Sesame Seed Market Size and Share

Sesame Seed Market Analysis by Mordor Intelligence

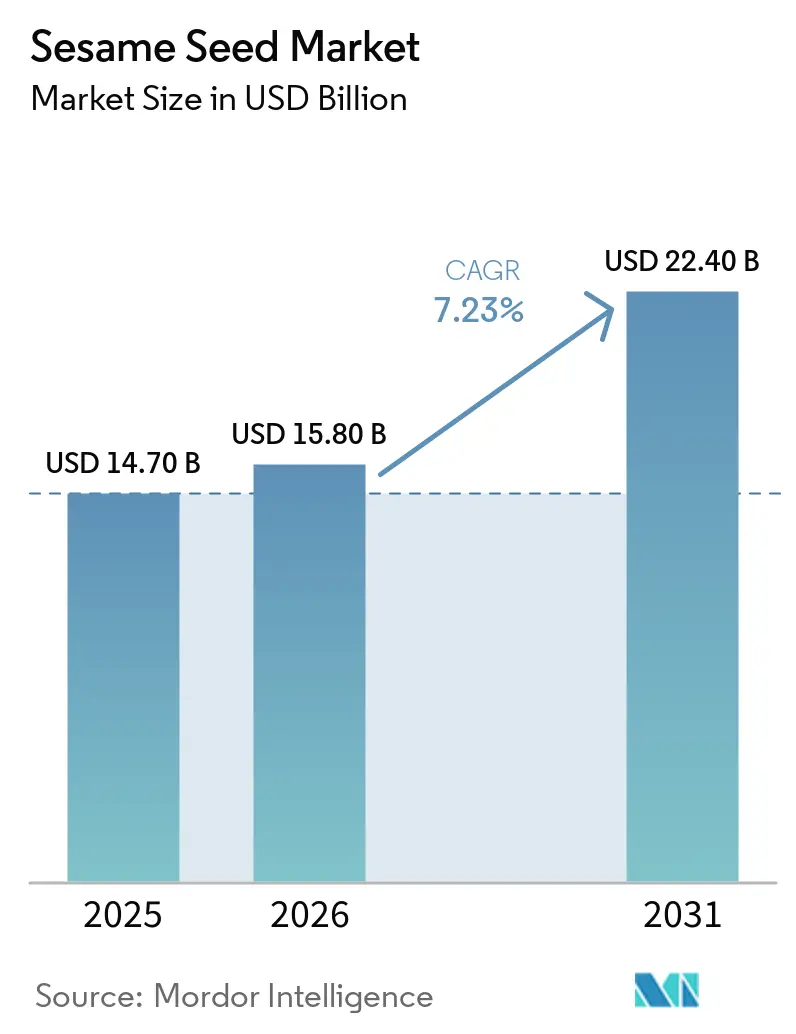

The sesame seed market size is projected to grow from USD 14.70 billion in 2025 to USD 15.80 billion in 2026 and is forecast to reach USD 22.40 billion by 2031 at a 7.23% CAGR over 2026-2031. Momentum comes from shifting protein-sourcing strategies, premiumization in ethnic cuisines, and tightening food-safety regulations that reward traceable supply chains. China continues to anchor processing demand, while Africa supplies most raw seed yet captures limited downstream value. Aflatoxin limits in the European Union and Japan have accelerated investments in pre-shipment testing, and freight disruptions on the Red Sea route highlight logistics risk. Despite these challenges, the sesame seed market benefits from rising plant-based protein usage in food and cosmetics, genome-edited drought-tolerant cultivars, and the roll-out of blockchain traceability that unlocks price premiums.

Key Report Takeaways

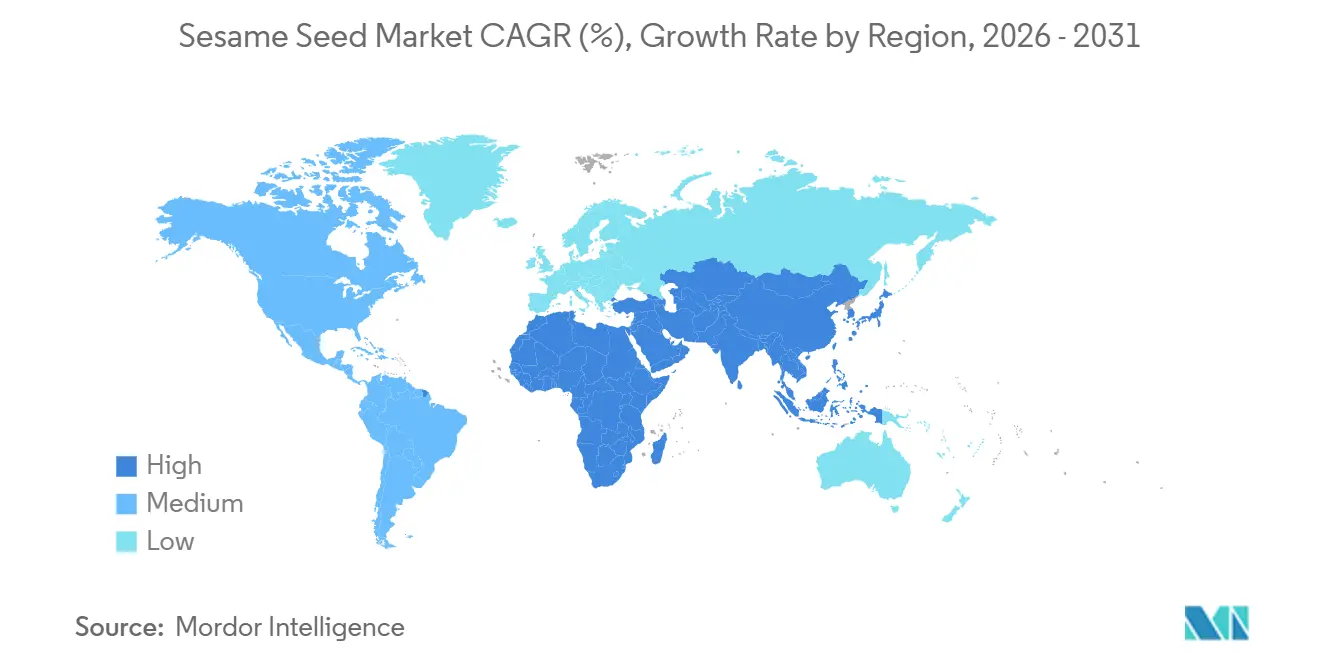

- By geography, Asia-Pacific led with 46.0% of the sesame seed market share in 2025, while Africa registered the fastest 9.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sesame Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for plant-based proteins | +1.2% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Expanding premiumization in ethnic foods | +0.8% | North America, Europe, Middle East, and urban Asia-Pacific | Medium term (2-4 years) |

| Trade liberalization in key importing nations | +0.6% | Asia-Pacific importers and African exporters | Short term (≤ 2 years) |

| Genome-edited drought-tolerant cultivars | +0.5% | Africa, India, and Myanmar | Long term (≥ 4 years) |

| AI-enabled origin traceability platforms | +0.4% | Global with early European Union and Japan uptake | Medium term (2-4 years) |

| Growth of halal-certified supply chains | +0.7% | Middle East, Southeast Asia, and Muslim-majority regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Plant-Based Proteins

Sesame and tahini provide complete-protein alternatives in vegan and vegetarian products, and tahini boasts 17 grams of protein per 100 grams [1]Source: United States Department of Agriculture, “FoodData Central,” usda.gov.Consumer preference for allergen-friendly formulations that avoid soy has lifted tahini inclusion in ready-to-eat spreads and meal-replacement beverages. Regulatory clarity from the Food and Drug Administration (FDA) and the European Union (EU) Novel Food pathway simplifies new-product launches, drawing multinational brands to contract schemes in Tanzania and Ethiopia that guarantee steady seed volumes. Foodservice margins also benefit as hummus and sesame-protein snacks migrate from niche to mainstream restaurant menus across urban North America and Europe.

Expanding Premiumization in Ethnic Foods

Authentic Middle Eastern and Asian dishes command premiums in retail and foodservice, with single-origin sesame from Kumamoto Prefecture in Japan retailing 40% above commodity grade. Gulf Cooperation Council consumers demand halal-certified tahini, creating volume pull for audited supply chains[2]Source: Islamic Food and Nutrition Council of America, “Halal Certification Standards,” ifanca.org. In personal care, Korean and Japanese brands promote sesame oil’s traditional heritage to justify selling prices 30% higher than synthetic emollients. Vertical integration and certification investment allow exporters to capture these premiums and lift the sesame seed market.

Trade Liberalization in Key Importing Nations

China trimmed sesame seed import tariffs in 2024, boosting sesame shipments in the following year. Japan now clears compliant Ethiopian and Tanzanian seed in three days, down from seven, under new partnership agreements. South Korea’s duty elimination on Indian sesame oil opened a USD 50 million annual lane. These moves lower landed costs and redirect trade flows toward African and South Asian origins, able to provide certificates of preferential origin.

AI-Enabled Origin Traceability Platforms

IBM Food Trust pilots in Ethiopia and Tanzania link GPS-tagged farm plots with pesticide test results, satisfying the European Union Deforestation Regulation that became effective in 2025. AI image recognition already screens seed for variety compliance and aflatoxin risk, cutting testing costs by 20% to 30%. Certified lots command price uplifts that flow back to farmers participating in digitized networks, raising the overall value captured within the sesame seed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile freight and container costs | -0.9% | Africa, the Middle East, and South Asia | Short term (≤ 2 years) |

| Stringent maximum residue limits in the European Union and Japan | -0.7% | Exporters to North America and Europe | Medium term (2-4 years) |

| Fragmented smallholder supply base | -0.6% | Africa–Europe and Africa–North America trade lanes | Long term (≥ 4 years) |

| Climate-driven aflatoxin outbreaks | -0.8% | Commercial farms worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Freight and Container Costs

Red Sea rerouting in 2024 and 2025 increased voyage times by up to two weeks and pushed 40-foot container spot rates from USD 2,500 to USD 3,800 on Africa-to-Asia lanes. The Suez Canal Authority also raised tolls by 15% in January 2025 [3]Source: Suez Canal Authority, “Transit Statistics and Tariffs,” suezcanal.gov.eg. Export margins narrowed, particularly for smallholder-sourced shipments aggregated through freight forwarders, while unpredictable shipping costs are discouraging investment in local processing facilities, reinforcing Africa’s role as a raw-material supplier rather than a value-added processor.

Fragmented Smallholder Supply Base

Most sesame farms in Africa, India, and Myanmar are under 2 hectares, leading to widely varying moisture levels, foreign-matter content, and aflatoxin risk at aggregation points. Contract farming and cooperatives cover less than 20% of the planted area, and governance challenges and limited access to working capital further constrain their scale. This fragmentation limits processors’ ability to secure a consistent supply of feedstock for mechanized hulling or oil extraction, keeping value-addition concentrated with multinational traders while smallholders earn primarily commodity prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Asia-Pacific held 46.0% of the sesame seed market value in 2025, fueled by China’s 900,000-metric-ton import requirement and Japan’s significant consumption. Chinese crushers convert seed into oil for domestic use and for re-export across Southeast Asia. Japan values mechanically hulled, visually uniform seed, rewarding exporters that invest in optical sorters and strict moisture control. South Korea’s market splits between low-cost refined oil and artisanal cold-pressed oil, showing consumer willingness to pay for origin certification.

Africa records the fastest 9.8% CAGR through 2031. Tanzania is a leading exporter and offers tax incentives for new hulling and crushing plants. Ethiopia has restored production and uses warehouse-receipt finance to improve liquidity for smallholders. Nigeria positions itself as a West African processing hub, yet suffers from inconsistent electricity and high inland freight costs. Sudan remains the largest grower but faces declining yields due to irrigation infrastructure decay and civil insecurity.

North America and Europe are steady net importers. The United States sources sesame primarily for tahini production and bakery toppings. European buyers enforce the EU Deforestation Regulation, shifting sourcing toward traceable Tanzanian and Ethiopian seed. The Middle East commands high-value demand for halal-certified tahini and hulled seed, with Gulf Cooperation Council consumption at more than 2 kilograms per capita annually. South America remains minor, with Paraguay and Bolivia serving regional consumption.

Mordor Intelligence provides coverage of the sesame seed market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Olam International, Cargill Inc., and Archer Daniels Midland together accounted for the majority of traded volumes of sesame seed in 2025. Their vertical integration into origin-country hulling facilities in Ethiopia and Tanzania secures supply and reinforces traceability. Cargill Inc. finances cooperatives in Tanzania to lock in forward contracts, while Archer Daniels Midland acquired a supercritical CO2 extraction plant in Gujarat to supply cosmetics-grade oil to Western brands.

Regional competitors such as Dipasa in West Africa and Selet Hulling in Ethiopia leverage proximity to farms and cooperative relationships but face working-capital constraints that limit scale. Wilmar International signed a memorandum with Nigeria to build a crushing complex in Kano, contingent on infrastructure upgrades. Technology adoption is rising, with AI image recognition cutting laboratory costs at collection centers by up to 30%. Certifications in halal and organic further separate integrated traders from fragmented local exporters as regulatory scrutiny tightens.

Emerging farmer cooperatives in Tanzania and Ethiopia use warehouse-receipt finance to bypass middlemen, improving price realization. However, liquidity on the Ethiopian Commodity Exchange sesame contract launched in 2024 remains limited. Sustainability mandates such as the European Union Deforestation Regulation create a compliance moat for early adopters that invest in satellite monitoring and GPS farm mapping.

Recent Industry Developments

- November 2025: The International Fund for Agricultural Development (IFAD), Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF), Euglena, and Grameen Euglena have initiated a project in Bangladesh aimed at supporting small-scale sesame farmers. The project focuses on enhancing seed quality and providing high-grade sesame to Japanese companies through a social procurement model.

- September 2025: Olam Agri signed a Memorandum of Understanding (MoU) with Kadoya Sesame Mills, the International Fund for Agricultural Development (IFAD), and MC Agri Alliance during TICAD 9 to assist Nigerian smallholder sesame farmers in enhancing productivity, quality, and sustainability.

- October 2024: Tanzania is developing a cashew processing industrial park in Mtwara, which will also feature facilities for sesame processing. This initiative aims to enhance the value of local crops and promote agro-industrial development.

Global Sesame Seed Market Report Scope

Sesame seeds are small, flat, oil-rich seeds from the Sesamum indicum plant, widely used in cooking, baking, and oil extraction. The Sesame Seed Market Report is Segmented by Geography (North America, Europe, Asia-Pacific, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecasts, List of Key Players, Logistics and Infrastructure, Regulatory Framework, and Seasonality Analysis. The Market forecasts are provided in value (USD) and volume (Metric tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Bolivia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Paraguay | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Bolivia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Paraguay | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the current value of the sesame seed market?

The sesame seed market size stands at USD 15.8 billion in 2026.

How fast is the sesame commodity market is anticipated to grow?

The market is forecast to post a 7.23% CAGR, reaching USD 22.40 billion by 2031.

What are the primary challenges facing exporters?

Key headwinds include volatile container freight costs, stringent aflatoxin limits in the European Union and Japan, and climate-driven contamination risks.

Which region contributes the most to sesame seed value?

Asia-Pacific holds 46.0% of market value, driven by China’s large crushing sector.

Page last updated on: