and messaging tailored to evolving male grooming standards.

By Ingredient Type:

Natural Formulations Gain Regulatory AdvantageIn 2024, conventional formulations command a dominant 62.34% share of the face wash market, thanks to their proven effectiveness, widespread availability, and cost-efficient production. These products often incorporate established active ingredients, resonating with a diverse consumer base, especially in mass-market segments. Brands like Clean & Clear, Pond’s, and Nivea leverage high-volume distribution and brand recognition to solidify their market positions. Even amidst heightened scrutiny, consumers, particularly in price-sensitive markets, gravitate towards conventional face washes for their quick results and affordability.

Conversely, face washes boasting natural and organic ingredients are on an upward trajectory, projected to grow at a CAGR of 8.22% from 2025 to 2030. This surge is largely attributed to a growing consumer inclination towards 'clean beauty' and plant-based formulations, which are increasingly viewed as safer and more sustainable. Regulatory changes, notably in Europe, where nine cosmetic ingredients are now under new restrictions, are further propelling this shift. Europe's dominance is underscored by its status as the leading importer of natural ingredients, accounting for 48% of global imports, cementing its role in championing the clean beauty movement. Brands such as Weleda and Dr. Hauschka, alongside newer entrants boasting COSMOS and NATRUE certifications, are capitalizing on this momentum, offering products that emphasize ethical sourcing and transparency.

By Distribution Channel:

Online Retail Dominates GrowthIn 2024, online retail stores command a leading 28.79% share of the global face wash market and are poised to be the fastest-growing channel, projected to expand at a CAGR of 9.55% from 2025 to 2030. This growth is largely attributed to consumers' growing preference for convenience, a wider product assortment, and direct engagement with brand narratives, often amplified by influencer content. Digital-native brands such as Minimalist, Plum, and Dot & Key have established robust e-commerce platforms. They've harnessed targeted social media initiatives, subscription services, and AI-driven skin diagnostics to elevate user engagement. Meanwhile, platforms like Nykaa and Amazon Beauty amplify this momentum, providing tailored solutions with seamless delivery, insightful reviews, and bundling options based on individual skin types and concerns.

Supermarkets and hypermarkets play a pivotal role, leveraging physical accessibility and the tendency for impulse purchases, especially among mass and mid-tier segments, though their growth is more tempered. Pharmacies and drugstores, including giants like Walgreens and Apollo Pharmacy, have cemented their reputation by offering dermatologically endorsed products, making them the go-to for sensitive skin and clinical formulations. Specialty beauty retailers, exemplified by Sephora, emphasize premium face washes and personalized in-store consultations

By Price Tier:

Premium Segment Captures Value MigrationIn 2024, mass market face wash products command a dominant 66.61% share, underscoring a robust consumer inclination towards budget-friendly solutions that cater to daily skincare needs. These face washes are staples on retail shelves, from supermarkets and drugstores to online platforms, especially in emerging markets where consumers are notably price-sensitive. Brands such as Clean & Clear, Pond’s, and Himalaya have solidified their leadership positions by ensuring broad appeal, maintaining recognizable branding, and delivering consistent performance at wallet-friendly prices. Yet, as consumers demand more value, this segment is evolving, prompting mass brands to innovate with superior ingredients, cleaner formulations, and enhanced packaging.

On the other hand, the premium segment is witnessing the fastest growth, with projections indicating a CAGR of 9.78% from 2025 to 2030. This surge is fueled by consumers' increasing focus on ingredient transparency, clinical efficacy, and the ethical values of brands. Brands like The Ordinary, Drunk Elephant, and Paula’s Choice have adeptly navigated this landscape, presenting science-driven formulations, minimalist packaging, and transparent communication about active ingredients.

Geography Analysis

Europe Face Wash Market

In 2024, Europe commands the global face wash market with a 37.65% share, propelled by heightened consumer awareness, stringent regulatory standards, and a robust demand for transparent skincare. While these regulations can be intricate, they spur innovation in both formulation and packaging, granting compliant brands a distinct competitive advantage. Countries such as Germany, France, the United Kingdom, and Italy exhibit a pronounced preference for natural and organic face washes. Esteemed brands like Weleda, La Roche-Posay, and Dr. Hauschka are gaining momentum, owing to their trusted ingredients and sustainability credentials. Europe's retail scene is a blend of traditional distribution methods and a surge in e-commerce, especially in premium and niche markets.

APAC Face Wash Market

Asia-Pacific emerges as the fastest-growing region, with projections of a 9.98% CAGR from 2025 to 2030. Increasing disposable incomes, a surge in digital commerce, and a youthful demographic spur this growth. Nations like China, India, and South Korea are at the forefront of global beauty trends, driven by swift innovation, tailored formulations, and robust domestic competition. Brands such as Mamaearth, Innisfree, and Perfect Diary are excelling in market adaptability, influencer collaborations, and skincare education, particularly in the mass and mid-tier segments. The rising trend of multi-step skincare routines and hybrid product formats is further amplifying per capita consumption.

The Americas and MEA Face Wash Market

Regions like North America are witnessing a surge in interest, especially in men's grooming and ingredient safety. Brands such as CeraVe, The Ordinary, and Jack Black are striking a chord with discerning consumers who prioritize efficacy and dermatological endorsement. In South America, there's a burgeoning beauty consciousness, paving the way for natural and budget-friendly face wash alternatives. Concurrently, the Middle East and Africa are seeing a spike in demand for premium products. Urban centers like Dubai, Riyadh, and Johannesburg are becoming hotspots, with both global and regional brands amplifying their presence through offline and online avenues.

Mordor Intelligence provides coverage of the face wash market across other key regional markets. Detailed country-level analysis extends to Bangladesh incorporating local coverage and market participation, as required.

Competitive Landscape

The market is moderately consolidated, with multinational giants like L'Oréal S.A., Unilever PLC, and The Procter & Gamble Company dominating the global face wash market, for their robust research and development, strong brand presence, and adeptness at navigating regulations. These industry titans are not just resting on their laurels; they're forging strategic partnerships and making acquisitions to stay attuned to shifting consumer trends. Unilever PLC is reshaping its portfolio with acquisitions like Paula’s Choice and Dermalogica, signaling a shift towards brands that emphasize clinical positioning and ingredient focus.

The competitive arena is coalescing around three pivotal themes: AI-driven personalization, eco-friendly packaging, and clinical validation. Brands are channeling investments into digital tools for bespoke skin analyses and tailored product suggestions. Neutrogena's Skin360 app and L'Oréal’s Perso device exemplify this trend, enabling users to customize their skincare. Clinical efficacy, once a niche concern, has taken center stage in building consumer trust, with brands like The Ordinary and Drunk Elephant emphasizing transparency, rigorous testing, and clear ingredient disclosures.

New-age disruptors are carving a niche with direct-to-consumer (DTC) strategies and influencer-driven marketing. Brands like Minimalist, Dot & Key, and The Man Company resonate with younger demographics, thanks to their clean formulations and engaging social media presence. These newcomers are making strides in traditionally underserved areas, such as men's grooming and products for sensitive skin, where established players have been slow to innovate.

Face Wash Industry Leaders

L'Oréal S.A.

Unilever PLC

The Procter & Gamble Company

Shiseido Company, Limited

The Estée Lauder Companies Inc

- *Disclaimer: Major Players sorted in no particular order

Face Wash Market Companies Covered in this Report

- L'Oreal S.A.

- Unilever PLC

- The Procter & Gamble Company

- Shiseido Company, Limited

- Beiersdrof AG

- The Estee Lauder Companies Inc

- Kenvue Inc.

- Kao Corporation

- Colgate-Palmolive Company

- Himalaya Wellness Company

- Kose Corporation

- Amorepacific Corporation

- Galderma Group AG (Cetaphil)

- Honasa Consumer Ltd.

- Bioderma Laboratories(NAOS)

- VLCC Health Care Ltd.

- Emami Ltd (The Man Company)

- Amway Corporation

- Forest Essentials Pvt. Ltd.

- The Body Shop International Limited

Recent Industry Developments in Face Wash Market

- June 2025: Glowbar launched the Expert Cleanser, a concentrated foaming face wash containing white willow bark, glycolic acid, and gluconolactone, packaged with a QR code linking studio bookings.

- February 2025: Starface introduced Star Wash, a gentle salicylic-acid foaming cleanser priced at USD 16–17, accompanying the brand’s U.S. expansion through Ulta.

- January 2025: Garnier released India’s first anti-acne face wash formulated for men, supported by multimedia campaigns across digital and traditional outlets.

Global Face Wash Market Report Scope

Segmentation Overview

| Gel-based |

| Foam-based |

| Micellar/Water-based |

| Oil-based |

| Oily |

| Dry |

| Combination |

| Sensitive |

| Normal |

| Women |

| Men |

| Kids/Children |

| Conventional |

| Natural and Organic |

| Supermarkets/Hypermarkets |

| Pharmacies/Drugstores |

| Online Retail Stores |

| Specialty Beauty Retail |

| Others |

| Mass |

| Premium/Luxury |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Gel-based | |

| Foam-based | ||

| Micellar/Water-based | ||

| Oil-based | ||

| By Skin Type | Oily | |

| Dry | ||

| Combination | ||

| Sensitive | ||

| Normal | ||

| By End User | Women | |

| Men | ||

| Kids/Children | ||

| By Ingredient Type | Conventional | |

| Natural and Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drugstores | ||

| Online Retail Stores | ||

| Specialty Beauty Retail | ||

| Others | ||

| By Price Tier | Mass | |

| Premium/Luxury | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the face wash market?

The face wash market is valued at USD 23.16 billion in 2025 and is expected to reach USD 32.55 billion by 2030.

Which region is growing the fastest in face wash sales?

Asia-Pacific is forecast to expand at a 9.98% CAGR through 2030, the highest of any region, driven by e-commerce adoption and rising disposable income.

Why is the sensitive-skin segment expanding so quickly?

Increased pollution exposure, stricter allergen regulations, and greater consumer awareness of barrier health are pushing demand for gentle, clinically tested cleansers, resulting in a 9.72% CAGR projection.

What ingredients are most in demand for natural face washes?

Botanical actives such as aloe vera, chamomile, green tea, and coconut-derived surfactants are popular because they align with clean-label expectations and offer gentle cleansing benefits.

Page last updated on: