Sensor-Embedded IoT Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

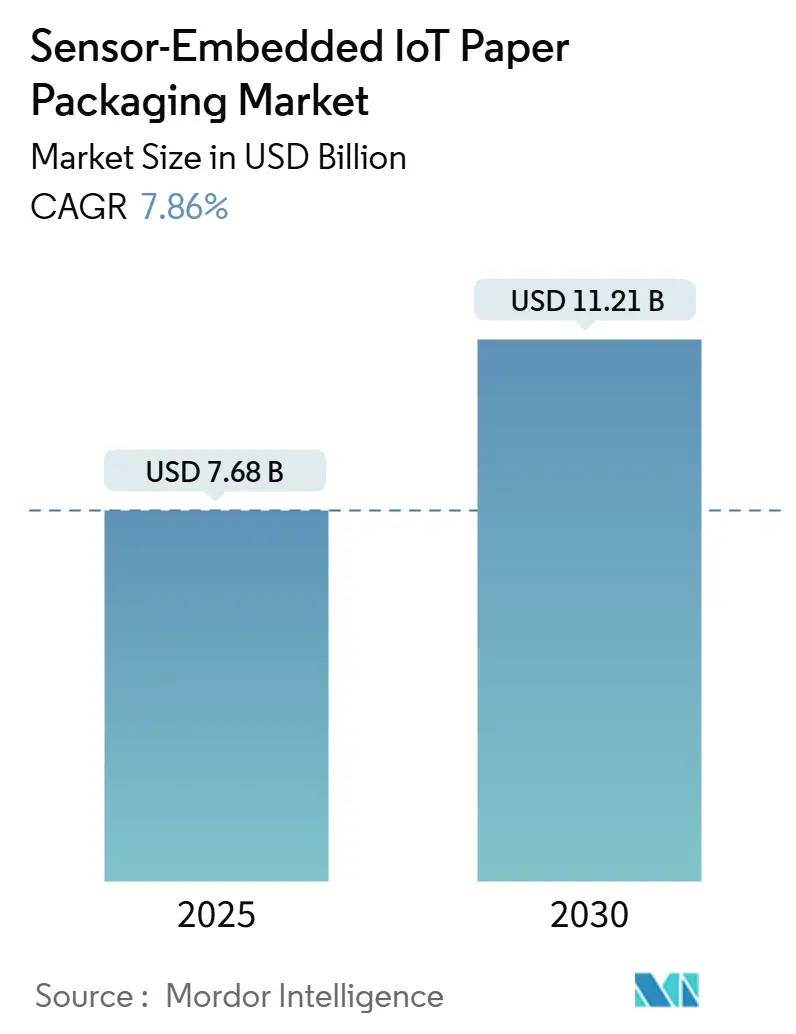

| Market Size (2025) | USD 7.68 Billion |

| Market Size (2030) | USD 11.21 Billion |

| Growth Rate (2025 - 2030) | 7.86% CAGR |

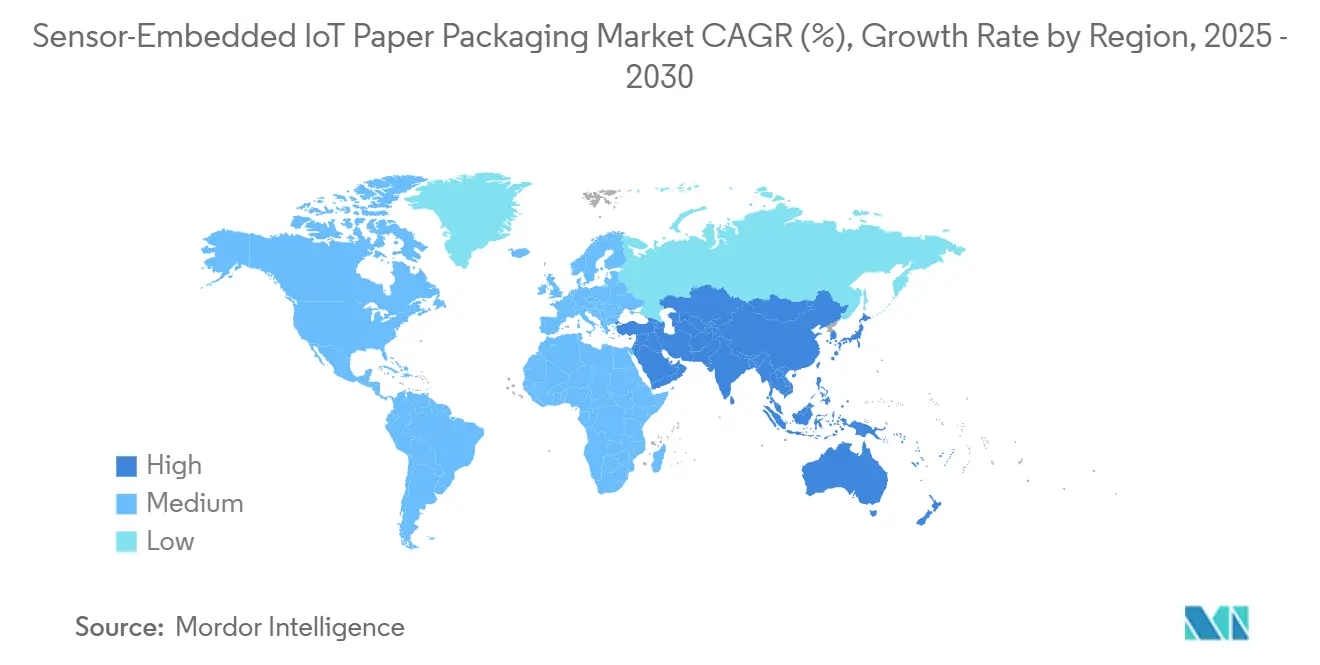

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensor-Embedded IoT Paper Packaging Market Analysis by Mordor Intelligence

The current Sensor-embedded IoT paper packaging market size stands at USD 7.68 billion in 2025 and is projected to reach USD 11.21 billion by 2030, delivering a 7.86% CAGR over the forecast horizon. Rapid scale-up is rooted in converging regulatory, environmental, and digitalization mandates, positioning the Sensor-embedded IoT paper packaging market as a cornerstone of next-generation supply-chain infrastructure. Regulatory traceability deadlines, falling printed-electronics costs, and the switch from plastic to fiber packs are expanding addressable applications across food, pharma, and industrial logistics. Brand owners increasingly view intelligent fiber packs as revenue enablers through real-time cold-chain assurance, anti-counterfeiting, and gamified consumer engagement. Simultaneously, insurers are rewarding monitored shipments with lower premiums, compressing payback periods for adopters. Intensifying competition is pushing incumbents to vertically integrate substrate, sensor, and data-platform capabilities to secure margin and customer stickiness.

Key Report Takeaways

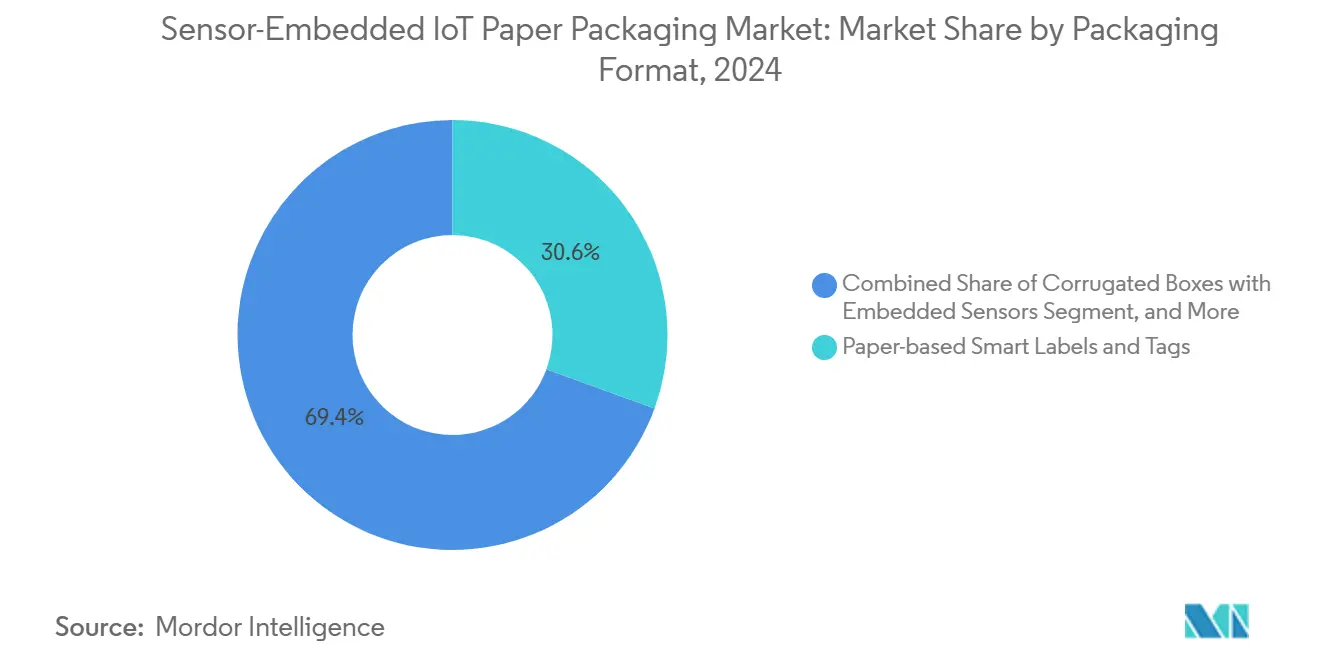

- By packaging format, paper-based smart labels and tags captured 30.56% of the sensor-embedded IoT paper packaging market share in 2024.

- By embedded sensor type, the sensor-embedded IoT paper packaging market size for the NFC/RFID sensor tags segment is projected to grow at 8.57% CAGR between 2025-2030.

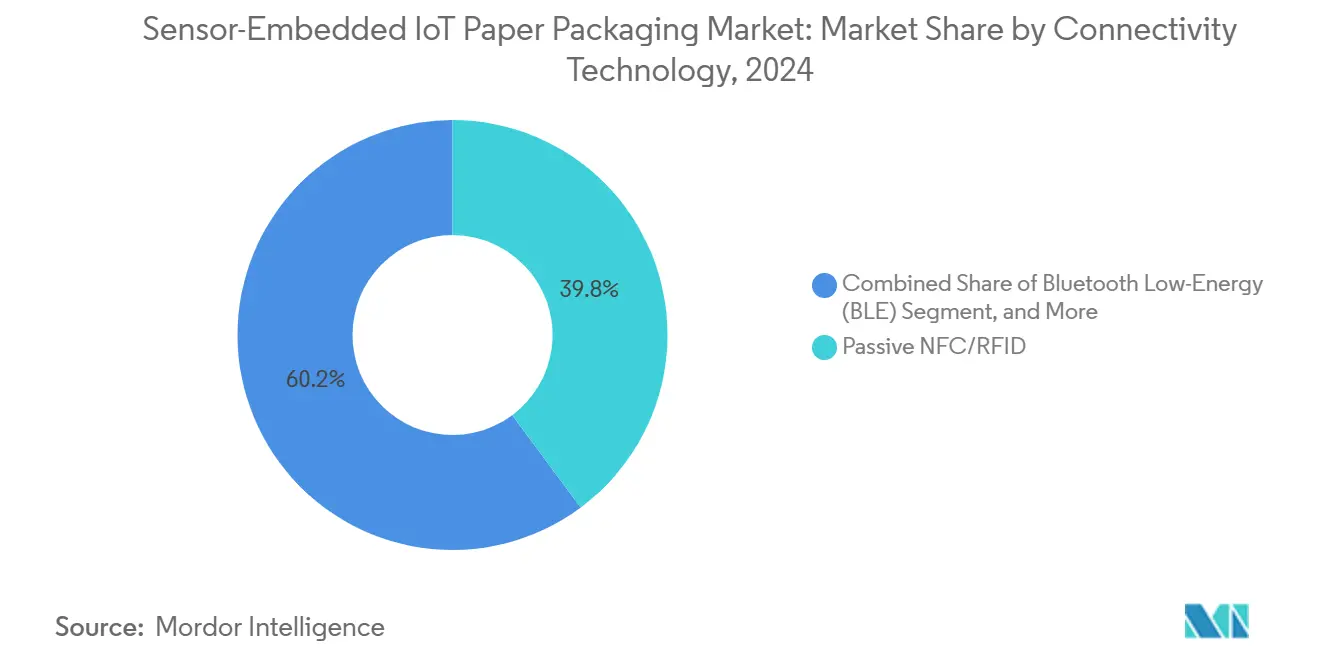

- By connectivity technology, passive NFC/RFID solutions captured 39.83% of the sensor-embedded IoT paper packaging market share in 2024.

- By end-use industry, the sensor-embedded IoT paper packaging market size for the industrial and logistics applications segment is projected to grow at 8.29% CAGR between 2025-2030.

- By geography, North America captured 33.07% of the sensor-embedded IoT paper packaging market share in 2024.

Global Sensor-Embedded IoT Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for real-time cold-chain monitoring | +1.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Regulatory push for end-to-end traceability and serialization | +1.4% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Falling costs of printed electronics and NFC chipsets | +0.9% | Global, with manufacturing concentration in APAC | Long term (≥ 4 years) |

| Gamified consumer engagement via smart paper packaging | +0.6% | North America and EU core, expanding to urban APAC | Medium term (2-4 years) |

| ESG-driven switch from plastic to fiber smart packs | +1.1% | EU-led, with North America following, APAC emerging | Long term (≥ 4 years) |

| Insurance premium discounts for IoT-enabled shipments | +0.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Cold-Chain Monitoring

Temperature excursions can wipe out USD 35 billion in pharmaceutical value yearly, placing continuous monitoring at the core of compliance and risk-management strategies. Cryogenic biologics such as Cryoprecipitated AHF must remain at −18 °C or colder during shipment, a requirement that sensor-embedded fiber packs fulfill while adding an immutable audit trail.[1]U.S. Food and Drug Administration, “21 CFR 600.15 Temperatures During Shipment,” ecfr.gov Health Canada’s transport guidelines reinforce the same temperature integrity expectations, ensuring harmonized North American oversight. The Sensor-embedded IoT paper packaging market therefore benefits from mandatory adoption across vaccines, biologics, dairy, and produce, allowing shippers to intervene before spoilage occurs and to claim insurance credits for verified compliance. Pharmaceutical, food, and third-party logistics players increasingly integrate temperature sensors directly into corrugated outers, reducing reliance on separate data-loggers and eliminating plastic housings, which supports both sustainability and cost-down objectives.

Regulatory Push for End-to-End Traceability and Serialization

The FDA’s Food Traceability Rule compels critical data collection at every hand-off, with records delivered within 24 hours of request and full compliance due January 2026. Packaging that carries passive NFC sensors can capture Key Data Elements automatically, cutting manual error risk and lowering administrative costs. Canada has mirrored the United States framework for cross-border food shipments, encouraging standardized solutions across North America. The rule’s 30-month grace period announced in 2025 only postpones penalties; investment decisions are already underway as retailers dictate compliant packaging from suppliers. Comparable mandates in the EU’s Circular Economy Action Plan are amplifying global convergence, collectively boosting the Sensor-embedded IoT paper packaging market.

Falling Costs of Printed Electronics and NFC Chipsets

Roll-to-roll printing has slashed functional ink expense and curing energy, driving 40% unit-cost reductions since 2020 while raising throughput to 200 m/min. Chip suppliers now deliver passive NFC dies for under USD 0.03, unlocking profitability in mid-priced grocery SKUs. SEMI’s 2024 FLEXI Awards highlighted volume production of flexible hybrid electronics as an inflection point for mass uptake. Lower barriers are stimulating new entrants and enabling tier-2 converters to retrofit existing presses, enlarging the Sensor-embedded IoT paper packaging market footprint across regional brands and private-labels previously deterred by cost.

Gamified Consumer Engagement via Smart Paper Packaging

Consumer studies reveal that NFC tags positioned center-right with high-contrast color cues generate the highest tap-through rates, particularly among Gen-Z shoppers. Brands embed loyalty points, authenticity proofs, and instructional videos accessible via smartphones, transforming packaging into a data-rich marketing channel. Digimarc’s 2024 acquisition of EVRYTHNG strengthens cloud connectivity that synchronizes sensor data with consumer apps, allowing freshness indicators or dosage reminders to display dynamically. By merging experiential content with supply-chain telemetry, companies can command price premiums and collect first-party data, further fueling investment in the Sensor-embedded IoT paper packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration cost versus conventional packs | -0.6% | Global, with higher impact in price-sensitive markets | Short term (≤ 2 years) |

| Short read-range of battery-free sensor tags on paper | -0.4% | Global, particularly affecting warehouse automation | Medium term (2-4 years) |

| Recycling contamination from embedded electronics | -0.6% | EU-led concerns, expanding globally | Long term (≥ 4 years) |

| Lack of calibration standards for printed cellulose sensors | -0.3% | Global, with regulatory focus in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Cost versus Conventional Packs

Sensor-ready fiber packs still command 15–25% premiums due to specialist inks, pick-and-place lines, and QC protocols. Avery Dennison’s Intelligent Labels division reported ≥20% volume growth but also heavy R&D capitalization that keeps unit cost above plain labels. Smaller converters face steep investment, slowing penetration in price-sensitive emerging markets. Volume scaling, printed antennae, and simplified assembly are expected to narrow the gap, yet the near-term drag persists on the Sensor-embedded IoT paper packaging market.

Recycling Contamination from Embedded Electronics

Embedded circuits complicate fiber recovery, risking down-cycling or landfill. The EU’s recyclability mandate intensifies scrutiny; SGS notes that non-removable electronics could fall foul of compliance audits. Current mills lack automated detachment systems, and manual removal raises cost. IPC/JEDEC standards outline marking but not removal guidelines, leaving recyclers to devise procedures. Until design-for-recycling advances, eco-conscious brands may hesitate, tempering the Sensor-embedded IoT paper packaging market acceleration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Smart Labels Drive Current Adoption

Paper-based smart labels own 30.56% of 2024 revenue, confirming their role as the Sensor-embedded IoT paper packaging market on-ramp for brands lacking capital to redesign primary packs. Retrofit flexibility and low profile enable rollout across SKU portfolios without machinery overhaul. Corrugated boxes grow fastest at 8.42% CAGR, piggybacking on e-commerce fulfilment and industrial supply-chain visibility. The smart-label segment benefits from Avery Dennison’s plan to lift Intelligent Labels organic sales >15% annually, signalling an ecosystem shift toward standardizing RFID within secondary packaging.[2]Avery Dennison Corp., “Form 10-K 2024,” sec.gov

E-commerce shippers prioritize corrugated cartons with shock and temperature sensors to mitigate return costs, aligning with global parcel volumes exceeding 200 billion annually. Folding cartons address blister-pack and vial secondary packaging in pharma, where traceability and tamper evidence converge. Flexible pouches integrate humidity and gas sensors for snack and coffee freshness cues, positioning premium lines for consumer differentiation. The modularity across formats enables the Sensor-embedded IoT paper packaging market to escalate incremental penetration rather than rely on single large conversions.

By Embedded Sensor Type: Temperature Monitoring Leads Market

Temperature devices captured 35.74% share in 2024, embedded mainly in vaccines, biologics, seafood, and dairy packs. Mandatory cold-chain reporting erects a non-negotiable floor under demand. NFC/RFID sensor tags outpace all categories at 8.57% CAGR thanks to dual ID-plus-sensing functionality, enabling inventory accuracy and condition monitoring in one component. Printed humidity sensors serve bakery and produce freshness, while pressure sensors authenticate that high-value electronics remain shock-free. Research on nanomaterial RFID antennas promises 50% size reduction, unlocking chipless sensors for low-margin packages. Multi-sensor hybrids are emerging, layering temperature, shock, and gas detection to build 360° visibility, expanding the Sensor-embedded IoT paper packaging market addressability across varied perishables.

By Connectivity Technology: Passive Solutions Dominate Present

Passive NFC/RFID held 39.83% of 2024 revenue, a testament to the ubiquity of handheld readers and smartphone compatibility. Battery-free operation and sub-USD 0.10 tags sustain cost leadership. Yet globalised, long-haul supply chains now demand 24/7 telemetry; hence cellular NB-IoT/LTE-M is scaling fastest at 8.34% CAGR. 5G coverage densification removes prior blind spots, enabling pallet-level tracing across oceans. BLE beacons fill mid-range warehouse automation niches, while LoRaWAN links large-format paper pallets in forestry and metals exports. Hybrid architectures combining passive IDs with cellular gateways blend cost efficiency and latency-free data, consolidating the Sensor-embedded IoT paper packaging market across multiple transport modes.

By End-Use Industry: Food Sector Drives Current Demand

Food and beverage dominated 31.95% revenue in 2024, propelled by zero-tolerance contamination policies and date-code automation. Supermarket chains enforce sensor-enabled traceability contracts to cut recall costs and food waste, pushing adoption downstream. Industrial logistics tops CAGR at 8.29% as predictive maintenance and autonomous warehouse programs hunger for location and condition data. Biopharma spends heavily on temperature-validated fiber shippers for personalized cell and gene therapies, while cosmetics leverage NFC to prove authenticity and amplify brand storytelling. Electronics brands attach shock sensors to high-value smartphones, slashing in-transit damage claims. Diversified vertical uptake cements the Sensor-embedded IoT paper packaging market as a multi-industry growth engine rather than a single-sector play.

Geography Analysis

North America’s 33.07% revenue share in 2024 reflects deep regulatory reach, mature cold-chain infrastructure, and high disposable income backing premium packaging. FDA mandates under FSMA 204 and 21 CFR 600.15 fix compliance time-lines that translate directly into procurement budgets for sensor-ready corrugated and labels. Canada’s synchronized rules remove trade friction, making the region a unified innovation sandbox. Retailers incentivize traceable fiber packs through supplier scorecards, embedding long-term demand into grocery and pharma categories. Insurers in the U.S. now offer up to 20% freight-cover discounts for shipments with live data feeds, tightening ROI cycles.

Asia-Pacific expands at 8.61% CAGR, leveraging manufacturing scale and accelerated digitization policies. China’s smart-factory incentives subsidize printed-electronics lines, narrowing integration cost gaps. Japan and South Korea export sensor knowledge into packaging converters, while India’s vaccine-export ambitions hinge on validated cold chains, catalyzing volume. ASEAN nations adopt GS1-compliant seafood tracking to retain EU market access, further boosting the Sensor-embedded IoT paper packaging market. Rising middle-class demand for premium, authenticated food drives NFC adoption at retail shelves, moving beyond export-driven use cases.

Europe’s Circular Economy legislation transitions the bloc from plastic to fiber substrates by mandate. The 2025 regulation requires recyclability and minimum recycled content, turning sensor-compatible virgin and recycled board into default solutions. Mondi’s EUR 1.2 billion (USD 1.29 billion) capex in sustainable lines mirrors Stora Enso’s capacity build, signalling supply readiness.[3]Mondi Group, “Half-Year Results 2024,” mondigroup.com Germany pilots paper crates with embedded NB-IoT for automotive parts, illustrating industrial diversification. Southern Europe pushes freshness-indicator labels on fruit exports, linking growers to overseas retailers via real-time dashboards. Regulatory certainty and brand ESG commitments anchor the Sensor-embedded IoT paper packaging market into Europe’s long-term packaging roadmap.

Competitive Landscape

The field features cross-disciplinary competition, with packaging titans, electronics majors, and high-growth start-ups jostling. Stora Enso and Mondi integrate barrier boards, printed antennas, and digital platforms, leveraging mill capacity and fiber R&D to lock in customers. Avery Dennison expands its RFID franchise, acquiring design houses and middleware firms to offer turnkey “pack-to-cloud” solutions. Digimarc focuses on digital watermarking that piggybacks on sensor data to authenticate and recycle packs efficiently.

Technology specialists such as Wiliot and PragmatIC unveil battery-free Bluetooth or chipless RFID sensors aimed at mass merchandise. Converter alliances with semiconductor fabs accelerate time-to-market yet raise IP-sharing tensions. Brand owners increasingly sign multi-year exclusivity deals to secure supply, nudging market concentration upward. In 2024, the top five suppliers accounted for 42% of global revenue, a moderate level that permits niche entrants but still rewards scale efficiencies. Integration of cloud analytics, predictive algorithms, and circular-design consulting becomes a differentiation lever as hardware commoditizes, setting the next battleground for Sensor-embedded IoT paper packaging market leadership.

Sensor-Embedded IoT Paper Packaging Industry Leaders

Stora Enso Oyj

Smurfit Westrock PLC

Mondi PLC

Avery Dennison Corporation

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stora Enso reported a 9% year-on-year sales rise to EUR 2,362 million and ramp-up of its Oulu consumer board line slated for full capacity by 2027, underscoring commitment to renewable smart-pack substrates.

- February 2025: The EU enacted Regulation (EU) 2025/40 on Packaging and Packaging Waste, making recyclability mandatory by 2030 and pushing fiber-based intelligent packs mainstream.

- October 2024: Avery Dennison posted 5% organic sales growth in Q3 2024, citing Intelligent Labels expansion into food and apparel and targeting >15% long-run category growth.

- July 2024: Mondi announced H1 2024 EBITDA of EUR 565 million (USD 611 million) alongside EUR 1.2 billion (USD 1.29 billion) organic growth investments, including fiber packs designed for embedded sensors.

Global Sensor-Embedded IoT Paper Packaging Market Report Scope

| Corrugated Boxes with Embedded Sensors |

| Folding Cartons with Embedded Sensors |

| Flexible Paper Pouches and Sacks with Sensors |

| Paper-based Smart Labels and Tags |

| Paper Pallets and Crates with Sensors |

| Temperature Sensor |

| Humidity / Moisture Sensor |

| Pressure and Shock Sensor |

| Gas / VOC Sensor |

| NFC / RFID Sensor Tag |

| Optical / Colorimetric Sensor |

| Passive NFC / RFID |

| Bluetooth Low-Energy (BLE) |

| Wi-Fi / LoRaWAN |

| Printed Electronic Data-Loggers |

| Cellular (NB-IoT / LTE-M) |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Electronics and Semiconductors |

| Industrial and Logistics |

| Other End-Use Industry (Perishables, Chemicals) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Packaging Format | Corrugated Boxes with Embedded Sensors | ||

| Folding Cartons with Embedded Sensors | |||

| Flexible Paper Pouches and Sacks with Sensors | |||

| Paper-based Smart Labels and Tags | |||

| Paper Pallets and Crates with Sensors | |||

| By Embedded Sensor Type | Temperature Sensor | ||

| Humidity / Moisture Sensor | |||

| Pressure and Shock Sensor | |||

| Gas / VOC Sensor | |||

| NFC / RFID Sensor Tag | |||

| Optical / Colorimetric Sensor | |||

| By Connectivity Technology | Passive NFC / RFID | ||

| Bluetooth Low-Energy (BLE) | |||

| Wi-Fi / LoRaWAN | |||

| Printed Electronic Data-Loggers | |||

| Cellular (NB-IoT / LTE-M) | |||

| By End-Use Industry | Food and Beverage | ||

| Pharmaceuticals and Healthcare | |||

| Cosmetics and Personal Care | |||

| Electronics and Semiconductors | |||

| Industrial and Logistics | |||

| Other End-Use Industry (Perishables, Chemicals) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Sensor-embedded IoT paper packaging market in 2025?

The Sensor-embedded IoT paper packaging market size is USD 7.68 billion in 2025 with a forecast value of USD 11.21 billion by 2030.

Which region grows fastest for sensor-embedded fiber packs?

Asia-Pacific is projected to register the quickest expansion at an 8.61% CAGR through 2030, driven by manufacturing digitization and stricter food-safety rules.

What segment shows the highest revenue share?

Paper-based smart labels hold the largest share at 30.56% of 2024 revenue, making them the leading adoption format.

Why are insurers offering discounts on IoT-enabled shipments?

Continuous sensor data lowers cargo loss risk, enabling insurers to cut premiums and deductibles, which improves shipment economics for adopters.

Which connectivity technology is scaling fastest?

Cellular NB-IoT/LTE-M is advancing the quickest at an 8.34% CAGR due to its real-time, long-range monitoring capability across global supply chains.

How does EU regulation impact smart paper packaging?

Regulation (EU) 2025/40 requires all packaging to be recyclable by 2030, pushing brands toward fiber substrates that integrate sensors while meeting circular-economy targets.

Page last updated on: