China Shrimp Market Analysis by Mordor Intelligence

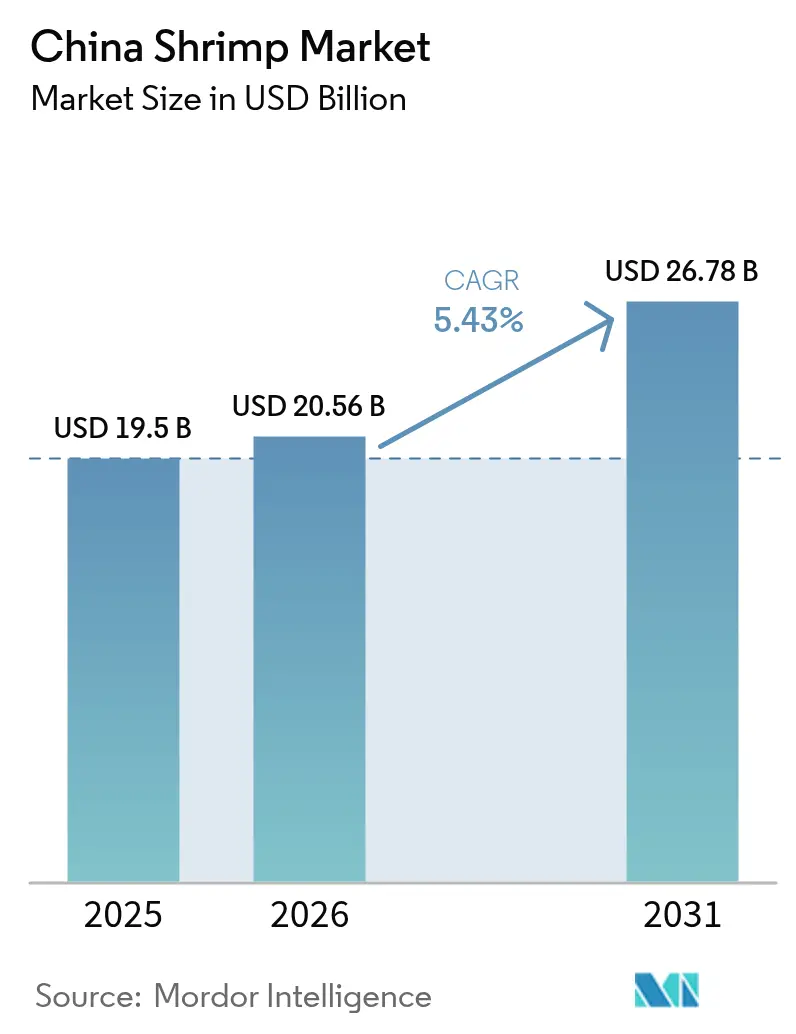

The China shrimp market size is expected to grow from USD 19.5 billion in 2025 to USD 20.56 billion in 2026 and is forecast to reach USD 26.78 billion by 2031 at 5.43% CAGR over 2026-2031. This growth is attributed to rising household spending, advancements in cold-chain infrastructure, and the adoption of recirculating aquaculture systems. However, low-cost imports from Ecuador are constraining pricing power. Domestic production is supported by innovations such as advanced greenhouse technology and solar-aquaculture hybrids, which are enhancing yields and addressing the challenges posed by coastal land-use restrictions on pond expansion. Urban consumers' preference for shrimp as a lean, health-conscious protein continues to drive demand. Conversely, stricter discharge regulations and recurring disease outbreaks are increasing production costs, leading small-scale producers to either consolidate operations or exit the market.

Key Report Takeaways

- By trade flow, Ecuadorian shrimp led with 65.74% of the China shrimp market share in frozen import volume during 2025, while India-origin shipments are forecast to grow at 7.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Shrimp Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income and preference for lean protein | +1.2% | National, strongest in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Government incentives for modern recirculating aquaculture systems | +0.9% | Guangdong, Fujian, Shandong, Hainan, and Guangxi | Long term (≥ 4 years) |

| Strategic pivot to disease-resistant Specific Pathogen Free (SPF) broodstock | +0.8% | Major breeding centers nationwide | Medium term (2-4 years) |

| Vertical integration of processing and cold-chain logistics | +0.7% | Guangdong, Shandong, and Jiangsu | Long term (≥ 4 years) |

| Growing online B2B seafood procurement platforms | +0.6% | Coastal and Yangtze Delta regions | Short term (≤ 2 years) |

| Synergies with solar-aquaculture infrastructure | +0.5% | Provinces with high solar irradiance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Preference for Lean Protein

Household consumption reached 39% of national GDP in 2024 and is projected to rise 3%-4% annually to 2035, creating a broad base of purchasing power for premium seafood. Per-capita meat intake doubled between the mid-1990s and 2024, and shrimp is gaining share because urban millennials favor low-fat protein that aligns with fitness trends. Foodservice revenue expanded 8.4% year-over-year in the first five months of 2024 as restaurants aggressively featured shrimp in quick-service menus. E-commerce data show that even amid 12% average price deflation during 2023, premium shrimp maintained stable margins, indicating buyers will pay for traceability and perceived freshness. The demographic engine behind this demand, millennials and Gen Z, has higher disposable income, is digitally savvy, and values sustainability credentials, giving suppliers that adopt Environmental, Social and Governance (ESG) labeling a clear advantage. As middle-class households migrate inland, cold-chain growth is extending its reach, stimulating demand beyond coastal cities.

Government Incentives for Modern Recirculating Aquaculture Systems

Provincial subsidies and low-interest loans are accelerating recirculating aquaculture system (RAS) roll-outs that recycle water and slash pathogen exposure. Hubei made substantial investments in 2024 to support in constructing of greenhouse facilities, while Shandong offers tax rebates covering 30% of capital expenditure for farms that meet biosecurity benchmarks [1]Hubei Provincial Government, “RAS Subsidy Program 2024,” Hubei.gov.cn. The recirculating aquaculture system (RAS) units achieve 3-5 times higher stocking density and cut water use by 90%, satisfying strict discharge rules while maximizing land productivity [2]Ministry of Agriculture and Rural Affairs, “Cold-Chain Treatment Report 2023,” Moa.gov.cn. The systems also enable year-round cycles, smoothing seasonal price swings that previously reached 60%. Payback periods of 4-6 years are proving attractive for mid-sized farms with credit access. Suppliers of filtration membranes and sensor suites are benefitting from a wave of retrofit orders. Over time, recirculating aquaculture system (RAS) adoption should raise national output without expanding coastal footprints, supporting the long-run competitiveness of the China shrimp market.

Strategic Pivot to Disease-Resistant Specific Pathogen Free (SPF) Broodstock

Losses from acute hepatopancreatic necrosis disease (AHPND) and white spot syndrome have exceeded USD 3 billion since 2010, pushing growers toward specific pathogen-free (SPF) broodstock that lowers mortality to 10%-15% versus 40%-100% in conventional ponds. Guangdong and Hainan breeding centers now generate a significant number of post-larvae annually, yet demand still outstrips supply by 30% during peak March-May stocking. Genome-editing research, including the Clustered regularly interspaced short palindromic repeats (CRISPR) applications, has demonstrated 45% yield gains in tilapia and is on track for Pacific white shrimp trials estimated by 2027 [3]Nature Biotechnology, “Genome Editing Applications in Aquaculture,” Nature.com. Regulatory pathways remain uncertain, but early adoption promises a first-mover edge. Higher survival rates reduce feed wastage and antibiotic use, aligning with government efforts to curb antimicrobial resistance. Capital investment in hatcheries is likely to accelerate as integrated players aim for closed-loop genetic control and to capture premium prices from disease-conscious buyers.

Vertical Integration of Processing and Cold-Chain Logistics

Origin-level blast freezing covered majority of aquatic products in 2023, illustrating a national push to curtail spoilage and elevate product grade. Total cold-storage capacity has climbed significantly, and Yuhu Cold Chain now runs IoT-enabled warehouses in Guangzhou, Chengdu, and Wuhan that guarantee stable -18 °C storage from harvest to retail shelf. Integrating feed mills, hatcheries, processing plants, and e-commerce channels lets producers capture 15%-25% of the final retail margin, bypassing distributors who formerly took 30%-40%. Blockchain traceability reassures consumers and supports premium positioning. AI-optimized route planning has shaved last-mile costs 12%-18%, enabling same-day delivery within 200 kilometers of production hubs. As online grocery penetration edges toward 25% of food retail by 2027, integrated operators can lock in market access and defend against fluctuating wholesale prices.

Market Restraints*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring acute hepatopancreatic necrosis disease outbreaks | −0.8% | National, highest in pond systems | Short term (≤ 2 years) |

| Volatile feed ingredient costs (soybean, fishmeal) | −0.7% | National, all systems | Medium term (2-4 years) |

| Strict coastal discharge and ecological regulations | −0.6% | Guangdong, Fujian, Shandong, Hainan, and Guangxi | Long term (≥ 4 years) |

| Intensifying competition from low-cost Ecuadorian imports | −0.9% | Retail and foodservice channels nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recurring Acute Hepatopancreatic Necrosis Disease Outbreaks

Acute Hepatopancreatic Necrosis Disease Outbreaks (AHPND), driven by Vibrio parahaemolyticus bearing the pirAB toxin genes, routinely causes 40%-100% pond mortality within 20-30 days post-stocking at water temperatures above 28 °C. Biosecurity practices, water filtration, probiotics, and quarantine remain the only defense because no approved therapeutics exist. White spot syndrome virus compounds the burden in many coastal sites. Transitioning to RAS facilities can cut infection vectors, yet demands USD 70,000-280,000 per hectare, a barrier for smallholders who still account for roughly 60% of output. Insurance uptake hovers below 15%, leaving most growers exposed to catastrophic losses. Disease flare-ups, therefore, dampen stocking confidence, delay harvests, and temper the medium-term expansion of the China shrimp market.

Volatile Feed Ingredient Costs (Soybean, Fishmeal)

Fishmeal prices spiked in mid-2024 due to El Niño-driven reductions in Peruvian anchovy landings, while soybean meal also rose because of severe drought conditions in South America. Feed forms 50%-60% of total operating costs, so a 10% price rise trims farm margins by 5-6 points. Alternative proteins, such as insect meal or algae, remain 20%-40% costlier and face regulatory hurdles. Even as genetic selection and precision feeding have lifted feed conversion ratios from 1.8:1 to 1.5:1 over the past decade, further gains require automated feeders costing USD 14,000-42,000 per installation. Margin squeeze reduces reinvestment in biosecurity and innovation, slowing productivity gains needed to offset flat farm-gate prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Guangdong produces a major share of the national shrimp volume in 2025, due to its 1,900-kilometer shoreline, warm climate, and proximity to Hong Kong and Macau export gateways . Shandong followed, leveraging greenhouse technology that enables winter culture and earns premiums during seasonal shortages. Fujian, Hainan, and Guangxi together delivered a significant share of output, supported by high-salinity coastlines and established hatchery clusters. Coastal protection statutes cap horizontal expansion, funneling capital toward yield-intense RAS projects and solar-aquaculture hybrids that maximize output per hectare. Inland provinces such as Hubei and Jiangsu now deploy RAS at scale, demonstrating geographic diversification of supply.

Consumption patterns mirror urban income tiers. The Yangtze River Delta, including Shanghai, Jiangsu, and Zhejiang, reports the country’s highest per-capita intake. Pearl River Delta cities, notably Guangzhou and Shenzhen, follow closely. Inland provinces average lower consumption but are steadily catching up as cold-chain penetration deepens.

Regulatory enforcement varies. Guangdong and Fujian perform quarterly discharge audits, spurring rapid adoption of treatment wetlands. Hainan specializes in SPF broodstock, supplying 40% of national demand and exporting post-larvae across Southeast Asia. Jiangsu and Zhejiang focus on processing and logistics, hosting blast-freezing and e-commerce hubs. This specialization highlights the growing maturity of the China shrimp market, where each province leverages its comparative advantages to drive growth.

Competitive Landscape

The China shrimp market is fragmented, with the top producers collectively accounting for a small portion of total output. Guangdong HAID Group Co., Ltd. typifies vertical integration, controlling feed mills, SPF hatcheries, contract farms, and processing plants that supply national retail chains. Zhanjiang Guolian Aquatic Products Co., Ltd. e-commerce hub gives it direct access to restaurant chains, capturing distributor margins and shortening payment cycles.

Technology-led entrants deploy genome-editing research and closed-loop RAS to supply premium, antibiotic-free shrimp sought by health-conscious consumers. Blockchain-enabled traceability, wins 15%-20% price premiums in Tier-1 supermarkets. Digital procurement platforms disintermediate traditional wholesalers, forcing incumbents to build direct-sales units or cede margin. Consolidation is projected as stricter environmental rules render sub-scale farms unviable, giving well-capitalized players an acquisition pathway to expand pond inventory without greenfield permits.

White-space opportunities include genome-edited SPF lines projected for commercial availability by 2027 and offshore cage farming supported by 5G telemetry that mitigates land constraints. Firms that secure intellectual property and regulatory approvals early will command a technology moat. Cold-chain expansion into inland Tier-3 cities offers incremental market share gains, while cross-border e-commerce opens limited but lucrative channels for high-end value-added products.

Recent Industry Developments

- November 2024: Zhanjiang Guolian Aquatic Products is set to invest USD 1.52 million in a new marine industry investment fund, as the seafood processor seeks to expand its influence across China's shrimp supply chain.

- October 2024: The first shipment of whiteleg shrimp from Honduras officially entered the Chinese market on Sunday under a zero-tariff arrangement. This development reflects strengthened economic and trade relations between China and Honduras, aligned with the early harvest provisions of the free trade agreement (FTA).

- May 2023: The People's Republic of China (PRC) and Ecuador have signed a free trade agreement. This pact grants preferential tariffs on more than 95% of Ecuador's exports to China. Notably, this includes a variety of seafood products, such as white shrimp, fish, and fish oil. Over time, duties on these items have been slashed from a range of 5% to 20% down to a flat zero.

China Shrimp Market Report Scope

A shrimp can be defined as a small-sized marine crustacean with an elongated body, typically consumed as food, hence, it is of high commercial importance. The report covers Shrimp Farming in China and offers an analysis of Production (Volume), Consumption (Value and Volume), Import (Value and Volume), Export (Value and Volume), and Prices. The report offers the market size and forecasts for volume in metric tons and value in (USD) for all the above segments.

By Country

| Production Analysis (Volume) |

| Consumption Analysis (Volume and Value) |

| Import Analysis (Volume and Value) |

| Export Analysis (Volume and Value) |

| Price Trend Analysis |

| By Country | Production Analysis (Volume) |

| Consumption Analysis (Volume and Value) | |

| Import Analysis (Volume and Value) | |

| Export Analysis (Volume and Value) | |

| Price Trend Analysis |

Key Questions Answered in the Report

What is the current value of the China shrimp market?

The market is valued at USD 20.56 billion in 2026 and is on track to hit USD 26.78 billion by 2031.

How fast is the China shrimp market growing?

The market is expanding at a 5.43% CAGR through 2031, supported by technology upgrades and rising consumer demand.

Which province leads shrimp production in China?

Guangdong tops the list, contributing about 34.70% of national output thanks to its long coastline and warm climate.

Why are recirculating aquaculture systems important?

Recirculating Aquaculture Systems (RAS) units boost stocking density up to five-fold and cut water use 90%, helping farms meet strict discharge rules while raising yields.

Page last updated on: