Seaweed-Based Barrier Paperboard Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

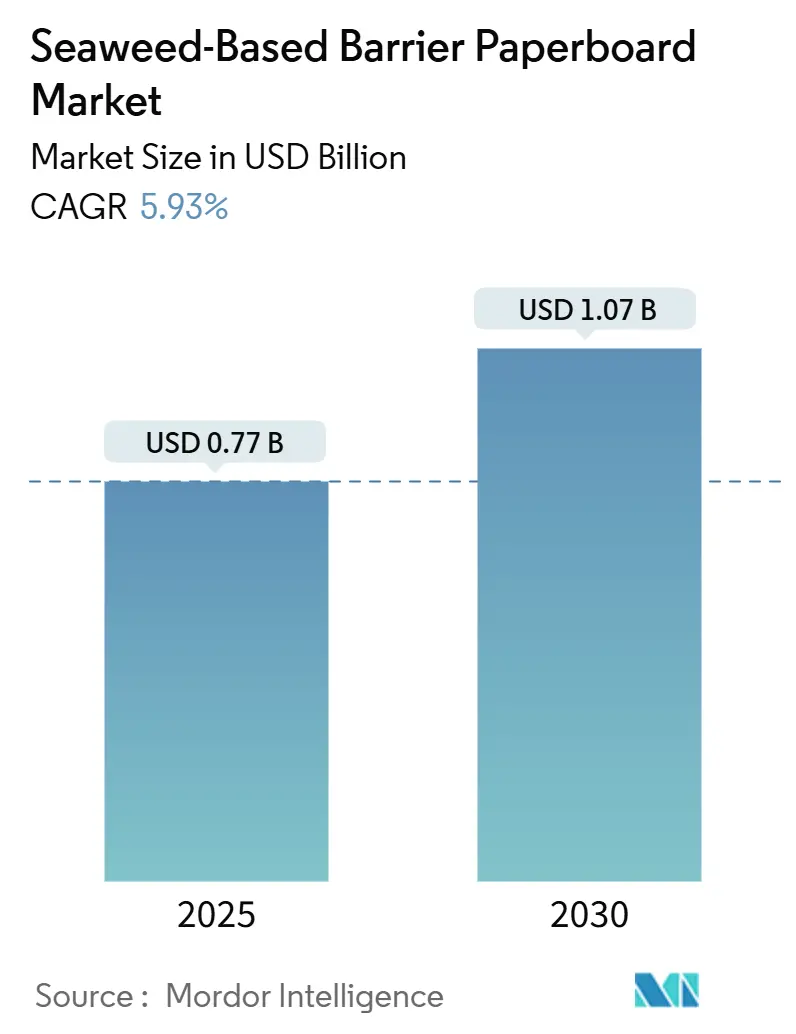

| Market Size (2025) | USD 0.77 Billion |

| Market Size (2030) | USD 1.07 Billion |

| Growth Rate (2025 - 2030) | 5.93% CAGR |

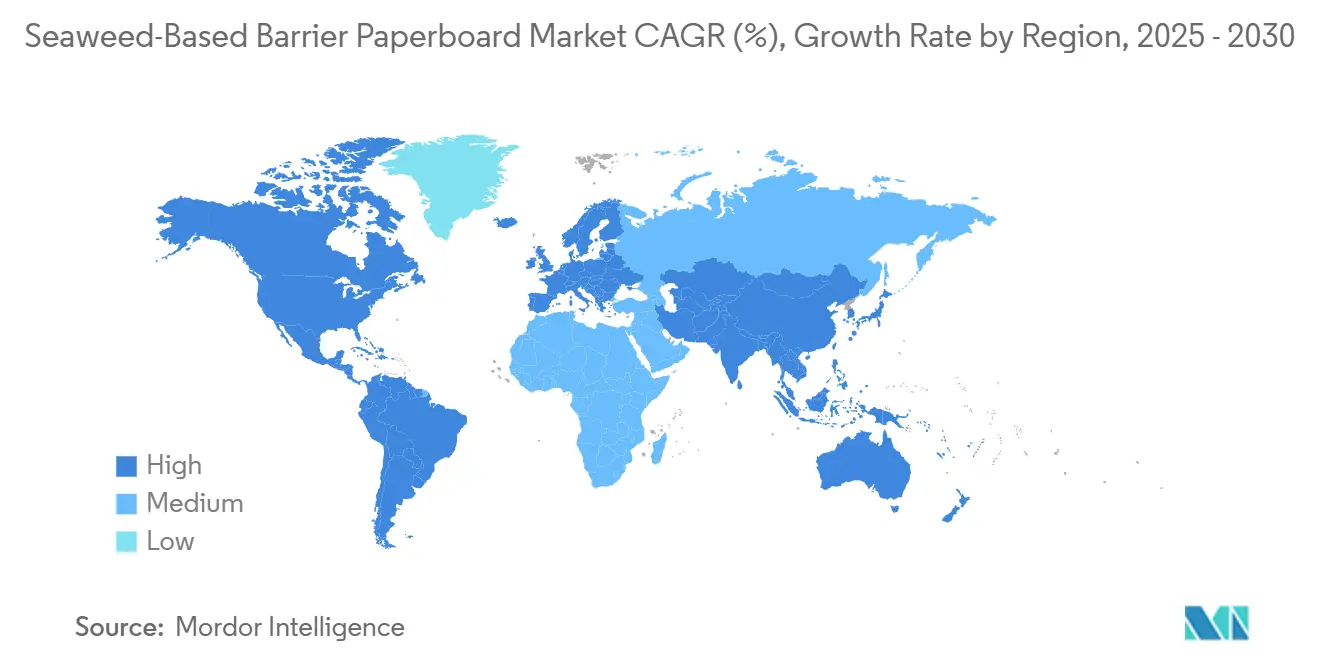

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Seaweed-Based Barrier Paperboard Market Analysis by Mordor Intelligence

The seaweed-based barrier paperboard market size is valued at USD 770.2 million in 2025 and is forecast to expand at a 5.93% CAGR, reaching USD 1,027.2 million by 2030. Growth rests on three pillars: binding regulations that phase out PFAS coatings, corporate sustainability targets that prioritize marine-derived packaging, and the resource efficiency of seaweed cultivation that requires neither arable land nor freshwater.[1]U.S. Food and Drug Administration, “FDA Determines Authorization for 35 Food Contact Notifications Related to PFAS Are No Longer Effective,” fda.gov Brands now view feedstock resilience, cost parity prospects, and positive consumer sentiment as interlocking advantages, while converters emphasize barrier performance that matches polyethylene or PLA without added capital expense. Established Asian cultivation hubs ensure feedstock security, European research programs de-risk technology, and North American policy shifts accelerate adoption, together forming a global demand flywheel for the seaweed-based barrier paperboard market.

Key Report Takeaways

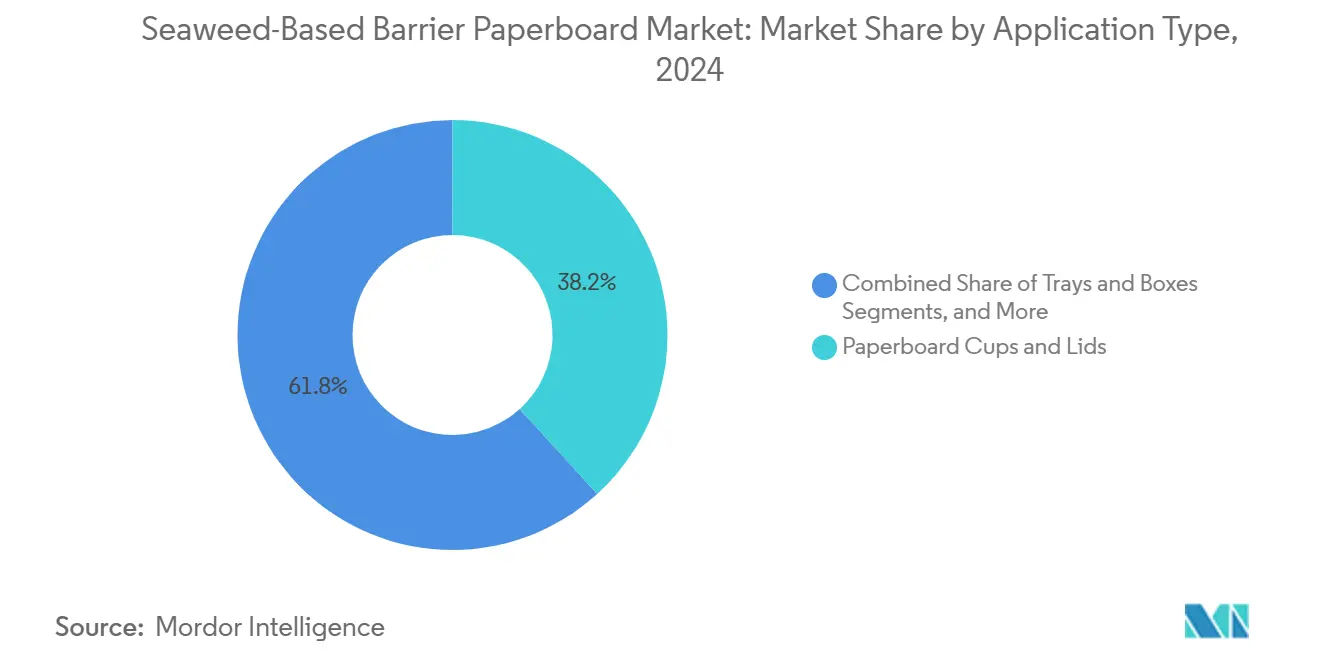

- By application, the seaweed-based barrier paperboard market size for paperboard cups and lids segment is projected to grow at a 6.7% CAGR between 2025-2030.

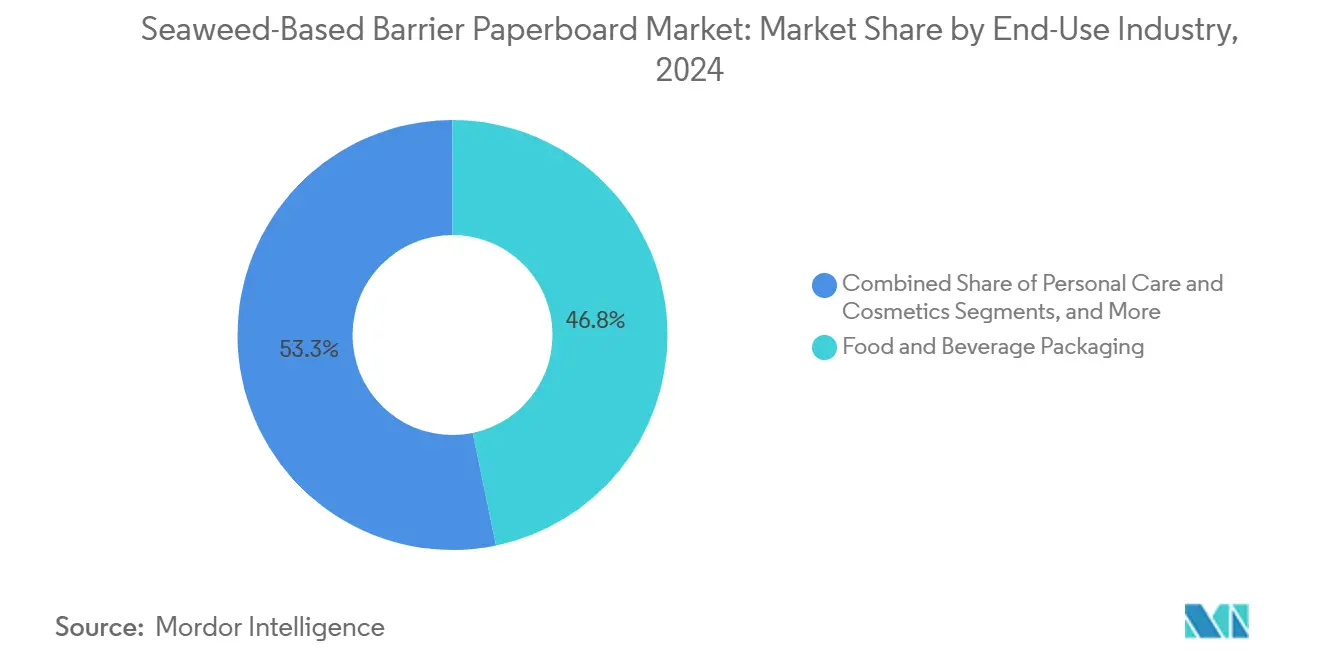

- By end-use industry, food and beverage packaging captured 46.75% of the seaweed-based barrier paperboard market share in 2024.

- By geography, the seaweed-based barrier paperboard market size for the Asia-Pacific region is projected to grow at an 8.6% CAGR between 2025-2030.

Global Seaweed-Based Barrier Paperboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream Plastic-Reduction Policies | +1.8% | Global, led by EU and North America | Medium term (2-4 years) |

| Brand Sustainability Mandates | +1.2% | North America and EU, expanding into APAC | Short term (≤2 years) |

| Commercial-Scale Seaweed Fiber Integration | +1.0% | Core APAC; spill-over to EU and North America | Long term (≥4 years) |

| Declining Alginate Extraction Costs | +0.8% | Global, strongest in major cultivation zones | Medium term (2-4 years) |

| Carbon-Credit Monetization | +0.6% | EU and North America; emerging APAC | Long term (≥4 years) |

| Circular-Economy Partnerships with Quick-Service Restaurants | +0.5% | North America and EU, pilots in APAC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Mainstream Plastic-Reduction Policies

Legally binding bans on single-use plastics alter procurement norms and trigger mandatory substitution in favor of biodegradable options. The EU Packaging and Packaging Waste Regulation exemplifies this enforcement approach. A Duke University policy inventory covering two decades reports that 73% of global plastic policies mandate rather than incentivize change, creating clear demand signals for converters that invest in seaweed coatings.[2]Rachel Karasik et al., “20 Years of Government Responses to the Global Plastic Pollution Problem,” nicholasinstitute.duke.edu Universal compliance removes price-based disadvantages and encourages standardization across primary and secondary packaging lines.

Brand Sustainability Mandates

Large consumer-facing companies increasingly anchor purchasing contracts to compostability and carbon intensity benchmarks. Mondi disclosed that reusable, recyclable, or compostable products generated 87% of 2024 packaging revenue, proving commercial traction for sustainability positioning. Seaweed-based barrier paperboard benefits from this brand pull, especially in premium segments such as baby care, where hypoallergenic credentials command higher price points.

Commercial-Scale Seaweed Fiber Integration

Deep eutectic solvents now recover 51.2% alginate, pushing extraction yields to levels that support industrial economics. Compatibility trials show that seaweed slurries can be dosed into existing size-press lines without major retrofits, which lowers capital hurdles. As global production surpasses 7.5 million tonnes per year, attention shifts from lab validation to line throughput, with partnerships between fiber innovators and paperboard majors accelerating knowledge transfer.

Declining Alginate Extraction Costs

Microwave and ultrasound-assisted methods cut processing time and solvent consumption, lifting overall economics of alginate supply chains. The global alginate market, valued at USD 770 million in 2021, already prices in a 5.02% CAGR thanks to growing economies of scale. Coupling barrier production with cascade valorization such as extracting nutraceuticals ahead of fiber isolation—spreads capex across multiple revenue streams and moves seaweed-based barrier paperboard closer to cost parity with polyethylene coatings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Price versus PE/PLA Coatings | -1.5% | Global, strongest in price-sensitive regions | Short term (≤2 years) |

| Limited Industrial Capacity and Feedstock | -1.2% | Global, acute in Europe and North America | Medium term (2-4 years) |

| Seasonal Variability in Seaweed Composition | -0.8% | Temperate zones of North Atlantic and North Pacific | Long term (≥4 years) |

| Certification and Traceability Ambiguity | -0.6% | Global, complex cross-border trade | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Premium Price versus PE/PLA Coatings

Seaweed-based barriers currently command a 20-40% premium over petro-based coatings, reflecting smaller production runs and specialized extraction kit. A cradle-to-gate assessment notes 10-52 kg CO₂e per kg wet weight, translating into higher unit costs in commodity food segments. Carbon taxes and PFAS-related liabilities are expected to erode that differential, yet price pressure remains the chief brake on mass conversion in the near term.

Limited Industrial Capacity and Feedstock

More than 80% of global cultivated biomass originates in China, Korea, and Japan, while European and North American converters still rely on imports. The resulting shipping costs and currency exposure create risk for manufacturers whose clients demand local sourcing guarantees. Western start-ups plan 8 million tonnes of extra capacity by 2030, but current volumes trail demand projections, making long-term offtake contracts essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Type: Cups Drive Foodservice Transformation

Paperboard cups and lids captured 38.24% of 2024 revenue within the seaweed-based barrier paperboard market size and post the fastest 6.7% CAGR forecast to 2030, supported by quick-service mandates that phase out fluorinated grease barriers. Seamless integration into existing cup-stock lines and the ability to withstand hot and cold beverages place this format at the center of foodservice decarbonization roadmaps. Beyond beverages, the segment benefits from national plastic levies that raise costs of alternative polymers.

Trays and boxes follow in volume, aligned with the surge in fresh-meal delivery services that require moisture resistance during chilled transit. Flexible wraps remain smaller in tonnage yet attract premium brand adoption when antimicrobial carrageenan blends add shelf-life functionality. Labels and tags hold niche share but register double-digit growth as apparel and cosmetics players harmonize every packaging component under single material platforms to streamline recycling streams. Together these applications illustrate how performance requirements and equipment compatibility dictate the order in which seaweed-based barrier paperboard penetrates markets.

By End-Use Industry: Personal Care Accelerates Premium Adoption

Food and beverage packaging retained a 46.75% share in 2024, keeping leadership in the seaweed-based barrier paperboard market, anchored by FDA GRAS status for brown algae derivatives that ease compliance risk.[3]U.S. Food and Drug Administration, “21 CFR 176.170 — Components of Paper and Paperboard in Contact with Aqueous and Fatty Foods,” ecfr.gov Converters supply major snack, bakery, and chilled-meal brands that seek grease, moisture, and oxygen barriers without PFAS or synthetic waxes.

Personal care and cosmetics, at a 6.2% CAGR, represent the next frontier as sensitive-skin formulations demand hypoallergenic and compostable packs. A systematic review shows 61% of baby-care labels already employ sustainable substrates, and seaweed-based barrier paperboard answers shelf appeal and compliance goals in one material choice. Foodservice, pharmaceuticals, and consumer electronics occupy smaller but rising shares, each driven by discrete value propositions, contact safety, regulatory headroom, or moisture barrier without ion migration, respectively.

Geography Analysis

Asia-Pacific generated 38.56% of 2024 sales and is projected to compound at 8.6% annually, underpinned by an integrated cultivation-to-conversion ecosystem that yields steady biomass at low landed cost. China harvests 5 million tonnes each year, South Korea 800,000 tonnes, and Japan 600,000 tonnes, collectively anchoring raw material supply for converters across the region. Export revenues of USD 525 million in Korean seaweed underscore commercial maturity.

Europe ranks second in value, propped by policy incentives and R&D programs such as the SeaFilm project, which validates alginate coatings for frozen seafood wraps. Yet local cultivation lags, forcing reliance on imports while regional roadmaps target 8 million tonnes of added capacity by 2030. North America sees accelerated demand after the 2025 PFAS notification withdrawal, though feedstock security hinges on west-coast kelp farm scaling backed by USDA support.

South America and the Middle East and Africa remain nascent, yet they display leapfrog potential as regulators fast-track sustainable materials and coastal zones explore aquaculture for economic diversification.

Competitive Landscape

The seaweed-based barrier paperboard market shows fragmentation that favors alliances between scale manufacturers and biotech specialists. DS Smith, Mondi Group, and International Paper test seaweed fibers within existing barrier formulations, leveraging established customer bases and mill networks.

Notpla, Sway Innovation, Kelpi, and Oceanium occupy the materials innovation space, routinely drawing public grants to mature extraction and resin chemistries. Sway secured USD 272,000 from the National Science Foundation to optimize thermoplastic seaweed resin that feeds directly into film extrusion lines. Competition pivots on barrier metrics, process throughput, and intellectual property breadth, with first movers racing to patent species-specific blends that improve moisture vapor transmission rates or oil resistance.

Cost parity remains the finish line. Companies hedge by working on cascade valorization, capturing food additives or cosmetica actives before harvesting fiber, thereby subsidizing barrier paperboard economics. Market exit risks center on feedstock shortages, underscoring the advantage of vertical integration or long-term supply agreements with Asian farms.

Seaweed-Based Barrier Paperboard Industry Leaders

Notpla Ltd.

B’ZEOS AS

Sway Innovation Co.

Marine Innovation Co Ltd.

Kelpi Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA ruled 35 PFAS food-contact notifications ineffective, setting a June 30 2025 compliance deadline that opens immediate space for seaweed barriers.

- September 2024: The USDA report highlighted the rapid expansion of the United States seaweed farming and its potential as a bioplastic feedstock.

- July 2024: Mondi allocated EUR 1.2 billion (USD 1.29 billion) to organic growth projects that include marine-derived barrier technologies.

- May 2024: Sway Innovation received USD 272,000 from the National Science Foundation to scale Thermoplastic Seaweed Resin aimed at polybags and food packaging.

Global Seaweed-Based Barrier Paperboard Market Report Scope

| Paperboard Cups and Lids |

| Trays and Boxes |

| Flexible Paper Wraps |

| Labels and Tags |

| Food and Beverage Packaging |

| Foodservice and Take-away |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Consumer Electronics Packaging |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application Type | Paperboard Cups and Lids | ||

| Trays and Boxes | |||

| Flexible Paper Wraps | |||

| Labels and Tags | |||

| By End-use Industry | Food and Beverage Packaging | ||

| Foodservice and Take-away | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Consumer Electronics Packaging | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the seaweed-based barrier paperboard market?

The market is worth USD 770.2 million in 2025 and is projected to reach USD 1,027.2 million by 2030 at a 5.93% CAGR.

Which application leads market share today?

Paperboard cups and lids hold 38.24% share and also record the fastest 6.7% CAGR through 2030.

Why does Asia-Pacific dominate the seaweed-based barrier paperboard market?

The region supplies more than 80% of global cultivated seaweed, providing cost-effective feedstock and integrated processing infrastructure that secure 38.56% of 2024 market revenue.

How do recent PFAS regulations affect demand?

The FDA withdrawal of 35 PFAS food-contact approvals effective June 30 2025 forces converters to adopt alternative barriers, immediately expanding demand for seaweed-based coatings.

Which end-use segment is growing fastest?

Personal care and cosmetics packaging grows at a 6.2% CAGR, driven by premium branding and hypoallergenic material requirements.

Page last updated on: