Mobile Device Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

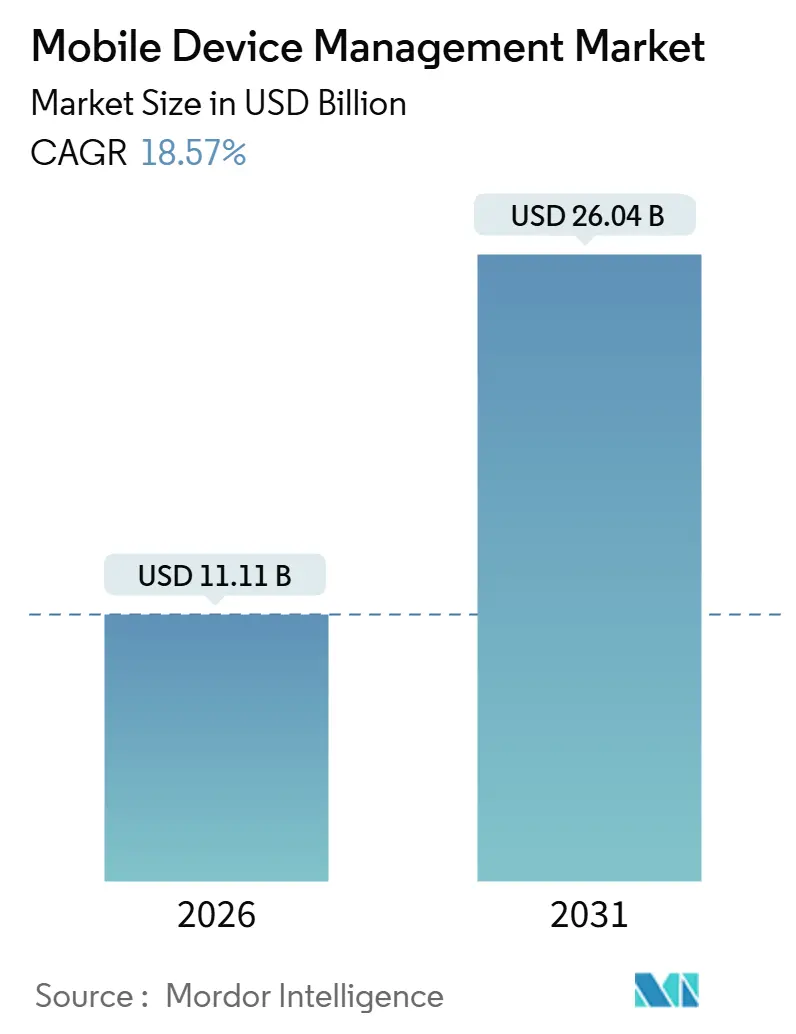

| Market Size (2026) | USD 11.11 Billion |

| Market Size (2031) | USD 26.04 Billion |

| Growth Rate (2026 - 2031) | 18.57% CAGR |

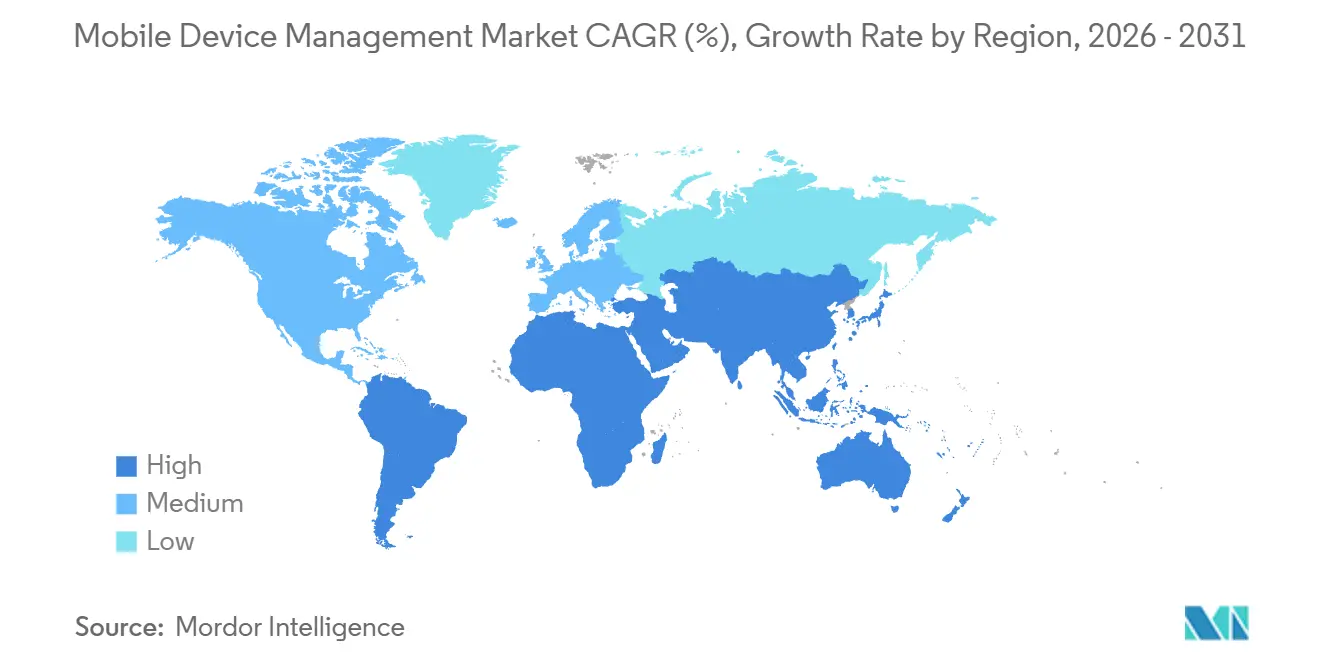

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Device Management Market Analysis by Mordor Intelligence

The Mobile Device Management market size stands at USD 11.11 billion in 2026 and is projected to reach USD 26.04 billion by 2031, reflecting an 18.57% CAGR over the period. This trajectory reflects a decisive shift toward zero-trust security, enhanced cyber-insurance standards, and 5G-enabled workforce models that subject every endpoint to continuous scrutiny. Cloud-native unified endpoint management, stringent insurer mandates, and the accelerating adoption of BYOD now position the Mobile Device Management market as a critical layer in enterprise risk reduction, rather than a back-office IT task. The rapid proliferation of industrial IoT sensors, post-quantum cryptography upgrades, and ESG-linked procurement rules further expands the addressable opportunity. Competitive differentiation is shifting from feature checklists to demonstrable cryptographic agility, lifecycle transparency, and seamless identity federation, while integration cost, privacy regulations, and battery constraints on rugged devices temper near-term adoption momentum.

Key Report Takeaways

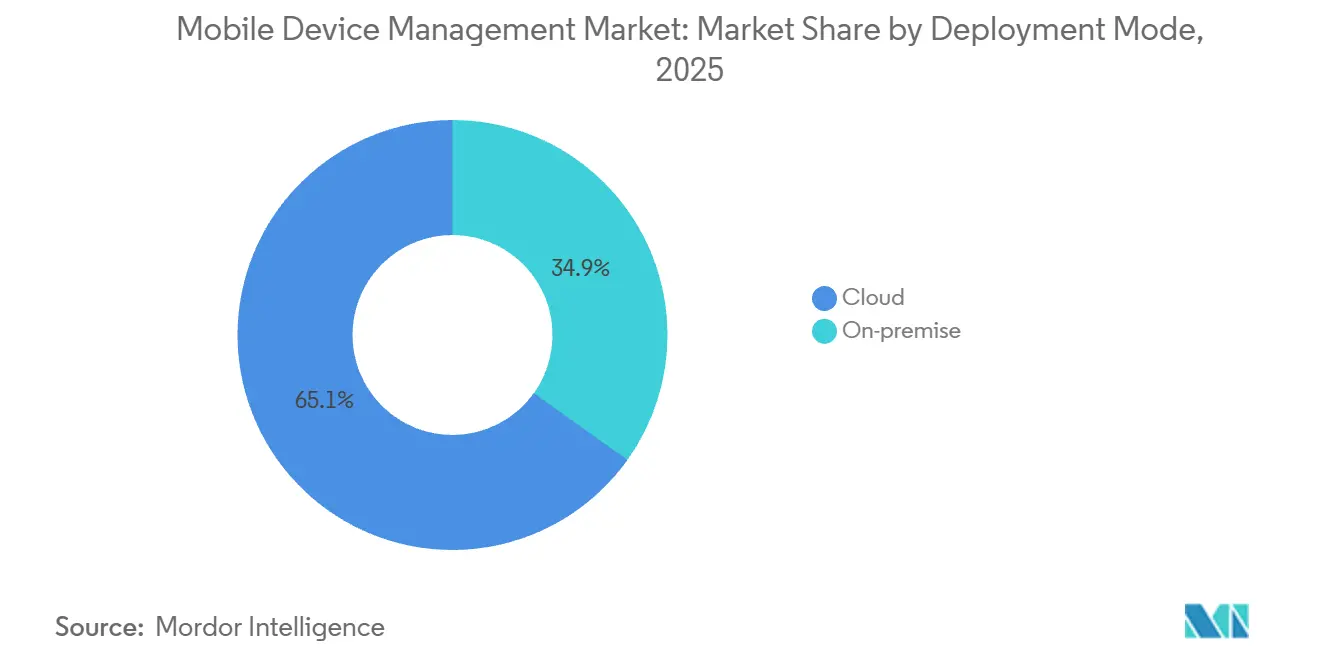

- By deployment mode, cloud deployment captured 65.13% revenue share in 2025 and is forecast to expand at a 19.12% CAGR through 2031.

- By device type, smartphones and tablets led with 48.28% share in 2025, while IoT and industrial IoT endpoints are poised to advance at a 20.34% CAGR through 2031.

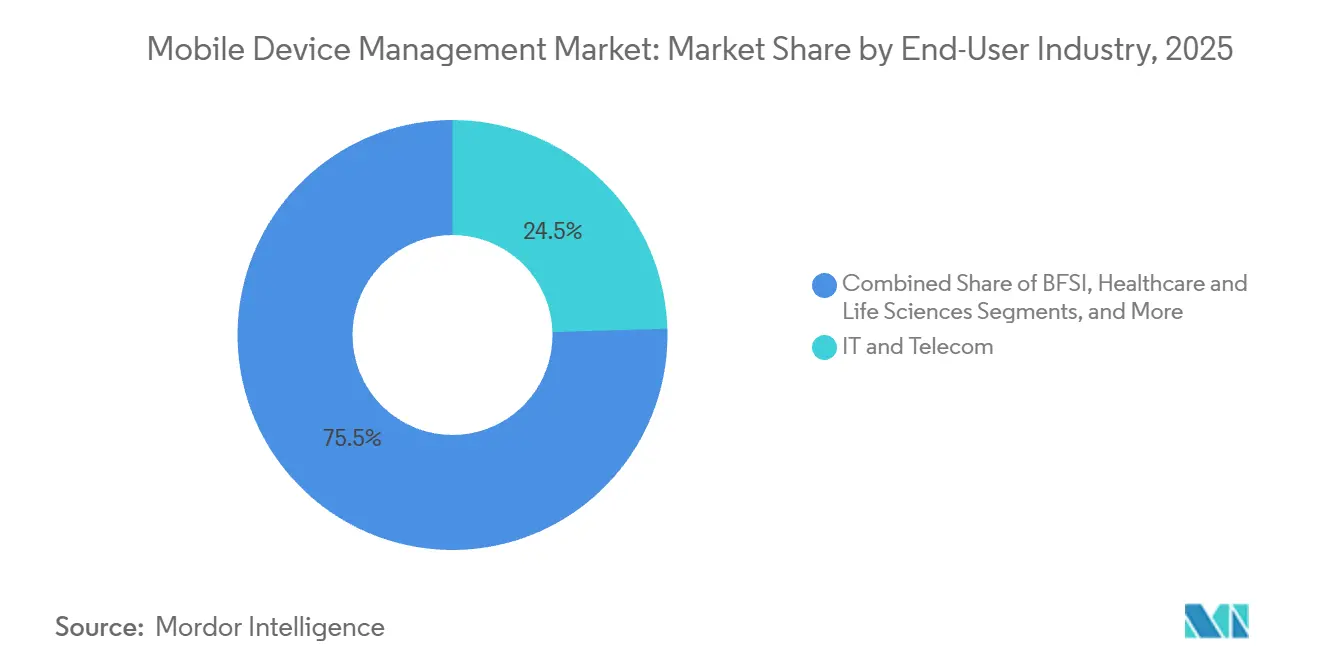

- By end-user industry, IT and telecom held a 24.53% spending share in 2025, but healthcare and life sciences are projected to grow at a 21.32% CAGR through 2031.

- By ownership model, corporate-owned devices retained a 56.91% share in 2025, while BYOD programs are anticipated to grow at a 21.32% CAGR through 2031.

- By geography, North America accounted for 38.71% market share in 2025, whereas Asia Pacific is expected to record the highest regional CAGR at 10.23% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Device Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of Enterprise BYOD Policies | +3.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Accelerating Shift to Cloud-Native UEM Suites | +4.2% | Global, led by North America and Asia Pacific | Medium term (2-4 years) |

| Surge in Cyber-Insurance Mandates for Endpoint Control | +3.1% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| 5G-Enabled Field-Service Workforce Expansion | +2.9% | Global, with early traction in Asia Pacific and Middle East | Long term (≥ 4 years) |

| Post-Quantum Security Preparations Elevating Device Trust Stacks | +2.4% | North America and Europe, with spillover to Asia Pacific | Long term (≥ 4 years) |

| ESG-Linked Procurement Favouring Secure-Device Vendors | +1.8% | Europe, expanding to North America and Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of Enterprise BYOD Policies

Hybrid work has pushed 82% of organizations to allow employee-owned phones and tablets on corporate networks in 2025, up from 67% in 2023. This expanded fleet multiplies operating-system permutations, personal cloud apps, and unmanaged data paths, demanding containerization and remote-wipe controls. Insurers are increasingly denying or surcharging coverage when unmanaged endpoints exist, making MDM adoption a prerequisite for risk transfer. Cost savings from eliminating corporate device stipends can entice finance teams; however, breach-related penalties under the GDPR or the California Consumer Privacy Rights Act may offset those savings. As a result, executives view the Mobile Device Management market as a direct hedge against regulatory fines and premium hikes rather than an optional efficiency tool.

Accelerating Shift to Cloud-Native UEM Suites

Organizations are abandoning on-premise consoles for cloud platforms that consolidate phones, laptops, wearables, and IoT devices behind a single policy fabric. Microsoft Intune, integrated with Azure Active Directory, exemplifies how conditional access decisions now assess real-time device health, user identity, and app context.[1]Microsoft Corporation, “Microsoft Intune,” microsoft.com Elastic capacity removes server procurement cycles, while automatic updates ensure continuous compliance with emerging zero-trust guidelines. Medium-term gains include machine-learning remediation of configuration drift and predictive hardware failure alerts, cutting endpoint management labor by as much as 40%. Delayed migrations risk technical debt as emerging standards such as FIDO2 and post-quantum algorithms outpace on-premise software release cycles.

Surge in Cyber-Insurance Mandates for Endpoint Control

After ransomware claims topped USD 20 billion in 2024, carriers such as Lloyd’s of London began requiring attested device encryption, patch management, and remote-wipe capabilities before issuing or renewing policies. The New York State Department of Financial Services echoed this stance by mandating annual endpoint control certification for regulated entities. Enterprises that fall short face premium increases of 50% or outright coverage exclusions, resulting in the shifting of MDM procurement authority from CIOs to CFOs. Financial reporting risk, therefore, fuels Mobile Device Management market purchases, especially in healthcare, where a single breach can unleash HIPAA fines and class-action litigation.

5G-Enabled Field-Service Workforce Expansion

Standalone 5G networks allow rugged tablets, smart helmets, and wearables to stream video diagnostics and AR instructions with millisecond latency. Ericsson forecasts 6.4 billion 5G subscriptions by 2031, with industrial segments expected to capture an outsized share. Utilities, construction firms, and logistics operators now bundle eSIM credentials with MDM policies to enforce geofencing and quality-of-service tiers. Carriers that leverage network slicing allocate dedicated bandwidth to enterprise devices, ensuring that mission-critical traffic outranks consumer data. The Mobile Device Management market, therefore, expands alongside 5G adoption, as every new sensor or handheld requires secure bootstrapping, firmware updates, and posture verification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-Front Integration Cost with Legacy IAM/ITSM Stacks | -2.1% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Fragmented Regulatory Data-Sovereignty Rules | -1.7% | Global, with concentration in Europe, Asia Pacific, and Middle East | Medium term (2-4 years) |

| Growing Employee Privacy Pushback on Device Tracking | -1.3% | Europe and North America, emerging in Asia Pacific | Medium term (2-4 years) |

| Limited Battery/CPU Headroom on Rugged IoT Endpoints | -0.9% | Global, with focus on manufacturing and logistics sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Up-Front Integration Cost with Legacy IAM/ITSM Stacks

Enterprises relying on outdated identity managers and help-desk tools must fund custom APIs, directory sync, and workflow orchestration when deploying modern MDM. Consulting fees often exceed USD 500,000, and projects can last a year, straining budgets for mid-sized firms.[2]IBM Corporation, “MaaS360 with Watson,” ibm.com Mixed authentication protocols create single points of failure and incident-response delays, while strict change-control boards in finance and healthcare prolong testing cycles. This cost friction temporarily slows the uptake of Mobile Device Management among heavily regulated incumbents.

Fragmented Regulatory Data-Sovereignty Rules

GDPR limits cross-border transfers without adequacy rulings, China’s Personal Information Protection Law mandates domestic data storage, and India’s Digital Personal Data Protection Act empowers the government to designate critical data categories. Multi-tenant cloud vendors must build regional data centers or hybrid options, eroding economies of scale. On-the-fly policy shifts as employees travel between jurisdictions remain rare features, forcing many organizations to maintain parallel MDM instances. Compliance overhead, therefore, subdues Mobile Device Management market growth, especially for globally distributed enterprises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Suites Capture Two-Thirds Share

Cloud-hosted platforms controlled 65.13% of 2025 revenue, confirming their dominance in the Mobile Device Management market. The model’s 19.12% CAGR to 2031 reflects elastic scaling, automatic feature updates, and pay-as-you-go pricing that converts capital outlays into operating expenses. Vendors such as Microsoft and VMware expose REST APIs that integrate with SIEM, IAM, and EDR tools, trimming integration timelines. Even defense and financial institutions that once rejected public cloud now adopt hybrid blueprints that mirror policies across sovereign data centers for disaster recovery, further enlarging the cloud’s footprint.

Autonomous endpoint management accelerates the shift, as machine-learning engines analyze telemetry, predict component failures, and self-correct drift. Gartner estimates a 40% cut in labor costs by 2029 when autonomous capabilities mature, underscoring why the Mobile Device Management market favors cloud delivery. Zero-touch provisioning enables devices to ship directly to end users and self-enroll through QR codes, a practice that was cemented during pandemic lockdowns. The value proposition, however, hinges on hardware attestation and a secure supply chain, because compromised firmware can defeat remote-management safeguards before devices even connect.

By Device Type: IoT Endpoints Outpace Smartphones

Smartphones and tablets owned 48.28% of 2025 revenue, but industrial IoT endpoints will grow at 20.34% CAGR as factories embed cellular modules in robots, fleets deploy rugged handhelds, and utilities install smart meters.[3]Ericsson, “Ericsson Mobility Report,” ericsson.com Cellular IoT connections are projected to reach 5.6 billion by 2030, each requiring certificate rotation, patching, and network-access controls. Laptops remain vital for code development and financial modeling, yet browser-based apps flatten their growth curve.

Rugged and wearable devices thrive in construction, mining, and clinical settings where harsh environments or infection-control rules preclude consumer hardware. Lightweight protocols such as OMA-DM and LwM2M shrink agent footprints, conserving battery and CPU. 5G network slicing offers dedicated bandwidth for telemetry, ensuring reliable throughput for autonomous vehicles or remote surgery. These dynamics channel investment toward IoT-oriented functionality within the Mobile Device Management market, including power-aware policy polling and edge-cached updates.

By End-User Industry: Healthcare Becomes the Growth Engine

IT and telecom captured 24.53% of 2025 spending thanks to early BYOD acceptance and developer workstation security. Yet, healthcare and life sciences will be the Mobile Device Management market’s fastest-growing segment at a 21.32% CAGR through 2031, driven by telehealth, remote patient monitoring, and decentralized clinical trials. HIPAA demands encryption, role-based permissions, and audit logging on every mobile device accessing electronic health records, propelling hospital procurement cycles.

Financial services continue to invest, maintaining endpoint controls to meet Gramm-Leach-Bliley and PCI DSS requirements, although branch consolidation moderates growth. Retailers deploy mobile point-of-sale terminals and inventory scanners that integrate with ERP platforms, while manufacturers embed tablets on production lines to display quality checklists and predictive maintenance alerts. Education purchasing plateaus as post-pandemic device fleets age without replacement budgets, and privacy concerns restrict student tracking. Logistics operators enforce geofence rules on handheld devices to deter route deviations, reflecting the use-case specificity that broadens but fragments the Mobile Device Management market demand.

By Ownership Model: BYOD Accelerates under Hybrid Work

Corporate-owned hardware retained a 56.91% share in 2025; however, BYOD programs are expanding at a 21.32% CAGR, as employees resist carrying dual devices. Containerization separates corporate data within encrypted partitions; however, privacy statutes such as GDPR Article 88 or the California Consumer Privacy Rights Act require employers to disable intrusive monitoring. Choose-your-own-device schemes reduce support complexity but limit the availability of volume discounts.

Generational expectations are shifting toward personal hardware flexibility, and cyber-insurance underwriters now require mobile application management on any device that touches corporate data. Consequently, the Mobile Device Management market must strike a balance between user autonomy and compliant oversight. Regions with lighter privacy regimes will adopt BYOD more quickly, while European works councils and North American unions may prompt enterprises to revert to corporate-owned models.

Geography Analysis

North America held a 38.71% share in 2025, buoyed by early BYOD uptake, rigorous cyber-insurance clauses, and a dense vendor ecosystem. The United States Cybersecurity and Infrastructure Security Agency classifies endpoint management as a core safeguard for critical infrastructure, accelerating public-sector rollouts.[4]Cybersecurity and Infrastructure Security Agency, “Cross-Sector Cybersecurity Performance Goals,” cisa.gov Canadian and Mexican data-protection laws are driving the growth of regionally hosted cloud instances, yet the United States-Mexico-Canada Agreement facilitates cross-border data flow. Market growth steadies as large enterprises near saturation, but small firms without dedicated IT staff remain a significant expansion vector for the Mobile Device Management market.

Europe’s trajectory depends on GDPR compliance and ESG directives. Germany, the United Kingdom, and France anchor demand, while the Corporate Sustainability Due Diligence Directive rewards vendors that disclose their carbon footprints and support the right to repair. Russian sanctions restrict Western cloud services, prompting the development of domestic alternatives. Works councils routinely negotiate device-tracking limitations under GDPR Article 88, affecting feature uptake more than license volumes.

Asia Pacific is the fastest-growing region at 10.23% CAGR, underpinned by India’s Digital India scheme, China’s smart manufacturing push, and Japan’s Society 5.0 infrastructure vision. South Korea’s mature 5G landscape encourages early adoption of low-latency MDM features for autonomous systems. Australia and New Zealand strengthen cybersecurity baselines through the Essential Eight, reinforcing MDM’s role. The Middle East sees momentum in the United Arab Emirates and Saudi Arabia, while Africa’s nascent uptake concentrates in Nigeria and Kenya’s fintech ecosystems. Collectively, these initiatives broaden the Mobile Device Management market but demand feature localization and sovereign data hosting.

Regulatory Landscape

Mobile device management deployments are increasingly shaped by security and data-governance rules that tighten requirements for managed endpoints and connected products. In the European Union, the Digital Operational Resilience Act (DORA) took effect in January 2025 for financial entities, elevating expectations for complete ICT asset inventories and control testing, areas where MDM and unified endpoint management consoles are used to document managed devices, encryption status, and configuration compliance.

Data sovereignty and product-security obligations also influence platform architecture and vendor operating models. The EU Data Act introduced data access and portability obligations that apply from September 12, 2025, and adds data-by-design obligations for new connected products from September 12, 2026, increasing focus on interoperability and data-handling transparency around managed connected endpoints. Separately, the EU Cyber Resilience Act (Regulation (EU) 2024/2847) mandates cybersecurity requirements for products with digital elements and ties vulnerability handling to defined support periods (Article 13 sets a minimum support period of five years unless the expected use duration is shorter), reinforcing demand for MDM capabilities that can evidence patching, inventory accuracy, and lifecycle policy enforcement across fleets. In the United States, NIST SP 800-124 Revision 2 continues to provide a baseline for enterprise mobile device security strategy, explicitly emphasizing centralized management approaches across the device lifecycle.

Value Chain Analysis

The MDM value chain begins with device and OS ecosystems that supply enrollment, attestation, and policy hooks, then extends into platform vendors that deliver the management plane (console, agents, APIs, analytics, and compliance reporting) as software and subscriptions. Upstream dependencies include handset, rugged device, and IoT OEM capabilities for zero-touch provisioning and hardware-backed identity, along with PKI and certificate services for encryption and authentication. Adjacent security and identity layers, including IdPs, SIEM, EDR, and application management, form core integration points that determine implementation scope and total cost, particularly where enterprises must connect MDM to legacy IAM and ITSM workflows.

Downstream, distribution and delivery occur through direct enterprise sales, cloud marketplaces, channel partners, and managed mobility services (MMS) providers that bundle procurement, staging, kitting, enrollment, break-fix, and end-user support with software policies for large or geographically dispersed fleets. As organizations strengthen IT supply chain resilience and nth-party risk management, vendor due diligence increasingly covers platform hosting, subcontractors, and API dependencies, pushing MDM providers and service partners to document controls and operational continuity. The shift toward unified endpoint management and IoT/Things management also expands ecosystem participation from carriers and private 5G integrators to industrial device OEMs, adding more stakeholders to onboarding, credentialing, and lifecycle refresh cycles.

Competitive Landscape

The top five suppliers - Microsoft, VMware, IBM, JAMF, and BlackBerry - hold roughly 45% to 50% combined revenue, creating moderate market concentration. Microsoft bundles Intune with Microsoft 365, cross-selling to an entrenched Azure Active Directory base and automating zero-touch provisioning via Windows Autopilot. VMware Workspace ONE, now under Broadcom, fuses desktop virtualization, device management, and security analytics. IBM’s MaaS360 layers Watson AI for anomaly detection, correlating telemetry against global threat patterns. JAMF controls the Apple niche, where creative and education sectors dominate, and recently partnered with Apple on hardware-backed attestation.

Gap areas persist in rugged IoT devices, where standard MDM agents drain batteries. Emerging players like Hexnode, 42Gears, and Scalefusion target small businesses in India and Southeast Asia with lightweight agents and support in local languages. NIST’s post-quantum cryptography standards have sparked a race to retrofit algorithms, benefiting vendors with deep in-house cryptography expertise. Carriers, including Verizon and AT&T, bundle MDM with 5G data plans, embedding endpoint posture checks into network slices and simplifying procurement for field-service clients.

Price increases, such as Broadcom’s 15% to 20% hike after integrating Workspace ONE with Symantec, prompt some customers to evaluate alternatives, sustaining churn dynamics that prevent oligopoly. Overall, innovation hinges on cryptographic agility, API openness, and sovereignty flexibility rather than classic feature parity, steering the Mobile Device Management market toward services-led differentiation.

Mobile Device Management Industry Leaders

VMware Inc.

Microsoft Corporation (Intune)

IBM Corporation

Citrix Systems Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity centers on deeper application governance inside device management programs, as enterprises tighten control over app versions, update cadence, and access to sensitive resources. Microsoft Intune actions in 2026, including enforcement of minimum app versions on Android and service-release features such as Enterprise Application Management auto-updates and enrollment improvements for personally owned devices with work profiles, highlight active buyer needs around reducing exposure from outdated clients and simplifying BYOD onboarding. These developments support demand for MDM offerings that combine device posture, app policy, and identity-driven access decisions in a single workflow, particularly for organizations standardizing on cloud-native management.

A second whitespace area is management-plane hardening and auditability, driven by both regulatory pressure and attacker behavior that targets administrative control layers. The Cloud Security Alliance framing of MDM/EMM infrastructure as an enterprise wiper attack surface reinforces buyer scrutiny of privileged access controls, phishing-resistant MFA, incident response readiness, and delegated administration in MDM consoles. Alongside this, post-quantum security preparations and hardware-backed attestation trends elevate requirements for cryptographic agility and device identity assurance, creating room for vendors and service partners that can operationalize certificate rotation, firmware trust signals, and lifecycle transparency across smartphones, rugged devices, and IoT/IIoT endpoints.

Recent Industry Developments

- June 2026: Microsoft announced that advanced Microsoft Intune Suite capabilities, including Intune Remote Help, Advanced Analytics, and Microsoft Tunnel for Mobile Application Management, are scheduled to roll out to Microsoft 365 E3 and E5 enterprise customers in Q3 2026. The move strengthens Microsoft’s bundling strategy by placing higher-value management and support functions inside broadly adopted productivity licenses. It also raises competitive pressure on standalone MDM vendors that differentiate through add-on modules for remote assistance, analytics, and secure access.

- April 2026: IBM launched MaaS360 Smart Device Groups to enable near real-time device classification and policy application based on dynamic attribute monitoring. This adds operational leverage for large fleets where static group assignments slow response to configuration drift and emerging risk. The capability supports more continuous policy enforcement, aligning MDM workflows with zero-trust and audit requirements that depend on current device posture.

- March 2026: IBM highlighted a large-scale deployment in which Beacon Mobility used MaaS360 to manage 10,000 Android tablets with centralized enrollment, configuration, and security controls. The example underscores the role of MDM in operationally intensive environments such as transportation and logistics where device uptime, standardized configurations, and remote support drive service reliability. It also showcases the platform and services ecosystem around large rollouts, including provisioning processes and policy consistency across distributed users.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the mobile device management (MDM) market covers commercial software and related subscription services used by IT teams to enroll, configure, secure, monitor, and remotely wipe enterprise endpoints through a centralized console.

Scope exclusions: Stand-alone mobile threat defense tools, device connectivity services, and hardware-only locking or tracking features are excluded.

Segmentation Overview

- By Deployment Mode

- On-Premise

- Cloud

- By Device Type

- Smartphones and Tablets

- Laptops and Desktops

- Rugged and Wearable Devices

- IoT/IIoT Endpoints

- By End-User Industry

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Retail and E-Commerce

- Government and Public Sector

- Manufacturing

- Education

- Transportation and Logistics

- By Ownership Model

- Corporate-Owned Devices

- BYOD

- COPE (Corporate-Owned, Personally Enabled)

- CYOD (Choose-Your-Own-Device)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to make sure our assumptions match how enterprises actually manage device fleets. We relied on public source types such as cybersecurity and mobility guidance from NIST, communications and device statistics from the ITU, and labor and digital adoption indicators from the World Bank and OECD.

We also reviewed company filings, investor presentations, product documentation, and reputable press coverage to map typical pricing models (per device, per user, and bundled endpoint suites) and to track deployment shifts toward cloud consoles. Where public disclosures were limited, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases to cross-check product scope language and investment signals. These examples are not exhaustive, and many other sources were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test device-per-employee assumptions, MDM attach rates by endpoint type, and typical annual contract values across cloud and on-prem deployments. We spoke with a mix of buyers, channel partners, and solution implementers across major regions so the adoption curve reflected differences in compliance needs, remote work intensity, and device refresh patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 44% |

| Mid tier: 59% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 16% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

Market sizing starts with a top-down demand pool build where enterprise endpoint counts and managed device penetration are used to reconstruct the paid MDM addressable base by region. After that, spend per managed endpoint is applied to reach the total market value. To keep the estimate realistic, the output is then checked using selective bottom-up approximations, such as sampled price points from common contract structures and channel checks on typical deal sizes, followed by adjustments where the two views do not align.

Key inputs used in the model include the installed base of smartphones, tablets, and laptops used for work, enterprise BYOD and COPE policy prevalence, compliance-driven management needs in regulated industries, cloud console adoption trends, and average pricing progression for per-device subscriptions and support. When any input was not consistently available, we used a conservative proxy and revalidated the assumption in follow-up calls so the gap did not inflate the total.

For forecasting, we primarily use scenario analysis supported by regression checks against leading indicators like device fleet growth, remote work persistence, and security policy tightening, which were also discussed with interviewees. The final forecast path is chosen only after short-term adoption constraints and pricing normalization trends are reflected in the year-by-year build.

Data Validation & Update Cycle

Validation is done through multiple checks so the final numbers are traceable to a few clear drivers. We compare outputs against independent signals like enterprise endpoint growth, cloud adoption movement, and changes in security and compliance mandates, and then investigate any large variance before sign-off.

If a large disconnect appears between regions or between device categories, the model is revisited and assumptions are re-tested with follow-up outreach to practitioners. Reports are refreshed annually, and interim updates are made when material events shift adoption or pricing expectations. Before delivery, a final analyst review pass is completed so clients receive the most current view.

Mordor Intelligence's Mobile Device Management Market Sizing Compared With Other Published Estimates

Published market numbers for MDM do not always match because studies may count different product bundles, follow different timing for base years, or apply different pricing logic across devices and users. We looked at the common drivers behind these gaps so readers can understand why the spread happens.

The biggest differences usually come from what gets counted as MDM versus adjacent endpoint tools, how bundles are split across modules, and whether the value includes services that sit outside device administration. Different currency conversion timing and refresh cadence can also move the current-year value up or down, even when the long-term direction looks similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.11 B (2026) | |

| Global Consultancy A | USD 7.67 B (2024) | Uses an earlier base year and a narrower device-and-service interpretation in which spending is more tightly tied to mobile-only endpoints and a shorter historical window, which can keep current value lower even when growth is modeled faster. |

| Industry Publisher B | USD 15.75 B (2025) | Blends a wider suite-style scope where unified endpoint bundles and adjacent management features can be attributed into the MDM total, and it also applies a different pricing escalation path through the forecast window. |

The spread is mainly explained by what is counted inside the MDM scope and how bundled endpoint suites are allocated, a modeling choice used by Mordor Intelligence so only commercial-grade MDM software and related subscriptions are counted, while stand-alone threat defense tools and device connectivity are kept out.

Key Questions Answered in the Report

What is the current value of the Mobile Device Management market?

The market is valued at USD 11.11 billion in 2026 and is forecast to reach USD 26.04 billion by 2031.

How fast is the Mobile Device Management market expected to grow?

It is projected to post an 18.57% CAGR between 2026 and 2031.

Which deployment mode leads revenue?

Cloud platforms held 65.13% of 2025 revenue, reflecting enterprises’ preference for elastic scaling and zero-touch provisioning.

Which region will grow the fastest?

Asia Pacific is expected to register a 10.23% CAGR through 2031, driven by large-scale digitalization programs in India, China, and Japan.

Why is healthcare a high-growth vertical?

Telehealth, remote patient monitoring, and strict HIPAA security rules drive a 21.32% CAGR for healthcare and life sciences through 2031.

How are cyber-insurance requirements influencing adoption?

Insurers now demand proof of endpoint control, and enterprises lacking MDM face premium hikes of 50% or policy denials, prompting accelerated deployment.

Page last updated on: