Tanzania Grains Market Analysis by Mordor Intelligence

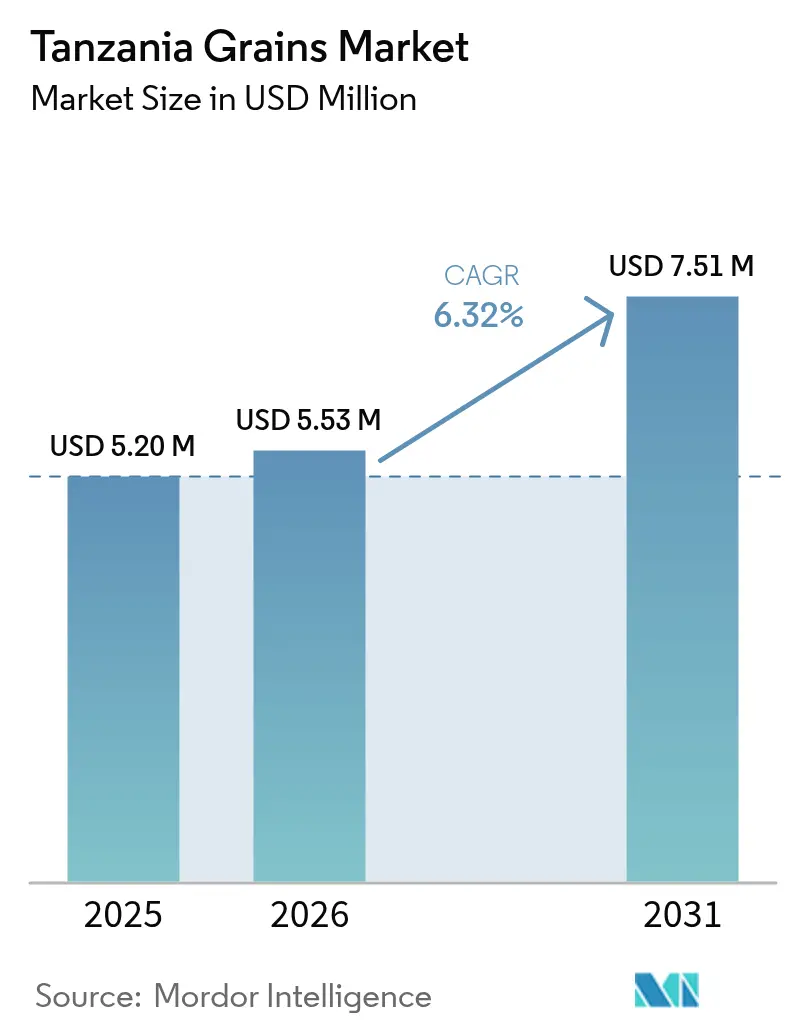

Tanzania grains market size in 2026 is estimated at USD 5.53 million, growing from 2025 value of USD 5.20 million with 2031 projections showing USD 7.51 million, growing at 6.32% CAGR over 2026-2031. Robust public buying programs, expanded fertilizer subsidies, and widening contract-farming models position the market for sustained expansion, even as storage gaps and credit constraints temper price realization. Brewer-led contract farming now absorbs 17,000 metric tons of barley and sorghum each year, embedding quality standards and predictable pricing into formerly fragmented chains. Warehouse-receipt financing is unlocking working capital for smallholders, although climate volatility remains a headwind, with the United States Department of Agriculture (USDA) indicating a dip in 2025/26 maize output.

Key Report Takeaways

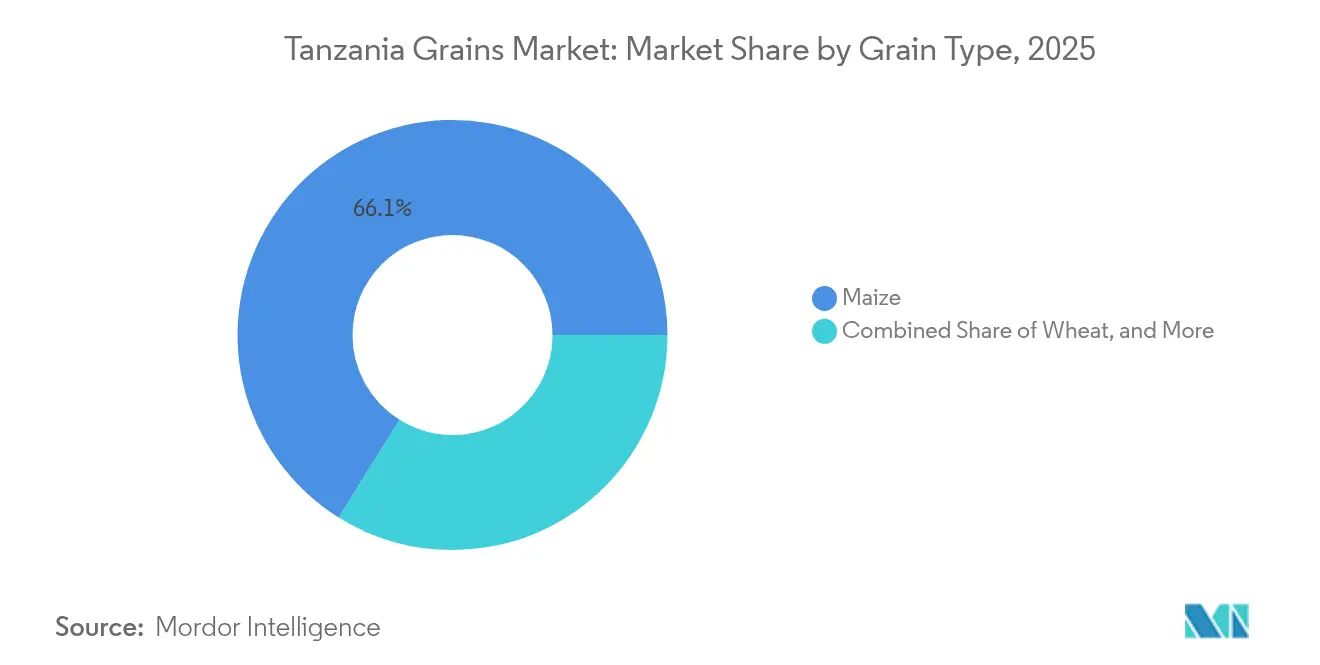

- By grain type, maize led with 66.12% of the Tanzania grains market share in 2025. Wheat is forecast to expand at a 7.78% CAGR from 2026 to 2031, the fastest among all grain categories.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Tanzania Grains Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of cereal-based foods | +1.2% | National, concentrated in Dar es Salaam, Mwanza, and Arusha | Medium term (2-4 years) |

| Government initiatives for staple-crop self-sufficiency | +1.4% | National, emphasis on the Southern Highlands and Lake Zone | Long term (≥ 4 years) |

| Growing demand for animal feed | +0.9% | National, strongest in peri-urban dairy and poultry clusters | Medium term (2-4 years) |

| Expanding adoption of warehouse-receipt financing | +0.6% | National, early gains in Dodoma, Singida, and Iringa | Long term (≥ 4 years) |

| Contract farming by beverage companies | +0.5% | Northern Highlands (Manyara, Karatu, and Monduli) | Short term (≤ 2 years) |

| Climate-resilient seed varieties uptake | +0.8% | National priority in semi-arid zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Cereal-Based Foods

Urban population growth and dietary changes are lifting per-capita cereal intake. A 66% increase in national cereal output between the 2022/23 and 2023/24 seasons was largely absorbed domestically, resulting in smaller exportable surpluses [1]Source: Ministry of Agriculture Tanzania, “Crop Production Report 2023/24,” moa.go.tz. The mandatory fortification of maize and wheat flour, effective March 2025, addresses micronutrient deficiencies that affect 33% of children under five and 37% of women of reproductive age, thereby anchoring fortified products in school feeding programs [2]Source: Tanzania Food and Drugs Authority, “Food Fortification Regulations 2025,” tfda.go.tz. Rice prices in Dar es Salaam increased from USD 0.82 per kilogram in April 2022 to USD 0.86 per kilogram in February 2025, underscoring steady urban demand. The alignment of nutrition policy, urbanization, and income gains keeps processed grains in consumer baskets.

Government Initiatives For Staple-Crop Self-Sufficiency

The maize procurement target of 700,000 metric tons for the fiscal year 2024/25 aims to stabilize prices and support smallholder farmers' incomes. In January 2025, the National Food Reserve Agency procured 72,000 metric tons, utilizing regional aggregators to distribute funds. The fertilizer subsidies amounting to TZS 151 billion (USD 58 million) in 2024 contributed to increased yields in the Southern Highlands and Lake Zone. Additionally, the agriculture budget has tripled over four years, reaching TZS 1.379 trillion (USD 530 million). The Food Self-Sufficiency Ratio stood at 128 in 2023/24, and the storage capacity remains limited to 360,000 metric tons, significantly below the target of 3 million metric tons. This shortfall leads to local surpluses, exerting downward pressure on prices and encouraging unrecorded exports.

Growing Demand For Animal Feed

Livestock intensification reshapes grain demand. The World Bank estimates that USD 546 million is needed to modernize Tanzania’s cattle, poultry, and dairy value chains, which support 36.6 million heads of cattle. Commercial fish-feed output jumped from 1,182 metric tons in 2021 to 6,211 metric tons in 2023, although 74% of raw materials are still imported, exposing feed millers to currency swings. Breweries source 17,000 metric tons of local grains annually under fixed-price contracts, signaling structured off-take that ripples upstream. Demand from dairy, poultry, and aquaculture clusters in Dar es Salaam, Mwanza, and Arusha is set to grow.

Expanding Adoption of Warehouse-Receipt Financing

The Tanzania Mercantile Exchange now accepts maize and rice warehouse receipts, allowing stored grain to secure short-term loans. A Memorandum of Understanding (MoU) signed in 2024 with Zambia, Malawi, and Zimbabwe harmonizes standards and lowers lender risk. The United States Agency for International Development (USAID) and the Eastern Africa Grain Council launched a three-year program that positions Tanzania as a surplus supplier to Kenya using the same instrument. The World Bank’s USD 95 million Financial Sector Transformation and Growth Project channels lines of credit through local banks, and digital reverse-factoring tools aim to reach 1,000 agribusinesses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Incidence of pests and diseases | -0.7% | National, acute in maize belt and rice-growing zones | Short term (≤ 2 years) |

| Limited access to affordable credit | -0.5% | National, pronounced in smallholder regions | Medium term (2-4 years) |

| Post-harvest storage losses | -0.6% | National, the highest in remote districts | Medium term (2-4 years) |

| Weather-induced production volatility | -0.4% | National, concentrated in semi-arid and rain-fed areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Incidence of Pests and Diseases

The Fall Armyworm reduces maize yields by up to 54%, while aflatoxin levels have spiked to 162.40 µg/kg in some districts, exceeding the 10 µg/kg East African ceiling [3]Source: Food and Agriculture Organization, “Aflatoxin Surveillance in East Africa,” fao.org. Tanzania lies within the maize lethal necrosis belt, where dual infections drain USD 291-339 million from East African output annually. The Larger Grain Borer consumes 20-50% of grain in traditional stores, although hermetic bags curb losses and are scaling up under donor funding. Resistant hybrids and biocontrol agents such as Telenomus remus are spreading, yet adoption is incomplete, shaving 0.7% points off growth in the short term.

Limited Access to Affordable Credit

Morogoro research suggests credit could raise yields by 15.09%, but 17% interest rates under the Small Industries Development Organization (SIDO) Credit Guarantee Scheme still deter uptake. The African Development Bank’s USD 129.71 million youth agribusiness loan and the United States Agency for International Development (USAID) are USD 83 million corporate support skew toward established players, leaving smallholders underserved. VisionFund enrolled 7,000 farmers in bundled credit-insurance pilots covering 21,000 hectares, but has not reached scale. This funding gap reduces growth until digital lending and receipt-based finance expand their outreach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grain Type: Maize Dominance Masks Wheat’s Import-Substitution Surge

Maize anchors demand with 66.12% of the Tanzania grains market share in 2025. The Ministry of Agriculture logged a large volume of maize in the 2023/24 season, driven by subsidies and favorable rainfall. The government’s 700,000 metric ton procurement target signals ongoing policy support, even as spot prices remain the lowest in East Africa. Drought-tolerant hybrids sustain yields and raise export competitiveness, strengthening the Tanzania grains market.

A faster-growing wheat segment posts an 7.78% CAGR forecast through 2031, although current output is only 80,000 metric tons. A USD 40 million Moshi malting plant now demands 25,000 metric tons of local barley each year, a seven-fold jump on historic volumes. Excise incentives and heat-tolerant varieties that mature in 90 days help shorten the import gap and underscore wheat’s role in future Tanzania grain market size expansion. Rice output remains steady at 2.51 million metric tons milled, backed by Direct-Seeded Rice, while sorghum and millet occupy drought-resilient niches and anchor regional exports.

Geography Analysis

Production clusters in the Southern Highlands, specifically Iringa, Mbeya, and Rukwa, supply maize and wheat to the domestic market. The Lake Zone, Mwanza, Shinyanga, and Kagera regions add maize and rice, while Morogoro and Kilombero in the coastal plains focus on rice cultivation. A Food Self-Sufficiency Ratio of 128 in 2023/24 confirms net-export status within the East African Community. Kenya’s maize imports from Tanzania decreased in 2022/23 following export curbs, illustrating the policy swings that shape the Tanzanian grains market.

In 2024, the Tanzania Mercantile Exchange integrated its warehouse-receipt systems with those of Zambia, Malawi, and Zimbabwe, enabling cross-border settlements that mitigate lender risk and enhance liquidity. The Northern Highlands districts, including Manyara, Karatu, and Monduli, are becoming key centers for barley production through contract farming, promoting regional specialization. Urban centers such as Dar es Salaam, Mwanza, and Arusha drive demand, with rice prices remaining at USD 0.86 per kg in 2025, indicating a stable value chain that supports the growth of the Tanzania grains market.

Remote districts still lose up to 50% of stored grain to pests and moisture. Hermetic bags and metal silos are gaining popularity, supported by donor distributions. Uneven adoption continues to keep post-harvest losses high. Government plans to hit 3 million metric tons of storage by 2030 aim to reduce volatility and promote formal trading, stabilizing the Tanzania grains market size.

Competitive Landscape

The Tanzania grains market exhibits moderate concentration. Thousands of community mills still supply local zones, but March 2025 fortification rules threaten to halve their number by December 2025, channeling volume toward capitalized incumbents that can finance dosifier upgrades. Bakhresa budgeted USD 500 million for a new Dar es Salaam soft-drinks and malt line, set to be operational in 2026, signaling revenue diversification and capacity expansion. Mohamed Enterprises added rail-linked grain silos in Dodoma in 2024, increasing storage capacity to 120,000 metric tons and reducing inland freight by 18%. National Milling, meanwhile, automated its Dar es Salaam plant in mid-2025, lifting wheat-flour output by 15% without expanding floor space.

Opportunities for growth are focused on warehouse-receipt financing and contract farming. In 2024, the Tanzania Mercantile Exchange signed a memorandum of understanding with regional platforms in Zambia, Malawi, and Zimbabwe to harmonize standards and facilitate cross-border trading. This initiative aims to reduce counterparty risk for lenders and improve liquidity for smallholders. Tanzania Breweries and Serengeti Breweries collectively procure 17,000 metric tonnes of grains annually through contract-farming arrangements, incorporating quality specifications that influence upstream seed and agrochemical markets. Additionally, in April 2024, the International Finance Corporation approved a contract-farming framework designed to mitigate risks for smallholder participation.

Digital matchmaking platforms such as the Micro, Small, and Medium Enterprises (MSME) Financing Gateway enlisted 40 lenders and 20 advisers in November 2024, creating a pipeline for millers that need working capital to meet fortification and storage norms. Serengeti Breweries mirrored the model in 2025 by scaling sorghum purchases under floor-price agreements, providing revenue certainty that shores up upstream seed and fertilizer demand. These strategic moves, plus tightening regulation and fintech innovation, are gradually raising entry barriers and nudging the sector toward a moderately consolidated structure.

Recent Industry Developments

- August 2024: The National Food Reserve Agency (NFRA) purchased 55,000 metric tons of cereal crops from various traders in its Dar es Salaam-based Kipawa zone. The procurement comprised 20,000 metric tons of paddy and 35,000 metric tons of maize, sourced from large-scale traders and cooperative societies that aggregate produce from farmers.

- June 2023: The Cereals and Other Produce Board of Tanzania invested USD 42.4 million to procure key cereal crops from farmers across the country. This initiative seeks to transform the agricultural scene, especially in cereal cultivation and trade, with a focus on enhancing farmers' incomes.

- July 2022: The African Development Bank Group approved USD 73.5 million to boost food production in Tanzania. The funds strengthen the supply of improved wheat, and rice seeds that are climate resilient, ensure fertilizer availability and affordability, and support policies that enhance the regulatory environment for the rapid uptake of certified seeds and fertilizers.

Tanzania Grains Market Report Scope

Cereal crops are small, hard, and edible dry seeds that grow on grass-like plants and are cultivated for their digestible constituents and a botanical structure that comprises the bran, endosperm, and germ. Tanzania Cereals Market is segmented into Types (Maize, Rice, Sorghum, Wheat, and Other Cereals). The study covers Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The report offers market estimation and forecasts in Value (USD Million) and Volume (Metric Tons).

By Grain Type

| Maize | Production Analysis (Volume) |

| Consumption Analysis (Value and Volume) | |

| Import Analysis (Value and Volume) | |

| Export Analysis (Value and Volume) | |

| Price Trend Analysis | |

| Rice | Production Analysis (Volume) |

| Consumption Analysis (Value and Volume) | |

| Import Analysis (Value and Volume) | |

| Export Analysis (Value and Volume) | |

| Price Trend Analysis | |

| Sorghum | Production Analysis (Volume) |

| Consumption Analysis (Value and Volume) | |

| Import Analysis (Value and Volume) | |

| Export Analysis (Value and Volume) | |

| Price Trend Analysis | |

| Wheat | Production Analysis (Volume) |

| Consumption Analysis (Value and Volume) | |

| Import Analysis (Value and Volume) | |

| Export Analysis (Value and Volume) | |

| Price Trend Analysis | |

| Other Cereals | Production Analysis (Volume) |

| Consumption Analysis (Value and Volume) | |

| Import Analysis (Value and Volume) | |

| Export Analysis (Value and Volume) | |

| Price Trend Analysis |

| By Grain Type | Maize | Production Analysis (Volume) |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Rice | Production Analysis (Volume) | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Sorghum | Production Analysis (Volume) | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Wheat | Production Analysis (Volume) | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

| Other Cereals | Production Analysis (Volume) | |

| Consumption Analysis (Value and Volume) | ||

| Import Analysis (Value and Volume) | ||

| Export Analysis (Value and Volume) | ||

| Price Trend Analysis | ||

Key Questions Answered in the Report

What is the 2026 value of the Tanzania grains market?

The market stands at USD 5.53 million in 2026 and is projected to reach USD 7.51 million by 2031.

Which grain holds the largest share?

Maize accounts for 66.12% of Tanzania grains market share in 2025.

What growth rate is projected for wheat?

Wheat is forecast to post an 7.78% CAGR between 2026 and 2031.

How will the fortification rule affect small mills?

More than 3,000 small mills must install micronutrient dosifiers by December 2025 or exit, pushing volume toward compliant operators.

Why is warehouse-receipt financing important?

It lets farmers pledge stored grain for loans, improving cash flow and reducing the need for distress sales.

What climate-smart seeds are available?

DroughtTEGO maize hybrids and heat-tolerant wheat lines yield better under stress and are scaling through public-private trials.

Page last updated on: