Shaving Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

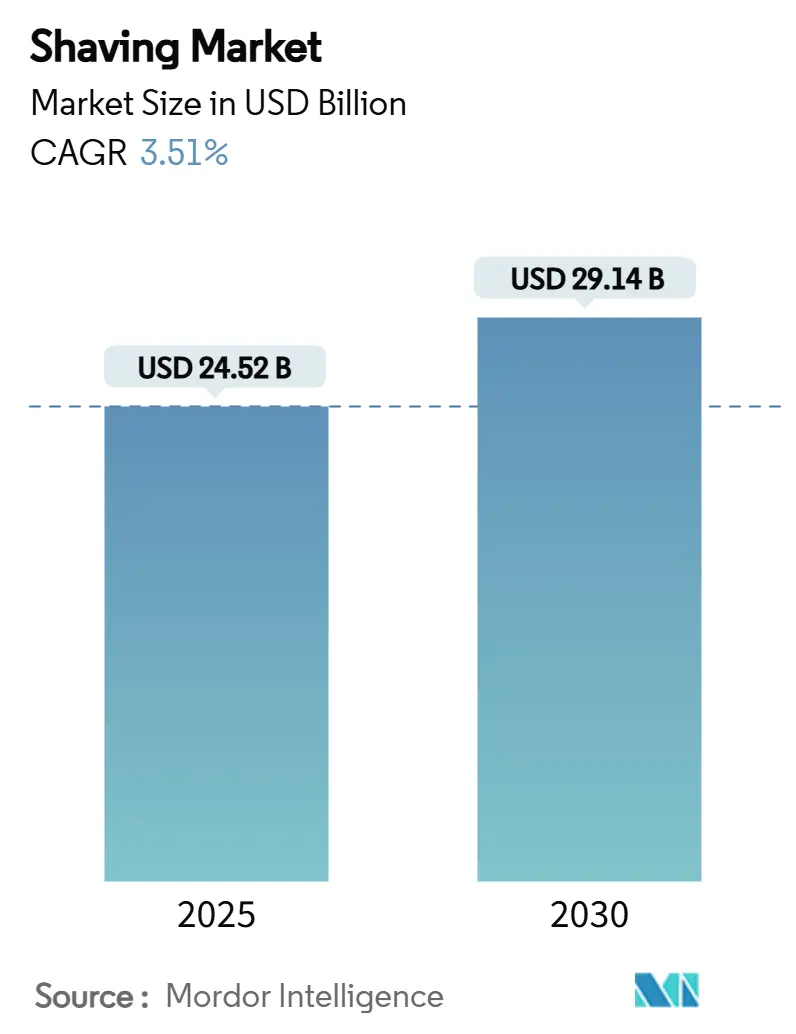

| Market Size (2025) | USD 24.52 Billion |

| Market Size (2030) | USD 29.14 Billion |

| Growth Rate (2025 - 2030) | 3.51% CAGR |

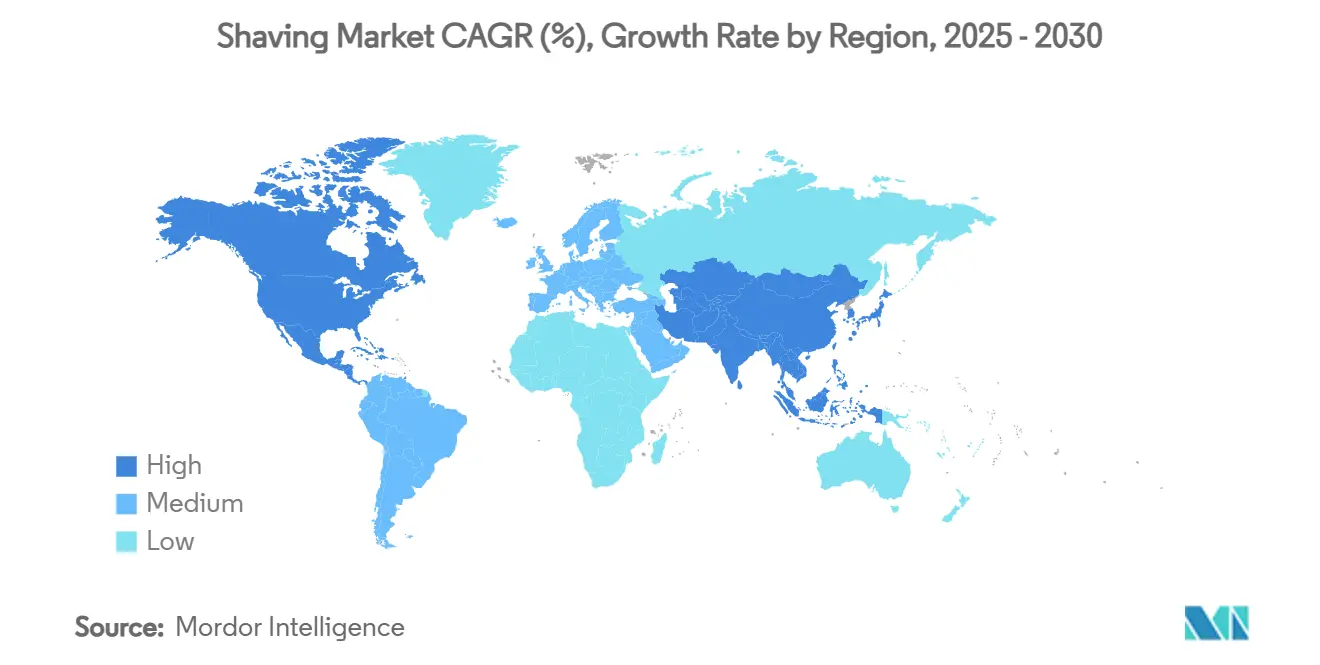

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Shaving Market Analysis by Mordor Intelligence

The shaving market size reached USD 24.52 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 3.51% through 2030, achieving USD 29.14 billion by the forecast period's end. The market's resilience stems from grooming's essential nature, with technological advancements in electric shavers and sustainability initiatives reshaping competitive dynamics across traditional and emerging segments. Innovation in blade coatings, AI-enabled electric shavers, and eco-friendly packaging is adding value faster than volume, supporting steady revenue growth in a mature global landscape. Premiumization continues to lift average selling prices as consumers gravitate toward multifunctional, skin-friendly solutions that promise speed, safety, and personalization. Retail channel disruption remains a second growth pillar: supermarkets and hypermarkets still drive the largest volumes, yet online platforms capture an ever-larger share as same-day delivery and subscription models take root. Regionally, Asia-Pacific anchors both scale and momentum, propelled by urbanization and a youthful population that views grooming as part of daily self-expression.

Key Report Takeaways

- By product type, razors and blades commanded 38.22% of the shaving market share in 2024, while electric shavers are projected to grow at a 4.72% CAGR through 2030.

- By price tier, the mass segment represented 79.82% of the shaving market in 2024, and the premium segment is growing at a CAGR of 5.21 through 2030.

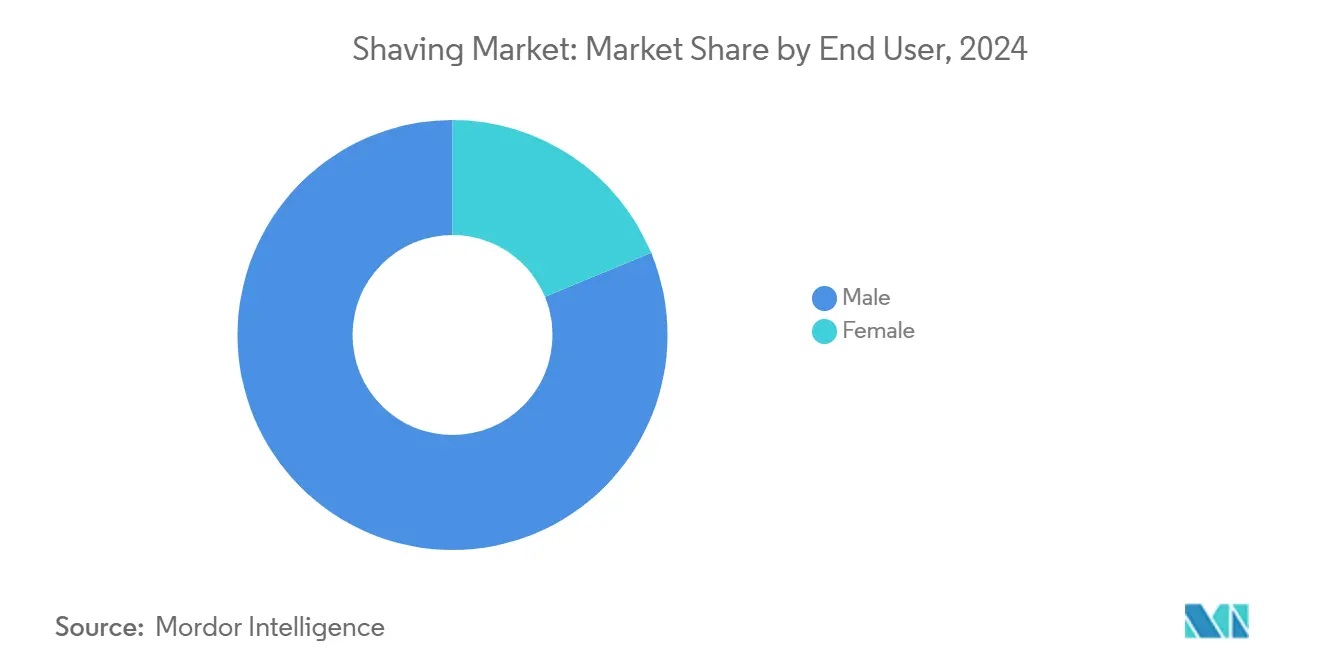

- By end-user, male users accounted for 81.24% of the shaving market size in 2024, yet female-focused lines are growing at a 5.34% CAGR through 2030.

- By distribution channel, supermarkets and hypermarkets held a 35.22% share of the shaving market size in 2024; online retail is advancing at a 5.67% CAGR to 2030.

- By geography, Asia-Pacific led with 33.04% shaving market share in 2024 and is forecast to post the fastest 5.03% CAGR through 2030.

Global Shaving Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Grooming Consciousness | +0.8% | Global, with strongest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Technological Advancements | +1.2% | North America and Europe leading, Asia-Pacific adoption accelerating | Long term (≥ 4 years) |

| Health and Hygiene Awareness | +0.6% | Global, post-pandemic acceleration in all regions | Short term (≤ 2 years) |

| Influence of Social Media and Celebrities | +0.7% | Global, particularly strong in North America and Asia-Pacific | Medium term (2-4 years) |

| Sustainability and Eco-Friendly Packaging | +0.5% | Europe and North America primary, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Multi-Functional and Convenient Products | +0.4% | Global, with premium segment concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements

Artificial intelligence integration transforms shaving experiences through personalized cutting power adjustment, as demonstrated by Philips' i9000 Series launch featuring AI-driven beard density recognition and real-time pressure guidance. Smart connectivity enables manufacturers to gather usage data, optimize product performance, and develop predictive maintenance capabilities that enhance customer loyalty and lifetime value. Advanced materials science delivers breakthrough innovations like Panasonic's NAGORI sustainable material, reducing plastic usage by 40% while maintaining performance standards. Sensor technology advancement enables motion control systems that provide real-time feedback on shaving technique, reducing skin irritation and improving outcomes for novice users. These technological leaps create significant differentiation opportunities for manufacturers willing to invest in research and development, while potentially obsoleting traditional mechanical solutions.

Health and Hygiene Awareness

Post-pandemic hygiene consciousness elevates shaving products beyond aesthetic considerations to essential health and wellness tools, driving demand for antimicrobial materials and easy-to-clean designs. Dermatological research highlighting shaving-induced skin irritation risks increases consumer focus on blade quality, lubricating strip formulations, and ergonomic handle designs that minimize pressure and friction. Professional recommendations from dermatologists and healthcare providers carry increased weight in product selection, benefiting brands with clinical backing and medical endorsements. The awareness trend drives innovation in sensitive skin formulations, with BIC's Flex 5 Sensitive Razor incorporating aloe, Vitamin E, and licorice extracts to address specific skin concerns. Regulatory emphasis on safety substantiation under MoCRA ( Modernization of Cosmetics Regulation Act) reinforces this trend by requiring manufacturers to demonstrate product safety through clinical testing and adverse event monitoring.

Influence of Social Media and Celebrities

Social media platforms and celebrity endorsements set grooming trends, raise brand recognition, and directly impact consumer purchasing decisions. Digital platforms reshape grooming product discovery and purchase decisions, through targeted advertising and influencer partnerships. Celebrity endorsements and viral marketing campaigns demonstrate social media's power to build premium grooming brands. For instance, in June 2025 BIC Soleil unveiled an empowering global brand platform, "Your Time to Shine." The campaign, which debuted first in North America, illuminated screens across connected TV, VOD, and social platforms, as well as via channels popular with consumers in their daily lives, from podcasts to dating apps. Micro-influencers and grooming tutorials create authentic product demonstrations that traditional advertising cannot match, particularly for complex products like electric shavers requiring technique education. The trend toward transparency and authenticity in social media content drives demand for brands with clear ingredient lists, sustainable practices, and genuine customer testimonials. This influence extends to packaging design and brand positioning, with visually appealing, Instagram-worthy products gaining competitive advantages in crowded retail environments.

Multi-Functional and Convenient Products

Consumers now favor shaving solutions that collapse multiple grooming steps into a single, portable device. Hybrid tools such as Philips OneBlade Pro switch seamlessly between edging, trimming, and clean-shave modes, eliminating the need for separate razors, trimmers, and clippers. Wet-and-dry compatibility adds shower convenience, while snap-on length combs support rapid beard styling for time-pressed users. USB-C fast-charge batteries and self-cleaning docks further streamline upkeep, making these all-in-one devices ideal for gym bags and business travel. As a result, manufacturers that focus on multi-functionality and grab-and-go ergonomics are capturing higher average selling prices and deeper customer loyalty. The integration of smart features like mobile app connectivity and personalized grooming recommendations has further enhanced the appeal of these devices. Market research indicates that consumers are willing to pay premium prices for devices that offer comprehensive grooming solutions, driving manufacturers to invest heavily in research and development of advanced multi-functional tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and Low-Quality Products | -0.9% | Global, particularly severe in Asia-Pacific and online channels | Short term (≤ 2 years) |

| High Price of Advanced Shavers | -0.6% | Emerging markets primarily, some impact in price-sensitive segments globally | Medium term (2-4 years) |

| Rise of Alternative Hair Removal Methods | -0.8% | North America and Europe leading, gradual spread to other regions | Long term (≥ 4 years) |

| Skin Sensitivity Issues | -0.4% | Global, with higher impact in regions with sensitive skin demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Low-Quality Products

The proliferation of counterfeit shaving products reached alarming levels, with US Customs and Border Protection reporting that 31% of intercepted counterfeit goods in FY 2023 were beauty-related, directly undermining brand trust and market value. E-commerce platforms inadvertently facilitate counterfeit distribution through inadequate verification systems, forcing legitimate manufacturers to invest heavily in brand protection, authentication technologies, and legal enforcement actions. Counterfeit products pose serious safety risks through substandard materials, inadequate quality control, and lack of regulatory compliance, potentially causing skin injuries that damage the entire category's reputation. The FDA's enhanced registration requirements under MoCRA (Modernization of Cosmetics Regulation Act) provide new tools for combating counterfeits but require significant industry investment in compliance systems and monitoring capabilities.

Skin Sensitivity Issues

Skin sensitivity issues are a significant factor restricting the growth of the shaving market. Many consumers experience irritation, razor burns, redness, and even allergic reactions after shaving, making the process uncomfortable and discouraging regular use of traditional shaving products. This discomfort often leads individuals to reduce the frequency of shaving or to avoid it altogether, especially if they have sensitive or reactive skin. Additionally, the negative experiences associated with skin sensitivity can erode brand loyalty, as consumers are more likely to experiment with different products or switch to brands that promise hypoallergenic or soothing formulations. Companies are compelled to invest in research and development to create gentler products, but this can increase costs and complicate product lines. The challenge for brands is to address these issues effectively while maintaining product efficacy and consumer trust. This ongoing struggle limits the potential for market expansion and poses a persistent obstacle to the sustained growth of the shaving industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electric Shavers Lead Innovation Drive

Electric shavers represent the fastest-growing product segment with a 4.72% CAGR forecast for 2025-2030, despite razors and blades maintaining market dominance with 38.22% share in 2024. This growth acceleration reflects technological convergence around AI-powered personalization, sustainable materials, and multi-functional designs that address evolving consumer preferences for convenience and performance. Philips' i9000 Series exemplifies this trend with AI-driven cutting power adjustment and UV cleaning capabilities, while Panasonic's Palm Shaver introduces sustainable NAGORI materials reducing plastic usage by 40%. Traditional razors and blades maintain their position through continuous innovation in blade technology, ergonomic improvements, and premium positioning.

Trimmers and clippers benefit from the broader grooming consciousness trend, particularly in beard styling and body grooming applications that complement traditional shaving routines. Shaving creams, gels, and foams face pressure from waterless and sustainable alternatives, driving reformulation toward natural ingredients and eco-friendly packaging solutions. Pre- and after-shave lotions experience renewed interest as consumers adopt comprehensive grooming routines influenced by social media education and dermatological awareness. The segment's evolution toward integrated ecosystems creates cross-selling opportunities for manufacturers offering complete grooming solutions rather than standalone products.

By Price: Premium Segment Drives Value Creation

The premium segment's 5.21% CAGR growth significantly outpaces overall market expansion, while the mass segment maintains 79.82% market share in 2024, reflecting consumer bifurcation between value-seeking and quality-focused purchasing behaviours. Premium products command higher margins through advanced features, sustainable materials, and brand prestige, enabling manufacturers to invest in research and development and marketing initiatives that further differentiate their offerings. Mass market products face increasing pressure from private label alternatives and counterfeit goods, forcing manufacturers to emphasize value proposition through improved performance and competitive pricing strategies.

The premiumization trend extends beyond product features to packaging sustainability, with Gillette's 100% plastic-free packaging initiative targeting environmentally conscious consumers willing to pay premium prices for sustainable solutions. Economic volatility creates headwinds for premium segment growth in price-sensitive markets, but demographic shifts toward younger, higher-income consumers support long-term expansion potential. Subscription models and direct-to-consumer channels enable premium brands to build customer relationships and justify higher prices through personalized experiences and convenience benefits.

By End User: Female Segment Emerges as Growth Engine

Female consumers drive the highest growth rate at 5.34% CAGR for 2025-2030, despite males maintaining 81.24% market share in 2024, reflecting significant untapped potential in women's grooming products and intimate care solutions. Philips' OneBlade Intimate launch as a unisex shaver addresses this opportunity by targeting pubic and underarm grooming needs previously underserved by traditional products. The female segment's growth stems from increased workforce participation, social media influence, and evolving beauty standards that normalize body hair removal across diverse demographics and age groups. According to Bureau of Labor Statistics, the employment rate of women in the United States rose from 53.2% in 2021 to 55.2% in 2024 [1]Source: Bureau of Labor Statistics, "Employment rate of women in the United States", www.bls.gov. Product development increasingly focuses on ergonomic designs, gentle formulations, and discreet packaging that address women's specific needs and preferences.

Male grooming consciousness continues expanding beyond traditional shaving to comprehensive skincare routines, with 68% of US Gen Z men using facial skincare products in 2024, creating opportunities for integrated product offerings. The gender-neutral trend in grooming products challenges traditional marketing approaches, requiring brands to develop inclusive messaging and product designs that appeal to diverse consumer identities. Subscription services and personalized recommendations enable brands to better serve both segments through tailored product selections and educational content.

By Distribution Channel: Digital Transformation Accelerates

Online retail stores achieve the highest growth rate at 5.67% CAGR for 2025-2030, while supermarkets and hypermarkets maintain 35.22% market share in 2024, reflecting the ongoing digital transformation of consumer shopping behaviors. Digital channels enable direct-to-consumer brands to bypass traditional retail margins and build customer relationships through personalized experiences and educational content. The COVID-19 pandemic accelerated online adoption, with consumers becoming comfortable purchasing personal care products without physical inspection, particularly for replenishment purchases of familiar brands. Increase in number of smartphone users has significantly contributed to the digital demand. According to GSMA (Groupe Spécial Mobile Association), the global smartphone penetration rate as share of population rose from 68% in 2022 to 71% in 2024[2]Source: GSMA (Groupe Spécial Mobile Association), "Smartphone penetration rate", gsma.com

Convenience and grocery stores benefit from impulse purchasing and emergency replacement needs, while traditional retail channels adapt through omnichannel strategies that integrate online and offline experiences. The rise of subscription models, demonstrates consumer preference for convenient, predictable grooming product delivery. Other distribution channels, including specialty stores and direct sales, face pressure from digital alternatives but maintain relevance for premium products requiring demonstration and consultation. The channel evolution creates opportunities for brands to optimize distribution strategies based on product positioning and target demographics.

Geography Analysis

Asia-Pacific simultaneously commands the largest market share at 33.04% in 2024 and the fastest growth rate at 5.03% CAGR for 2025-2030, driven by urbanization, rising disposable incomes, and evolving grooming consciousness among younger demographics. China's premiumization trend drives demand for advanced electric shavers and sustainable packaging solutions, while Japan's mature market focuses on precision engineering and quality differentiation. The region's manufacturing capabilities and cost advantages enable local brands to compete effectively against international players, particularly in price-sensitive segments where value proposition remains paramount.

North America and Europe represent mature markets with established grooming habits and premium product adoption, but face headwinds from economic volatility and market saturation in traditional segments. These regions lead in sustainability initiatives and regulatory compliance, with European consumers particularly responsive to eco-friendly packaging and natural ingredient formulations, as demonstrated by Gillette's 100% plastic-free packaging initiative targeting 2030 recyclability goals. The FDA's Modernization of Cosmetics Regulation Act (MoCRA) effective July 2024 strengthens safety requirements in North America, potentially creating competitive advantages for established manufacturers with robust quality systems while raising barriers for smaller entrants.

Middle East and Africa, along with South America, present emerging opportunities with growing middle-class populations and increasing exposure to global grooming trends through social media and international brand expansion. These regions exhibit significant potential for market penetration as urbanization accelerates and disposable incomes rise, particularly among younger demographics influenced by Western grooming standards and social media beauty trends. Brazil and Argentina lead South American growth through established retail infrastructure and consumer acceptance of premium grooming products, while Gulf Cooperation Council countries drive Middle Eastern expansion through high per-capita incomes and luxury product preferences. The geographic diversity requires localized product development, pricing strategies, and distribution approaches that account for cultural preferences, regulatory requirements, and economic conditions specific to each market.

Competitive Landscape

The shaving market exhibits moderate concentration, indicating established multinational corporations maintain significant market positions while facing intensifying pressure from direct-to-consumer brands and alternative hair removal technologies. Edgewell Personal Care's Schick and Wilkinson Sword brands compete through technological differentiation and regional market focus, while Koninklijke Philips maintains leadership in electric shavers through AI-powered innovations like the i9000 Series. Market leaders invest heavily in research and development and manufacturing capabilities to maintain technological advantages and economies of scale that smaller competitors cannot easily replicate.

Technology integration becomes a key differentiator, as evidenced by Philips' AI-powered personalization features and Panasonic's sustainable material innovations that create barriers to entry for smaller competitors lacking research and development capabilities. Direct-to-consumer brands disrupt traditional distribution models by building customer relationships through social media marketing and subscription convenience, forcing established players to develop omnichannel strategies and acquire innovative competitors. Patent filings in smart shaving technologies and sustainable materials indicate continued innovation focus, with companies seeking to protect intellectual property advantages in premium segments where differentiation commands higher margins.

Opportunities emerge in underserved segments like intimate grooming, sustainable packaging solutions, and personalized subscription services that address specific consumer needs traditional mass-market approaches cannot efficiently serve. Philips' OneBlade Intimate launch as a unisex shaver demonstrates how established players can capture new market segments through targeted product development and inclusive marketing strategies. Emerging disruptors focus on natural ingredients, viral marketing, and direct-to-consumer models that bypass traditional retail margins while building authentic customer relationships through social media engagement. Counterfeit products pose significant challenges, with 31% of intercepted counterfeit goods being beauty-related, forcing legitimate manufacturers to invest in brand protection technologies and authentication systems.

Shaving Industry Leaders

-

Koninklijke Philips N.V.

-

Conair LLC

-

Wahl Clipper Corporation

-

Panasonic Holdings Corporation

-

The Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: GilletteLabs introduced NFL-Licensed razors featuring team designs. The Official NFL Licensed Razors featured the team colors and logos of 12 NFL teams, available at select retailers throughout the 2025 season. The collection showcased 12 distinct GilletteLabs designs, incorporating the iconic team colors and signature marks of established NFL franchises.

- May 2025: BIC, a global leader in shaving innovation, launched its new BIC Flex 5 Sensitive, a men's razor designed to tackle sensitive skin with precision and comfort. Clinically proven for sensitive skin, this dermatologist-tested razor featured five long-lasting blades for an ultra-close, effortless shave, for clearing away those cold-weather beards and other seasonally neglected zones.

- May 2025: Harry's, the men's grooming brand, unveiled Harry's Plus, its new, next generation razor system, and the most significant launch in the brand's history. Harry's Plus is a whole new razor system with an advanced pivoting cartridge that effortlessly adapts to the contours of the face, 5 German-engineered blades that shaved progressively closer to the skin, a lubricating strip with aloe for enhanced smoothness, and an ergonomic metal handle.

Global Shaving Market Report Scope

| Razors and Blades |

| Electric Shavers |

| Trimmers and Clippers |

| Shaving Creams, Gels and Foams |

| Pre- and After-shave Lotions |

| Mass |

| Premium |

| Male |

| Female |

| Supermarkets and Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Razors and Blades | |

| Electric Shavers | ||

| Trimmers and Clippers | ||

| Shaving Creams, Gels and Foams | ||

| Pre- and After-shave Lotions | ||

| By Price | Mass | |

| Premium | ||

| By End User | Male | |

| Female | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the shaving products market?

The shaving products market was valued at USD 24.52 billion in 2025 and is projected to reach USD 29.14 billion by 2030.

Which region leads the shaving products market?

Asia-Pacific commanded the largest 33.04% share in 2024 and is also the fastest-growing region with a 5.03% CAGR to 2030.

What product segment is growing fastest?

Electric shavers show the highest momentum, registering a 4.72% CAGR for the 2025-2030 period.

How are online channels impacting sales?

Online retail, growing at a 5.67% CAGR, is reshaping purchasing habits through subscription bundles and algorithm-driven recommendations.

Page last updated on: