Shaving Foam Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

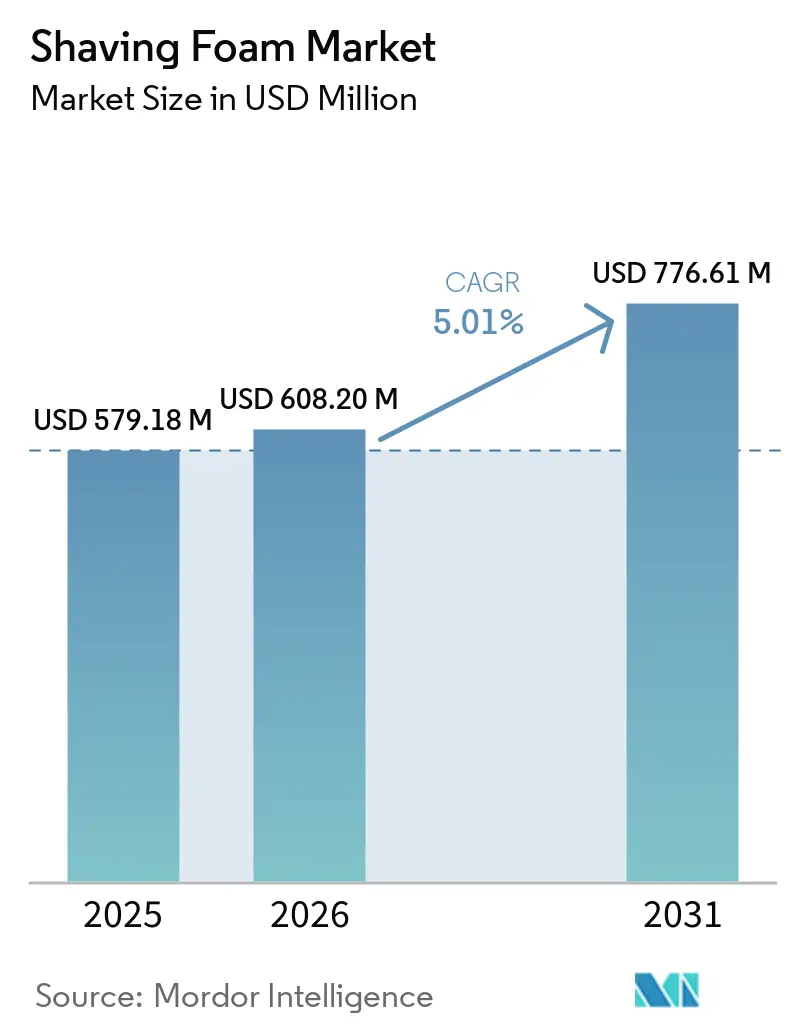

| Market Size (2026) | USD 608.20 Million |

| Market Size (2031) | USD 776.61 Million |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

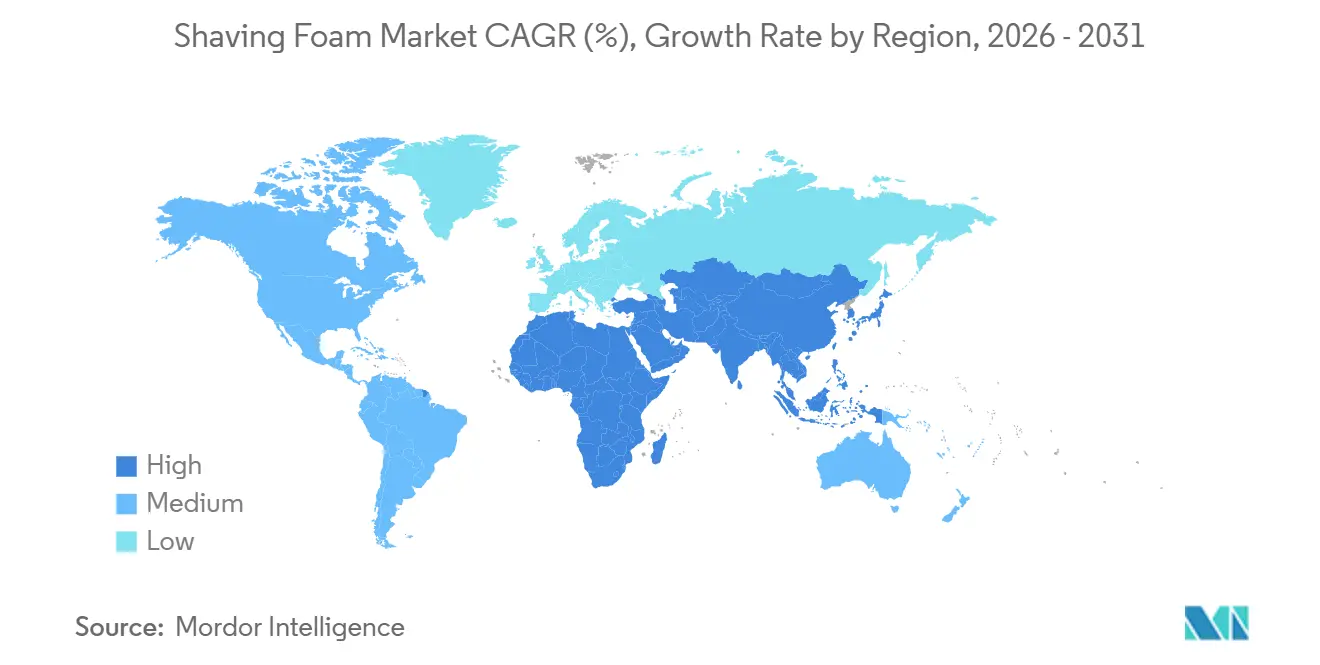

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Shaving Foam Market Analysis by Mordor Intelligence

The Shaving Foam Market size is expected to grow from USD 579.18 million in 2025 to USD 608.20 million in 2026 and is forecast to reach USD 776.61 million by 2031 at 5.01% CAGR over 2026-2031, underscoring the category’s enduring relevance despite the rise of electric grooming devices. Continuous aerosol innovation, growing demand for premium and eco-friendly formulations, and retailers’ omnichannel strategies sustain healthy sales momentum. Europe retains leadership thanks to strict environmental rules that spur sustainable product development, while Asia-Pacific’s urbanization and digital commerce push regional consumption higher. Established multinationals defend positions by upgrading formulations and bundling digital skin-analytics services, even as agile direct-to-consumer entrants siphon niche audiences. Raw-material price swings and tighter global VOC limits temper near-term margins but also accelerate green chemistry adoption.

Key Report Takeaways

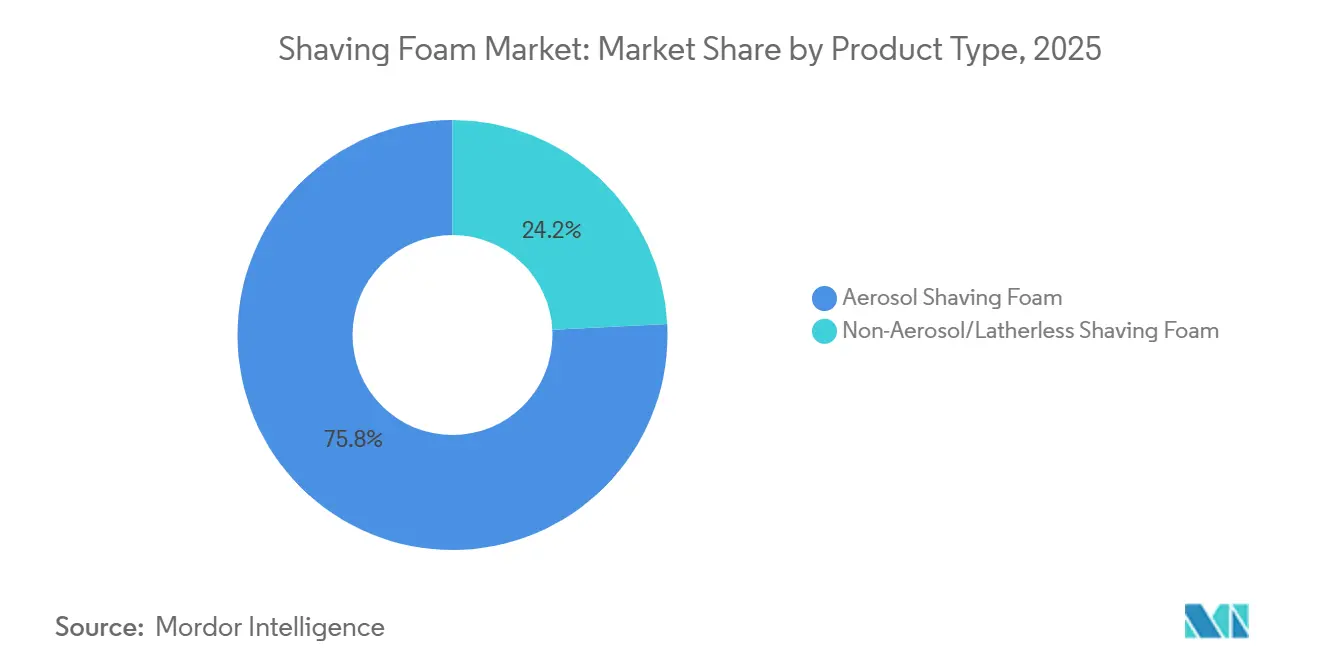

- By product type, aerosol formats led with 75.82% revenue share of the shaving foam market in 2025, while propellant-free alternatives are projected to expand at 5.23% CAGR through 2031.

- By consumer gender, male users commanded 95.02% share in 2025, whereas women’s products are advancing at a 7.05% CAGR through 2031.

- By category, conventional formulations captured 77.82% share in 2025; organic variants are expected to register 6.58% CAGR to 2031.

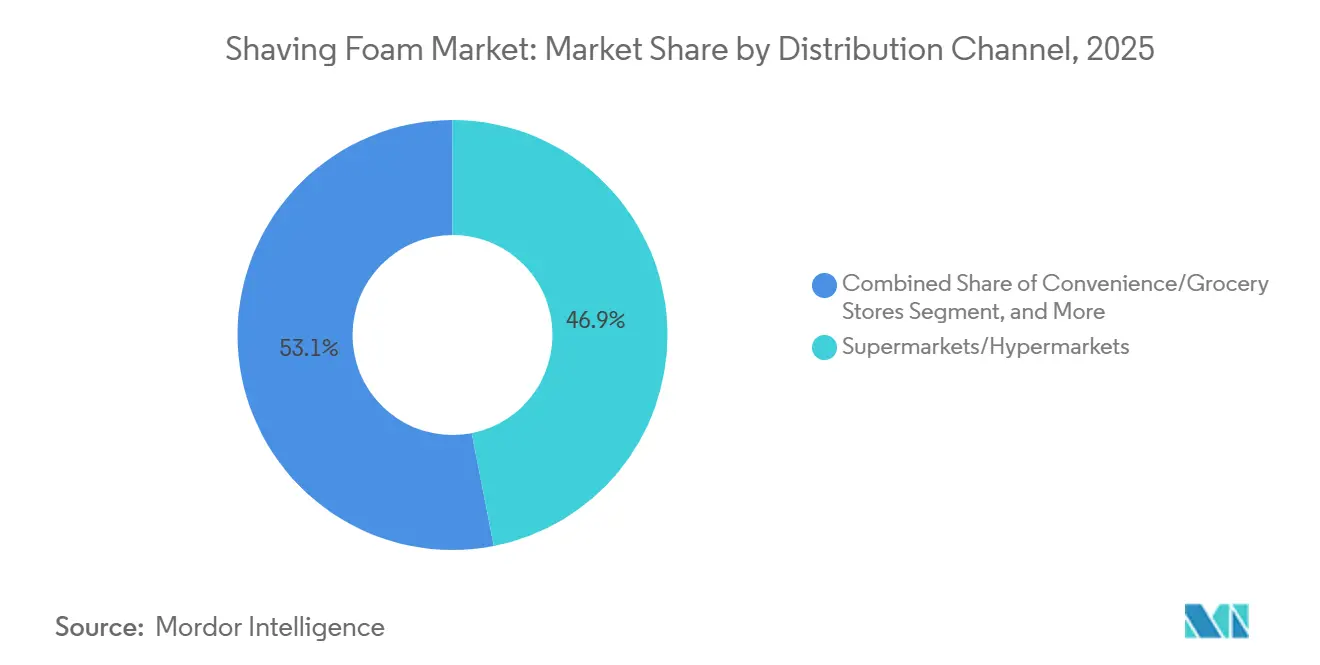

- By distribution channel, supermarkets and hypermarkets secured 46.92% share in 2025, whereas online retail is poised to grow at 7.62% CAGR through 2031.

- By geography, Europe held 32.98% of the shaving foam market share in 2025, while Asia-Pacific is forecast to post the fastest 6.23% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Shaving Foam Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising male grooming consciousness and daily self-care routines among younger demographics | +1.2% | Global, with strongest uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization and demand for added benefits | +0.9% | North America, Western Europe, and affluent Asia-Pacific markets | Medium term (2-4 years) |

| Adoption of propellant-free eco-friendly foams | +0.7% | Europe, North America, with spillover to Australia and Japan | Long term (≥ 4 years) |

| Ethnic-specific sensitive-skin formulations demand | +0.5% | North America, United Kingdom, South Africa, and multicultural urban centers | Short term (≤ 2 years) |

| Expansion of e-commerce and subscription models for personalized grooming kits | +1.0% | Global, led by North America and Asia-Pacific, with rapid adoption in India and China | Short term (≤ 2 years) |

| Influence of celebrity endorsements and social media advertisements | +0.6% | Global, with highest impact in North America, Europe, and social-media-saturated markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising male grooming consciousness and daily self-care routines among younger demographics.

Millennials and Gen Z males are redefining the grooming market by integrating it into their self-care routines. Shaving, once a mundane chore, is now a moment for mindfulness, self-expression, and personal presentation. Subscription-based grooming services reported retention rates exceeding 70% in 2025, highlighting how routine-based purchasing fosters loyalty and low churn. For brands, this shift presents an opportunity—positioning grooming products as personal ritual essentials rather than functional tools enables premium pricing and repeat purchases. Philips capitalized on this trend in 2024 by partnering with actor Adam Scott to market electric and wet-shaving tools as integral to daily wellness routines, addressing the rising demand for self-care products. Younger consumers prioritize transparency and efficacy, scrutinizing ingredient lists and expecting brands to communicate the functional benefits of components like aloe vera for soothing or glycerin for glide. This demographic values ethical sourcing and pays a premium for products aligning with their values and delivering perceived effectiveness. These preferences are driving a 5.01% CAGR, as brands with clear, compelling value propositions capture a larger market share. High-frequency users favor brands combining quality, transparency, and ethical practices, further strengthening their market position.

Premiumization and demand for added benefits

Consumers are shifting from basic lather to formulations offering skin conditioning, anti-irritation benefits, or post-shave hydration, blending shaving prep with skincare. This premiumization trend is prominent in North America and Western Europe, where higher disposable incomes enable experimentation with premium products. Brands are enhancing offerings with botanical extracts, vitamins, and peptides, marketing them as multi-benefit solutions. Premium SKUs command 30-50% higher retail prices, while incremental ingredient costs remain modest, driving margin expansion. However, brands must substantiate efficacy claims, especially with the Cosmetic Ingredient Review panel's March 2025 guidance on aerosolized product inhalation safety, requiring clinical evidence[1]Source: Cosmetic Ingredient Review. "Inhalation Safety Guidance for Aerosolized Products", cir-safety.org. . Sensory experience also drives premiumization, with fragrance, texture, and packaging aesthetics influencing purchase decisions alongside functional performance. Brands investing in sensory differentiation and credible benefit communication are capturing share in the conventional segment's 77.82% base while encouraging trials among consumers exploring organic alternatives.

Adoption of propellant-free eco-friendly foams

Environmental concerns and regulatory pressures are driving a shift toward non-aerosol and latherless formulations, eliminating hydrocarbon propellants and reducing packaging waste. The European Union's updated cosmetics regulations, effective December 2025, impose stricter limits on volatile organic compound emissions, compelling brands to reformulate or risk losing market access. Eco-conscious consumers favor propellant-free foams, dispensed via pumps or as gels that lather with water, which also mitigate supply-chain risks tied to petroleum-based butane and propane. However, pump-dispensed products require more vigorous application and may deliver inconsistent lather density, potentially impacting user satisfaction. Brands that optimize foam stability and glide performance in these formats can capitalize on the projected 5.23% CAGR in the non-aerosol segment. Refillable packaging systems are emerging as differentiators, though adoption remains limited due to convenience concerns and added costs. Achieving widespread acceptance of propellant-free alternatives will require significant investments in manufacturing retooling and consumer education.

Ethnic-specific sensitive-skin formulations demand

The growing demand for products tailored to coarse, curly hair and melanin-rich skin stems from their susceptibility to razor bumps, ingrown hairs, and post-inflammatory hyperpigmentation. Brands targeting Black, Hispanic, and South Asian consumers are incorporating ingredients like tea tree oil, salicylic acid, and shea butter to address these concerns. This market segment is expanding in multicultural urban hubs across North America, the UK, and South Africa, where cultural pride aligns with purchasing power. Authenticity is crucial; brands founded by or collaborating with these communities gain trust and organic promotion. Established players must go beyond ingredient tweaks, focusing on reformulation, clinical validation across diverse skin types, and culturally resonant marketing. The urgency is evident as consumers actively seek effective, culturally competent solutions, offering brands an opportunity to secure loyalty. However, the segment faces commoditization risks. Differentiation will depend on clinical validation and community endorsement rather than superficial positioning claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile propellant and surfactant raw-material prices | -0.8% | Global, with acute pressure in regions dependent on imported petrochemicals | Short term (≤ 2 years) |

| VOC-emission regulations on aerosol products | -0.6% | Europe, North America, with emerging compliance requirements in Asia-Pacific | Medium term (2-4 years) |

| Rising popularity of electric shavers and trimmers | -0.7% | Global, with highest substitution rates in North America and Western Europe | Long term (≥ 4 years) |

| Health concerns over chemical ingredients | -0.5% | Global, with heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile propellant and surfactant raw-material prices

In 2025, key surfactants and emollients like sodium laureth sulfate, ammonium lauryl sulfate, and isopropyl myristate experienced significant price swings due to crude-oil volatility and supply-chain disruptions, threatening margins. Propellant costs also remain exposed to hydrocarbon feedstock fluctuations, with liquefied petroleum gas prices spiking during geopolitical tensions or refinery outages. Brands in the mass segment with limited pricing power face a dilemma: absorb rising costs and compress margins or pass them on, risking volume loss. Procurement cycles, with contracts renewing quarterly or semi-annually, leave little room to mitigate spot-market volatility. Strategic responses include vertical integration, securing long-term supply agreements, or backward-integrating into surfactant production. Others optimize formulations to reduce ingredient usage, though reformulation risks alienating loyal users by altering lather density or skin feel. Brands that effectively hedge input costs while maintaining product consistency are better positioned to outperform competitors during raw-material market turbulence.

VOC-emission regulations on aerosol products

As air-quality concerns and climate commitments intensify, developed markets are tightening regulatory frameworks on volatile organic compounds. The European Union's cosmetics regulation update in December 2025 sets stricter limits on aerosol propellants, pushing brands to reformulate or risk exclusion. Meanwhile, in the U.S., the Environmental Protection Agency's December 2024 scrutiny of formaldehyde, a trace contaminant in some aerosol systems, underscores inhalation safety, despite modern formulations leaning towards alternative blowing agents[2]Source: U.S. Environmental Protection Agency, "Formaldehyde Assessment", epa.gov. Compliance isn't just a checkbox; it demands R&D investments, clinical testing, and packaging redesigns. This financial strain hits smaller players, who often lack the technical resources. Brands have a window of 18-36 months post-regulatory announcement to comply. However, those who act swiftly can market their reformulated products as "ahead of regulation," turning compliance costs into a competitive edge. And it's not just a Western concern; as Asia-Pacific regulators eye these developments, brands aligning early with these stringent norms stand to gain a significant advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aerosol Dominance Faces Eco-Pressure

In 2025, aerosol shaving foam held a dominant 75.82% market share, reflecting decades of consumer loyalty and the format's key advantages: instant lather, consistent density, and portability. However, this dominance is under threat. Rising raw material costs and stricter regulations on volatile organic compounds are eroding aerosols' cost and compliance benefits. Meanwhile, non-aerosol and latherless alternatives are growing at a 5.23% CAGR through 2031, appealing to eco-conscious consumers and brands seeking supply chain resilience. Latherless gels and creams, which foam upon water contact, eliminate propellants and reduce packaging weight, cutting logistics costs. Additionally, the Cosmetic Ingredient Review's March 2025 advisory on aerosol inhalation safety has driven brands to explore pump-dispensed foams that deliver similar lather without pressurized canisters.

The key challenge is whether non-aerosol formats can replicate aerosols' sensory benefits, rich lather, smooth glide, and ease of use, without altering user habits. Brands like Proraso and Taylor of Old Bond Street have built loyal followings with traditional soap-based lathers, but scaling these formats for mass-market adoption requires innovative packaging and consumer education. Aerosols' strength lies in their entrenched user base: millions associate the format with convenience and effectiveness. This creates inertia that non-aerosol entrants must overcome through superior performance or compelling sustainability narratives. During the forecast period, hybrid strategies are expected, with brands maintaining aerosol products for mainstream consumers while introducing propellant-free options for premium or eco-focused segments.

By Consumer Gender: Men's Dominance Challenged by Women's Growth

In 2025, men dominated the market with a 95.02% share, reflecting the male-centric grooming tradition. However, the women's segment is growing at a 7.05% CAGR through 2031, driven by reduced stigma around female body-hair removal and the introduction of products tailored to women's skin and hair needs. Women's shaving foams now focus on moisturization and fragrance, addressing the larger areas women shave, like legs and underarms, and their preference for skincare benefits. Brands such as Gillette, Venus, and Schick Intuition have normalized female shaving through gender-specific packaging and marketing, transforming it into a routine grooming practice.

The women's segment, growing 40% faster than the overall market, highlights younger women adopting grooming habits earlier and more frequently. While urban areas, influenced by Western beauty standards and higher disposable incomes, lead this growth, Asia-Pacific and Latin America are also emerging as key regions due to shifting cultural attitudes. Brands have a dual opportunity: capture this underpenetrated segment and command premium pricing through tailored formulations and marketing. However, commoditization remains a risk; if women's shaving products mirror men's beyond packaging, price competition could erode margins. Investing in clinically validated gender-specific benefits, such as reduced irritation or longer-lasting smoothness, will help brands differentiate and sustain premium positioning.

By Distribution Channel: Digital Disruption Accelerates

In 2025, supermarkets and hypermarkets accounted for 46.92% of sales, leveraging high foot traffic, impulse purchase visibility, and promotional bundling to boost volume. However, online retail is growing at a 7.62% CAGR through 2031, reshaping competition with convenience, personalization, and direct-to-consumer economics. E-commerce platforms allow brands to bypass retailer margins, reinvest savings in customer acquisition, and utilize first-party data for retention marketing. Subscription models, like Dollar Shave Club's grooming kits, secure recurring revenue and reduce churn through automated replenishment. Health and beauty specialty stores, offering expert advice and premium assortments, face challenges from mass retail's pricing and online convenience.

The 7.62% CAGR in online retail stems from structural advantages: lower overhead, algorithmic personalization, and the ability to serve niche segments unviable for physical retail. In Asia-Pacific, e-commerce is outpacing traditional distribution, enabling brands to reach tier-2 and tier-3 cities in India and China without brick-and-mortar partnerships. However, online channels increase price transparency and comparison shopping, compressing margins for undifferentiated products. Successful online brands focus on performance marketing, customer data platforms, and retention strategies like loyalty programs and personalized recommendations. During the forecast period, omnichannel strategies are expected to dominate, with brands maintaining retail presence for discovery and trial while driving repeat purchases online to capture both high-frequency and occasional users.

By Category: Organic Variants Gain as Ingredient Scrutiny Intensifies

In 2025, conventional formulations held a dominant 77.82% market share, driven by established supply chains, cost advantages, and consumer familiarity. Meanwhile, organic shaving foam variants are growing at a 6.58% CAGR through 2031, fueled by increasing ingredient scrutiny and demand for natural, cruelty-free, and sustainably sourced products. A December 2025 U.S. Food and Drug Administration report on per- and polyfluoroalkyl substances in cosmetics heightened consumer concerns about synthetic chemicals, even in rinse-off products like shaving foam[3]Source: U.S. Food and Drug Administration. "FDA Report on Testing of Cosmetics for PFAS", fda.gov. Organic formulations, certified by USDA Organic, COSMOS, or Ecocert, exclude synthetic preservatives, sulfates, and artificial fragrances, appealing to consumers prioritizing ingredient transparency and environmental impact.

The 6.58% CAGR in organic variants reflects premiumization and values-driven purchasing, particularly among millennials and Gen Z, who view consumption as an expression of identity. Brands like Bulldog Skincare and Proraso position organic lines as performance-equivalent to conventional alternatives, leveraging botanical extracts and essential oils for lather, glide, and post-shave conditioning. However, organic certification adds cost and complexity, requiring certified ingredient sourcing, segregated production lines, and third-party audits, limiting participation to scaled or premium-positioned brands. The forecast period will test organic growth's durability; if consumers see no functional advantage over conventional formulations, price sensitivity may limit adoption. Brands substantiating organic claims with clinical efficacy data and transparent sourcing narratives will secure loyalty, while those relying solely on certification risk commoditization.

Geography Analysis

In 2025, Europe commanded a significant 32.98% share of the shaving foam market, thanks to its long-standing wet-shaving traditions and proactive environmental regulations championing propellant innovations. German and UK consumers are opting for premium nitrogen-based cans, proudly certified under the stringent inhalation-safety guidelines of the European Aerosol Federation. The category's stability is bolstered by established retail channels and the rise of private labels, with sustainability certifications crucial for shelf placement. Additionally, manufacturers are tapping into EU Green Deal grants to upgrade their filling lines, leading to a marked reduction in carbon footprints.

Asia-Pacific is poised to lead, projecting a robust 6.23% CAGR through 2031. This growth is driven by rapid urbanization, rising disposable incomes, and a younger demographic gravitating towards Western beauty standards and premium personal care. China and Korea are at the forefront of online beauty shopping, setting the stage for social-commerce-driven launches of shaving products. With local preferences leaning towards skin-whitening additives and herbal fragrances, multinational R&D hubs in Seoul, Shanghai, and Mumbai are joining forces to craft region-specific products.

North America, while home to a substantial market, is witnessing a maturation phase, particularly as electric shavers gain traction at the expense of foam sales. The region benefits from clear regulatory guidelines, supporting long-term planning. Yet, retailers are pushing for recyclable cans, resonating with broader corporate ESG goals. In South America, the Middle East, and Africa, despite starting from a modest base, there's a discernible rise in shaving foam consumption, spurred by a burgeoning middle class. Sales often see seasonal spikes, coinciding with major events like football tournaments or Ramadan's gifting season. Furthermore, cross-border e-commerce is proving pivotal, granting consumers in secondary cities access to premium imports often missing from local stores.

Competitive Landscape

The market shows moderate concentration, with Procter & Gamble's Gillette, Edgewell Personal Care's Schick and Wilkinson Sword, and Beiersdorf's Nivea Men holding significant shares. These brands have built their positions over decades through brand equity, strong retail ties, and hefty marketing investments. Yet, emerging direct-to-consumer brands are now challenging these established giants, leveraging astute digital marketing and niche product positioning. In 2024, Procter and Gamble's grooming segment highlighted the industry's complexities: the company took a USD 1.3 billion impairment hit on Gillette, but also celebrated growth, thanks to premium positioning and a push into e-commerce, which now makes up 18% of total sales.

As the market matures, the focus shifts from category expansion to market share capture. This evolution prompts companies to invest heavily in product differentiation, marketing innovation, and channel diversification. In this commoditized arena, moves towards premiumization, sustainability, and direct consumer engagement stand out as key differentiators. Unilever's audacious USD 1.5 billion buyout of Dr. Squatch highlights this industry shift, zeroing in on premium men's grooming brands with a strong social media presence. Their ambition: elevate the premium product share from 35% to 50%, leveraging the distinct advantages of viral marketing over conventional ads.

New avenues are emerging in ethnic-specific products, women's grooming, and eco-friendly packaging that resonates with both regulatory standards and consumer environmental concerns. Brands that blend age-old grooming wisdom with modern digital tools, such as skin analytics and tailored recommendations, gain a competitive edge. This trend is reminiscent of the wider beauty sector's adoption of AI-driven virtual try-on features, even if consumer awareness remains limited.

Shaving Foam Industry Leaders

-

Edgewell Personal Care

-

Beiersdorf AG (Nivea)

-

Unilever PLC

-

Colgate-Palmolive Co.

-

The Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Gillette Venus partnered with Team USA figure skaters for the Milano Cortina 2026 Winter Olympics. Collaboration includes athlete endorsements and campaigns promoting smooth skin and irritation-free shaving.

- July 2025: Unilever completed its USD 1.5 billion acquisition of Dr Squatch, boosting its premium men’s grooming portfolio. The deal was framed as part of Unilever’s push into premium, high-growth personal care, with Dr. Squatch adding a strong digital-native brand and a loyal customer base.

- June 2025: Procter and Gamble outlined a productivity-focused strategy at the Deutsche Bank conference, spotlighting grooming innovation and cost discipline. The company highlighted grooming as a key area, using examples like Gillette Guard in India to show how it is driving category growth through superior products, better value, and stronger consumer relevance.

Global Shaving Foam Market Report Scope

Shaving foam is a pressurized or non-pressurized grooming product that dispenses as a light, airy lather and is applied to the skin before shaving to soften hair, lubricate the surface, and reduce friction between the razor and skin. The shaving foam market is segmented by product type into aerosol and non-aerosol/latherless, by consumer gender into men and women, by category into conventional and organic, by distribution channel into supermarkets/hypermarkets, health and beauty stores, online retail, and others, and by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market forecasts provided in terms of value (USD).

| Aerosol Shaving Foam |

| Non-Aerosol/Latherless Shaving Foam |

| Men |

| Women |

| Conventional |

| Organic |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Aerosol Shaving Foam | |

| Non-Aerosol/Latherless Shaving Foam | ||

| By Consumer Gender | Men | |

| Women | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the shaving foam market be by 2031?

The shaving foam market size is projected to reach USD 776.61 million by 2031 on the back of a 5.01% CAGR from 2026.

Which product format is growing fastest within shaving foams?

Propellant-free gels and pump foams are the fastest-rising format, forecast to grow at 5.23% CAGR as regulatory pressure and eco concerns mount.

Why is Asia-Pacific the most attractive region for future expansion?

Rising disposable incomes, urban e-commerce adoption, and a young consumer base push Asia-Pacific growth to 6.23% CAGR, outpacing every other region.

Are organic shaving foams taking significant share from conventional products?

Organic variants still represent a minority of revenue, yet they are advancing at 6.58% CAGR as ingredient transparency and certification draw health-conscious buyers.

Page last updated on: