Secure Elements In Consumer Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

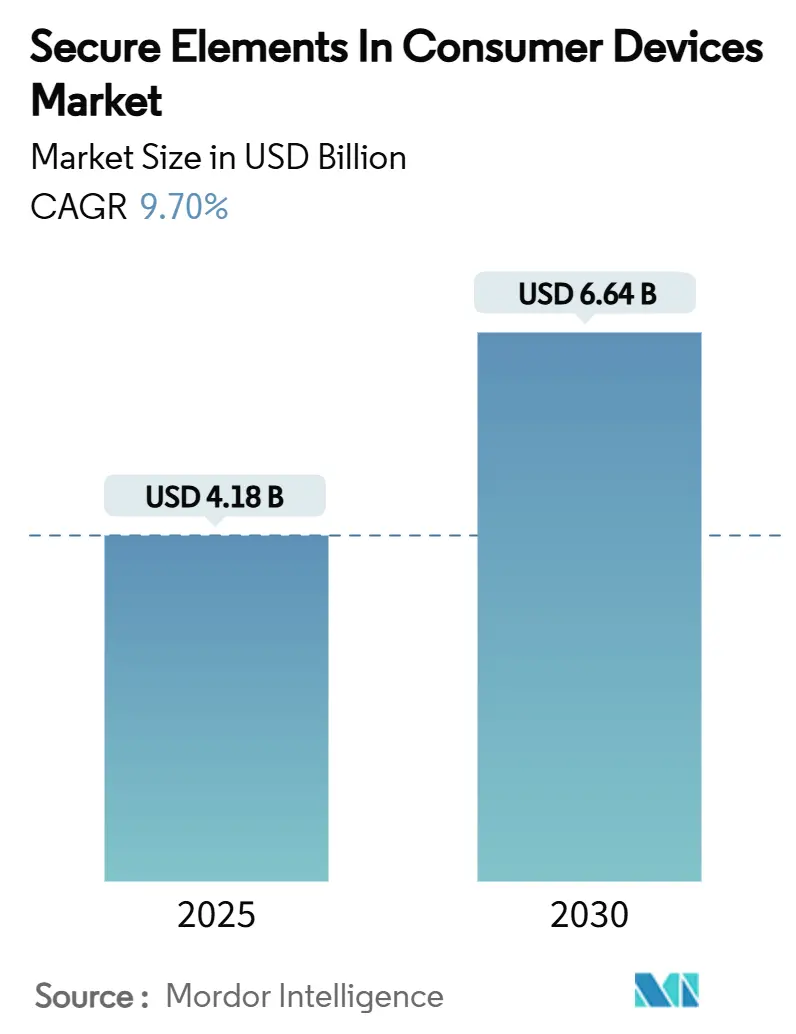

| Market Size (2025) | USD 4.18 Billion |

| Market Size (2030) | USD 6.64 Billion |

| Growth Rate (2025 - 2030) | 9.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Elements In Consumer Devices Market Analysis by Mordor Intelligence

The secure elements in consumer devices market size stands at USD 4.18 billion in 2025 and is forecast to climb to USD 6.64 billion by 2030, reflecting a 9.70% CAGR from 2025 to 2030. Momentum comes from regulatory pressure, the mainstreaming of mobile payments, and the migration of security-by-design principles from payments to broader consumer electronics. Asia-Pacific retains leadership on the back of its contract-manufacturing base, yet North America and Europe show sharp upticks tied to new IoT cybersecurity labeling rules. Semiconductor vendors are fast-tracking embedded secure element roadmaps to defend design slots while consumer OEMs pivot toward on-chip enclaves to shave board area and bill-of-materials. These converging forces collectively sustain double-digit expansion in the secure elements in consumer devices market.

Key Report Takeaways

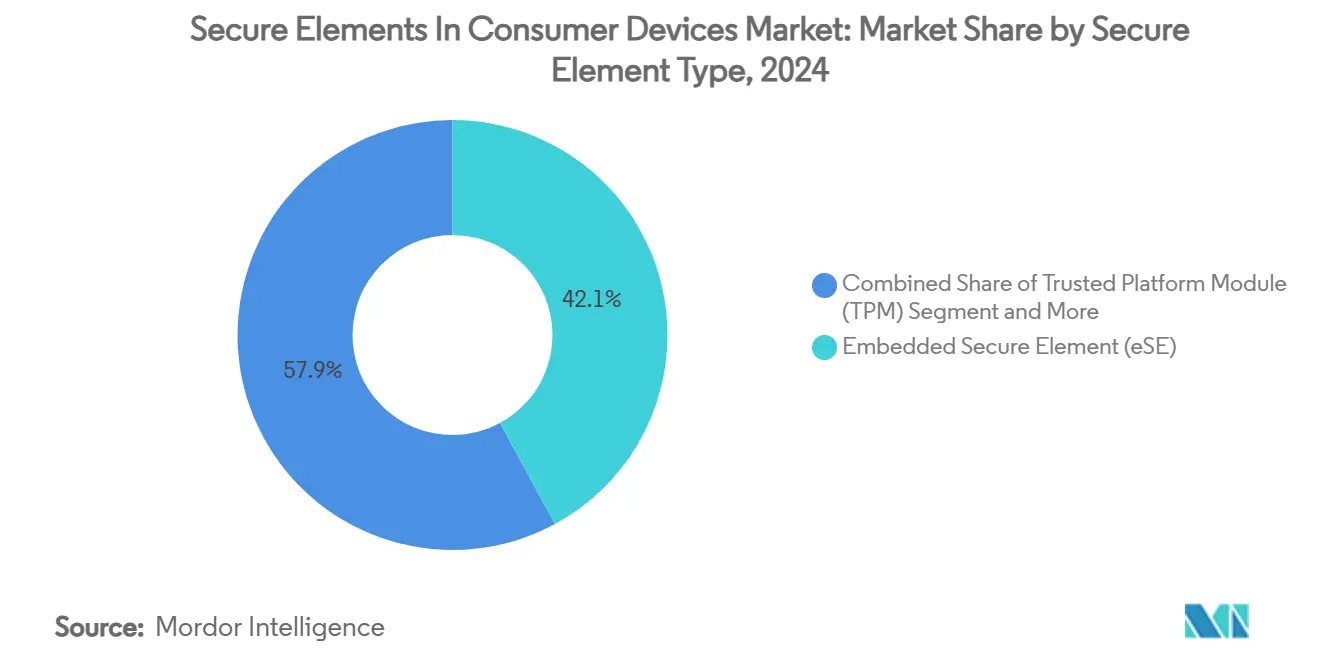

- By secure element type, embedded secure elements led with 42.1% of the secure elements in consumer devices market share in 2024, while integrated secure elements/safe enclaves are advancing at an 11.2% CAGR through 2030.

- By device category, smartphones captured 54.7% revenue share of the secure elements in consumer devices market size in 2024; smart home/IoT hubs show the fastest trajectory at 11.3% CAGR to 2030.

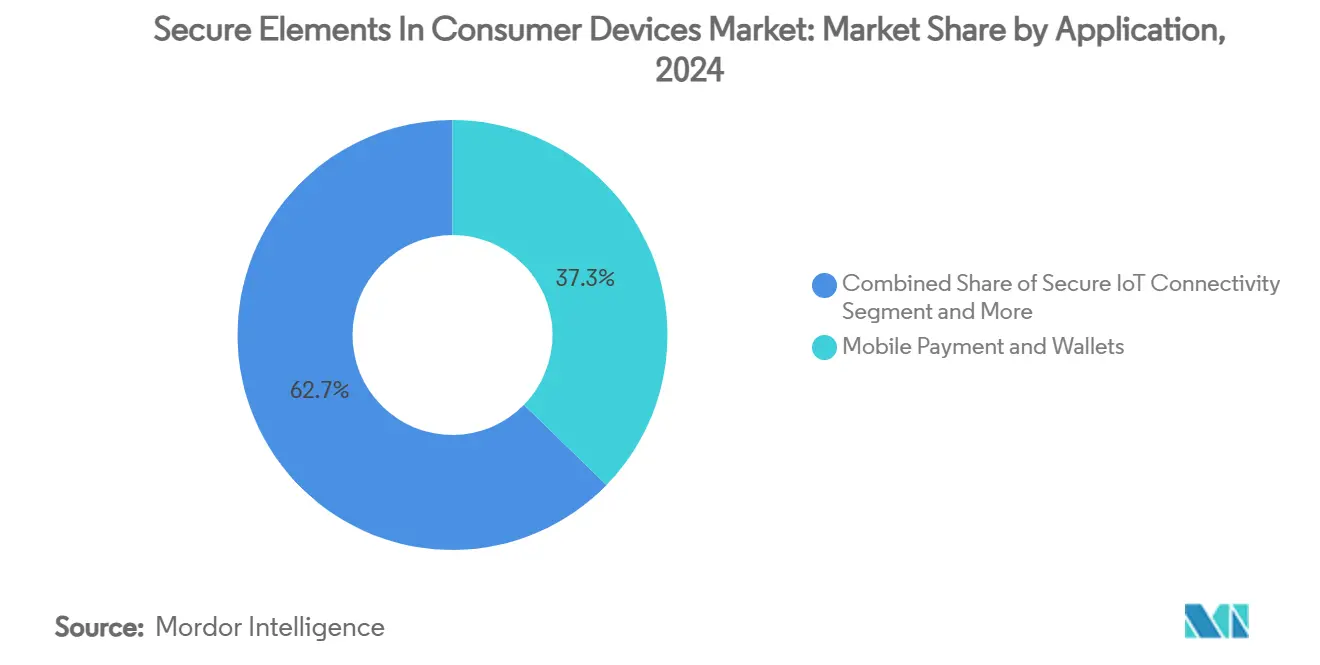

- By application, mobile payment and wallets commanded a 37.3% share of the secure elements in consumer devices market in 2024, whereas secure IoT connectivity is projected to expand at a 11.5% CAGR to 2030.

- By integration, system-on-chip deployment held 48.7% of the secure elements in consumer devices market share in 2024, and embedded SIM is forecast to grow at 11.8% CAGR during 2025-2030.

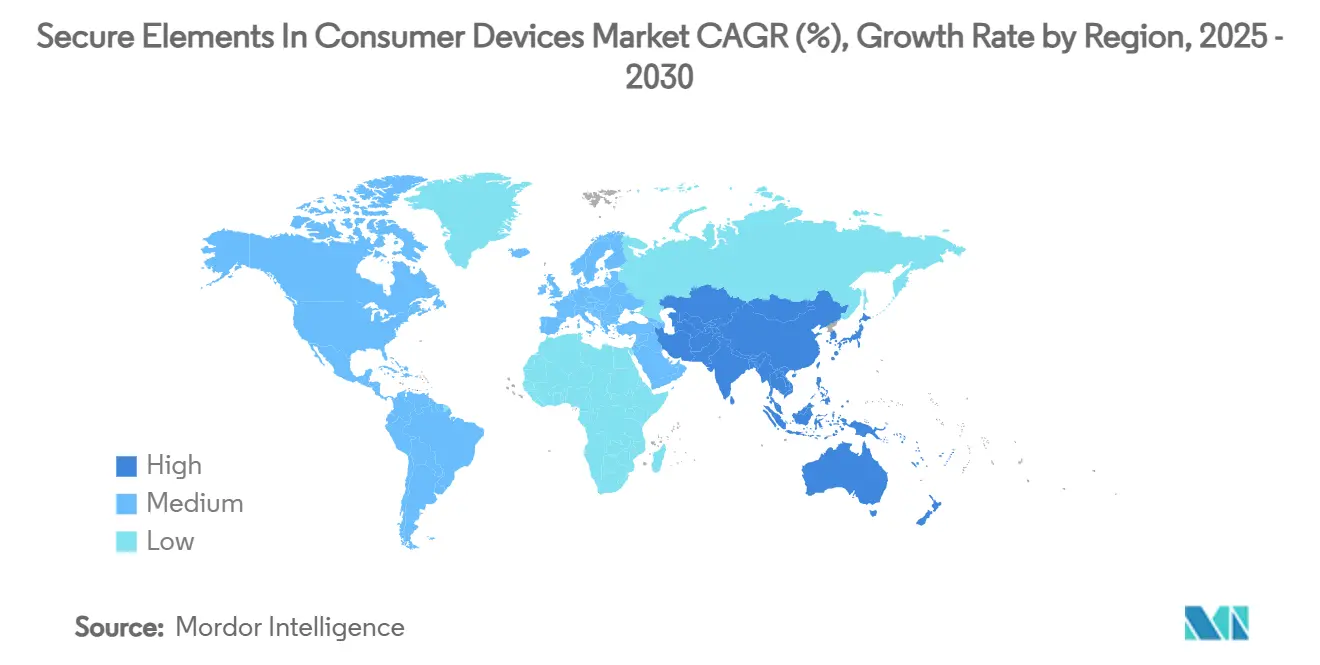

- By geography, Asia-Pacific accounted for 40.1% of overall revenue in 2024, with the region also recording the highest forecast CAGR at 11.0% to 2030.

Global Secure Elements In Consumer Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of mobile payments and NFC wallets | +2.1% | Global, with acceleration in APAC and Europe | Medium term (2-4 years) |

| Integration of eSIM in mid-tier and entry smartphones | +1.8% | Global, slower adoption in China and India | Long term (≥ 4 years) |

| Consumer IoT device security mandates (EU CRA, U.S. IoT Cyber Label) | +2.3% | North America and EU, spillover to APAC | Short term (≤ 2 years) |

| Premium-tier laptops shifting to TPM 2.0 post-Windows 11 | +1.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| On-device credential storage for digital ID/passports | +1.6% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Rise of ultra-wideband (UWB) digital keys for cars and smart locks | +1.5% | North America and Europe, premium automotive segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of mobile payments and NFC wallets

Consumers accelerated contactless payment uptake, elevating transaction volumes in wallets linked to biometric authentication and tokenized card credentials. [1]Visa, “Mobile Wallets Are Becoming Universal,” visa.com Merchants benefit from reduced checkout friction, while device makers migrate from removable secure elements to embedded solutions supporting multi-scheme credentials. Fintech convergence fosters new revenue models that favor secure-element-backed token provisioning. Asia-Pacific and Europe remain the testing grounds for super-apps that bundle payments, mobility, and loyalty, inflating attach rates of secure components in mid-range phones. The secure elements in the consumer devices market, therefore, gain durable tailwinds as wallet ubiquity becomes the de facto baseline for hardware design.

Integration of eSIM in mid-tier and entry smartphones

eSIM shipments multiplied tenfold between 2018 and 2023 as tier-one OEMs eliminated physical SIM trays. [2]GSMA, “eSIM Summit Deck,” gsma.com Operators now target 37% of cellular IoT links on eSIM by 2030. Energy-efficient 28 nm eSIM ICs cut power draw by 50%, making them viable for budget Android handsets. Yet uneven regulatory stances in China and cost sensitivities in India limit penetration, creating a bifurcated opportunity set. For vendors, integrating eSIM logic inside application processors tightens control of the secure elements in the consumer devices market.

Consumer IoT device security mandates

The EU Cyber Resilience Act introduces penalties of EUR 15 million or 2.5% of global turnover for non-compliance, pushing OEMs to hard-wire certified secure elements by late 2027. The US Cyber Trust Mark applies NIST baselines to routers, cameras, and smart speakers. Compliance pathways favor tamper-resistant storage of credentials and signed firmware, adding immediate upside to the secure elements in the consumer devices market. Supply-chain transparency tools, including SBOM repositories, further elevate hardware-root-of-trust requirements.

Premium-tier laptops shifting to TPM 2.0 post-Windows 11

Microsoft mandates TPM 2.0 for new Windows 11 installs, extending a hardware root of trust to more than 300 million notebooks shipped annually. Corporate buyers tighten zero-trust architectures around BitLocker and Windows Hello, ratcheting demand for discrete TPM sockets and integrated enclaves inside PC chipsets. Semiconductor roadmaps blend TPM logic with advanced MRAM on 16 nm MCU nodes to future-proof secured-core PCs, reinforcing growth in the secure elements in the consumer devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost sensitivity in low-end consumer electronics | -1.6% | APAC core, spillover to MEA and Latin America | Long term (≥ 4 years) |

| Fragmented standards across payment, ID and IoT ecosystems | -1.3% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Supply-chain concentration in 200mm secure MCU fabs | -1.2% | Global, with acute impact in automotive and industrial | Medium term (2-4 years) |

| Side-channel attack disclosures eroding OEM confidence | -0.9% | Global, particularly affecting premium device segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost sensitivity in low-end consumer electronics

Entry-level phones and wearables face single-digit ASP ceilings that discourage discrete secure element adoption. Board space and component cost trade-offs steer OEMs toward software keys or integrated enclaves. China’s delayed eSIM green-lighting further dampens volume prospects. Nevertheless, regulatory deadlines start to push even budget SKUs toward minimum hardware security, partially offsetting this headwind for the secure elements in the consumer devices market.

Supply-chain concentration in 200 mm secure MCU fabs

Only a handful of foundries certify lines for CC EAL 6+ secure ICs, and those same 200 mm tools now chase power semiconductor backlogs. SEMI forecasts 14% capacity growth by 2026 yet warns of persistent lead-time elongation. [3]SEMI, “Global 200 mm Fabs to Reach Record High Capacity by 2026,” semi.org Automotive electrification soaks up new slots, squeezing consumer IC availability and stoking price volatility. Vendors hedge via multi-site qualification, but geopolitical export controls still expose procurement risk that tempers upside in the secure elements in consumer devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Secure Element Type: Embedded solutions drive integration

Embedded secure elements held 42.1% of the secure elements in consumer devices market share in 2024 as OEMs eliminated discrete cards while preserving tamper resistance. Integrated secure elements, the fastest-growing cohort, post an 11.2% CAGR on the back of enclave features in mobile APs and PC chipsets. Discrete TPMs see a volume rebound under Windows 11 mandates, whereas removable MicroSD form factors remain niche. Convergence toward system-in-package enables mixed-signal integration without compromising certification paths. Samsung’s quantum-safe Knox Vault exemplifies the push to future-proof embedded designs.

Volume migration to integrated silicon shrinks footprint and BOM yet raises certification complexity, prompting alliances between IP vendors and test labs. Post-quantum cryptography readiness increasingly differentiates secure element portfolios. Overall, embedded architectures cement their role as the performance-per-watt benchmark, reinforcing dominance within the secure elements in consumer devices market.

By Device Category: Smartphones lead, IoT hubs accelerate

Smartphones generated 54.7% of segment revenue in 2024, reflecting wallet ubiquity and biometric unlock features tied to hardware roots of trust. Smart home/IoT hubs expand at 11.3% CAGR as EU and US cybersecurity labels mandate secure firmware updates. Wearables gain share via contactless payments and health data protection, aided by ultra-miniature SECORA Connect modules.

Gaming consoles leverage custom security processors to thwart piracy, whereas connected appliances emerge as regulation-driven adopters. Smartphones will retain a bulk share, yet non-phone devices collectively outpace handset growth, diversifying opportunities in the secure elements in consumer devices market.

By Application: Mobile payments dominate, IoT security surges

Mobile payment and wallets comprised 37.3% of demand in 2024. However, secure IoT connectivity accelerates at 11.5% CAGR, propelled by smart-city rollouts and industrial automation use-cases. Digital ID pilots in Germany and South Korea showcase government endorsement of smartphone credential storage.

DRM, device authentication, and anti-counterfeit tags round out mid-single-digit growth niches. Automotive digital keys gain momentum through UWB-enabled smartphones that pair with door ECUs, underscoring cross-industry appetite for certified secure storage. The secure elements in consumer devices market thus broaden beyond fintech into identity, content, and mobility sectors.

By Integration: SoC dominance, eSIM acceleration

System-on-chip embedded security engines captured 48.7% share in 2024, with phone and PC AP vendors embedding ARM TrustZone-style islands. Embedded SIM rises fastest at 11.8% CAGR as IoT device makers cut SKU complexity. Discrete stand-alone chips maintain footholds in applications requiring independent certification.

SiP hybrids blend radio, MCU, and security blocks for wearables, while removable implementations recede amid reliability issues. Integrated approaches will remain the default, yet discrete devices persist where the highest assurance is mandatory, ensuring multi-track growth within the secure elements in consumer devices market.

Geography Analysis

Asia-Pacific held 40.1% of the secure elements in consumer devices market size in 2024 and is projected to expand at a 11.0% CAGR through 2030. Asia-Pacific remains the revenue engine, but regulatory catalysts in Europe and North America redistribute margin pools. Chinese OEMs emphasize cost-optimized integrated enclaves, while Korean and Japanese brands champion quantum-safe hardware to court export markets. China’s handset output and India’s smartphone adoption underpin volume, even as eSIM restrictions temper uptake.

In the European Union, product conformity assessments drive microcontroller replacement cycles and stimulate local test lab services. Europe’s Cyber Resilience Act accelerates secure-element inclusion across white goods and gateways, whereas North America sees TPM and smart-home certification gains. The United States’ voluntary label scheme influences retailer stocking decisions, nudging smart speakers, cameras, and thermostats toward certified chips. Latin America leans on contactless transit and government ID digitization to justify secure element spend, whereas Middle East megaprojects integrate secure gateways into city platforms. Supply-chain localization policies further encourage multi-fab diversification, ensuring regional balancing acts in the secure elements in consumer devices market. Regional divergence in telecom rules and component subsidies will shape manufacturer sourcing strategies across the forecast horizon.

Competitive Landscape

The market shows moderate concentration: the top five players account for roughly 65% of global revenue. NXP, Infineon, and STMicroelectronics maintain leadership through vertical integration that spans IC design, EAL 6+ certification, and lifecycle management services.

Recent strategy moves underscore platform consolidation. In July 2025, STMicroelectronics agreed to acquire part of NXP’s sensor unit for USD 950 million to cross-sell security MCU IP. Samsung baked quantum-resistant encryption into Galaxy S25, reinforcing device differentiation. Infineon released the 28 nm OPTIGA eSIM cutting energy draw by 50%, targeting mid-tier phones.

White-space entrants focus on post-quantum TPM chips; SEALSQ earmarked USD 35 million for R&D and eyes Q4 2025 launches. [4]SEALSQ, “FY 2024 Results and Strategic Growth Plan,” sealsq.com Nordic Semiconductor’s nRF54L family secured PSA Level 3 certification while tripling Bluetooth LE efficiency. Cadence’s purchase of Secure-IC in 2025 signals EDA vendors’ intent to embed security IP earlier in SoC flows.

Competitive intensity revolves around reducing die area, slashing standby power, and bundling device-cloud lifecycle software. Vendors able to certify at scale across multiple geographies stand to widen lead positions within the secure elements in consumer devices market.

Secure Elements In Consumer Devices Industry Leaders

NXP Semiconductors N.V.

Infineon Technologies AG

STMicroelectronics N.V.

Samsung Electronics Co., Ltd.

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: STMicroelectronics to purchase part of NXP’s sensor business for up to USD 950 million.

- July 2025: Samsung unveiled Knox Enhanced Encrypted Protection and quantum-safe Wi-Fi for mobile devices.

- July 2025: Infineon introduced OPTIGA Connect Consumer OC1230, the world’s smallest eSIM solution.

- March 2025: NXP launched 16 nm S32K5 automotive MCUs with an integrated EdgeLock secure enclave.

- February 2025: Samsung brought post-quantum cryptography to Galaxy S25 smartphones.

- January 2025: Cadence announced the acquisition of Secure-IC to bolster embedded security IP.

- January 2025: Microchip committed USD 880 million to expand SiC and silicon capacity in Colorado.

Global Secure Elements In Consumer Devices Market Report Scope

| Embedded Secure Element (eSE) |

| Integrated Secure Element (iSE)/Secure Enclave |

| SIM-based Secure Element (eSIM/uSIM) |

| Trusted Platform Module (TPM) |

| Removable Secure Element (MicroSD Form Factor) |

| Smartphones |

| Wearables (Smartwatches, Fitness Bands) |

| Tablets and E-readers |

| Laptops and PCs |

| Smart Home/IoT Hubs |

| Gaming Consoles and VR Headsets |

| Connected Consumer Appliances |

| Other Devices |

| Mobile Payment and Wallets |

| Digital ID and eGovernment Credentials |

| Content Protection and DRM |

| Device Authentication and Anti-Counterfeit |

| Secure IoT Connectivity |

| Automotive Digital Keys and Infotainment |

| Other Applications |

| Discrete Stand-Alone Chip |

| System-in-Package (SiP) |

| Integrated into SoC/Secure Enclave |

| Embedded SIM (eSIM) |

| Removable (MicroSD) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Secure Element Type | Embedded Secure Element (eSE) | ||

| Integrated Secure Element (iSE)/Secure Enclave | |||

| SIM-based Secure Element (eSIM/uSIM) | |||

| Trusted Platform Module (TPM) | |||

| Removable Secure Element (MicroSD Form Factor) | |||

| By Device Category | Smartphones | ||

| Wearables (Smartwatches, Fitness Bands) | |||

| Tablets and E-readers | |||

| Laptops and PCs | |||

| Smart Home/IoT Hubs | |||

| Gaming Consoles and VR Headsets | |||

| Connected Consumer Appliances | |||

| Other Devices | |||

| By Application | Mobile Payment and Wallets | ||

| Digital ID and eGovernment Credentials | |||

| Content Protection and DRM | |||

| Device Authentication and Anti-Counterfeit | |||

| Secure IoT Connectivity | |||

| Automotive Digital Keys and Infotainment | |||

| Other Applications | |||

| By Integration | Discrete Stand-Alone Chip | ||

| System-in-Package (SiP) | |||

| Integrated into SoC/Secure Enclave | |||

| Embedded SIM (eSIM) | |||

| Removable (MicroSD) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the secure elements in consumer devices market by 2030?

The market is expected to reach USD 6.64 billion by 2030.

Which device category generates the largest revenue?

Smartphones accounted for 54.7% of 2024 revenue due to widespread wallet and biometric adoption.

Which application segment is growing the fastest?

Secure IoT connectivity leads with an 11.5% CAGR forecast for 2025-2030.

Why are embedded secure elements gaining share?

They save board space and cost while preserving tamper resistance, capturing 42.1% market share in 2024.

How do new regulations affect demand?

EU and US cybersecurity mandates require certified hardware roots of trust, accelerating secure element integration across consumer IoT devices.

What integration approach is most common?

Security logic embedded inside system-on-chip processors held 48.7% share in 2024 and remains the dominant pathway.

Page last updated on: