Secure Boot And Firmware Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

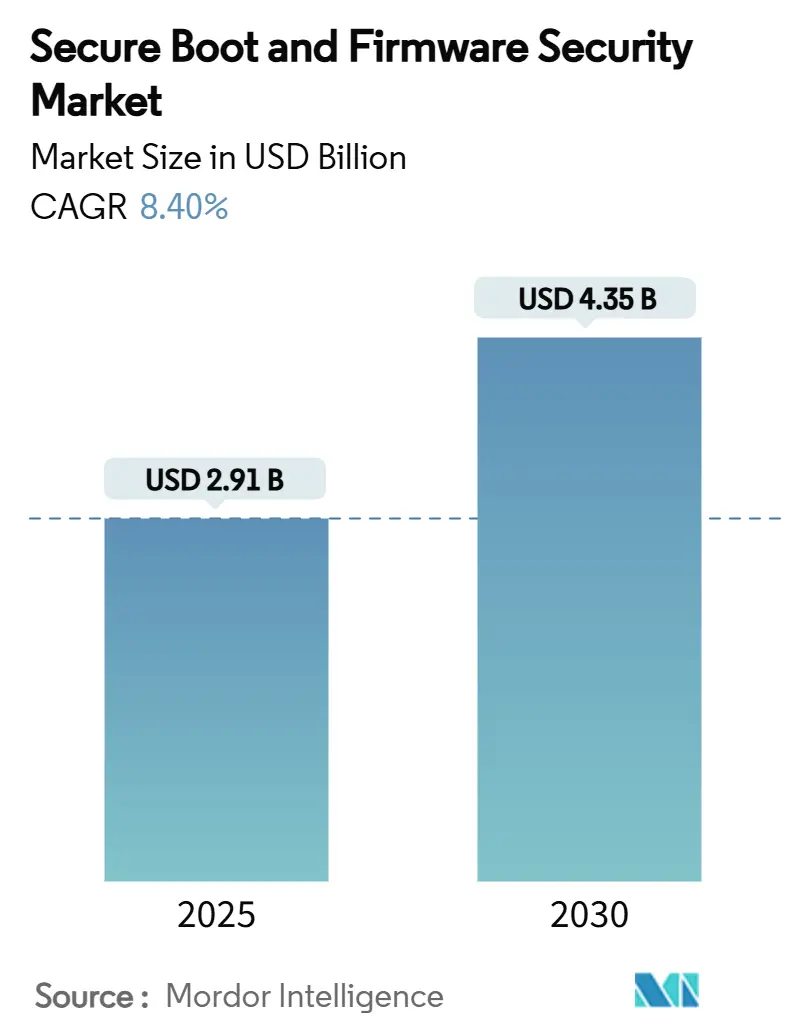

| Market Size (2025) | USD 2.91 Billion |

| Market Size (2030) | USD 4.35 Billion |

| Growth Rate (2025 - 2030) | 8.40% CAGR |

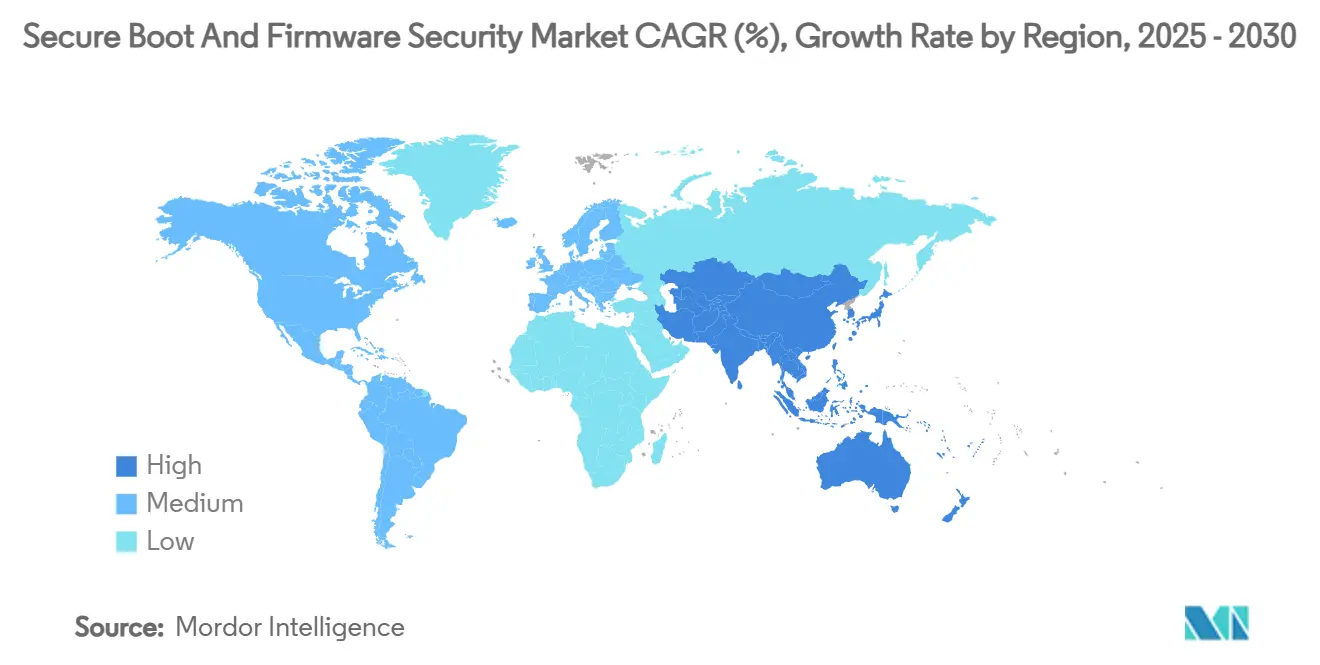

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Boot And Firmware Security Market Analysis by Mordor Intelligence

The secure boot and firmware security market size reached USD 2.91 billion in 2025 and is forecast to climb to USD 4.35 billion by 2030, reflecting an 8.40% CAGR during 2025-2030. Hardware-anchored trust establishment, tightening global regulations, and highly publicized supply-chain attacks are pushing enterprises to embed verification at the silicon layer rather than rely on software defences alone. In North America, secured-core server and PC rollouts accelerate demand, while Asia-Pacific rides domestic chip initiatives and industrial IoT upgrades to become the fastest-growing region. Silicon-based roots of trust currently dominate revenues, yet over-the-air (OTA) firmware update frameworks are scaling fastest as connected devices require continuous patching across dispersed fleets. Competitive intensity is moderate; incumbent BIOS suppliers are forging alliances with security specialists to close skills gaps, and semiconductor vendors are using confidential computing features to differentiate at the data-center edge.

Key Report Takeaways

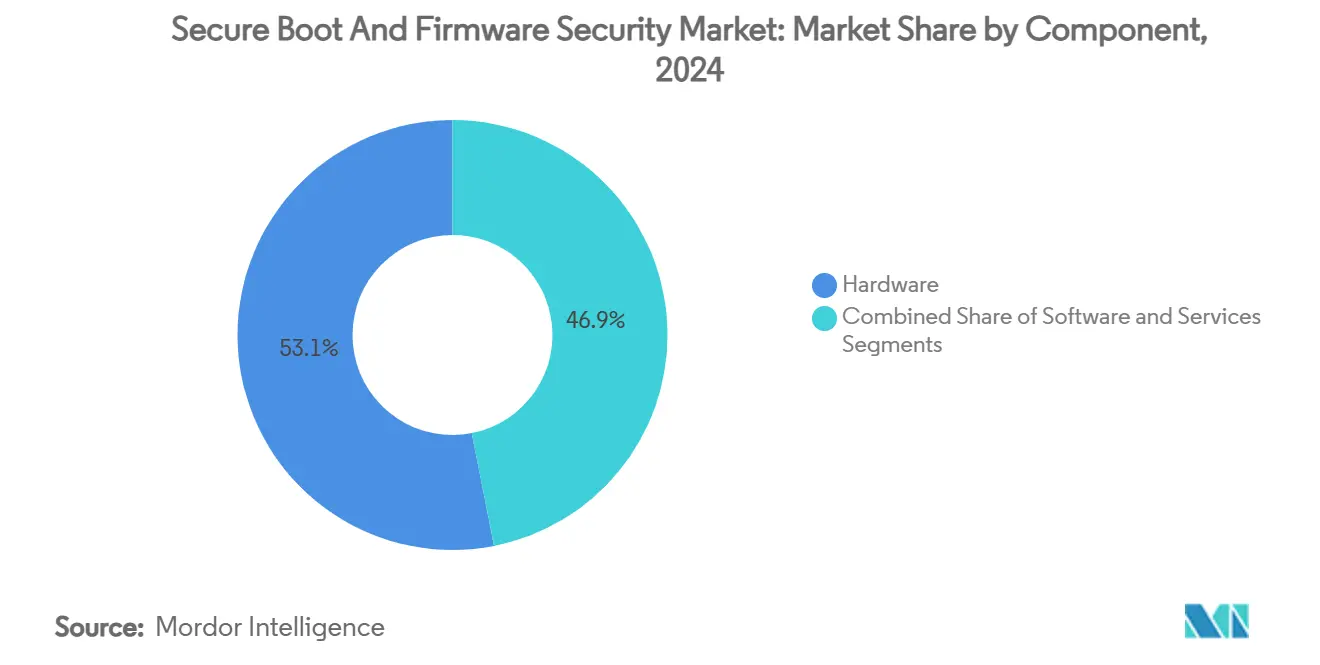

- By component, hardware captured 53.1% of secure boot and firmware security market share in 2024, while software solutions are projected to expand at a 10.2% CAGR to 2030.

- By device type, servers and data-center systems led with 30.7% revenue share of the secure boot and firmware security market in 2024; IoT and embedded systems are advancing at a 9.6% CAGR through 2030.

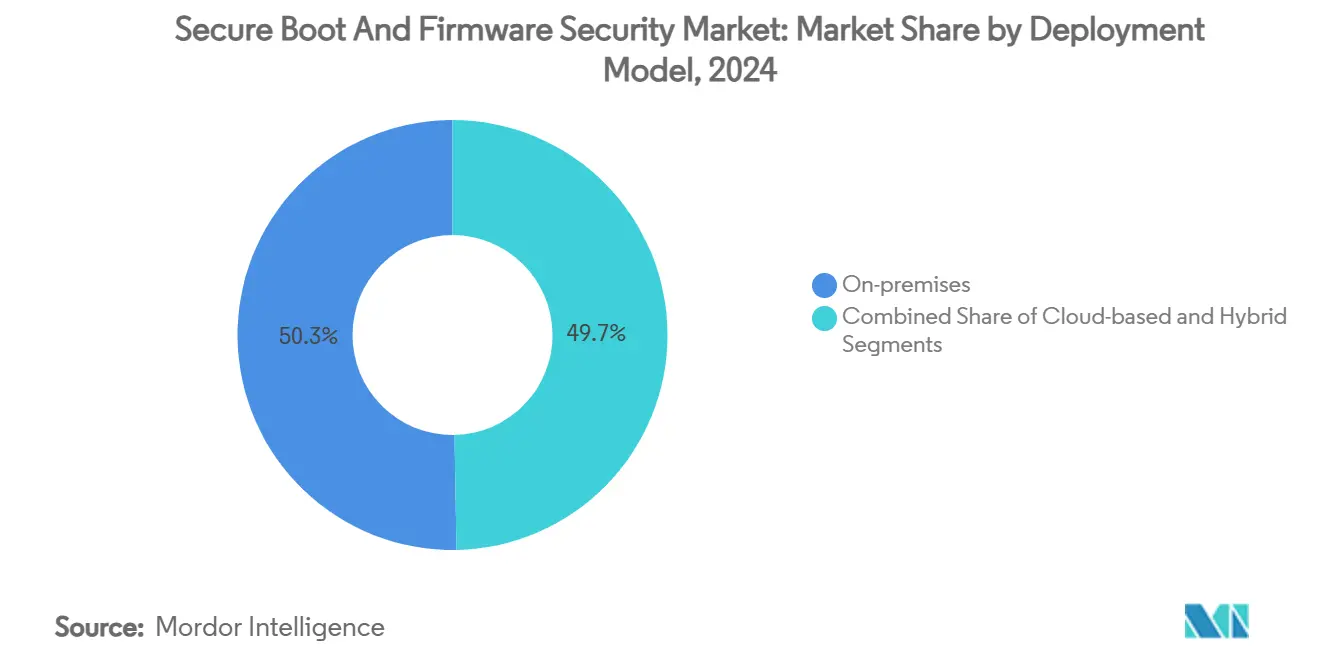

- By deployment model, on-premises implementations accounted for 50.3% of the secure boot and firmware security market size in 2024, whereas cloud-based deployments are set to grow at a 10.5% CAGR to 2030.

- By end-use industry, IT and telecommunications held 28.7% of 2024 revenue; automotive is forecast to expand at a 9.7% CAGR up to 2030 in the secure boot and firmware security market.

- By security technology, secure boot commanded 31.1% of 2024 spending in the secure boot and firmware security market, while secure firmware update (OTA) is poised for a 9.9% CAGR between 2025-2030.

- By geography, North America led with a 39.1% share of the secure boot and firmware security market in 2024, and Asia-Pacific is projected to log a 10.0% CAGR through 2030.

Global Secure Boot And Firmware Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of secured-core PCs by OEMs | +1.2% | North America and EU | Medium term (2-4 years) |

| Regulatory mandates on hardware root-of-trust for critical infrastructure | +1.8% | Global | Long term (≥ 4 years) |

| Expansion of zero-trust architecture to firmware layer | +1.5% | North America and EU | Medium term (2-4 years) |

| Uptake of over-the-air secure firmware update frameworks | +1.3% | Global | Short term (≤ 2 years) |

| Adoption of confidential computing GPUs driving secure boot in data centers | +0.9% | Global | Medium term (2-4 years) |

| Shift to Rust-based firmware development reducing memory-safety bugs | +0.7% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Secured-core PCs by OEMs

Microsoft’s Windows 11 baseline requirements for TPM 2.0 and UEFI Secure Boot have pushed OEMs to redesign laptops, desktops, and enterprise workstations around silicon-anchored trust. Dell, HP, and Lenovo now market secured-core configurations as default offerings to corporate buyers seeking firmware resilience that traditional endpoint protection cannot deliver. [1]Karen Spiegelman, “Microsoft Brings Zero Trust to Hardware in Windows 11,” Dark Reading, darkreading.com Server portfolios follow the same path: Dell’s PowerEdge and HPE’s ProLiant families embed persistent silicon roots of trust that authenticate every firmware component before execution. The strategy elevates firmware controls from optional add-ons to table stakes, thereby expanding the secure boot and firmware security market across client and data-center devices.

Regulatory Mandates on Hardware Root-of-Trust for Critical Infrastructure

The EU Cyber Resilience Act obliges connected-device makers to implement secure boot, while China’s 2025 cybersecurity measures require domestic chips with embedded security features in government procurements. [2]James Gong, “China Cybersecurity and Data Protection: June 2025,” Bird & Bird, twobirds.com Parallel mandates in the energy and transport sectors compel operators to log cryptographic attestations for every firmware update. In automotive, UN Regulation 155 obliges OEMs to demonstrate a secure boot on electronic control units before vehicle type approval. Converging statutes create a synchronized compliance wave that forces suppliers worldwide to prioritize silicon-based trust anchors in product roadmaps, reinforcing long-run market demand.

Expansion of Zero-Trust Architecture to Firmware Layer

Zero-trust strategies now treat device firmware as a critical control plane rather than an afterthought. Cisco, Red Hat, and Microsoft integrate secure boot attestation into endpoint posture checks to verify that no policy exemptions occur before network access is granted. Continuous runtime measurement extends these assurances beyond boot, enabling infrastructure teams to revoke access if firmware drift arises. The shift embeds secure boot telemetry into identity and access workflows, enlarging the secure boot and firmware security market as enterprises refresh hardware to achieve full-stack verification.

Uptake of Over-the-Air Secure Firmware Update Frameworks

Connected cars, industrial robots, and smart appliances require trusted updates delivered without physical intervention. Frameworks such as Uptane and HARMAN OTA 12.0 sign every payload and validate device state before install, ensuring that only manufacturer-approved code runs in production. Automotive OEMs are thus migrating to centralized update orchestration that spans multiple electronic control units, while semiconductor suppliers integrate OTA-ready bootloaders to streamline compliance. The operational value of automated patching drives double-digit growth in secure firmware update sub-segments.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persisting leakage of OEM platform keys ("PKfail" incidents) | -1.1% | Global | Short term (≤ 2 years) |

| Fragmented supply-chain creating verification blind-spots | -0.8% | Global | Medium term (2-4 years) |

| High integration cost for legacy industrial controllers | -0.6% | North America and EU | Medium term (2-4 years) |

| Limited availability of formal assurance talent and tools | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persisting Leakage of OEM Platform Keys (“PKfail” Incidents)

Research by Binarly showed that more than 200 device families shipped with test platform keys still installed in production, allowing attackers to load unsigned firmware and bypass secure boot. The incident dented buyer confidence and forced emergency patch cycles, delaying some planned refresh projects. Although vendors coordinated remedial updates, the episode highlights how a single mismanaged key can neutralize an entire trust architecture, restraining market momentum until governance processes improve.

Fragmented Supply-Chain Creating Verification Blind-Spots

System boards, BIOS images, drivers, and management controllers often originate from different suppliers, lacking common signing policies. Mismatched key lifecycles introduce silent gaps where malicious payloads can persist across firmware updates. Industrial control manufacturers struggle most because long component lifetimes and proprietary field-bus protocols complicate patching. Additional certification layers inflate cost and elongate deployment timelines, curbing adoption in budget-sensitive sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Silicon-Based Security

Hardware captured 53.1% of 2024 revenue, underlining buyer preference for immutable trust anchors like TPM 2.0 chips and secure microcontrollers. Infineon’s OPTIGA Trust M exemplifies discrete components easily integrated into consumer and industrial IoT boards. [3]Infineon Technologies, “OPTIGA Trust M,” infineon.com Software platforms grow fastest at 10.2% CAGR as enterprises seek centralized dashboards that inventory firmware versions, schedule OTA patches, and automate CVE mapping. Services remain smallest in value yet play an outsized role in complex rollouts, especially where legacy assets require bespoke bootloaders. Collectively, the mix reinforces hardware primacy while opening opportunities for managed firmware operations.

The secure boot and firmware security market size for hardware components is projected to remain above the 50% threshold through 2030, even as automated remediation tools proliferate. Software revenue acceleration nonetheless reflects demand for remote attestation and analytics that translate low-level measurements into actionable risk scores. Vendors offering combined hardware-plus-software bundles position best positioned to capture cross-selling synergies.

By Device Type: Data Centers Lead While IoT Accelerates

Servers and data-center systems generated 30.7% of 2024 spending owing to confidential computing rollouts across hyperscalers. Each rack node must attest CPU, BMC, and accelerator firmware before joining clusters, cementing secure boot as a mandatory checklist item. IoT and embedded endpoints expand at a 9.6% CAGR because factories, utilities, and consumer brands are deploying millions of sensors that must survive in hostile field conditions.

The secure boot and firmware security market share advantage for servers narrows over time as IoT volumes surge, yet data-center average selling prices keep revenues high. Automotive electronic control units also post strong growth, buoyed by UN R155 audits that treat firmware integrity as a functional-safety prerequisite.

By Deployment Model: Cloud Migration Accelerates Security Transformation

On-premises architectures held 50.3% of 2024 expenditure, reflecting regulated workloads that require local custody of cryptographic material. However, cloud models are scaling fastest at 10.5% CAGR as AWS Nitro-enclaves and Azure confidential VMs support guest-supplied keys validated by secure boot attestations. Hybrid schemes blend the two, letting customers store golden keys on-site while leveraging cloud orchestration for fleet-wide scanning.

The secure boot and firmware security market size for cloud deployments is expected to double by 2030, even though absolute control remains with on-prem systems in defence and healthcare. Vendors, therefore, package portable attest APIs that abstract environment differences, smoothing multicloud governance.

By End-Use Industry: IT Sector Leads While Automotive Surges

IT and telecommunications accounted for 28.7% of 2024 revenue as cloud operators refreshed hardware to enable hardware-rooted zero-trust onboarding. Automotive emerges as the fastest riser at 9.7% CAGR because software-defined vehicles require continual feature drops secured by OTA-validated boot chains.

The secure boot and firmware security industry also finds tailwinds in industrial automation, where Ethernet-connected PLCs expose previously air-gapped machinery. Healthcare systems accelerate adoption to comply with new FDA pre-market cybersecurity submissions that assess boot integrity.

By Security Technology: Secure Boot Foundations Enable Advanced Capabilities

Secure boot remained the largest technology layer with 31.1% of 2024 spending because it sits at the root of every firmware protection stack. OTA secure firmware update services are rising at a 9.9% CAGR, mirroring connected-device fleet growth. Measured boot, trusted execution environments, and firmware encryption act as concentric rings, each hinging on initial boot validation to ensure key secrecy. Post-quantum algorithm pilots in firmware signing scripts further differentiate premium offerings.

Consequently, vendors market integrated suites that start with secure boot attestation and extend to runtime memory guards, reducing procurement friction for enterprises that previously stitched point tools together.

Geography Analysis

North America retained 39.1% secure boot and firmware security market share in 2024, propelled by the U.S. federal zero-trust strategy and CHIPS Act incentives that encourage domestic silicon with embedded security. [4] David Perera, “Chinese Connected Car Tech Banned by Biden Administration,” bankinfosecurity.com Procurement rules for defence and critical infrastructure stipulate attested firmware, driving rapid refresh across servers, routers, and industrial control gateways. Restrictions on Chinese firmware imports imposed in March 2025 further concentrate spending with vetted suppliers, bolstering local revenue pipelines.

Asia-Pacific registers the highest regional CAGR at 10.0% through 2030. China’s pivot to indigenous processors in government PCs creates a new tier of local BIOS and TPM vendors, while Japan funds secure industrial IoT retrofits in pursuit of resilient supply chains. South Korea capitalizes on its semiconductor depth to export secure microcontrollers, and India’s smart-manufacturing schemes add volume via Make in India stipulations. Regulatory convergence around hardware roots of trust ensures that demand is not limited to premium enterprise gear but spans mid-market devices as well.

Europe sustains healthy growth under the Cyber Resilience Act and automotive UN R155 compliance. German industrial conglomerates lead the adoption of measured-boot PLCs, while Nordic telcos insist on attested 5G base-band firmware. Brexit compels UK buyers to track both EU and domestic guidance, but the underlying technical requirements remain aligned, keeping cross-border supply chains intact. Overall, geopolitical tech sovereignty drives parallel national investments, collectively enlarging the secure boot and firmware security market.

Competitive Landscape

American Megatrends International (AMI) and Phoenix Technologies dominate BIOS supply, yet PKfail backlash forced both to reform key-handling processes and co-develop patches with Microsoft. Eclypsium and Binarly differentiate by offering cloud-delivered binary analysis that uncovers malicious implants before boot. Semiconductor giants Infineon, NXP, and STMicroelectronics add cryptographic acceleration blocks to microcontrollers, turning hardware into a security value proposition rather than a commodity input.

Strategic alliances are proliferating: AMI collaborates with Samsung to embed quantum-safe encryption in PC firmware; Intel Capital led Eclypsium’s USD 62 million Series B to ensure supply-chain illumination for its data-center customers. Meanwhile, hyperscalers co-design silicon with confidential-computing hooks, compelling vendors to prove boot-time attestation compatibility. Patent races in post-quantum signing and Rust-native secure bootloaders suggest that IP leadership will increasingly determine premium pricing.

Industrial-control specialists such as Thales, Siemens, and Honeywell represent growth adjacencies; they pair domain knowledge with firmware integrity monitoring to secure operational technology networks. Medical-device OEMs form another niche where FDA submissions mandate end-to-end boot verification, drawing boutique consultancies into multimillion-dollar validation projects. Overall, market consolidation remains moderate, with room for disruptors that deliver turnkey, standards-compliant toolchains.

Secure Boot And Firmware Security Industry Leaders

Intel Corporation

Microsoft Corporation

Advanced Micro Devices, Inc.

American Megatrends International LLC

Phoenix Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Thales reported 8.1% sales growth to EUR 10.3 billion (USD 11.2 billion) on defence and avionics strength, while integrating Imperva into its cyber portfolio.

- June 2025: Samsung introduced Knox Enhanced Encrypted Protection and quantum-resistant Wi-Fi encryption to flagship smartphones.

- May 2025: Binarly exposed systemic firmware key-management failures spanning multiple OEMs.

- March 2025: The U.S. government barred critical infrastructure use of Chinese firmware products, accelerating domestic vendor qualifications.

- February 2025: AMD posted record Q4 2024 revenue of USD 7.7 billion, driven by data-center demand for confidential computing.

- January 2025: AMI and Microsoft issued coordinated patches addressing widespread PKfail test-key exposures.

Global Secure Boot And Firmware Security Market Report Scope

| Hardware |

| Software |

| Services |

| Servers and Data Center Systems |

| PCs and Workstations |

| Mobile and Hand-held Devices |

| IoT and Embedded Systems |

| Automotive Electronic Control Units |

| Industrial Controllers (PLC / DCS) |

| On-premises |

| Cloud-based |

| Hybrid |

| IT and Telecom |

| Government and Public Sector |

| Industrial and Manufacturing |

| Automotive |

| Healthcare |

| Aerospace and Defense |

| Consumer Electronics |

| Other End-use Industries |

| Secure Boot |

| Measured Boot |

| Trusted Execution Environment (TEE) |

| Firmware Encryption and Signing |

| Secure Firmware Update (OTA) |

| Hardware Root of Trust (TPM, RoT MCU) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Device Type | Servers and Data Center Systems | ||

| PCs and Workstations | |||

| Mobile and Hand-held Devices | |||

| IoT and Embedded Systems | |||

| Automotive Electronic Control Units | |||

| Industrial Controllers (PLC / DCS) | |||

| By Deployment Model | On-premises | ||

| Cloud-based | |||

| Hybrid | |||

| By End-use Industry | IT and Telecom | ||

| Government and Public Sector | |||

| Industrial and Manufacturing | |||

| Automotive | |||

| Healthcare | |||

| Aerospace and Defense | |||

| Consumer Electronics | |||

| Other End-use Industries | |||

| By Security Technology | Secure Boot | ||

| Measured Boot | |||

| Trusted Execution Environment (TEE) | |||

| Firmware Encryption and Signing | |||

| Secure Firmware Update (OTA) | |||

| Hardware Root of Trust (TPM, RoT MCU) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current global value of secure boot and firmware security solutions?

The secure boot and firmware security market size reached USD 2.91 billion in 2025.

How fast is spending on firmware security expected to grow?

Global revenue is projected to rise at an 8.40% CAGR, reaching USD 4.35 billion by 2030.

Which component category brings in the most revenue?

Hardware accounts for 53.1% of 2024 sales thanks to trust-anchor chips integrated across servers, PCs, and IoT boards.

Which region is expanding quickest?

Asia-Pacific is forecast to record a 10.0% CAGR through 2030, driven by domestic semiconductor programs and industrial IoT deployments.

Why are OTA firmware updates gaining traction?

Manufacturers need to patch distributed devices securely and remotely; OTA frameworks provide cryptographic validation that meets new regulatory mandates.

What triggered industry concern around platform key management?

The 2024 PKfail incident exposed widespread leakage of test signing keys, undermining secure boot on more than 200 device lines and prompting urgent remediation work.

Page last updated on: