Secure Digital Card Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 11.01 Billion |

| Market Size (2030) | USD 14.05 Billion |

| Growth Rate (2025 - 2030) | 4.98% CAGR |

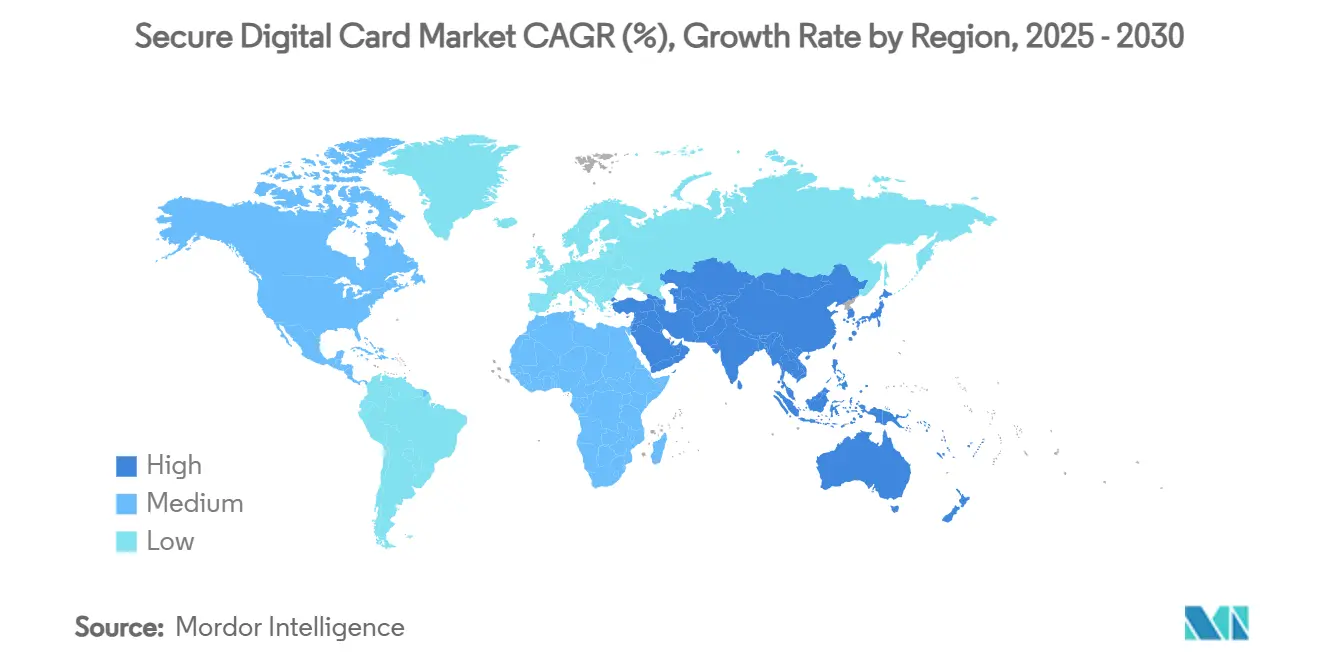

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

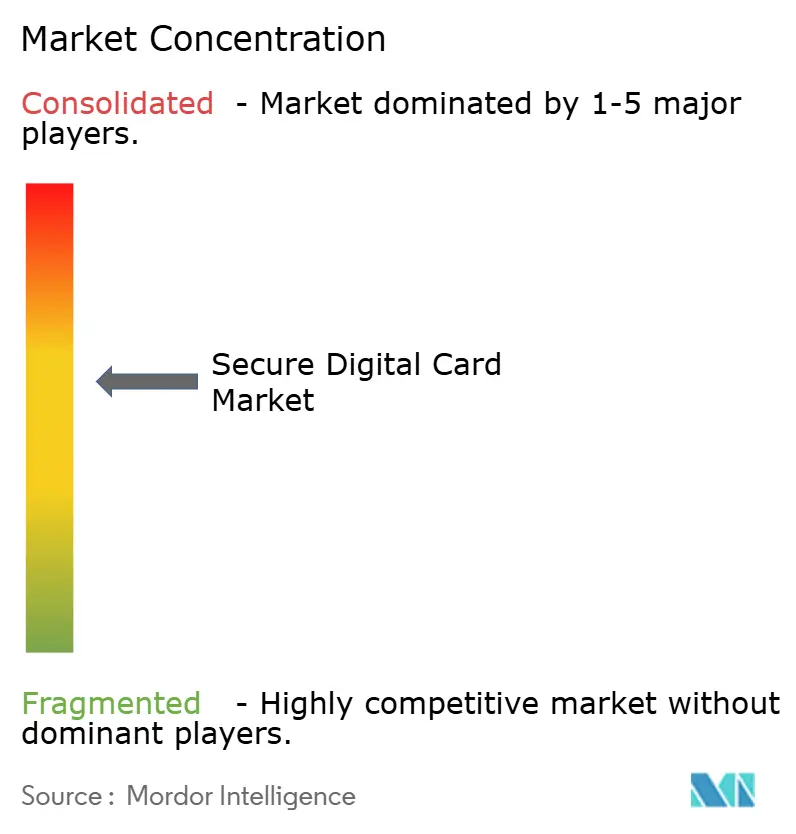

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Digital Card Market Analysis by Mordor Intelligence

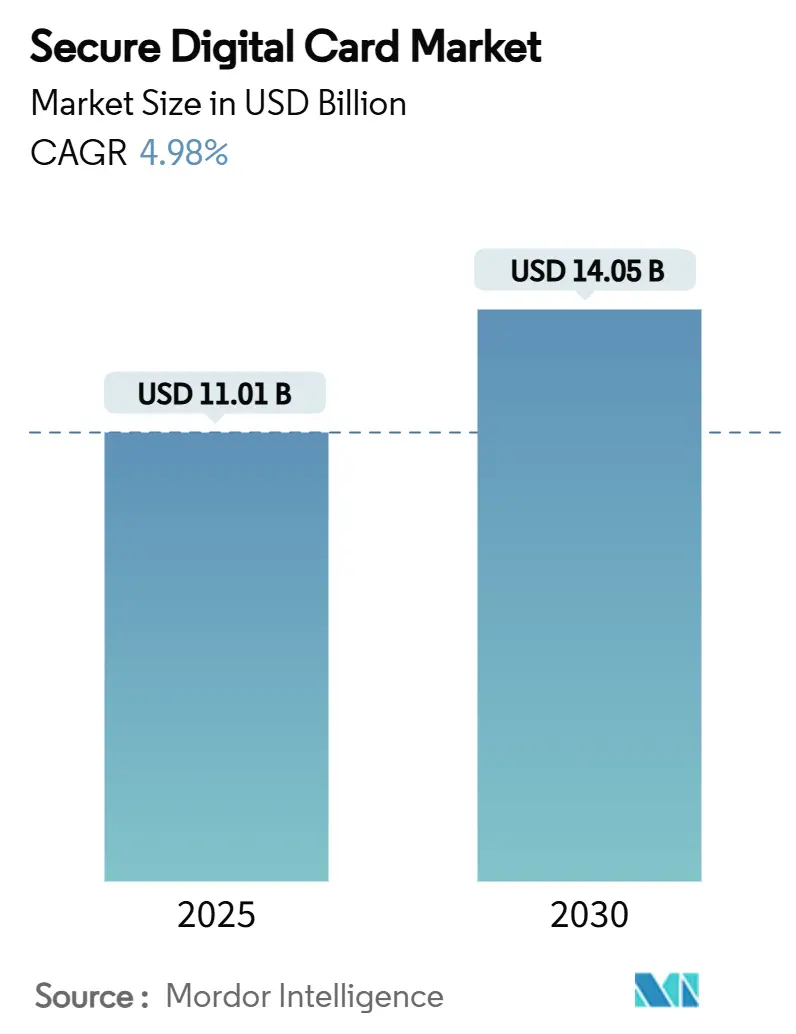

The Secure Digital Card market size stands at USD 11.01 billion in 2025 and is forecast to reach USD 14.05 billion by 2030, advancing at a 4.98% CAGR during the period. Sustained unit demand from smartphones, professional imaging devices, and embedded industrial systems keeps the Secure Digital Card market firmly on a growth footing. NVMe-class SD Express interface upgrades, stronger content-creation workflows in 8K, and the rising edge-AI footprint all translate into higher-capacity card adoption. Automotive and industrial OEMs now influence interface-speed roadmaps that were once dictated solely by consumer electronics, while regional production shifts in Asia create supply-chain efficiencies that underpin competitive pricing. On the downside, embedded UFS modules and cloud-centric storage models intensify substitution pressure, yet applications requiring field-replaceable, high-endurance media preserve tangible upside for the Secure Digital Card market.

Key Report Takeaways

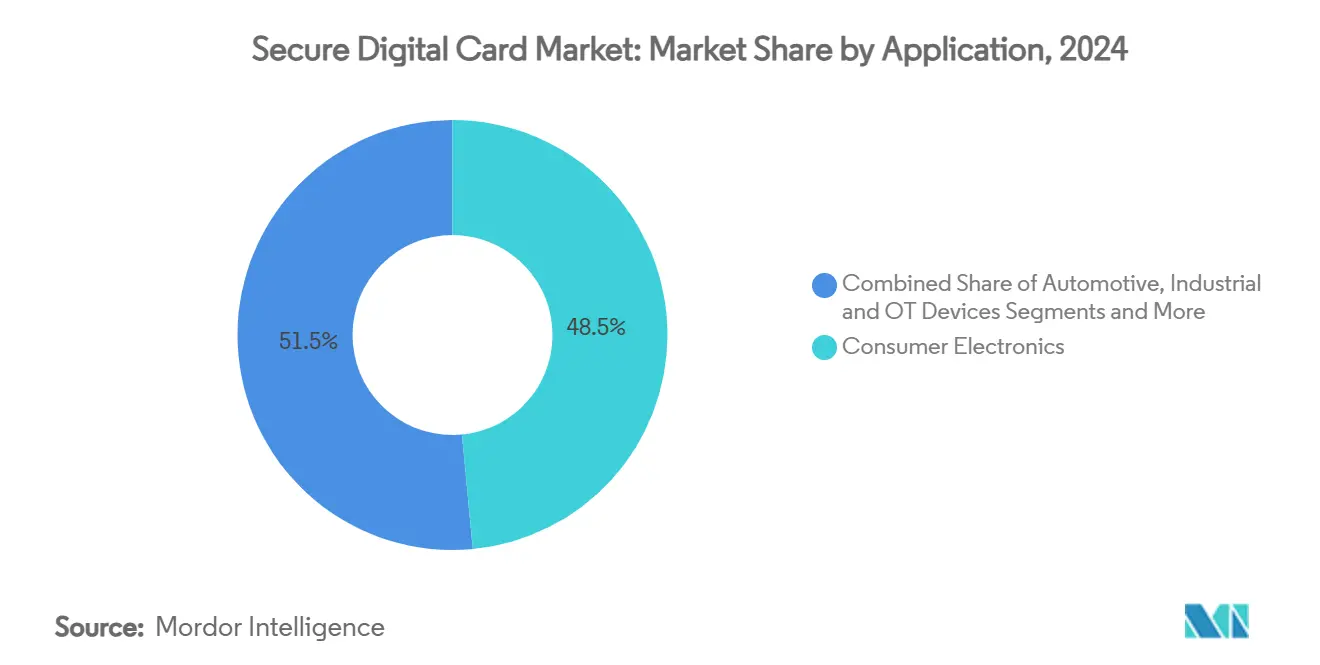

- By application, consumer electronics led with 48.5% of the Secure Digital Card market share in 2024, whereas industrial & OT devices are projected to register the fastest 5.7% CAGR through 2030.

- By form factor, microSD cards captured 55.1% of the Secure Digital Card market size in 2024 and are advancing at a 5.6% CAGR to 2030.

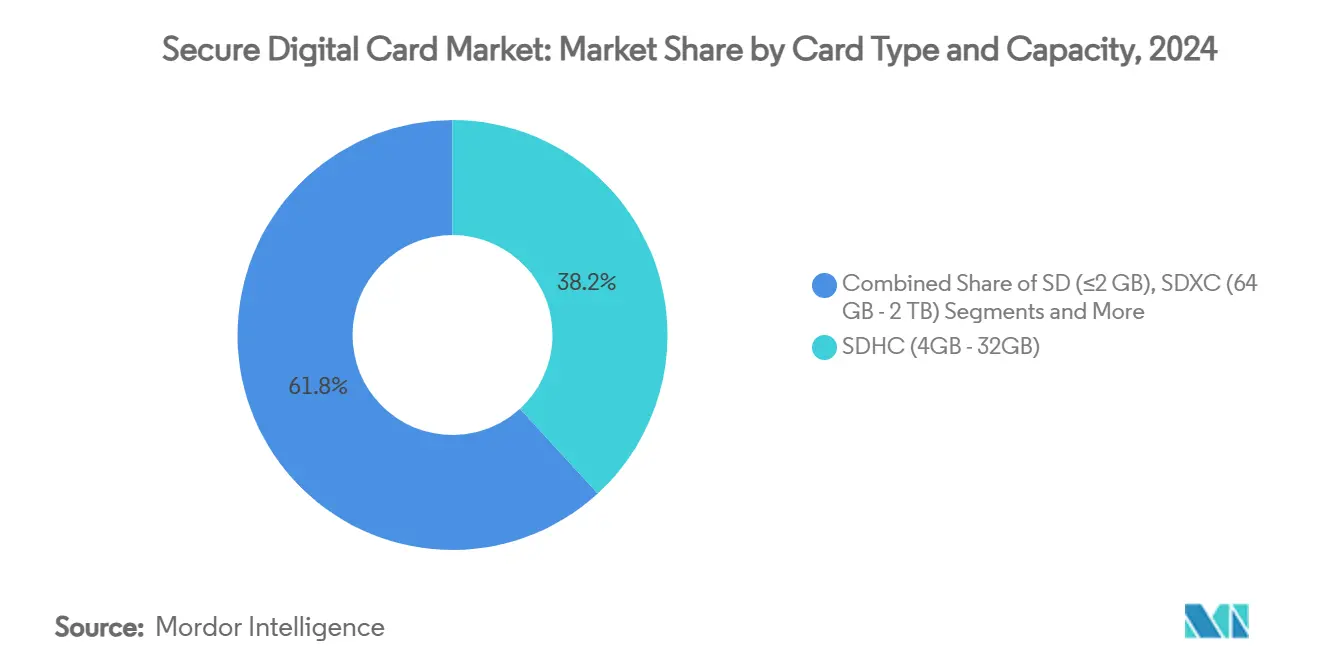

- By card type, SDHC held a 38.2% share of the Secure Digital Card market in 2024, while SDUC cards are projected to expand at a 5.3% CAGR over the forecast horizon.

- By distribution channel, offline retail controlled 62.3% Secure Digital Card market share in 2024; online/e-commerce is forecast to grow at a 5.4% CAGR to 2030.

- By geography, the Asia Pacific accounted for 46.7% of the Secure Digital Card market size in 2024 and is poised for a 5.2% CAGR through 2030.

Global Secure Digital Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing shipments of high-resolution imaging devices | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Smartphone replacement cycles favour higher-capacity cards | +0.8% | Asia Pacific core, spill-over to global markets | Short term (≤ 2 years) |

| Automotive infotainment and ADAS data logging requirements | +0.9% | North America & EU leading, Asia Pacific following | Long term (≥ 4 years) |

| IoT / edge devices needing removable local storage | +0.7% | Global, with early adoption in industrial hubs | Medium term (2-4 years) |

| SD Express interface enabling NVMe-class speeds for AI workloads | +0.6% | North America and Asia Pacific technology centers | Short term (≤ 2 years) |

| Rising demand for radiation-hardened cards for small-sat constellations | +0.4% | North America, Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing High-Resolution Imaging Shipments

Professional mirrorless cameras and cinema-grade rigs are shipping with dual-slot designs that prioritize SD XC/UC compatibility. Each hour of 8K raw footage generated on such devices can exceed 7 TB, necessitating terabyte-class cards that blend high sequential write speeds with broad host compatibility. Western Digital’s 4 TB SDUC prototypes targeting V30 video speed classes underscore this storage multiplier, while major camera OEMs publicly affirm continued reliance on SD media for cost-effective redundancy. [1]Western Digital, “Driving AI Innovation: Western Digital Reveals New Solutions and Delivers Keynote at #FMS2024,” westerndigital.com Action-camera brands that position high-bit-rate 4K120 capture as a baseline also bundle UHS-I U3 cards as essential accessories, keeping the Secure Digital Card market tied to mainstream content-creation trends.

Smartphone Replacement Cycles Favor Higher-Capacity Cards

Global handset refresh intervals now average 3–4 years, a pattern that forces users of mid-range and entry-level Android devices to rely on expandable storage as system updates, 4K video libraries, and offline entertainment files accumulate. Samsung’s 1 TB UHS-I microSD launch meets this latent requirement by offering a cost-efficient capacity extension that preserves the handset’s residual life. On-device AI features, from photo enhancement to large-language-model inference, cache datasets locally, pushing storage utilization toward the upper limits of soldered NAND.

Automotive Infotainment and ADAS Data Logging

Pre-production autonomous vehicles log upward of 30 TB per test day, driving the adoption of AEC-Q100-qualified SD cards certified to operate from –40 °C to 85 °C. European regulation now stipulates in-vehicle data storage systems for automated-driving compliance, locking in removable media as a serviceable module within the software-defined car. [2]UNECE, “Data Storage System for Automated Driving,” unece.org Infotainment stacks offload high-resolution navigation tiles and personalized media libraries onto microSD to decouple content updates from head-unit firmware cycles. Tier-1 suppliers select SD form factors over soldered solutions to simplify over-the-air map upgrades and field servicing, creating a long-tail shipment horizon for automotive-grade cards. As Level 3 and Level 4 deployments scale after 2027, the Secure Digital Card market benefits from a durable, high-margin automotive demand layer.

IoT / Edge Devices Needing Removable Local Storage

Factory-floor controllers, smart meters, and industrial gateways generate cyclical workloads that require high-endurance media exceeding 30 k program/erase cycles. Vendors such as ATP specify 1920 TBW microSD ranges, illustrating the endurance tiers now sought by systems integrators. Edge inference units cache AI models locally to mitigate bandwidth costs, while surveillance cameras embrace edge storage to meet data-sovereignty statutes across the EU and parts of Asia. Rugged microSD offerings rated for –40 °C to 85 °C operation support these environments and fulfill hot-swap maintenance requirements. As industrial digitization advances, each new edge node effectively embeds a removable mini-datastore, keeping the Secure Digital Card market engaged with Industry 4.0 momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward cloud storage services | -0.9% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Proliferation of embedded UFS and soldered eMMC | -0.7% | Asia Pacific leading, global adoption following | Short term (≤ 2 years) |

| NAND supply–chain volatility amid geopolitical tensions | -0.6% | Global, with acute impact on Asia Pacific manufacturing | Short term (≤ 2 years) |

| E-waste regulations driving OEMs to non-removable storage | -0.5% | Europe leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Cloud Storage Services

Mainstream consumer workflows—from multimedia backup to collaborative editing—are tilting toward cloud-first models bundled with mobile operating systems. The decline of microSD slots in flagship handsets illustrates OEM preference for subscription-oriented revenue, diluting retail card demand. Content streaming platforms further reduce the incentive for local media hoarding, especially in 5G markets where downlink speeds exceed 200 Mbps. Nevertheless, upload-cost sensitivities, data-sovereignty policies, and patchy rural coverage limit cloud substitution in emerging markets and industrial scenarios.

Proliferation of Embedded UFS and Soldered eMMC

UFS 4.0 modules deliver sequential reads above 600 MB/s and markedly lower latency than even SD Express 7.1 cards. Smartphone and laptop makers, therefore, solder high-density NAND directly to logic boards to achieve slim designs and enhanced ingress-protection ratings. Royalty-free licensing plus controller integration reduces bill-of-materials costs, allowing OEMs to advertise headline bandwidth numbers that exceed current SD cards. Yet this substitution is less pronounced in cameras, vehicles, and industrial controllers, where hot-swap convenience and service life prioritization keep removable storage viable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Card Type and Capacity: SDUC Cards Redefine the Upper-Tier

SDHC maintained a 38.2% Secure Digital Card market share in 2024 by balancing 4 GB–32 GB capacities with mainstream device support. Professional-grade SDUC, while nascent, is pacing at a 5.3% CAGR to 2030 on the back of prototype 4 TB launches that cater to cinema crews and AI-edge recorders. The Secure Digital Card market size attached to SDHC is projected to plateau as smartphones stream 4K content natively and edge IIoT endpoints demand larger data buffers. In contrast, SDUC adoption benefits from the 128 TB ceiling that future-proofs workflows requiring granular sensor capture and prolonged field deployments. SDXC remains the transitional workhorse for 64 GB–2 TB workloads, but price erosion is expected to pivot professional buyers toward SDUC once host-controller firmware updates mature.

Second-order dynamics point to firmware lock-ins: host devices shipping after 2026 are likely to integrate SD Express controllers that negotiate PCIe Gen 4 links with SDUC media, thereby raising average selling prices across the Secure Digital Card market. Manufacturers able to synchronize NAND-layer scaling with controller readiness stand to capture the early-mover premium as the SDUC ecosystem widens.

By Form Factor: microSD Continues to Outperform

MicroSD accounted for 55.1% of the Secure Digital Card market share in 2024 and is forecast to expand at a 5.6% CAGR, cementing its position as the de facto removable storage for confined design envelopes. Automotive head units, surveillance domes, and handheld consoles all report thermal envelopes that microSD packages can accommodate through optimized PCB contacts and heat-spreader labeling. Full-size SD cards retain a foothold in broadcast cameras and ruggedized laptops where large connectors assure insertion durability and higher write-cycle ceilings. MiniSD shipments are fading into legacy status, contributing negligible revenue to the Secure Digital Card industry.

Capacity leadership within microSD is set to breach the 2 TB barrier by 2027 as vendors shift to 321-layer 3D NAND stacks, allowing mobile-gaming and drone-videography ecosystems to store volumetric datasets locally. With SD Express signalling delivering up to 985 MB/s on PCIe Gen 3 x1 lanes, forthcoming microSD Express cards narrow the performance gap to soldered NVMe drives, sustaining ASPs and deepening the Secure Digital Card market penetration into upper-performance niches.

By Application: Industrial & OT Devices Gain Momentum

Consumer electronics still underpin 48.5% of the Secure Digital Card market size, but growth moderates as flagship smartphones abandon card slots. Industrial & OT devices are tracking a 5.7% CAGR to 2030 by leveraging plug-and-play maintenance models across smart-factory installations. Automotive is a parallel lift factor, with ADAS event-data recorders specifying removable media for regulatory audit trails. Surveillance cameras in parking facilities and public-safety grids push continuous-write workloads that reward high-endurance industrial SKUs, in turn enlarging the Secure Digital Card market. Medical devices such as portable ultrasound scanners employ SD cards for patient-data segregation, highlighting the segment’s diverse compliance-driven demand clusters.

Looking forward, aerospace and small-sat constellations shift toward radiation-hardened SD stacks, offering incremental but high-margin volume. Vendors that certify products to both industrial temperature grades and ITAR-light export controls position themselves for disproportionate share capture as space-borne edge computing gains traction.

By Distribution Channel: Online Platforms Narrow the Gap

Offline retailers preserved a 62.3% Secure Digital Card market share in 2024, thanks to point-of-sale attach rates at camera and smartphone counters. Brick-and-mortar presence also reassures professional users who require immediate swaps during field shoots. Yet online channels, rising at a 5.4% CAGR, are siphoning professional and industrial procurement volume by aggregating SKUs that big-box stores rarely stock. E-commerce listings now feature endurance ratings, SMART-like health metrics, and detailed firmware revision notes, reducing information asymmetry and empowering technical buyers.

Subscription-based replenishment models for surveillance operators as well as auto-reorder dashboards for IIoT integrators underpin predictable revenue streams, enabling retailers to upsell specialized SKUs. Consequently, online sellers will tighten the volume gap with physical retail by the end of the decade, realigning distribution-margin structures across the Secure Digital Card market.

Geography Analysis

Asia Pacific’s 46.7% Secure Digital Card market share roots in vertically integrated memory supply chains across South Korea, Japan, and mainland China. Regional smartphone assembly clusters, coupled with robust automotive electronics build-outs, keep annual shipments on a solid 5.2% CAGR trajectory. Domestic memory firms intensify capacity scaling at 300 mm fabs, buffering against geopolitical trade measures and ensuring localized downstream card assembly. As Indian handset production incentives gain traction, microSD attachment rates in tier-2 and tier-3 cities continue to lift regional unit demand.

North America represents a margin-rich arena anchored by professional imaging, autonomous-vehicle test fleets, and high-reliability industrial control systems. Emphasis on ADAS data-legality drives notable uptake of automotive-grade SD media. Cloud datacenter operators also deploy SD cards as boot media in rack-scale servers for OPEX optimization, enhancing the breadth of use cases that sustain the Secure Digital Card market across the continent.

Europe registers steady unit demand on the back of Industry 4.0 retrofits and regulatory mandates favoring repairable electronics. Ecodesign directives that stipulate replaceable storage components indirectly safeguard SD expansion slots in smartphones and tablets sold after 2027. The region’s defense and aerospace sectors cultivate niche volume for radiation-tolerant Secure Digital Card variants, while smart-city traffic-monitoring deployments further broaden market exposure.

Competitive Landscape

Samsung, Western Digital, and Kingston collectively control a majority share of the Secure Digital Card market through tightly coupled NAND fabrication and card assembly operations. Vertical integration supports cost leadership and firmware agility, allowing rapid transitions to SD Express product lines that command premium ASPs. Western Digital’s stand-alone flash entity leverages proprietary controller IP to launch 8 TB SDUC prototypes, reinforcing thought leadership in capacity ceilings. Samsung crosses mobile and automotive portfolios by pairing 800 MB/s SD Express performance with rugged environmental specs, capturing cross-segment synergies. [3]Samsung Electronics, “UFS Card: State-of-the-Art Storage Card Delivering Superior Performance and Reliability,” ufsa.org

Second-tier players such as Team Group and Silicon Power differentiate through application-specific firmware tuned for gaming handhelds, while ATP and Kingston carve out industrial niches focusing on ultra-high endurance and extended temperature operability. Space-grade innovators—including 3D Plus—use stacked-die shielding and ECC hardening to target small-sat payloads, a segment unaffected by mainstream ASP erosion.

Strategically, leaders prioritize interface advancement over raw capacity gains. SD Express brings NVMe transport to removable media, neutralizing UFS speed superiority and allowing the Secure Digital Card industry to re-engage premium device segments. Concurrently, corporate sustainability commitments encourage circular-economy design, elevating the role of field-replaceable SD cards in reducing device-level e-waste. Competitive maneuvering therefore revolves around endurance, thermals, and specialized compliance certifications rather than commoditized gigabyte pricing alone.

Secure Digital Card Industry Leaders

Samsung Electronics Co., Ltd.

Western Digital (SanDisk)

Kingston Technology Corp.

Kioxia Holdings Corp.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Team Group released the APEX SD7.1 microSD Express card with 800 MB/s reads and 700 MB/s writes, tailored to Nintendo Switch 2 workflows.

- July 2025: Silicon Power introduced the Hypera microSDXC Express card, combining PCIe 3.0 signaling with UHS-I fallback to serve the handheld-gaming segment.

- July 2025: YMTC detailed plans to secure 15% global NAND share by late 2026 via domestic tooling and 321-layer production lines.

- June 2025: ADATA debuted Premier Extreme microSD Express 7.1 cards at 800 MB/s, focusing on next-gen gaming consoles.

Global Secure Digital Card Market Report Scope

| SD (≤2 GB) |

| SDHC (4 GB–32 GB) |

| SDXC (64 GB–2 TB) |

| SDUC (>2 TB) |

| Full-size SD |

| miniSD |

| microSD |

| Consumer Electronics |

| Automotive |

| Industrial and OT Devices |

| Security and Surveillance |

| Medical Devices |

| Others |

| Offline/Retail |

| Online/E-commerce |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Card Type and Capacity | SD (≤2 GB) | ||

| SDHC (4 GB–32 GB) | |||

| SDXC (64 GB–2 TB) | |||

| SDUC (>2 TB) | |||

| By Form Factor | Full-size SD | ||

| miniSD | |||

| microSD | |||

| By Application | Consumer Electronics | ||

| Automotive | |||

| Industrial and OT Devices | |||

| Security and Surveillance | |||

| Medical Devices | |||

| Others | |||

| By Distribution Channel | Offline/Retail | ||

| Online/E-commerce | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the Secure Digital Card market size in 2025 and how fast is it expected to grow?

The market stands at USD 11.01 billion in 2025 and is forecast to advance at a 4.98% CAGR to reach USD 14.05 billion by 2030.

Which application segment is projected to expand the quickest?

Industrial and operational-technology devices are set to post the fastest growth, registering a 5.7% CAGR through 2030.

Why do SD cards remain relevant when cloud storage is expanding rapidly?

Many industrial, automotive, and edge-AI deployments require field-replaceable, high-endurance local media to ensure data integrity during intermittent connectivity and to satisfy regulatory audit needs that the cloud alone cannot meet.

How will SD Express influence the market over the next five years?

By delivering NVMe-class speeds up to 1.6 GB/s, SD Express narrows the performance gap with embedded UFS, enabling on-device AI workloads and sustaining premium price tiers for removable storage.

Which form factor leads current shipments and why?

The microSD form factor commands 55.1% market share because its compact size suits smartphones, automotive infotainment systems, and industrial IoT devices that operate in space-constrained environments.

Who are the principal companies shaping competitive dynamics?

Samsung, Western Digital (SanDisk), and Kingston Technology dominate through vertically integrated NAND production, while specialist brands such as Team Group, Silicon Power, and ATP focus on gaming and industrial endurance niches.

Page last updated on: