Lip Gloss Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

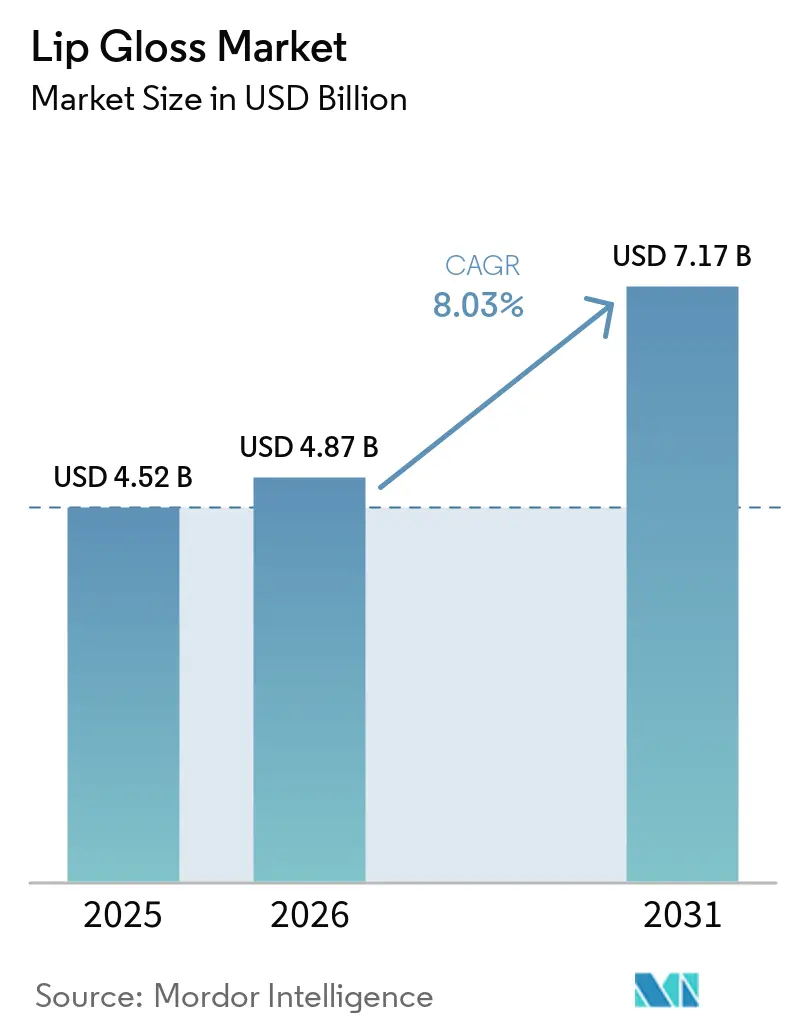

| Market Size (2026) | USD 4.87 Billion |

| Market Size (2031) | USD 7.17 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lip Gloss Market Analysis by Mordor Intelligence

The lip gloss market size is expected to grow from USD 4.52 billion in 2025 to USD 4.87 billion in 2026 and is forecast to reach USD 7.17 billion by 2031 at an 8.03% CAGR over 2026-2031. The lip gloss market is benefiting from a steady shift toward lip products that combine color, hydration, and treatment in one format, which keeps usage frequent and broadens appeal across age groups. The lip gloss market is also gaining from faster product discovery through social platforms and from shorter launch cycles, which help brands turn visibility into repeat purchases more quickly. Premiumization is supporting value growth in the lip gloss market, yet the category still keeps a strong mass base because gloss remains an accessible purchase even when shoppers become more selective. Online expansion is opening more room for the lip gloss market, while counterfeit risk, compliance costs, and input cost pressure are making brand trust, sourcing discipline, and margin management more important. These conditions are pushing the lip gloss market toward a model where product quality, channel control, and speed to market matter as much as scale.

Key Report Takeaways

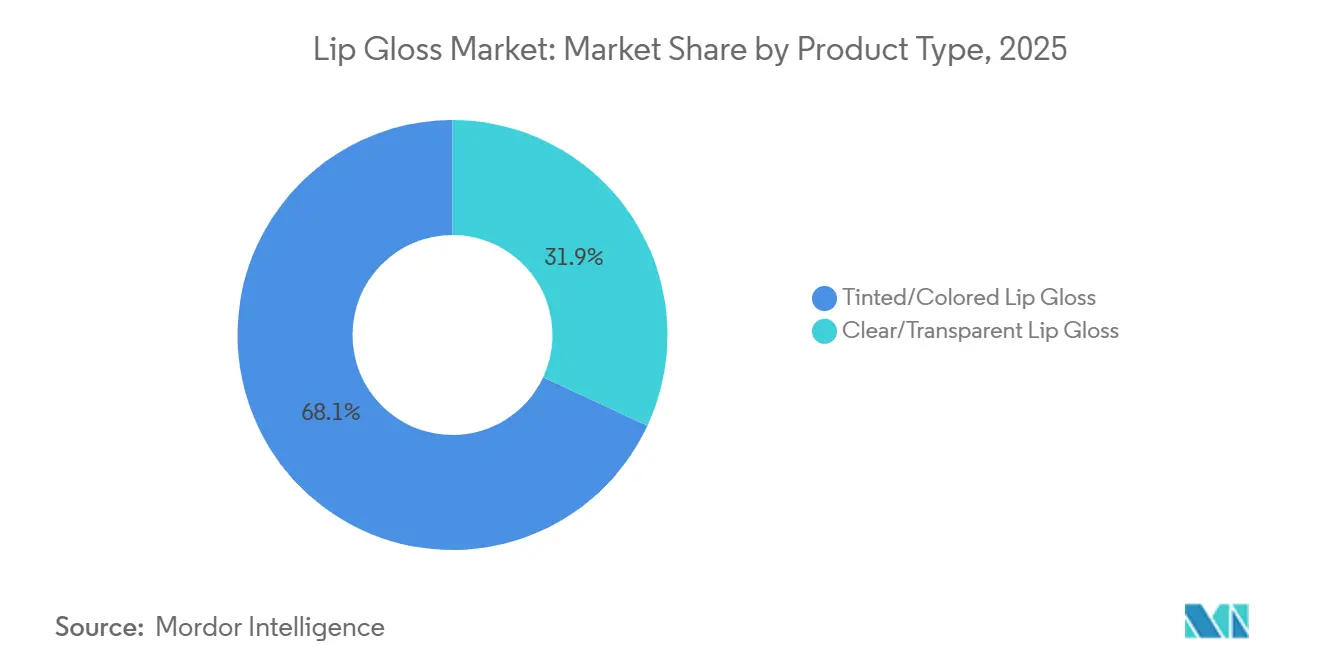

- By product type, tinted/colored lip gloss led with a 68.04% share in 2025 and is forecast to expand at an 8.78% CAGR through 2031.

- By price, mass products held a 71.03% share in 2025, while premium products recorded the highest projected CAGR at 9.33% through 2031.

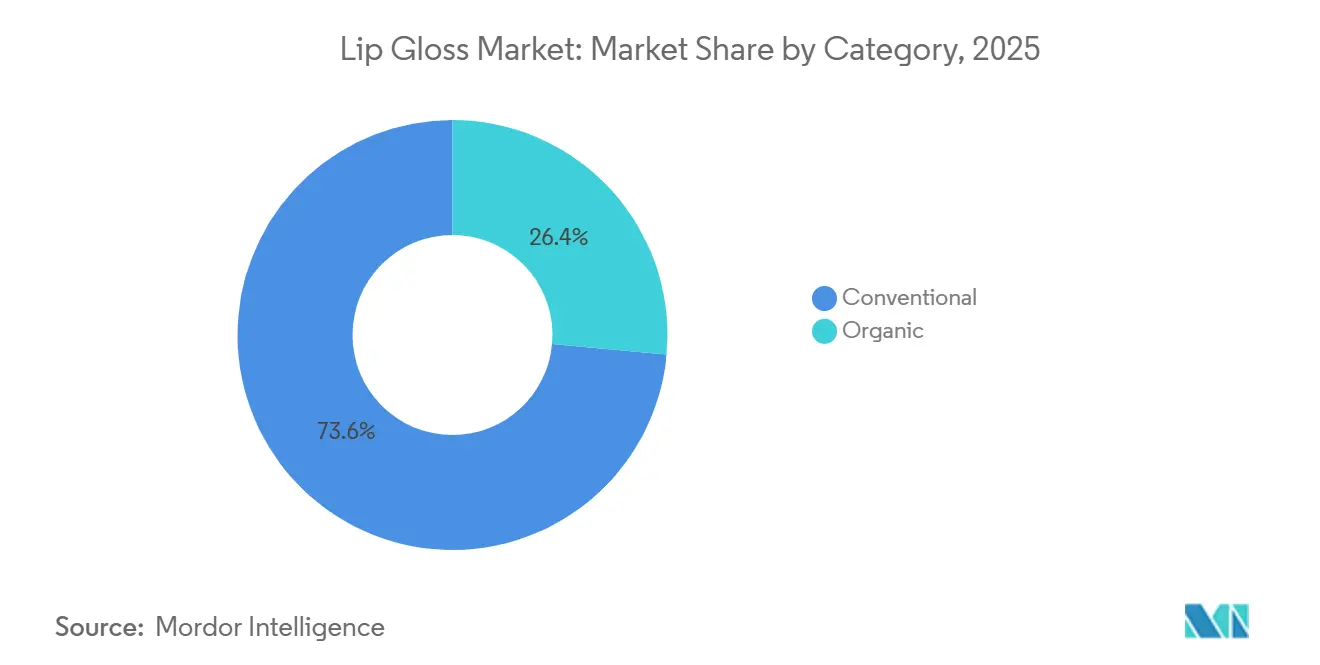

- By category, conventional products accounted for a 73.56% share in 2025, while organic products are advancing at a 7.69% CAGR through 2031.

- By distribution channel, beauty and health stores held a 46.73% share in 2025, while online retail stores are projected to grow at an 8.04% CAGR through 2031.

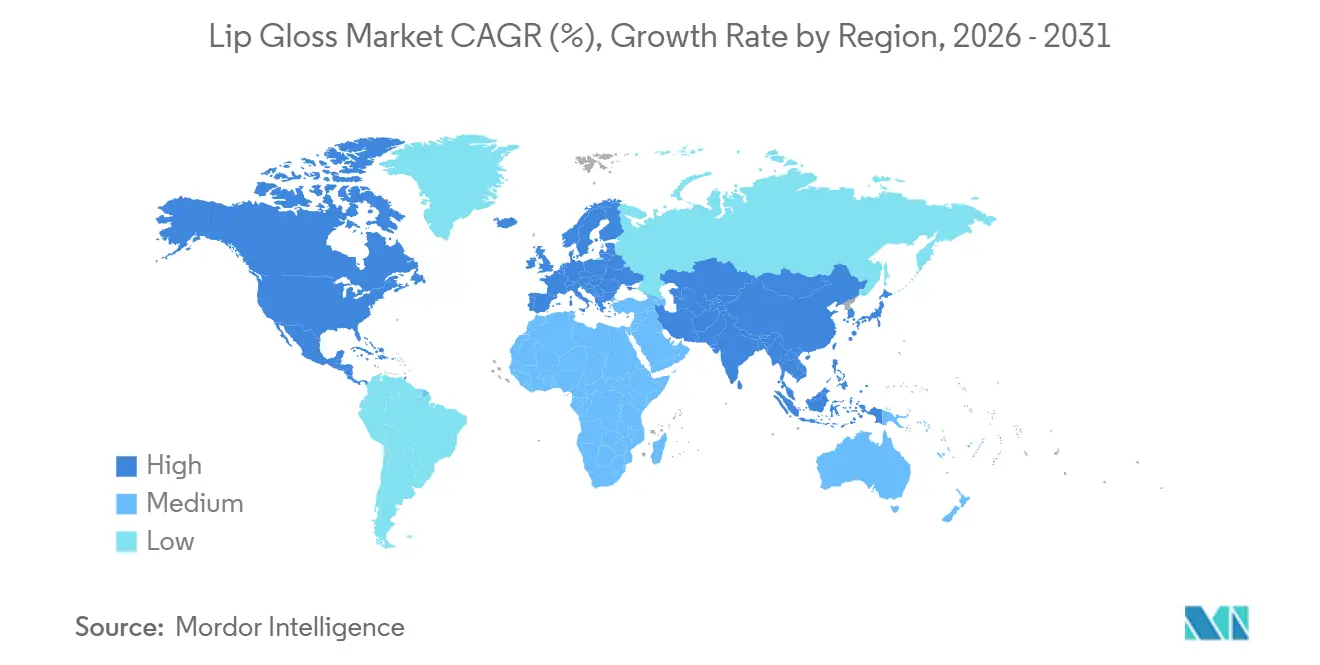

- By geography, North America held a 34.81% share in 2025, while Asia-Pacific is expected to record the fastest regional CAGR of 8.48% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lip Gloss Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social Media Influencers Accelerate Lip Gloss Adoption | +2.3% | Global, with concentrated effect in North America, South Korea, and Southeast Asia | Short term (≤ 2 years) |

| Product Innovations Enhance Texture and Wearability | +1.9% | Global, with early gains in North America, Western Europe, and East Asia | Medium term (2-4 years) |

| Clean-Label And Vegan Beauty Trends Boost Sales | +1.6% | North America and EU (European Union) core, with spillover to urban Asia-Pacific and Middle East | Medium term (2-4 years) |

| Rising Demand For Glossy, Natural Makeup Looks | +1.4% | Global, strongest in North America, France, South Korea, and Brazil | Short term (≤ 2 years) |

| Affordable Luxury Appeal Drives Impulse Purchases | +0.9% | Global, especially mass-market concentrated regions in South America and Middle East and Africa | Short term (≤ 2 years) |

| Rising Self-Care And Personal Grooming Awareness | +0.8% | Global, with fastest uptake in South Asia and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Social Media Influencers Accelerate Lip Gloss Adoption

Social platforms now shape how the lip gloss market reaches consumers, especially in the early stage of product discovery. Visual lip content works well in short-form formats because it is easy to demonstrate, quick to compare, and simple for consumers to imitate. Brands are responding by linking launches to culture and celebrity moments rather than relying only on shelf visibility. LANEIGE used this approach in January 2026 when it paired the JuicePop Box Lip Tint launch with the KATSEYE partnership across Sephora, Amazon, and Sephora at Kohl’s, showing how marketing and distribution are now coordinated from the start. This pattern is helping the lip gloss market convert attention into trial more quickly than many adjacent color cosmetics categories.

Product Innovations Enhance Texture and Wearability

The lip gloss market is moving beyond simple shine and is increasingly defined by comfort, treatment claims, and easier daily wear. Brands are launching products that combine color payoff with hydration, serum textures, blur effects, and smoother application, which widens use cases from occasional wear to everyday use. Shiseido’s May 2026 release of the PERFECT PINK Techno Satin Gel Lipstick collection and its focus on comfortable wear show how leading companies are building lip launches around performance and texture rather than color alone. LANEIGE’s JuicePop Box Lip Tint also reflects this direction because the launch centered on tinted, treatment-linked lip performance in mainstream prestige channels. As a result, the lip gloss market is seeing stronger repeat use from consumers who once separated lip care and lip color into different purchases.

Clean-Label and Vegan Beauty Trends Boost Sales

Clean positioning is influencing the lip gloss market because lip products sit close to daily comfort, ingredient awareness, and routine use. This makes formulation language more important than in some other makeup categories, especially when brands want to justify a premium or attract first-time buyers. Regulation is reinforcing that shift in Europe because cosmetic products must meet a clear compliance framework before sale, including safety assessment and product notification requirements[1]Source: European Union, "Consolidated text: Regulation (EC) No 1223/2009 of the European Parliament and of the Council of 30 November 2009 on cosmetic products (recast) (Text with EEA relevance)" eur-lex.europa.eu. That environment favors companies that can simplify formulas, document claims, and manage ingredient disclosure without slowing launches. For that reason, the lip gloss market is likely to keep rewarding brands that combine treatment benefits with cleaner and more transparent product positioning.

Affordable Luxury Appeal Drives Impulse Purchases

The lip gloss market continues to benefit from small-ticket indulgence because lip products are easier for consumers to add to a basket than higher-priced beauty items. This helps keep the mass base wide, even as premium products take more share through treatment claims and packaging upgrades. Brands are also using novelty and collaborations to make low-cost products feel current and collectible. E.l.f. Cosmetics used that playbook in January 2026 with the e.l.f. x Liquid Death Lip Embalms launch across elfcosmetics.com and TikTok Shop, showing how accessible pricing and high-visibility partnerships can work together. This balance between affordability and excitement remains an important support for the lip gloss market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit Products Undermine Consumer Trust Online | -1.4% | Global, with highest risk concentration in North America, United Kingdom, and Southeast Asia e-commerce markets | Short term (≤ 2 years) |

| Raw Material Price Volatility Impacts Production Costs | -1.1% | Global, with margin pressure concentrated in mass-market manufacturers in Asia and North America | Medium term (2-4 years) |

| Ingredient Sensitivity Limits Adoption Among Users | -0.7% | Global, with elevated concern among adult consumers in North America and Western Europe | Long term (≥ 4 years) |

| Regulatory Compliance Requirements Increase Business Complexity | -0.5% | EU core and North America, with spillover to ASEAN and GCC markets adopting stricter cosmetics standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Undermine Consumer Trust Online

Counterfeit exposure is a real constraint for the lip gloss market because it weakens trust in the same online channels that support discovery and repeat purchase. When consumers receive poor-quality or unsafe products through third-party sellers, brand damage can follow even when the brand was not responsible for the sale [2]Source: Personal Care Products Council, "Counterfeit Cosmetics", personalcarecouncil.org. The problem is serious enough that the Personal Care Products Council launched the Buy No Lie campaign in late 2025 to warn shoppers about fake beauty products during peak buying periods. This issue affects both prestige and mass products because lip items are easy to copy, easy to ship, and widely promoted online. Unless platform controls improve, the lip gloss market will continue to face friction in online conversion and brand loyalty.

Regulatory Compliance Requirements Increase Business Complexity

Compliance is becoming more demanding in the lip gloss market, especially for brands that operate across several regions and price tiers. In the European Union, cosmetic products must meet formal safety, labeling, and notification requirements before they can enter the market[3]Source: U.S. Food & Drug Administration, "Modernization of Cosmetics Regulation Act of 2022 (MoCRA)", fda.gov. These rules raise the cost of reformulation, documentation, and packaging updates, particularly when companies manage broad shade ranges and frequent launches. Larger companies can spread those costs across bigger portfolios, while smaller brands often face slower expansion and tighter margins. This means the lip gloss market will remain open to innovation, but not on equal terms for every participant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tinted Formats Command the Category

Tinted/colored lip gloss held 68.04% of the Tinted/colored lip gloss market share in 2025 and is expected to grow at an 8.78% CAGR through 2031. This combination of leading scale and fastest growth is unusual, and it shows that demand is not being driven by a short-lived fashion cycle. The segment fits both natural looks and stronger color expression, which makes it useful across everyday and occasion-led routines. It also benefits from the broader move toward hybrid lip products that offer shine, hydration, and treatment in a single format. As a result, the Tinted/colored lip gloss industry is seeing stronger purchase frequency in this segment than in more limited lip formats.

The segment’s momentum is also visible in current launch activity from major brands. LANEIGE introduced the JuicePop Box Lip Tint in January 2026 across Sephora, Amazon, and Sephora at Kohl’s, reinforcing the commercial focus on tinted lip formats in prestige-led retail. Shiseido’s May 2026 limited collection also leaned into high-pigment, comfortable-wear lip color, which supports the same consumer shift toward treatment-linked color use. Clear or transparent gloss still serves hydration-focused and layering use, but it does not currently match the broader appeal or stronger growth profile of tinted formats.

By Price: Mass Volumes Hold While Premium Margin Expands

Mass products accounted for 71.03% of the value in 2025, which confirms that the lip gloss market still rests on a wide entry-level consumer base. Lip gloss remains easy to trial, easy to replace, and affordable enough to support repeat buying across income levels. That keeps volume concentrated in the mass tier, especially where pharmacy, grocery, and digital convenience purchases matter. The mass segment also benefits from product formats that deliver a visible payoff without a large spending decision. This foundation gives the lip gloss market a resilient baseline even when consumers become cautious in other beauty categories.

Premium products are projected to grow at a 9.33% CAGR through 2031, which shows that value expansion is happening above the mass core. This growth is tied to formulas that promise more than color, including comfort, hydration, smoother texture, or treatment-led positioning. Shiseido’s 2026 limited lip launch and LANEIGE’s 2026 tint campaign both show how premium brands are selling lip products as performance beauty rather than simple makeup. The lip gloss industry is therefore keeping mass breadth while using premium innovation to raise category value.

By Category: Conventional Dominance and Organic Acceleration

Conventional products held 73.56% share in 2025, so the lip gloss market is still led by standard formulations and familiar ingredient systems. This reflects scale, price accessibility, and the fact that many shoppers continue to buy on shade, finish, and convenience first. Conventional products also benefit from broader shelf presence and faster rollouts across mainstream channels. That makes their position durable in the near term, even as preferences continue to shift. The category’s current structure shows that legacy formulations remain commercially strong, but they are no longer the only growth engine.

Organic products are forecast to grow at a 7.69% CAGR through 2031, which indicates that clean-label demand is moving further into the mainstream. The shift is being supported by tighter regulatory expectations, more ingredient-aware shoppers, and stronger brand use of treatment and transparency claims. In Europe, the compliance framework under the cosmetics regulation continues to favor disciplined formulation and documented product safety. Over time, this will keep lifting the organic segment, even though conventional products remain the larger part of the lip gloss market for now.

By Distribution Channel: Specialty Retail Leads, Online Closes the Gap

Beauty and health stores accounted for 46.73% of the lip gloss market size in 2025, which keeps specialty retail in the leading channel position. These stores matter because lip products still benefit from shade comparison, texture testing, and impulse buying near checkout or adjacent beauty displays. Consumers often want to see applicators, finishes, and wear feel before committing to a purchase, especially in newer formulas. This gives specialty chains a durable role in discovery, premium conversion, and multi-brand comparison. The lip gloss market, therefore, continues to rely on physical beauty retail for first purchase momentum.

Online retail stores are projected to expand at an 8.04% CAGR through 2031, which shows that repurchase behavior is moving steadily to digital channels. Brand launches already reflect that change, with LANEIGE distributing through Sephora, Amazon, and Sephora at Kohl’s, and e.l.f. using direct-to-consumer and TikTok Shop for lip-related drops. Supermarkets and hypermarkets remain important for mass access, while other channels such as travel retail, subscriptions, and social commerce extend reach at the edge of the category. The lip gloss market is therefore shifting toward a blended model in which stores drive trial and digital channels capture the refill cycle.

Geography Analysis

North America held 34.81% of the lip gloss market share in 2025, making it the largest regional contributor. The region benefits from mature beauty retail, high product availability, and a consumer base that responds well to formulation upgrades and premium claims. The market also favors brands that can coordinate specialty retail, direct channels, and social commerce rather than relying on only one route to market. Company behavior supports that view, with major brands using broad omnichannel launches to capture attention and repeat demand across U.S. beauty shoppers. North America also has a compliance environment that increasingly rewards established operators with stronger documentation and product control.

Europe remains a major bloc for the lip gloss market and is shaped by a mix of large mass channels and premium specialty retail. Germany and the United Kingdom continue to anchor demand and distribution, while France stands out for faster product upgrading within lip beauty. The European Union’s cosmetics framework sets a high compliance threshold, which raises operating discipline and tends to favor companies with deeper regulatory resources. South America adds a different profile, with Brazil supporting strong mass-volume demand through frequent purchase behavior and wide pharmacy access.

Asia-Pacific is the fastest-growing region at 8.48% CAGR through 2031, and it is becoming more important to the direction of the lip gloss market. China remains central because it combines scale, rising value demand, and product experimentation across younger consumers. South Korea continues to influence launch styles and format innovation, while India and Southeast Asia are widening the user base through urbanization and digital commerce adoption. The Middle East and Africa still represent a smaller regional position, but premium beauty expansion in markets such as the UAE and Saudi Arabia is creating a stronger base for future participation in the lip gloss market.

Competitive Landscape

The lip gloss market remains moderately concentrated, with global beauty groups, prestige houses, and agile challenger brands all competing for visibility and repeat purchase. Large companies benefit from portfolio depth, established compliance systems, and stronger shelf access across channels and regions. At the same time, smaller and faster-moving brands can gain traction quickly when they match trend timing, price, and digital reach. This keeps the lip gloss market competitive without letting any one company or small cluster fully control demand. The result is a category where scale matters, but execution still decides momentum.

Leading groups continue to invest in digital, brand breadth, and lip-focused innovation. L’Oréal reported 2025 sales of EUR 44.05 billion and said e-commerce exceeded 30% of total group sales, which shows how strongly large players now depend on digital channels for beauty growth. Cosmetics used a different model in January 2026 by pairing a lip launch with Liquid Death and distributing it through its own site and TikTok Shop, which shows how challenger brands can build visibility with lower-cost but high-impact activations. These approaches are different, but both reflect how the lip gloss market rewards strong channel fit and quick execution.

Prestige and masstige brands are also leaning into partnerships and product storytelling to defend share. LANEIGE tied its 2026 tint launch to a global music partnership and wide prestige distribution, showing how brand culture and retail access are now working together in lip launches. Shiseido used a limited-edition premium lip launch in Japan to reinforce product desirability and selective distribution in department stores and direct online channels. The lip gloss market is therefore being shaped by companies that can balance product novelty, brand trust, and channel precision. That balance will likely matter more than simple catalog size over the next few years.

Lip Gloss Industry Leaders

-

L'Oréal S.A.

-

Coty Inc.

-

Revlon, Inc.

-

Oriflame Holding AG

-

Chanel S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Shiseido launched the limited-edition "THE PERFECT PINK" Techno Satin Gel Lipstick collection (5 shades, JPY 4,400/~USD 29 per unit), distributed across approximately 330 department stores nationwide in Japan and via the official Shiseido website, targeting the growing demand for high-pigment, comfortable-wear lip color in the premium East Asian market.

- January 2026: LANEIGE announced K-pop group KATSEYE as global brand partners, co-launching the Juice Pop Box Lip Tint (8 shades at USD 23 each) at Sephora, Amazon, and Sephora at Kohl's, marking the brand's deliberate strategy of using music-driven celebrity partnerships to accelerate tinted lip product adoption among Gen Z consumers in the US.

- January 2026: E.l.f. Cosmetics partnered with Liquid Death to launch the "e.l.f. x Liquid Death Lip Embalms" collection (available on elfcosmetics.com and TikTok Shop starting January 14, 2026), following their 2024 collaboration that sold out in 45 minutes. The launch demonstrates the brand's strategy of using unconventional co-branding to generate viral reach on social commerce platforms

Global Lip Gloss Market Report Scope

Lip gloss is a cosmetic product applied to the lips to provide a shiny, glossy appearance and, in some formulations, a subtle tint of color. The lip gloss market report is segmented by product type (clear/transparent lip gloss and tinted/colored lip gloss), price (premium and mass), category (organic and conventional), distribution channel (supermarkets/hypermarkets, online retail stores, and other distribution channels), and geography (North America, Europe, Asia-Pacific, and more). The market forecasts are provided in terms of value (USD).

| Clear/Transparent Lip Gloss |

| Tinted/Colored Lip Gloss |

| Premium |

| Mass |

| Organic |

| Conventional |

| Beauty and Health Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Clear/Transparent Lip Gloss | |

| Tinted/Colored Lip Gloss | ||

| Price | Premium | |

| Mass | ||

| Category | Organic | |

| Conventional | ||

| Distribution Channel | Beauty and Health Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retail Stores | ||

| Other Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size outlook for lip gloss through 2031?

The lip gloss market size is expected to rise from USD 4.9 billion in 2026 to USD 7.2 billion by 2031, at an 8.0% CAGR over the forecast period.

Which product type leads lip gloss demand today?

Tinted/colored lip gloss leads with a 68.04% share in 2025 and is also the fastest-growing product type, with an 8.78% CAGR through 2031.

Why are premium lip products growing faster than mass products?

Premium products are growing at a 9.33% CAGR because brands are adding hydration, treatment claims, and stronger texture performance that support higher price points.

Which sales channel matters most for lip gloss brands?

Beauty and health stores remain the largest channel with 46.73% share in 2025, while online retail stores are growing fastest at an 8.04% CAGR through 2031.

Page last updated on: