Mobile Device Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

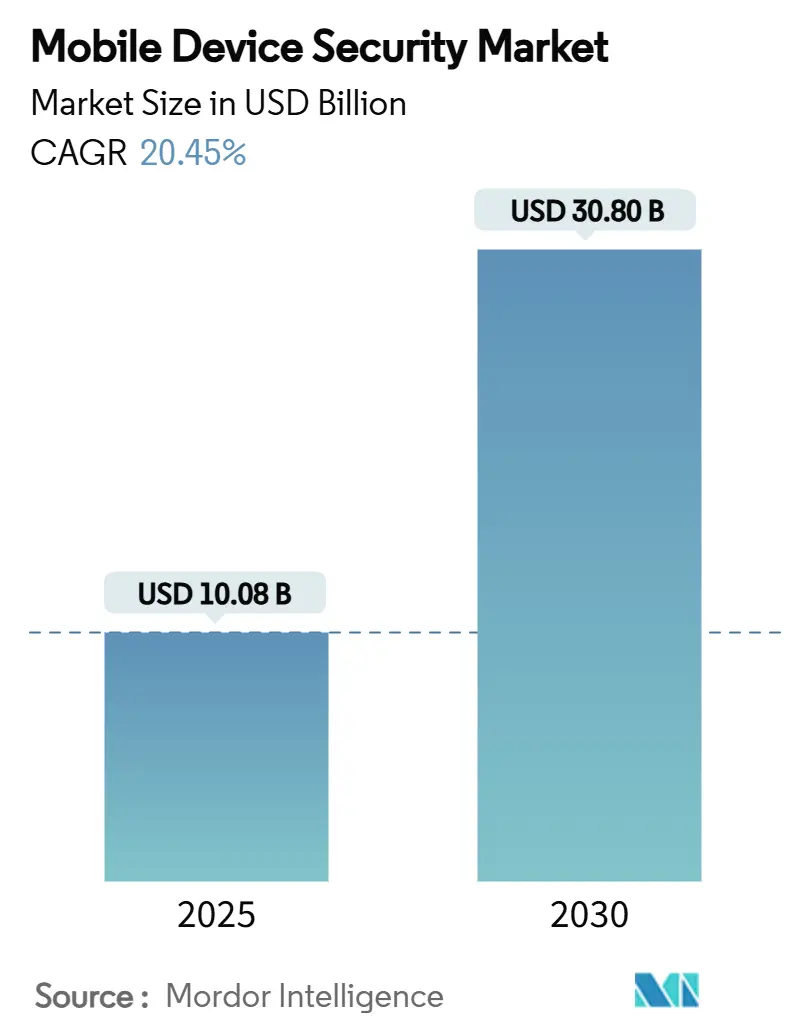

| Market Size (2025) | USD 10.08 Billion |

| Market Size (2030) | USD 30.80 Billion |

| Growth Rate (2025 - 2030) | 20.45% CAGR |

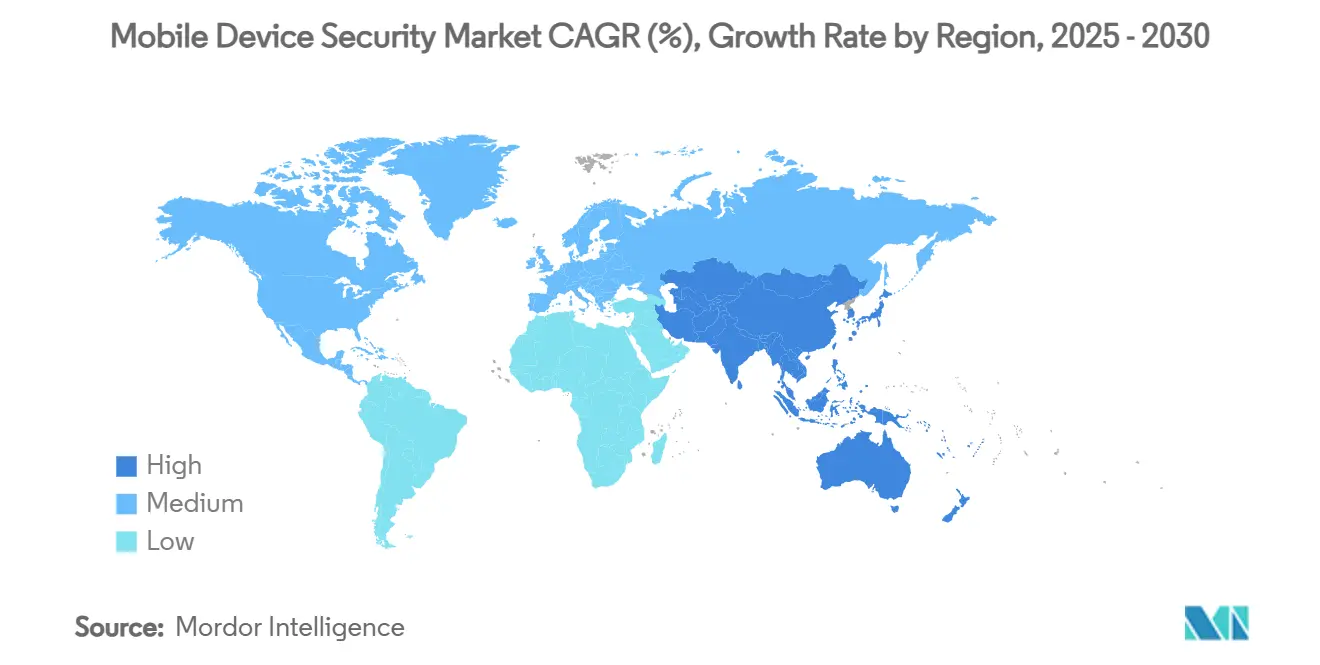

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

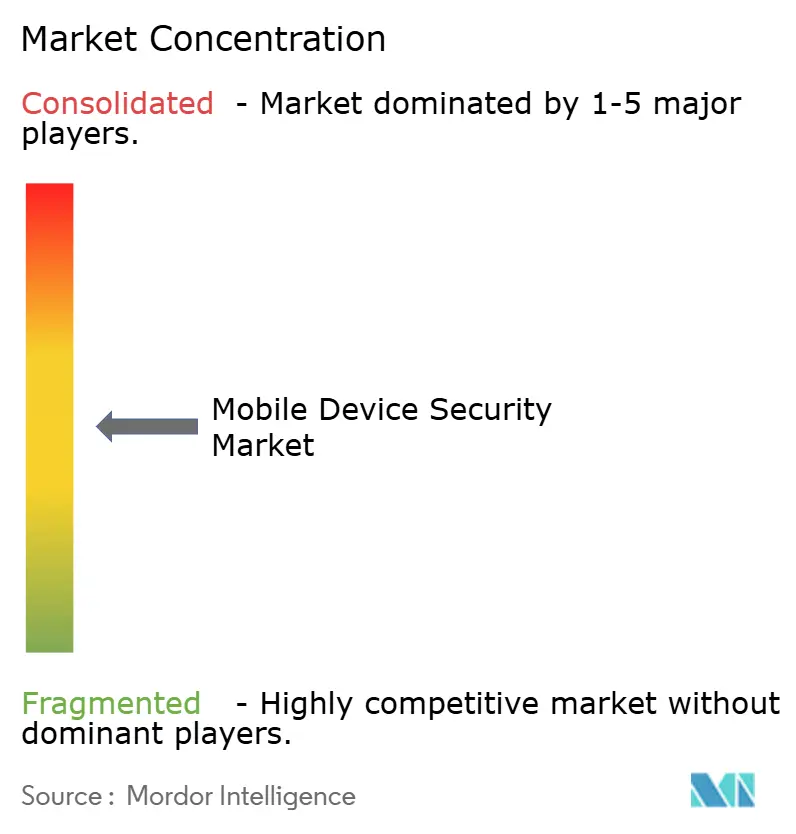

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Device Security Market Analysis by Mordor Intelligence

The mobile device security market size reached USD 10.08 billion in 2025 and is forecast to reach USD 30.80 billion by 2030, registering a 20.45% CAGR. Heightened malware sophistication, wider zero-trust adoption, and tougher privacy mandates encourage organizations to treat mobility protection as a board-level priority. Cloud-delivered defenses scale rapidly as mobile fleets grow, while AI-enabled analytics shorten threat-to-response times. Vendors differentiate through integrated orchestration that blends device, application, and identity controls, creating clear upgrade paths for buyers seeking unified platforms. Competitive momentum also stems from managed detection and response services that remove operational burdens for stretched IT teams.

Key Report Takeaways

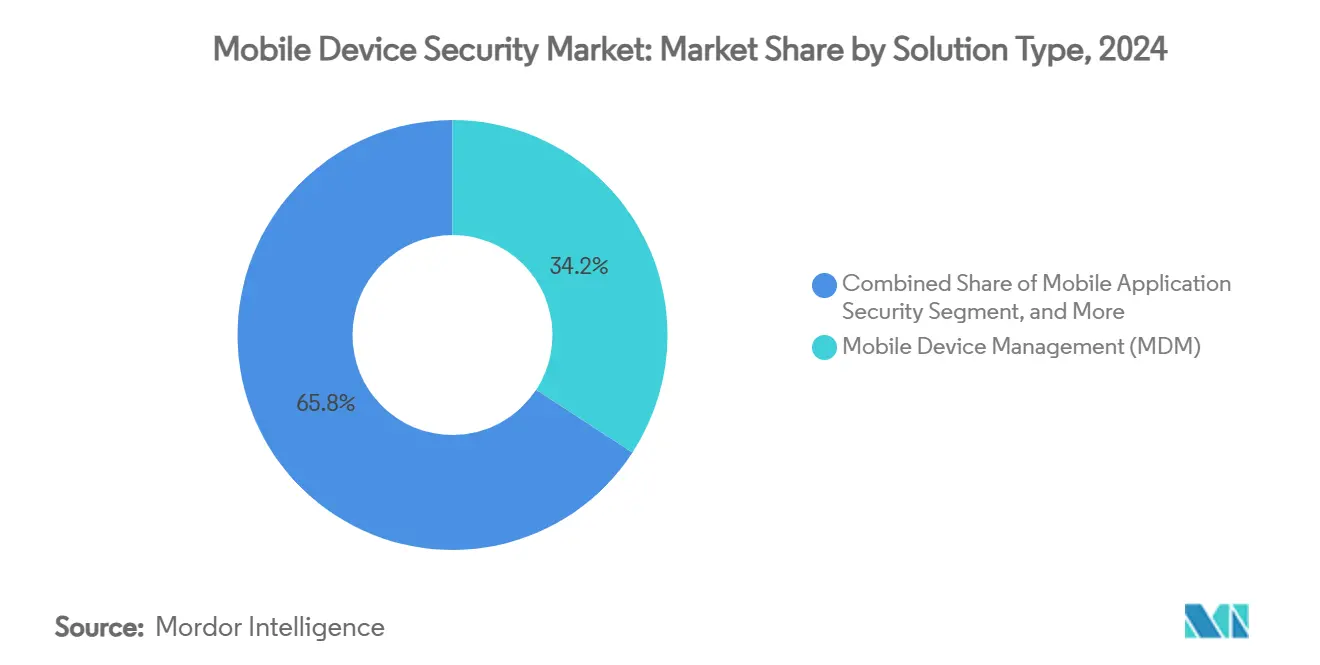

- By solution type, Mobile Device Management led with 34.2% revenue share in 2024; Mobile Threat Defense is advancing at a 26.2% CAGR through 2030.

- By deployment mode, cloud platforms accounted for 67.3% of the mobile device security market size in 2024 and are expanding at a 24.5% CAGR.

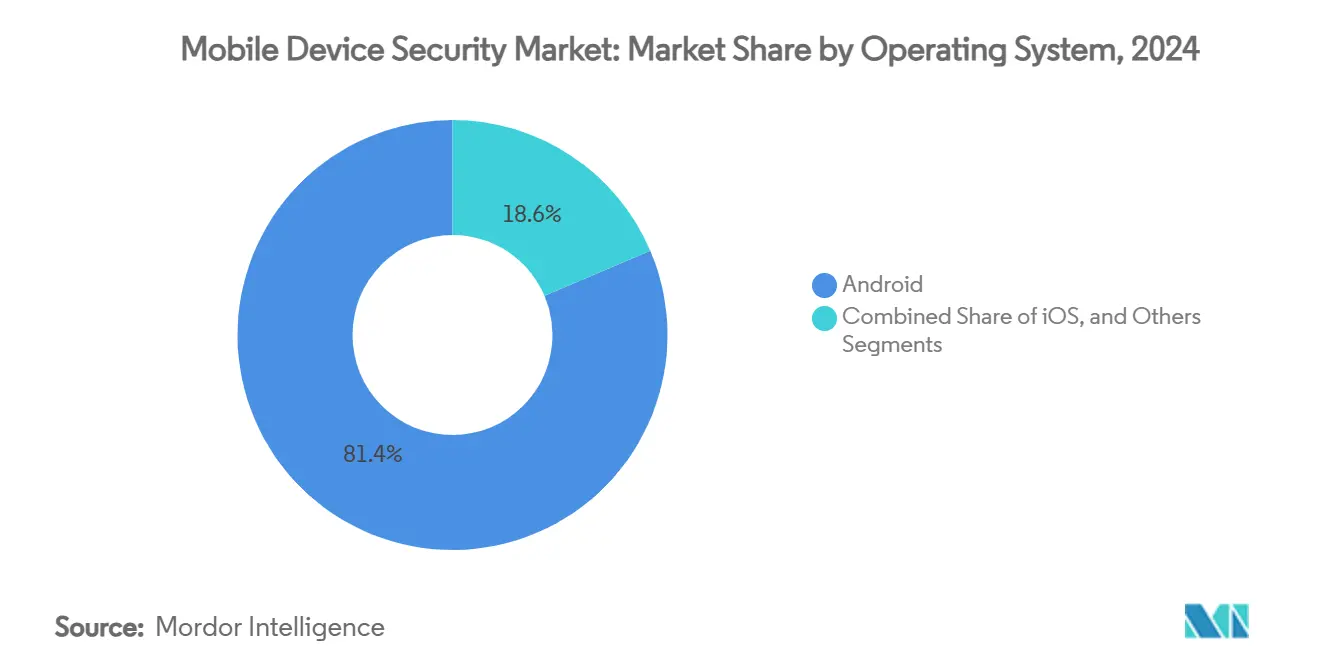

- By operating system, Android captured 81.4 of % mobile device security market share in 2024, while iOS-focused spending is rising at a 19.3% CAGR.

- By end-user industry, BFSI held 24.1% share of the mobile device security market size in 2024; healthcare is growing fastest at 25.6% CAGR.

- By geography, North America commanded 38.2% revenue in 2024, yet Asia-Pacific is set to post a 27.3% CAGR to 2030.

Global Mobile Device Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of BYOD policies | +4.2% | Global, with higher adoption in North America and the EU | Medium term (2-4 years) |

| Rising mobile payment and m-commerce transactions | +3.8% | Asia-Pacific core, spill-over to Latin America | Short term (≤ 2 years) |

| Increasing sophistication of mobile malware and phishing attacks | +5.1% | Global | Short term (≤ 2 years) |

| Regulatory pressure for data-protection compliance | +3.5% | North America and the EU, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Adoption of zero-trust frameworks in mobile security stacks | +2.9% | North America and the EU, early adoption in the Asia-Pacific | Medium term (2-4 years) |

| SME demand for MDR services focused on mobile endpoints | +1.8% | Global, with a concentration in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of BYOD Policies

Bring-your-own-device programs widened after the pandemic because workers expect seamless access from personal phones. The U.S. Department of Defense’s zero-trust mandate for 2027 accelerates data-centric models that decouple protection from hardware ownership. Contractors across the supply chain must now prove secure mobile workflows to retain federal projects. Weak consumer antivirus choices complicate matters—47% of free Android tools miss known malware, widening enterprise risk surfaces. Companies, therefore, couple Mobile Application Management with real-time telemetry to spot anomalous behavior on unmanaged devices and quarantine threats instantly. Policy coverage is expanding from device posture to application sandboxing and content containerization, ensuring sensitive data never leaves encrypted zones.

Rising Mobile Payment and M-Commerce Transactions

Transaction volumes on phones surged as emerging economies pivoted straight to mobile wallets. Central-bank research flags point-of-sale endpoints as prime targets, shifting attacker interest from handsets to payment back-ends.[1]Boston Fed, “The Future of Mobile Security: Understanding the Risk Environment for Mobile Payments,” bostonfed.org Financial institutions embed SDK-level shields that encrypt sessions and block code injection, thereby hardening checkout flows. Hardware-rooted attestation—illustrated by Samsung Knox—validates device integrity before approving a payment, a feature spreading quickly in Latin America, where 65% of residents used mobile pay apps in 2024. Retailers in turn integrate threat telemetry into fraud engines, blending cybersecurity and anti-money-laundering workflows for unified risk scoring.

Increasing Sophistication of Mobile Malware and Phishing Attacks

Attackers now automate social-engineering lures with generative AI, matching human success rates while slashing campaign costs. A 2024 breach at a major Indian bank used natural language chatbots to mimic executives and harvest credentials. Chipset-level flaws amplify danger; Google disclosed Qualcomm GPU bugs that expose billions of Android phones to remote code execution. Supply-chain infections such as BadBox 2.0 preinstall malware on low-cost devices, creating botnets exceeding 10 million endpoints. Healthcare staff are prime targets, with 39% of mobile attacks aiming at clinical users to seize patient records. Enterprises, therefore, elevate runtime kernel monitoring and anomaly-based phishing defenses to block multi-stage exploits.

Regulatory Pressure for Data-Protection Compliance

Governments refine rules that explicitly cover mobility. NIST’s iOS/iPadOS 18 guidance and Cybersecurity Framework 2.0 set technical baselines for federal deployments. Financial regulators note that 84% of banks boosted mobile security budgets after audit findings highlighted breach frequency. Defense Information Systems Agency STIGs for Samsung Android 15 prescribe granular Knox policies, influencing commercial best practice. The EU’s GDPR enforcement extends privacy-by-design to app coding, forcing developers to encrypt data at rest and in motion. Fines for non-compliance steer boardroom funding toward continuous compliance dashboards that plug directly into MDM event streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership for advanced security suites | -2.8% | Global, with a higher impact in emerging markets | Medium term (2-4 years) |

| Widespread availability of free / pirated security apps | -1.9% | Global, with a concentration in price-sensitive markets | Short term (≤ 2 years) |

| Battery-drain and UX impacts from always-on defense agents | -1.5% | Global | Short term (≤ 2 years) |

| Firmware fragmentation in the low-cost Android ecosystem | -2.1% | Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Advanced Security Suites

Vendor consolidation promises unified dashboards yet often lifts subscription spending. IBM’s USD 6.4 billion HashiCorp takeover and Palo Alto Networks’ QRadar purchase raise suite list prices as vendors chase margin through breadth. Smaller firms struggle with per-device fees and integration labor, leading them to settle for baseline MDM without full threat defense. Budget planners also face variable device counts as seasonal staff join and leave, complicating multi-year contract negotiations. Managed services partly resolve the cost hurdle but introduce vendor-lock concerns when switching providers. The tension slows adoption among price-sensitive buyers despite clear risk exposure.

Battery-Drain and UX Impacts from Always-On Defense Agents

Continuous scanning agents consume energy and data, triggering user pushback. Studies show antivirus apps can drive 28.9% of a phone’s daily battery burn while the screen is off. Background activity drains also correlate with device aging, nudging staff to turn off protections to extend runtime. Enterprises therefore adopt risk-adaptive policies that dial monitoring intensity based on context, striking a balance between safety and usability. Platform providers likewise lean on chipset telemetry to detect anomalies without running heavy user-space code, improving battery performance and user acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Threat-Centric Tools Narrow the Gap

Mobile Device Management kept 34.2% revenue leadership in 2024, proving the foundational need for policy enforcement. Yet the mobile device security market is tilting toward intelligence-led defense as Mobile Threat Defense accelerates at a 26.2% CAGR. Financial institutions deploy MTD to satisfy 23 NYCRR 500 detection clauses, moving beyond checklist compliance to behavior analytics.[2]Lookout, “MDM-MAM-MTD Financial Services Infographic,” lookout.com The mobile device security market size for MTD is set to overtake half of MDM outlays within four years, signaling a lasting pivot to threat visibility. Application security and identity modules ride zero-trust rollouts, embedding least-privilege logic directly into workflow apps. Data-centric encryption tools remain niche yet attract regulated sectors seeking file-level governance, positioning them for compound growth once privacy fines escalate.

The mobile device security market continues its transition from perimeter lockdown to risk-based orchestration. Buyers want event correlation across EMM, SIEM, and XDR channels to surface cross-device patterns. Vendors respond with open APIs and cloud-native data lakes that crunch billions of signals daily. Success will depend on automating response playbooks that shrink dwell time without flooding analysts with alerts, a capability where AI start-ups are challenging incumbents.

By Deployment Mode: Cloud First, Hybrid Rising

Cloud setups held a 67.3% share of the mobile device security market size in 2024 as firms sought elastic compute for machine-learning detection. Intune’s same-day support for Vision Pro illustrates how SaaS models accommodate new hardware faster than on-premises stacks. Always-updated analytics engines boost hit rates against zero-day exploits, validating the cloud’s 24.5% CAGR outlook. The mobile device security market nevertheless supports hybrid models for data-sovereign workloads, blending edge gateways with SaaS consoles.

Growing 5G adoption magnifies cloud pull because traffic paths already traverse operator cores. Operators now bundle connectivity with mobile security, as T-Mobile and Palo Alto Networks did in May 2025, tightening service integration. Government agencies still prefer on-prem processors for classified logs, sustaining single-tenant deployments. Over time, containerized micro-services will let agencies shift analytic workloads fluidly between locations, smoothing the cloud-hybrid divide.

By Operating System: Scale versus Uniformity

Android accounted for 81.4 of % mobile device security market share during 2024, powered by low-cost devices in Asia-Pacific. Yet that scale complicates patch discipline when chipset vulnerabilities such as Samsung’s GPU flaw appear. Enterprises, therefore, favor Samsung Knox or hardened OEM images to impose baseline controls. Apple’s homogeneous ecosystem attracts executives needing certifiable security, driving iOS spending even though unit share lags. The mobile device security market size opportunity on iOS grows as Apple expands into spatial computing, broadening the protected surface.

Alternative platforms remain under 5% combined but add complexity to policy engines that must recognize HarmonyOS and rugged Windows handhelds. To cope, security dashboards employ hardware-attestation standards such as FIDO, abstracting away OS idiosyncrasies. Vendors specializing in Android threat telemetry, like Zimperium, deepen ML models to spot exploit chains unique to open kernels, further segmenting the competitive field.

By End-User Industry: Healthcare Momentum Builds

BFSI’s 24.1% stake in 2024 underscores its regulatory head start, yet healthcare now tops growth at 25.6% CAGR thanks to telehealth ubiquity. The mobile device security market size tied to clinics will climb rapidly as remote diagnostics and bedside tablets multiply endpoints. Regulations such as HIPAA’s mobile addendum push hospitals to encrypt data in transit and at rest, spurring investment in data-centric controls. Retail and e-commerce entities also elevate budgets to reduce checkout fraud on apps, merging mobile security logs with fraud-scoring AI.

Government agencies allocate funds to meet zero-trust deadlines, securing field devices for defense and first-responder missions. Manufacturing, still nascent, integrates mobile dashboards with OT networks, demanding segmentation gateways that block lateral movement from phones into PLCs. These vertical patterns prove that the mobile device security market must flex to industry nuances while preserving platform commonality.

Geography Analysis

North America held 38.2% of 2024 spending as organizations upgraded mature BYOD fleets under strict compliance rules. Early adoption of zero-trust and large budgets ensure steady—though single-digit—growth. Canada’s public-sector cloud directive extends U.S. best practice northward, raising regional demand for FedRAMP-aligned SaaS consoles.

Asia-Pacific is the growth engine, projected at a 27.3% CAGR through 2030. Digitalization programs in India, Indonesia, and Vietnam onboard millions of first-time mobile workers, and the GSMA pegs 2023 regional mobile GDP contribution at USD 880 billion.[3]GSMA, “Mobile Economy Asia Pacific 2024,” gsma.com This economic weight incentivizes governments to draft security baselines akin to NIST, pushing enterprises to invest early. Domestic vendors compete on affordability, while multinationals supply high-assurance tools to multinationals and large banks.

Europe balances steady 15% growth with an emphasis on data-sovereignty controls. GDPR fines encourage encryption and pseudonymization at the application level, shaping demand for granular data-protection modules. Latin America’s 65% population adoption of mobile payments fuels BFSI and retail projects, although budget sensitivity tempers premium suite uptake. Africa and the Middle East witness rapid 5G rollouts that skip legacy infrastructure; governments bundle spectrum licenses with cybersecurity compliance codes, opening fresh avenues for providers offering turnkey managed security. Across these regions, the mobile device security market mirrors differing regulatory maturity yet converges on the same zero-trust goal.

Competitive Landscape

The mobile device security market hosts a mix of broad enterprise mobility suites and niche AI specialists. Microsoft, IBM, and VMware exploit existing endpoint footprints to cross-sell mobile add-ons, leveraging deep integration with productivity suites. Jamf’s USD 215 million Identity Automation deal extends Apple-centric identity governance paths, appealing to education and healthcare buyers.[4]Nasdaq, “Jamf Announces Definitive Agreement to Acquire Identity Automation for $215 Million,” nasdaq.com Lookout and Zimperium maintain an edge by feeding vast mobile telemetry into cloud AI to flag polymorphic malware within seconds. CrowdStrike brings XDR correlation, connecting mobile alerts with workstation and server logs for holistic incident response.

Carrier-security alliances intensify, exemplified by T-Mobile and Palo Alto Networks folding SASE into 5G plans, which blur lines between telco and security supplier. Managed service providers latch onto SME appetite for turnkey protection, packaging MDM, threat defense, and help-desk services under per-user pricing. Consolidation will likely continue as platform vendors acquire specialized analytics to widen capability maps, echoing Palo Alto’s 2024 QRadar asset purchase. Future differentiation will hinge on open APIs, policy automation, and transparent ML explainability rather than checklist feature counts.

Mobile Device Security Industry Leaders

Microsoft Corporation

IBM Corporation

VMware Inc. (AirWatch)

Broadcom Inc. (Symantec)

BlackBerry Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft Intune expanded support to Apple Vision Pro, reinforcing rapid SaaS adaptation to novel form factors.

- May 2025: T-Mobile and Palo Alto Networks unveiled a managed SASE bundle for wireless devices, integrating 5G Advanced connectivity with Prisma SASE 5G security.

- March 2025: Jamf agreed to acquire Identity Automation for USD 215 million, adding advanced identity lifecycle controls to its mobility suite.

- March 2024: F-Secure partnered with a tier-1 carrier to embed mobile security in customer packages, leveraging its Lookout Life acquisition for threat analytics.

Global Mobile Device Security Market Report Scope

| Cloud |

| On-Premises |

| Mobile Device Management (MDM) |

| Mobile Application Security |

| Mobile Threat Defense |

| Mobile Identity and Authentication |

| Mobile Data Protection |

| Android |

| iOS |

| Others (HarmonyOS, KaiOS, Windows) |

| BFSI |

| Healthcare |

| Retail and E-commerce |

| Government and Defense |

| IT and Telecom |

| Manufacturing |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| By Solution Type | Mobile Device Management (MDM) | ||

| Mobile Application Security | |||

| Mobile Threat Defense | |||

| Mobile Identity and Authentication | |||

| Mobile Data Protection | |||

| By Operating System | Android | ||

| iOS | |||

| Others (HarmonyOS, KaiOS, Windows) | |||

| By End-User Industry | BFSI | ||

| Healthcare | |||

| Retail and E-commerce | |||

| Government and Defense | |||

| IT and Telecom | |||

| Manufacturing | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the mobile device security market in 2025?

The mobile device security market size stands at USD 10.08 billion.

What CAGR is projected through 2030?

The market is forecast to expand at a 20.45% CAGR to reach USD 30.80 billion by 2030.

Which region is growing fastest in spending?

Asia-Pacific leads with a projected 27.3% CAGR, fueled by mobile-first strategies across emerging economies.

Which solution segment is outpacing others?

Mobile Threat Defense is the fastest-growing segment, projected at 26.2% CAGR as enterprises seek threat-centric visibility.

Why is healthcare accelerating investment?

Telehealth normalization and stringent patient-data regulations push healthcare spending to a 25.6% CAGR through 2030.

What deployment model dominates?

Cloud-delivered services hold a 67.3% share and continue to expand thanks to elastic compute and rapid feature rollouts.

Page last updated on: