Secured Web Gateway Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.7 Billion |

| Market Size (2031) | USD 57.4 Billion |

| Growth Rate (2026 - 2031) | 22.62% CAGR |

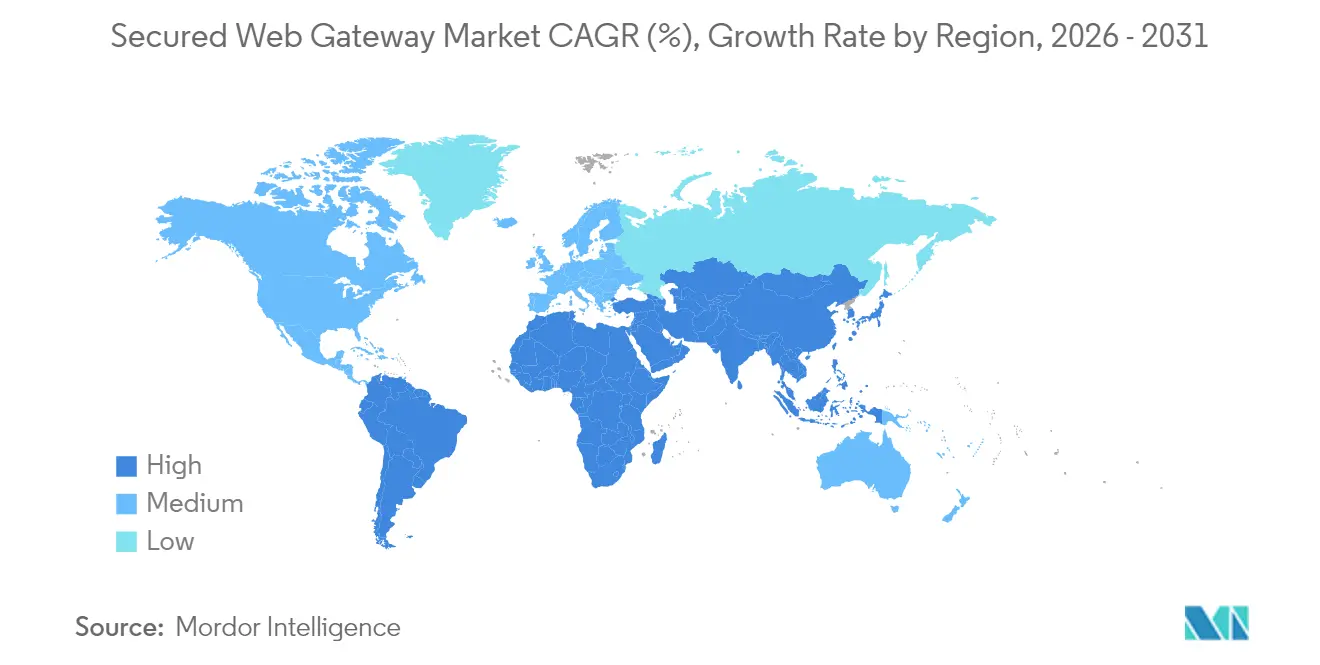

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secured Web Gateway Market Analysis by Mordor Intelligence

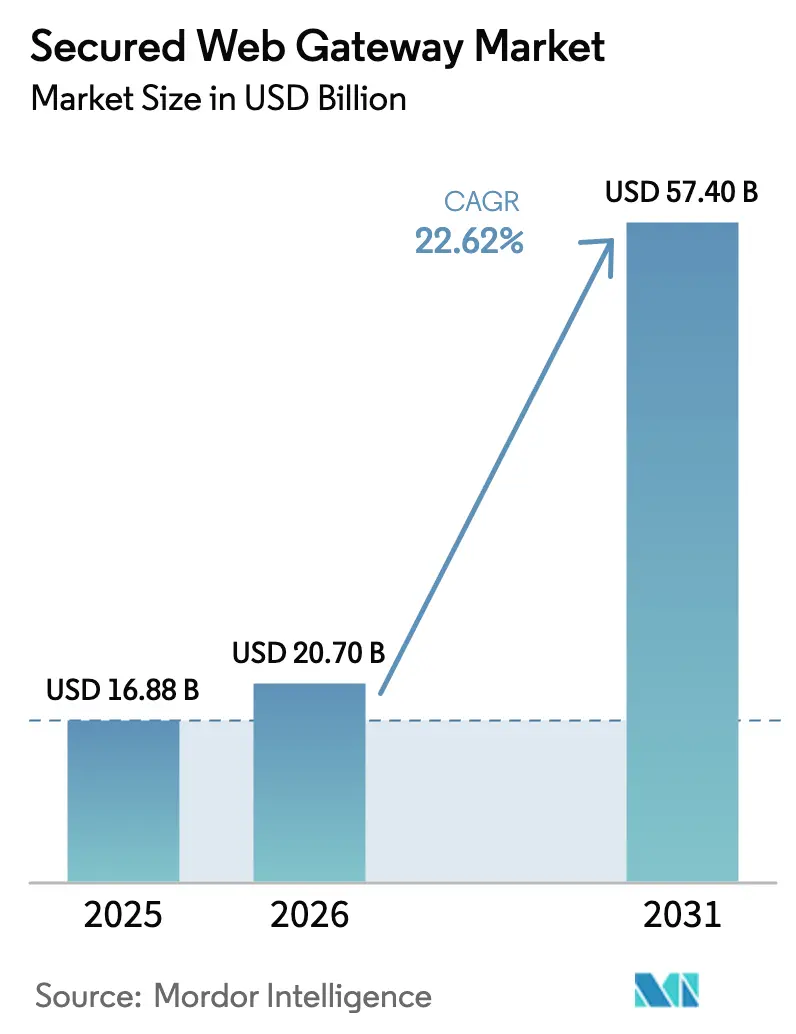

The secured web gateway market size is expected to grow from USD 16.88 billion in 2025 to USD 20.7 billion in 2026 and is forecast to reach USD 57.4 billion by 2031 at 22.62% CAGR over 2026-2031. Growth accelerates as enterprises redesign security for an environment in which AI-enabled malware mutates in real time, federal rules impose phishing-resistant authentication, and executives replace perimeter tools with cloud-native zero-trust controls. Cloud migration, permanent hybrid work, and supply-chain inflation further elevate demand for elastic security delivered at the edge. Vendor competition intensifies around AI-driven detection, with platforms such as Zscaler inspecting more than 500 billion daily transactions while sustaining double-digit revenue expansion. Organizations continue abandoning legacy VPNs: T-Mobile retired its on-premise gateways after a three-month rollout of the Zero Trust Exchange across all employees, illustrating the speed at which large enterprises can modernize when user experience improves . Meanwhile, Sophos paid USD 859 million to acquire Secureworks and fold its XDR technology into a broader platform, signaling a wave of consolidation that compresses buying cycles and magnifies the influence of a few AI-first suites. Heightened interest in managed security is equally visible: constrained by talent scarcity, many firms now purchase turnkey services that operate and fine-tune secure web gateways around the clock.

Key Report Takeaways

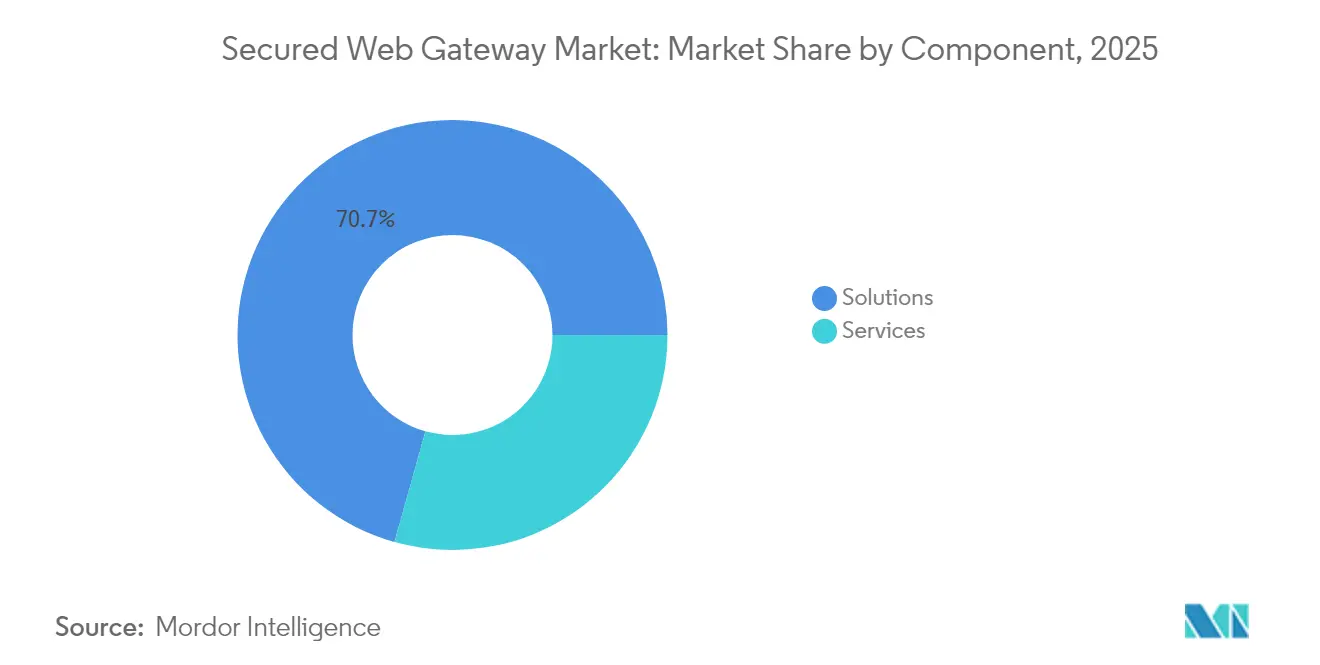

- By component, solutions accounted for 70.65% revenue share in 2025, whereas services are projected to advance at a 18.55% CAGR to 2031.

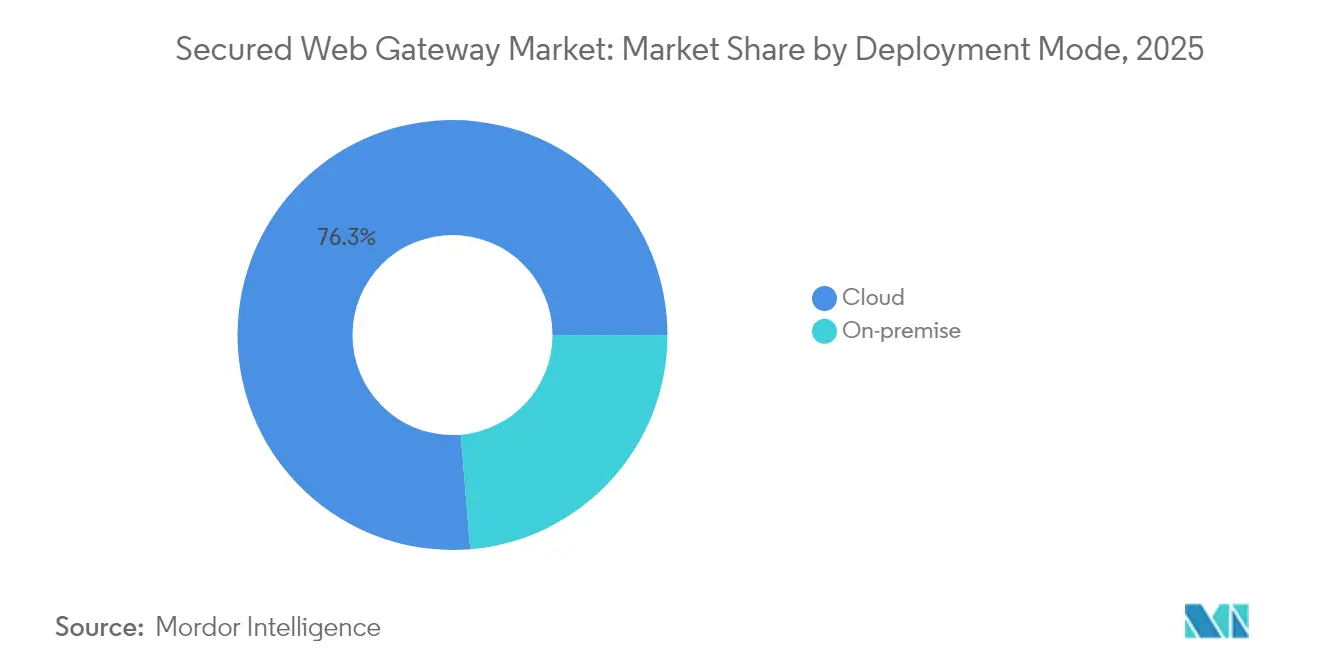

- By deployment mode, cloud models captured 76.32% of the secured web gateway market share in 2025 and continue to outpace on-premise alternatives at a 22.05% CAGR.

- By organization size, large enterprises held 63.88% of the secured web gateway market in 2025, yet small and medium enterprises are expanding the fastest at a 20.05% CAGR.

- By vertical, BFSI led with 27.12% revenue share in 2025, while IT and telecommunications is forecast to grow 21.34% annually through 2031.

- By geography, North America contributed 45.92% of global revenue in 2025; Asia-Pacific is on track for a 19.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Secured Web Gateway Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion in sophisticated AI-enabled cyber-attacks | +6.2% | North America and Europe | Short term (≤ 2 years) |

| Enterprise cloud migration and hybrid-workforce growth | +5.8% | North America and Asia-Pacific | Medium term (2-4 years) |

| Regulatory push for zero-trust web controls | +4.1% | North America and Europe | Medium term (2-4 years) |

| Integration of SWG into SASE refresh cycles | +3.7% | Global | Long term (≥ 4 years) |

| Rise of AI-powered real-time zero-day blocking | +3.4% | Global | Short term (≤ 2 years) |

| Shortage of in-house cybersecurity talent | +3.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion in Sophisticated AI-Enabled Cyber-Attacks

Polymorphic ransomware frameworks now iterate malicious code each time they execute, rendering static signatures obsolete. Security laboratories have demonstrated ChatGPT-generated malware that shifts both hash value and behavior mid-session, forcing defenders toward behavioral analytics and continuous validation. Cyber-crime damages are expected to crest USD 10.5 trillion in 2025, placing a premium on secure web gateways that integrate AI inference engines capable of real-time anomaly scoring. [1]WatchGuard Threat Lab, “BlackMamba Proof-of-Concept,” watchguard.comAsia-Pacific bears roughly one-third of recorded incidents, adding urgency for gateway deployments with multilingual threat-intel feeds.

Enterprise Cloud Migration and Hybrid-Workforce Expansion

Migration to SaaS and IaaS removes the data-center moat; employees and workloads now connect from unmanaged devices and edge locations. Microsoft’s Security Service Edge integrates identity, endpoint, and network controls so that Office 365 or Azure access is verified on every request, not just at login. Cisco reinforces the pattern by fusing SD-WAN and cloud-native security into a unified SASE architecture, allowing security policies to follow the user rather than the network. [2]Cisco Systems, “Secure Access Service Edge Solution Brief,” cisco.com Healthcare provider Main Line Health achieved micro-segmentation without redesigning its network, illustrating how dynamic policy automation protects patient data while avoiding downtime.

Regulatory Push for Zero-Trust Web Controls

Executive Order 14028 obliges all US federal agencies to adopt phishing-resistant MFA and continuous asset discovery, creating a ripple effect across contractors and critical-infrastructure operators. NIST SP 800-207 formalizes zero-trust concepts, shifting controls from the perimeter to each transaction. [3]NIST, “Special Publication 800-207 Zero-Trust Architecture,” nist.gov Financial institutions like Standard Chartered have implemented identity platforms that satisfy more than 30 overlapping regulations while accelerating digital onboarding. In healthcare, updated HIPAA security rules explicitly recommend network segmentation to limit unauthorized lateral movement, prompting rapid adoption of micro-segmentation within secure web gateway configurations.

Integration of SWG into SASE Refresh Cycles

The MEF SASE standard now provides common terminology, enabling technology teams to compare offerings more easily and favor single-vendor stacks that reduce operating overhead. . Fortinet recorded a 25.7% year-over-year jump in Unified SASE recurring revenue to USD 1.15 billion in Q1 2025, demonstrating enterprise appetite for converged networking and security services. Edge-native 5G and private-LTE networks amplify interest because local inspection nodes can enforce policy with single-digit-millisecond latency, a level impossible with back-hauled traffic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficulty filtering polymorphic malicious sites | –2.8% | Regions facing advanced threat actors | Short term (≤ 2 years) |

| Productivity impact from blocking uncategorised URLs | –2.1% | Knowledge-intensive industries | Medium term (2-4 years) |

| Latency from deep SSL inspection for rich media | –1.9% | Bandwidth-intensive geographies | Short term (≤ 2 years) |

| Vendor lock-in via proprietary policy languages | –1.6% | Multi-vendor environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Difficulty Filtering Polymorphic Malicious Sites

AI-generated code now hides payload assembly within benign HTML, CSS, and JavaScript fragments that only coalesce on the end device. Classic secure web gateways inspect traffic at the network layer and therefore miss client-side construction. Proof-of-concept exploits such as BlackMamba confirm that dynamic analysis must extend into the browser itself. Vendors have begun embedding lightweight isolation agents to gain DOM-level visibility, yet complexity and cost slow adoption for smaller firms.

Productivity Impact from Blocking Uncategorised URLs

Non-contextual URL filtering often blocks collaboration services that lack a formal reputation score, interrupting employee workflows. During the first half of 2025 many banks reported an average of 2.4 generative-AI applications blocked per site, depriving data-science teams of essential tools. Secure cloud browsers that render web pages in an isolated container now allow safe access, reducing help-desk tickets and restoring user experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Market Foundation

Solutions generated USD 11.92 billion in 2025, equal to 70.65% of total revenue for the secured web gateway market. Large enterprises gravitate toward integrated suites that combine URL filtering, sandboxing, CASB, and DLP in a single policy engine, reducing console sprawl. Fortinet’s FortiMail Workspace Security demonstrates this convergence by extending email defense to collaboration apps while using machine learning to profile user behavior. The services segment, encompassing assessment, implementation, and fully managed operations, will expand at 18.55% CAGR. Skill shortages persist: hundreds of vacancies remain open for cloud-security architects, prompting outsourcers to wrap 24 × 7 monitoring around vendor platforms. Managed providers that bundle zero-trust consulting with consumption-based billing appeal strongly to SMEs that cannot hire dedicated analysts.

Demand for advisory services also rises as companies migrate from hardware appliances to cloud traffic steering. Integrators must map legacy access-control lists into identity-centric policies, fine-tune CASB discovery, and orchestrate SD-WAN edge nodes. The secured web gateway industry therefore sees consulting engagements shift from short proof-of-concepts to multi-year transformation programs that guarantee policy drift detection. Vendors partner closely with carriers; BT became the first global provider to embed Zscaler’s AI-driven gateways inside its MPLS backbone, illustrating how telecoms can monetize integrated security post-migration. .

By Organization Size: SME Adoption Accelerates Despite Constraints

Large enterprises held 63.88% revenue in 2025, reflecting broader IT budgets and risk-management mandates. Many Fortune 500 corporations run pilot sandboxes that push suspicious traffic into isolated browser sessions, an approach impractical on smaller budgets yet critical to IP protection. Conversely SMEs represent the fastest-growing opportunity, expanding at 20.05% CAGR as attack surfaces widen across distributed teams. The typical SME still allocates less than 10% of its annual IT spend to security, but SaaS delivery erases up-front appliance costs and replaces them with per-user subscriptions, leveling entry barriers.

Cloud marketplace listings also accelerate SME uptake; businesses can roll the secured web gateway market into a single Azure invoice, simplifying procurement. WatchGuard’s Unified Security Platform targets precisely this persona, bundling firewall, DNS-layer filtering, and MDR dashboards into an interface that IT generalists can operate. Competitive differentiation centers on rapid deployment wizards, pre-populated compliance templates, and automated health checks that notify administrators before policy mismatches occur.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployment captured 76.32% of the secured web gateway market in 2025 and is forecast to reach more than 83.40% share by 2031. Vendors continually add local POPs so that 95% of users experience sub-50-millisecond round-trip latency, meeting digital-experience benchmarks once achievable only with regional break-outs. Zscaler’s multi-tenant architecture processed over 500 billion daily transactions in early 2025 while maintaining 99.999% availability, evidencing hyperscale performance. On-premise gateways persist in defense and critical-infrastructure segments where air-gap or data-residency rules mandate physical separation, yet even those buyers now layer a cloud sandbox over their high-risk traffic.

Vendor silicon innovation reinforces the shift. Fortinet’s FortiSP5 ASIC delivers firewall throughput 17 times faster than a standard CPU while consuming 88% less power, letting providers run more inspection nodes per rack and pass savings to customers. These efficiencies directly influence the secured web gateway market size for cloud services, drawing cost-sensitive firms into subscription models that eliminate capital expenditure.

By End-User Vertical: Financial Services Lead Adoption

BFSI organizations accounted for 27.12% of 2025 revenue because regulatory frameworks such as PCI DSS 4.0 and FFIEC Cybersecurity Assessment Tool demand layered defenses and explicit visibility into web traffic. Global banks deploy AI classifiers to isolate brand-impersonation sites before fraud occurs, integrating those verdicts into fraud-risk scoring at the transaction level. Telecommunications and IT services, forecast to grow at 21.34% CAGR, confront parallel pressures as 5G rollouts expand network edges and multiply API endpoints. Operators like Deutsche Telekom embed secure web gateways at the core and the far edge, preserving consistent policy across public cloud, MEC nodes, and customer premises.

Healthcare providers accelerate adoption following revised HIPAA guidance that emphasizes micro-segmentation and real-time monitoring of ePHI transport. . Main-Line Health’s deployment of dynamic segmentation inside its data centers illustrates how zero-trust tenets reduce lateral-movement risk without forklift upgrades. Manufacturers, meanwhile, integrate browser isolation with industrial-control-system firewalls to prevent phishing breaches from jumping into production lines. The secured web gateway market size for OT-aware gateways is expected to double by 2030 as plant operators adopt IT-OT convergence strategies.

Geography Analysis

North America contributed 45.92% of global secured web gateway market revenue in 2025. Executive Order 14028, Office of Management and Budget M-22-09 deadlines, and CISA zero-trust maturity targets require federal agencies and suppliers to complete phishing-resistant MFA rollouts and asset discovery by the end of fiscal 2025. Commercial adoption mirrors public-sector urgency. T-Mobile’s three-month cutover from VPN to cloud gateways proves that large enterprises can execute at speed when user experience improves. Canadian regulations are tightening in tandem; draft Bill C-27 elevates penalties for data mishandling to 5% of global revenue, prompting accelerated gateway procurement among financial and healthcare providers.

Asia-Pacific is the fastest-growing region at 19.15% CAGR. Governments across Australia, Singapore, and Japan have published zero-trust roadmaps that recommend secure web gateways as a foundational control. Regional cybersecurity spending is expected to rise from USD 17.6 billion in 2022 to USD 32 billion by 2025, with cyber-insurance premiums growing nearly 50% annually. Yet regulatory divergence complicates cross-border data flows: China’s draft rules may waive some export security assessments, but “important data” remains undefined, forcing multinational companies to maintain separate logging instances inside the mainland. Fast-digitalizing economies such as Vietnam, Thailand, and Malaysia become entry targets for cloud-native providers that can offer localized data centers without building hardware footprints.

Europe demonstrates steady uptake, driven by GDPR data-sovereignty mandates. Financial regulators now request evidence of web-traffic de-identification before approving cloud migrations, leading to guardrails that route sensitive categories through EU-resident inspection nodes. In 2025 the European Data Protection Board clarified that pseudonymized analytics data processed in non-EU clouds must remain encrypted end to end, increasing demand for gateways with inline field-level tokenization. Latin America and the Middle East, though smaller today, show double-digit growth as digital banking initiatives and smart-city programs expand their attack surfaces. In the Middle East, national oil companies deploy browser isolation to protect operational-technology networks from supply-chain attacks, while Brazilian fintechs adopt SWG to satisfy open-banking requirements.

Competitive Landscape

The secured web gateway market features moderate concentration. Zscaler, Fortinet, and Palo Alto Networks together controlled roughly one-third of 2024 revenue, while the next ten vendors competed for the remainder. Zscaler processed in excess of 500 billion daily transactions and reported USD 647.9 million in Q2 FY2025 revenue, a 23% year-over-year gain, illustrating scale benefits from multitenant design. Fortinet advances performance leadership through custom ASICs, recently unveiling FortiGate 700G, which supplies seven times higher throughput at a fraction of the power draw of x86 rivals, reducing total cost of ownership for carriers.

Strategic acquisitions continue reshaping the field. Sophos’ USD 859 million purchase of Secureworks brings MDR telemetry into its gateway stack, targeting mid-market buyers that prioritize integrated XDR, endpoint, and web controls. Lakera’s USD 20 million seed round focuses on protecting LLM pipelines from prompt attacks and model-poisoning, indicating that niche startups are carving specialized positions rather than attempting full-suite competition. Platform consolidation also favors open schemas: Splunk co-founded the Open Cybersecurity Schema Framework to simplify data sharing, reducing barriers for customers that fear vendor lock-in.

Partnerships with telecom operators and hyperscalers have become pivotal. BT embeds Zscaler’s inspection stack inside its MPLS and internet backbones, offering managed security services that integrate billing, connectivity, and support under one SLA. Microsoft’s Azure marketplace now lists bundled SWG-and-identity packages, enabling one-click procurement that automatically attaches usage charges to existing cloud commitments. AWS and Google Cloud follow similar paths, cementing cloud-service provider influence over routing choices. As these alliances mature, legacy appliance makers face margin compression, pushing them to reposition hardware as edge accelerators rather than standalone solutions.

Secured Web Gateway Industry Leaders

Zscaler Inc.

Cisco Systems Inc. (Cisco Umbrella)

Broadcom Inc. (Symantec Enterprise Division)

Netskope Inc.

Fortinet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Fortinet launched the FortiGate 700G next-generation firewall, delivering 7× higher throughput and 7× lower power use, while adding post-quantum cryptography readiness.

- June 2025: Check Point recruited 2,000+ new partners after revamping its partner program, driving a 30% jump in deal registrations.

- June 2025: Fortinet expanded its AI-powered workspace security suite, adding FortiMail Workspace Security and FortiDLP for Microsoft 365 and Google Workspace.

- May 2025: Cyera raised USD 300 million in Series D funding at a USD 3 billion valuation to scale its data-security posture-management platform.

Global Secured Web Gateway Market Report Scope

A secure web gateway (SWG) is a security solution that prevents unauthorized internet traffic from accessing a company's internal network. Enterprises use it to protect employees and users from malicious websites, web traffic, internet-borne viruses, malware, and other cyber threats. It also aids in regulatory compliance. An SWG is intended to prevent access to and from harmful websites and links. It acts as a security gateway, enforcing granular use controls and preventing risks from accessing online applications by screening web and internet traffic at the application level.

The secured web gateway market is segmented by component (solutions, services), by organization size (large organization, small & medium organizations), by deployment (cloud, on-premise), by end user (BFSI, healthcare, manufacturing, government & defense, IT and telecommunication, other end users) and by geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa).The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Solutions |

| Services |

| Large Enterprises |

| Small and Medium Enterprises (SME) |

| Cloud |

| On-premise |

| BFSI |

| Healthcare |

| Manufacturing |

| Government and Defense |

| IT and Telecommunication |

| Professional Services |

| Education |

| Other Verticals |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | GCC Countries |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solutions | |

| Services | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SME) | ||

| By Deployment Mode | Cloud | |

| On-premise | ||

| By End-user Vertical | BFSI | |

| Healthcare | ||

| Manufacturing | ||

| Government and Defense | ||

| IT and Telecommunication | ||

| Professional Services | ||

| Education | ||

| Other Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC Countries | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the Secured Web Gateway Market?

The Secured Web Gateway Market size is expected to reach USD 20.7 billion in 2026 and grow at a CAGR of 22.62% to reach USD 57.4 billion by 2031.

What is the current Secured Web Gateway Market size?

In 2026, the Secured Web Gateway Market size is expected to reach USD 20.7 billion.

Who are the key players in Secured Web Gateway Market?

Broadcom., IBM Corporation, Fortinet, Inc., Check Point Software Technologies Ltd. and Cloudflare, Inc. are the major companies operating in the Secured Web Gateway Market.

Which is the fastest growing region in Secured Web Gateway Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Secured Web Gateway Market?

In 2025, the North America accounts for the largest market share in Secured Web Gateway Market.

What years does this Secured Web Gateway Market cover, and what was the market size in 2025?

In 2025, the Secured Web Gateway Market size was estimated at USD 20.7 billion. The report covers the Secured Web Gateway Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Secured Web Gateway Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: