Biopolymer-Coated Paperboard Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

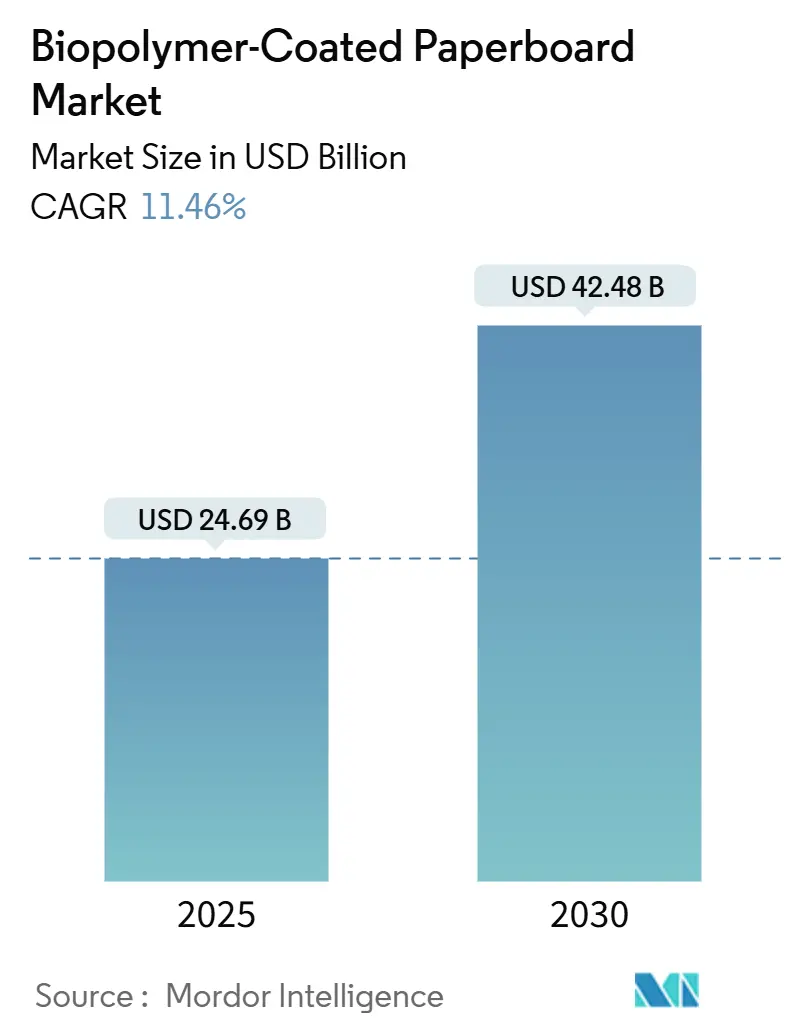

| Market Size (2025) | USD 24.69 Billion |

| Market Size (2030) | USD 42.48 Billion |

| Growth Rate (2025 - 2030) | 11.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biopolymer-Coated Paperboard Market Analysis by Mordor Intelligence

The global biopolymer-coated paperboard market size stands at USD 24.69 billion in 2025 and is projected to reach USD 42.48 billion by 2030, delivering an 11.46% CAGR through the forecast period. The regulatory clamp-down on single-use plastics, escalating brand sustainability mandates, and maturing bio-based barrier technologies collectively fuel this rise. Robust investment in PLA and PHA capacity lowers raw-material costs and mitigates supply risk, widening the addressable applications for foodservice, beverage, and personal-care packaging. Brands demand life-cycle transparency, prompting converters to prioritize coatings that meet recyclability thresholds without disrupting existing fiber collection streams. Equipment upgrades, notably high-speed water-based dispersion lines, now allow legacy mills to retrofit rather than replace infrastructure, compressing payback cycles on capital employed. The biopolymer-coated paperboard market also benefits from e-commerce cold-chain expansion, which requires fiber-based insulation solutions compatible with curbside recovery systems.

Key Report Takeaways

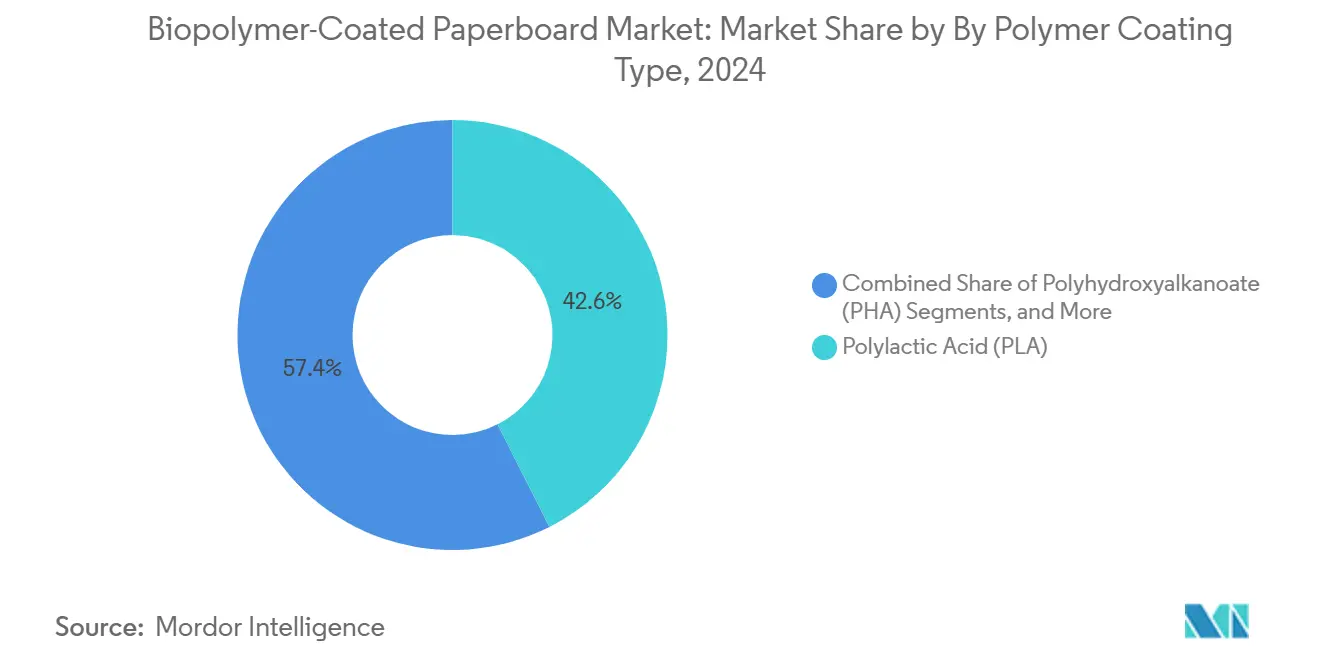

- By polymer coating, the biopolymer-coated paperboard market size for the PHA segment is projected to grow at a 13.23% CAGR between 2025-2030.

- By board grade, cupstock captured 32.74% of the biopolymer-coated paperboard market share in 2024.

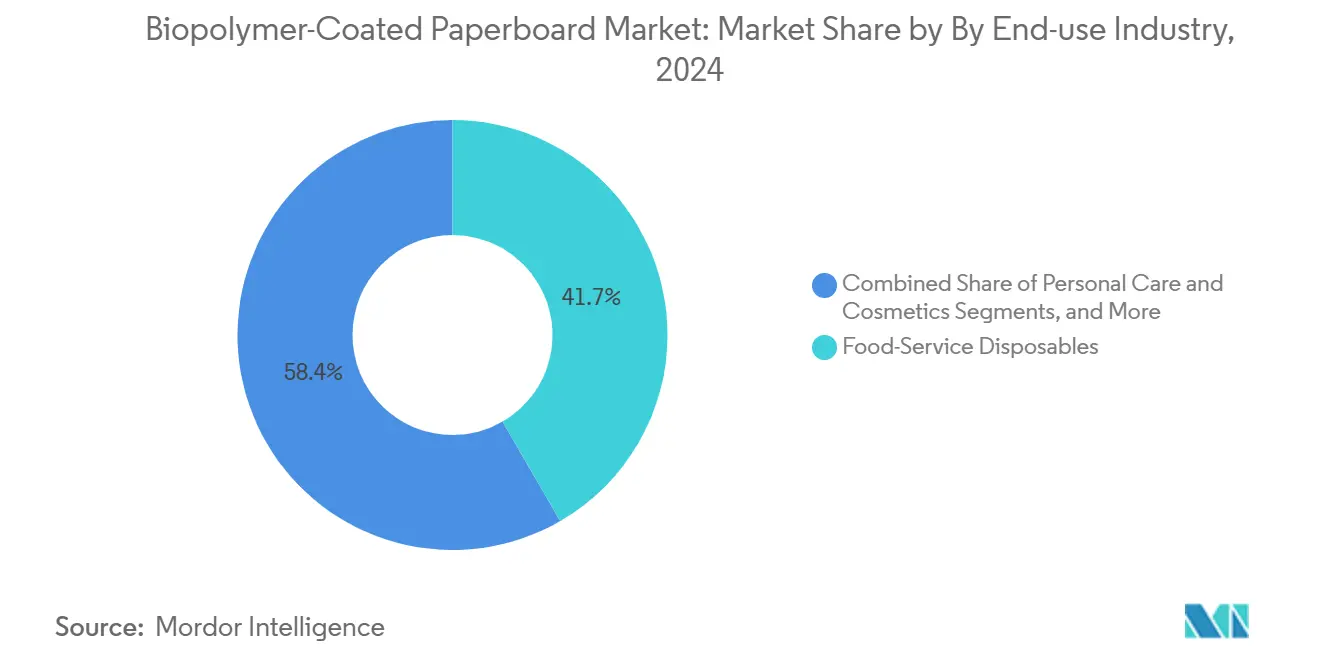

- By end-use, the biopolymer-coated paperboard market size for the personal care applications is projected to grow at a 12.85% CAGR between 2025-2030.

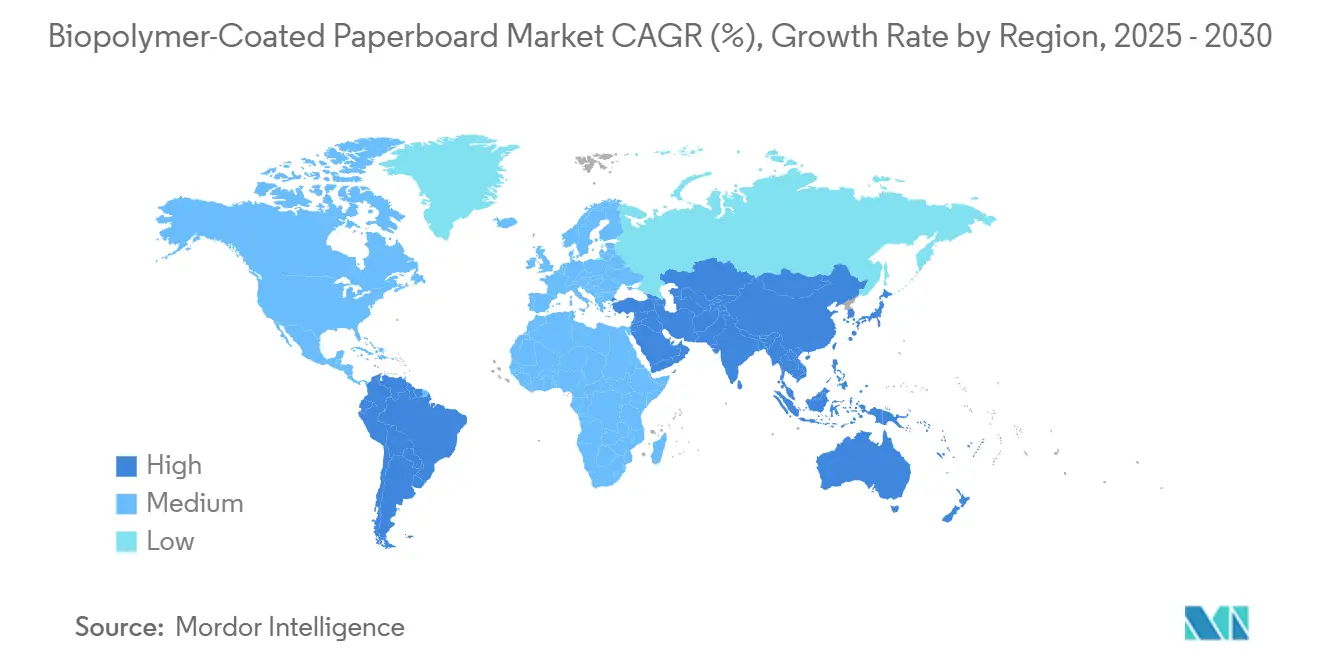

- By geography, Asia-Pacific captured a 13.18% of the biopolymer-coated paperboard market share in 2024.

Global Biopolymer-Coated Paperboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use-plastic legislation acceleration | +2.8% | Global with EU and North America leading | Short term (≤ 2 years) |

| Brand-owner ESG and recyclability demands | +2.1% | Global concentrated in developed markets | Medium term (2-4 years) |

| Rapid advances in water-based dispersion lines | +1.9% | North America and Europe expanding to APAC | Medium term (2-4 years) |

| Cost decline from new PLA/PHA capacity | +1.7% | Global with major capacity in APAC and North America | Long term (≥ 4 years) |

| E-commerce cold-chain insulated packs | +1.4% | Global led by North America and Europe | Short term (≤ 2 years) |

| Retailer take-back cupstock recycling | +1.2% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-use-plastic Legislation Acceleration

Governments are accelerating bans and levies on throw-away plastics, compressing decision windows for brand owners that wish to avoid non-compliance penalties. The EU rules, effective March 2025, stipulate recycled-content quotas and recyclability criteria that fiber-based packaging can meet more readily than multilayer plastics. Similar trajectories appear in California, which publishes an approved list that overwhelmingly favors fiber over polymer items.[1]State of California, “List of Approved Food Service Packaging,” calrecycle.ca.gov Multinationals must therefore harmonize pack formats across regions, which intensifies interest in the biopolymer-coated paperboard market for beverages, take-away foods, and ready meals. Rapid regulatory rollouts favor substrates that slot into existing curbside recovery streams, offering immediate compliance without costly downstream infrastructure changes. The momentum lifts order volumes for cupstock and folding boxboard converted with bio-barriers.

Brand-owner ESG and Recyclability Demands

Corporate environmental pledges increasingly exceed statutory baselines. Mondelēz targets 98% recyclable packs by 2025, compelling suppliers to validate fiber-plus-bio-barrier options through life-cycle studies and third-party audits. Consumer polling consistently links sustainable packaging with brand trust in premium categories. Procurement teams are now embedding recyclability and fiber sourcing clauses in tender documents, creating price premiums for converters that can certify closed-loop compatibility. Partnerships between converters and ingredient producers accelerate bespoke barrier formulations tailored to confectionery, snacks, and cosmetics. As ESG reporting tightens, the reputational upside of compliant packaging intensifies, further propelling the biopolymer-coated paperboard market.

Rapid Advances in Water-based Dispersion Coating Lines

Retrofitting legacy mills with water-based dispersion technology slashes VOC emissions while permitting high-speed runs above 600 m/min, a threshold traditionally reserved for PE coatings. Eastman’s Solus additives enhance wetting and adhesion, which cuts coat-weight yet sustains grease, moisture, and mineral-oil resistance. The capital requirement for retrofits sits well below that of greenfield polymer extrusion, lowering barriers for regional players. Shorter drying tunnels and reduced energy loads deliver operating-expense benefits that offset biopolymer resin premiums. These equipment gains allow medium-scale mills in Latin America and Southeast Asia to supply certified food-contact grades to multinational buyers, expanding geographic availability of compliant substrates.

Cost Decline from New PLA/PHA Biorefinery Capacity

NatureWorks’ 75,000-ton facility in Thailand and the Emirates Biotech project in the UAE will raise global PLA availability by nearly 25% once fully online. Scale economies, broader feedstock sourcing, and process intensification lower cost per kilogram, narrowing the price gap with fossil-based PE. PHA scaling by Danimer Scientific backed by a USD 700 million Georgia expansion brings another 125,000 tons by 2028, improving supply diversification. As spot resin prices moderate, converters secure multi-year supply contracts that stabilize input costs, enabling wider use in value-sensitive foodservice segments. Price predictability also unlocks investment in dedicated extrusion and curtain-coating assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus PE-coated board | -1.8% | Global most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Scarcity of industrial composting infrastructure | -1.3% | Global particularly acute in developing markets | Long term (≥ 4 years) |

| Feed-stock supply volatility for lactic-acid/PHA | -1.1% | Global with regional variations | Medium term (2-4 years) |

| Barrier-performance gaps for high-fat foods approvals | -0.9% | Global affecting specific food categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Premium versus PE-Coated Board

Biopolymer-coated grades command 15-30% price uplifts over PE-lined alternatives, which hampers penetration in cost-sensitive fisheries, produce, and quick-service restaurant channels. Commodity foodservice distributors remain cautious until suppliers can demonstrate total-cost parity through fiber recovery credits or lightweighting. Economic slowdowns further sharpen price pressures, occasionally triggering category reversion to legacy plastics. USDA corn projections up to 2033 suggest feedstock stability, yet resin prices still hinge on new-plant ramp-ups and freight costs. Sustained scaling of PLA and PHA capacity is therefore critical to compress price differentials and unlock high-volume segments of the biopolymer-coated paperboard market.

Scarcity of Industrial Composting Infrastructure

Only a minority of municipalities worldwide operate sites that reach the 60 °C required to fully biodegrade PLA within mandated timeframes. The gap is acute in Latin America, Africa, and parts of Southeast Asia, where collection and processing networks remain underfunded. Consumers face disposal ambiguity, diminishing perceived environmental benefit and risking greenwashing accusations. Policy moves in New York City to mandate 180,000 tons of organics processing annually point to future infrastructure growth yet the build-out timeline outstrips product rollout cycles. Until composting access widens, market messaging must emphasize recyclability over biodegradability, somewhat constraining broader adoption.

Feed-Stock Supply Volatility for Lactic-Acid/PHA

Agricultural inputs for biopolymers compete with food, feed, and biofuel markets, so weather-driven yield swings ripple into resin pricing. Regional sugar-price spikes and logistic bottlenecks during 2024 presented allocation challenges for smaller converters. Forward-contracting helps but ties up working capital. Diversifying feedstock from corn to bagasse and second-generation cellulosic streams reduces exposure but demands process re-qualification. Larger producers leverage multi-site sourcing, whereas mid-tier players face sporadic shortages that delay rollouts of new barrier grades, tempering CAGR upside for the biopolymer-coated paperboard market.

Barrier-Performance Gaps for High-Fat Foods Hindering Approvals

Grease-heavy bakery and confectionery coverings still rely on fluorine-based treatments or EVOH laminates to prevent oil migration. Bio-based waxes and dispersion coatings improve yearly yet remain short of certain regulatory thresholds for shelf-life critical dairy and cheese wraps. Brands hesitate to sacrificially shorten best-before dates, leading to mixed-material workarounds that dilute recyclability. R&D pipelines focusing on layered nanocellulose or hybrid PHA blends promise gains, yet multi-year stability data are still pending. This performance lag slows certification timelines for a subset of food categories, keeping a lid on otherwise strong growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Coating Type: PLA Dominance Faces PHA Challenge

The PLA segment generated USD 10.5 billion during 2024 and accounted for 42.56% of biopolymer-coated paperboard market share. The mature regulatory track record for food contact, coupled with established supply chains across Asia, Europe, and North America, cements its position in hot-cup and folding-carton uses. PLA’s predictable melt-flow enables converters to run higher line speeds, which secures procurement preference among multinational quick-service chains. However, sustainability scorecards increasingly prioritise end-of-life options beyond recyclability. PHA’s marine and soil biodegradation profile resonates with regions lacking waste-collection coverage, which fuels a 13.23% CAGR and elevates investor interest in Danimer Scientific’s expansion.[2]Georgia Department of Economic Development, “Danimer Scientific Expansion,” georgia.org Rapid capacity additions are projected to push PHA shipments above 1.2 million tons by 2030, translating into a biopolymer-coated paperboard market size of USD 8.2 billion for the segment. Early adopters in cosmetics and specialty snacks signal willingness to pay the premium in exchange for unique sustainability claims, suggesting PLA will face incremental share erosion in high-margin niches.

Second-tier technologies fill performance or cost niches. Starch-based coatings win in compost-ready produce trays that need high starch content for certification. Bio-wax and vegetable-oil blends serve burger wraps where elevated grease resistance is essential, though print-adhesion limitations restrict global deployments. Nanocellulose dispersion solutions remain pre-commercial but have posted oxygen transmission rate reductions of up to 80%, a promising path toward replacing aluminium in aseptic board. Collectively, these alternatives expand the palette for converters aiming to tailor barrier profiles by product category, which sustains competitive tension in the biopolymer-coated paperboard industry.

By Board Grade: Cupstock Leadership Amid Liquid Packaging Surge

Cupstock contributed 32.74% of revenue in 2024, valued at USD 8.1 billion, and retains top rank within the biopolymer-coated paperboard market. Accelerated rollouts of fiber-lined hot and cold beverage cups by global café chains mirror legislative shifts that restrict polystyrene and PE-lined vessels. Cup recovery pilots in the United Kingdom and United States improve recycling economics, thereby enhancing the life-cycle argument for bio-barrier cupstock. Recovered fiber fetches premium pricing due to high brightness and low contaminant levels, reducing total cost of ownership for retailers engaged in closed-loop programs.

Liquid packaging board is advancing at a 13.07% CAGR, outpacing every other grade to reach an anticipated biopolymer-coated paperboard market size of USD 6.7 billion by 2030. Beverage brands are employing multi-layer structures combining fiber, bio-based barrier, and thin aluminium to maintain product integrity while shrinking fossil content. Stora Enso’s Oulu line expansion exemplifies mill investment designed to switch volumes from traditional PE-extruded gable-top formats to bio-liner alternatives in juice and dairy applications. Folding boxboard continues to supply personal-care cartons where printability and bending stiffness remain decisive. SBS barrier board finds traction in premium chocolate and nutraceuticals that demand high-gloss graphics alongside moisture resistance, though higher cost caps volume growth today.

By End-Use Industry: Food-Service Dominance with Personal Care Growth

Food-service disposables represented USD 10.3 billion in 2024, equal to 41.65% of the biopolymer-coated paperboard market. Fast-casual and quick-service restaurants deploy fiber-based lids, clamshells, and drink carriers to satisfy municipal bans and brand environmental scorecards. High-throughput usage intensifies buyer focus on consistent seal performance and heat stability, leading many chains to adopt PLA and hybrid coatings. Visibility of packaging waste in public realms also drives corporate activism, which directs R&D budgets toward lightweight bio-coated formats.

Personal care and cosmetics is the fastest mover, delivering a 12.85% CAGR on the back of premium brand positioning. Fragrance and skincare houses elevate unboxing experiences with textured fiber substrates that underline natural ingredient stories. Regulatory pressure on microplastics in Europe creates spill-over demand for plastic-free accessories, such as lipstick sleeves and sample sachets produced on thin-gauge barrier board. Food and beverage retail remains a stable contributor as supermarket own-brands migrate cereal liners and snack trays to single-material fiber packs. Healthcare and pharma experimentation is rising but still limited by sterility and shelf-life validations, pointing to medium-term revenue potential once barrier strengths reach stringent ISO norms.

Geography Analysis

Europe secured 33.92% of 2024 global revenue, equivalent to USD 8.4 billion, buoyed by advanced waste-management systems that integrate biopolymer-coated board into existing fiber loops. Germany, France, and the United Kingdom together consume more than half of the regional volume due to progressive extended producer responsibility fees that favour recyclable formats. Capital projects such as Mondi’s EUR 200 million (USD 216 million) recycled containerboard investment in Italy demonstrate entrenched confidence in long-term fiber demand.[3]Mondi Group, “€200 Million Recycled Containerboard Investment,” mondigroup.com Widespread consumer awareness translates into willingness to absorb modest price premiums, ensuring steady order intake for PLA-lined cupstock and folding cartons.

Asia-Pacific is expanding at a 13.18% CAGR and is on course to overtake Europe in volume by 2029, driven by e-commerce growth and supportive policies such as China’s revised solid-waste law that limits non-recyclable pack imports. Thailand’s new PLA plant and multiple Southeast Asian capacity additions shorten lead times and cut delivered costs across the region. The Australian Packaging Covenant’s 2025 targets catalyse converter upgrades, while Japan and South Korea pioneer nanocellulose dispersion projects that could deliver next-wave barrier breakthroughs. India represents an emerging hotspot thanks to organised retail expansion and central government mandates restricting single-use plastics, although collection infrastructure constraints still temper near-term scale.

North America delivers stable mid-single-digit growth anchored by state-level interventions such as California’s approved list, which directs procurement toward fiber solutions. Existing mill networks in the United States and Canada allow rapid qualification of new grades, slicing time-to-market for cupstock and frozen-food trays. Corporate sustainability charters from PepsiCo, Starbucks, and Walmart ensure consistent baseline demand, while cold-chain innovations push volumes in temperature-controlled grocery and pharmaceutical shipping. South America and the Middle East amd Africa remain nascent but display rapid policy evolution; Chile’s plastics treaty and Saudi Arabia’s circular economy roadmap both hint at impending uptake once regional supply stabilises.

Competitive Landscape

The biopolymer-coated paperboard market features a moderate concentration, with the five largest producers holding roughly 38% of 2024 volume. Smurfit WestRock leverages USD 7.656 billion quarterly sales and vertically integrated mills to negotiate long-term bio-resin contracts, lowering raw-material volatility. Graphic Packaging continues bolt-on acquisitions, adding dispersion-coated cup assets that extend its quick-service restaurant dominance. Stora Enso’s Beyond Board services couple technical training and regulatory support, differentiating through consultative selling amid tightening compliance regimes.

Technology distinguishes challengers. Eastman supplies proprietary additives that elevate barrier performance at thinner coat weights, enabling converters to meet specifications while cutting resin costs. NatureWorks forms joint innovation hubs with converters to customise PLA blends for precise food-contact or cosmetics use cases, shortening development cycles. Danimer Scientific capitalises on intellectual property in PHA synthesis to court premium brands aiming for marine-biodegradable claims. Strategic alliances also emerge; paper mills partner with bio-polymer startups to co-develop mono-material solutions, blurring traditional supplier boundaries.

Regional players show agility by targeting local policy niches. Brazilian producer Klabin expands sugar-cane-based barrier board to capture South American beverage customers attracted by sugarcane’s low-carbon profile. Chinese converters integrate in-house barrier dispersion to circumvent import duties and accelerate response times for domestic e-commerce brands. As capacity adds globally, price competition intensifies, yet differentiation through certified recyclability, composability, and traceability keeps margins defensible in premium applications. Ongoing patent filings in nano-layer coatings and enzymatic de-inking signal sustained innovation vigour across the biopolymer-coated paperboard industry.

Biopolymer-Coated Paperboard Industry Leaders

Smurfit WestRock PLC

Graphic Packaging Holding Company

Huhtamaki Oyj

Metsa Board Corporation

Sappi Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Origin Materials commenced commercial PET-cap production in Michigan, opening circular feedstock avenues for closure applications.

- February 2025: Smurfit WestRock posted USD 7.5 billion Q4 2024 net sales and USD 1.166 billion adjusted EBITDA after merger integration.

- January 2025: Amcor secured a European patent for AmFiber Performance Paper, a recyclable high-barrier solution for food and healthcare.

- December 2024: Emirates Biotech chose Sulzer technology to construct the world’s largest PLA plant in the UAE, operational by 2028.

- October 2024: Stora Enso opened the world’s largest dry-forming unit in Skene, Sweden, cutting water and energy use in packaging fibre production.

Global Biopolymer-Coated Paperboard Market Report Scope

| Polylactic Acid (PLA) |

| Polyhydroxyalkanoate (PHA) |

| Starch-based and Dextrin |

| Bio-based Wax and Oil |

| Cellulose / Nanocellulose Dispersions |

| Folding Boxboard (FBB) |

| Food-Service Board (Cupstock) |

| Solid Bleached Sulfate (SBS) Barrier Board |

| Corrugated Liner and Fluting |

| Liquid Packaging Board |

| Food and Beverage Retail Packaging |

| Food-Service Disposables |

| Personal Care and Cosmetics |

| Healthcare and Pharma |

| Industrial and Electronics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Polymer Coating Type | Polylactic Acid (PLA) | ||

| Polyhydroxyalkanoate (PHA) | |||

| Starch-based and Dextrin | |||

| Bio-based Wax and Oil | |||

| Cellulose / Nanocellulose Dispersions | |||

| By Board Grade | Folding Boxboard (FBB) | ||

| Food-Service Board (Cupstock) | |||

| Solid Bleached Sulfate (SBS) Barrier Board | |||

| Corrugated Liner and Fluting | |||

| Liquid Packaging Board | |||

| By End-use Industry | Food and Beverage Retail Packaging | ||

| Food-Service Disposables | |||

| Personal Care and Cosmetics | |||

| Healthcare and Pharma | |||

| Industrial and Electronics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Indonesia | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the biopolymer-coated paperboard market?

Stricter global bans on single-use plastics, brand ESG mandates that emphasise recyclability, and falling PLA/PHA costs are the main catalysts accelerating 11.46% CAGR through 2030.

Which polymer coating currently leads the market?

PLA coatings hold 42.56% of 2024 revenue due to mature regulatory approvals and established supply chains, although PHA is growing faster at 13.23% CAGR.

Why is Europe the largest regional market today?

Europe benefits from comprehensive packaging regulations, advanced composting infrastructure, and consumer willingness to pay premiums, culminating in 33.92% share of 2024 global revenue.

How do water-based dispersion lines influence industry economics?

Retrofits allow mills to apply bio-coatings at high speeds while cutting VOC emissions and energy use, lowering total production costs and enabling broader adoption.

What are the leading restraints on wider adoption?

Price premiums over PE-coated board, limited industrial composting infrastructure, and performance gaps for high-fat food packaging remain the primary challenges.

Page last updated on: