Grease-Resistant Bakery Paperboard Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

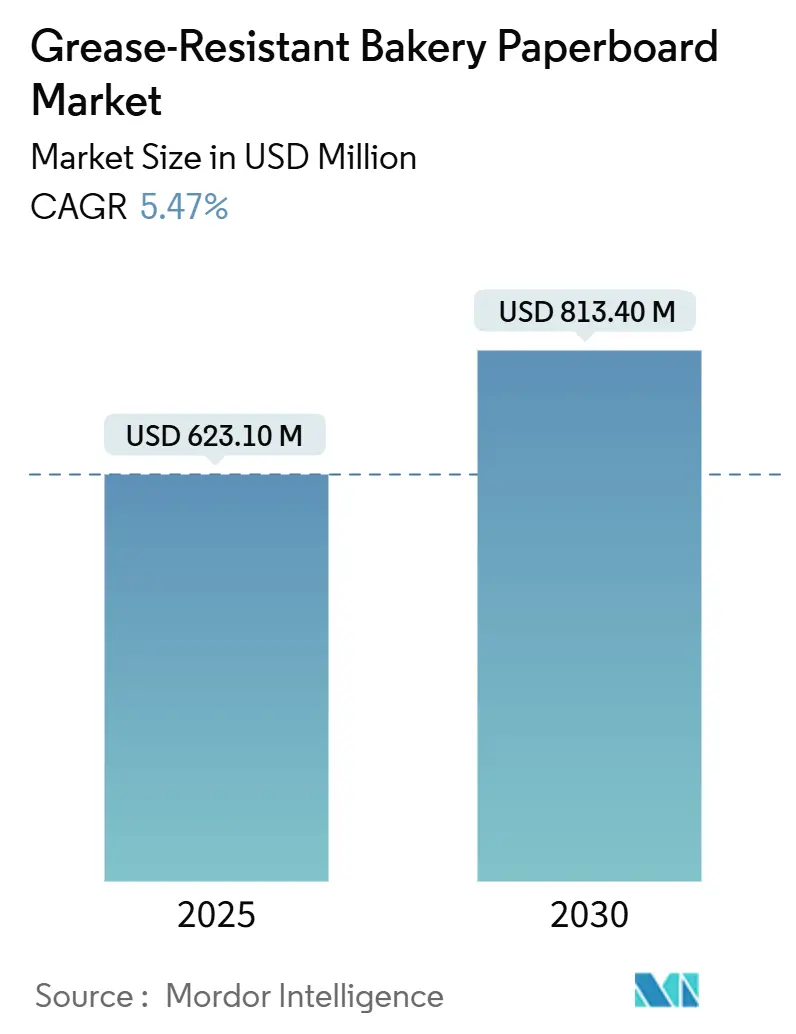

| Market Size (2025) | USD 623.10 Million |

| Market Size (2030) | USD 813.40 Million |

| Growth Rate (2025 - 2030) | 5.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grease-Resistant Bakery Paperboard Market Analysis by Mordor Intelligence

The grease-resistant bakery paperboard market size reached USD 623.1 million in 2025 and is forecast to climb to USD 813.4 million by 2030, advancing at a 5.47% CAGR. This expansion is powered by fast-tracked phase-outs of PFAS coatings, surging demand from ready-to-eat bakery formats, and sustained e-commerce growth. Regulatory clarity in the United States and the European Union has unlocked capital for PFAS-free barrier technologies, while bakery brand owners increasingly prioritize lightweight fiber-based packaging that meets recyclability targets. Investments in advanced calendering, bio-based coatings, and integrated converting lines are widening performance differentials among suppliers. North America sustains a scale advantage through mature converter networks, but Asia-Pacific is adding capacity fastest as bakery chains scale omnichannel distribution models.

Key Report Takeaways

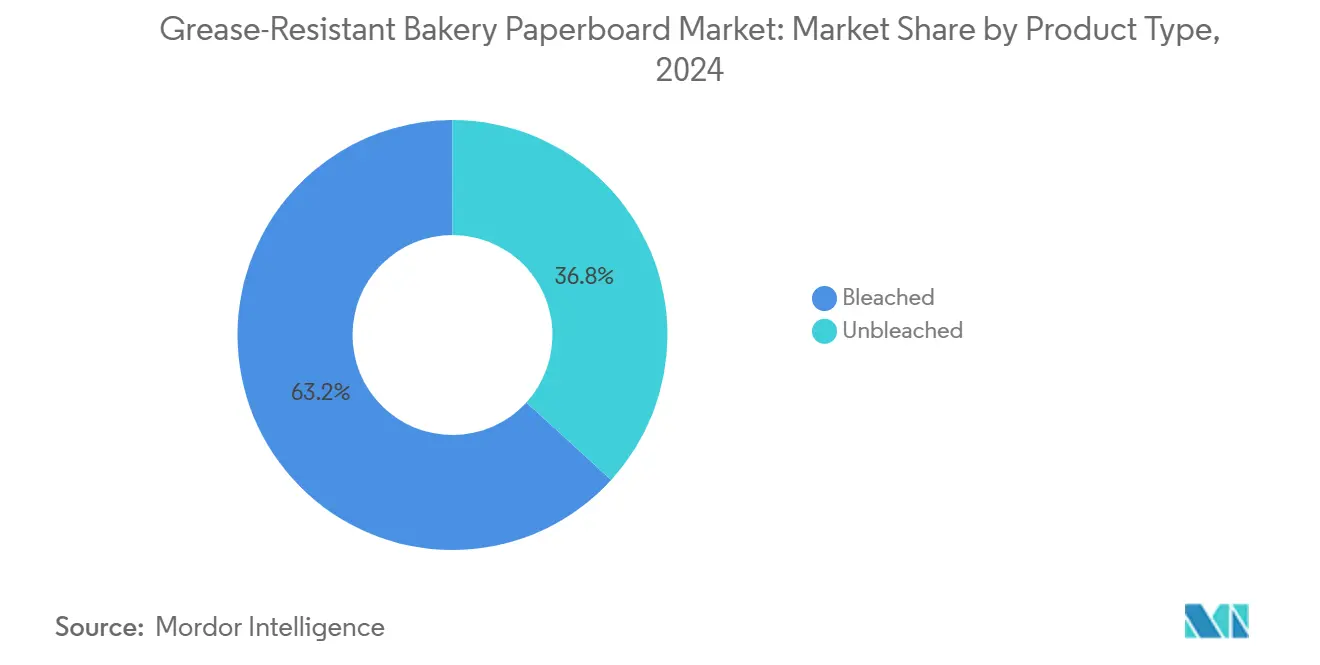

- By product type, bleached grades captured 63.23% of the grease-resistant bakery paperboard market share in 2024.

- By coating type, the grease-resistant bakery paperboard market size for bio-based/wax systems is projected to grow at a 7.13% between 2025-2030.

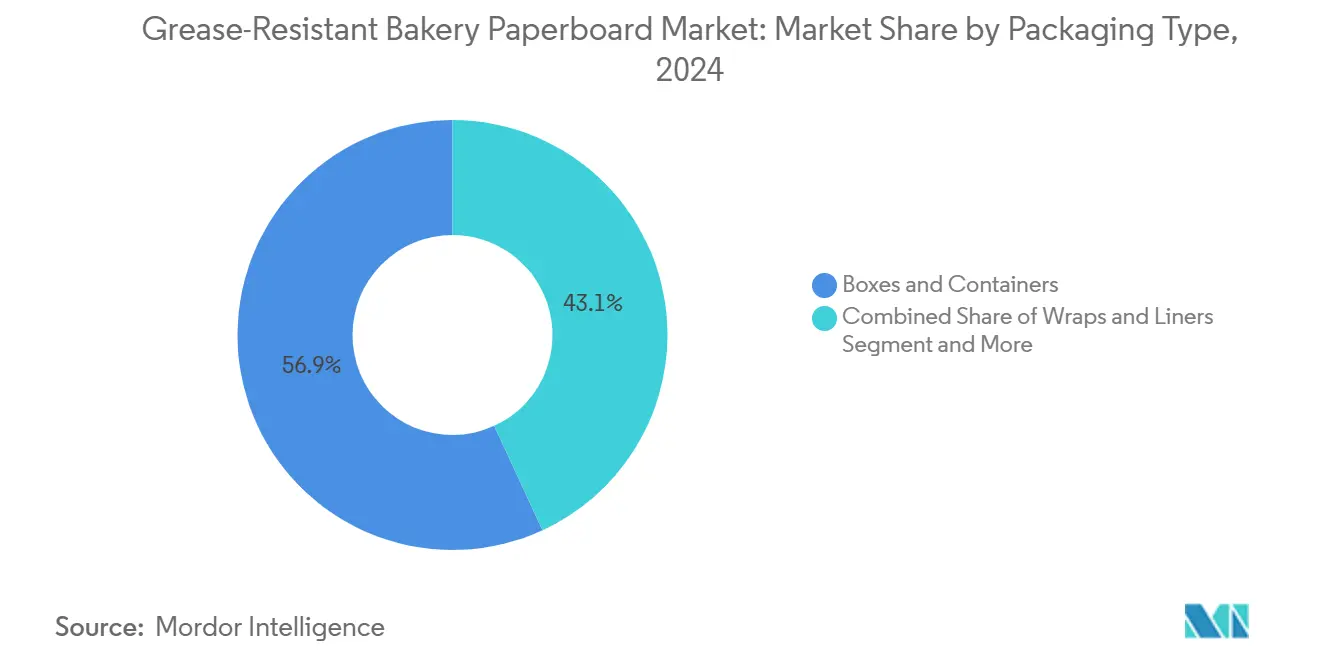

- By packaging type, boxes and containers captured 56.87% of the grease-resistant bakery paperboard market share in 2024.

- By application, the grease-resistant bakery paperboard market size for cookies and biscuits is projected to grow at a 5.83% CAGR between 2025-2030.

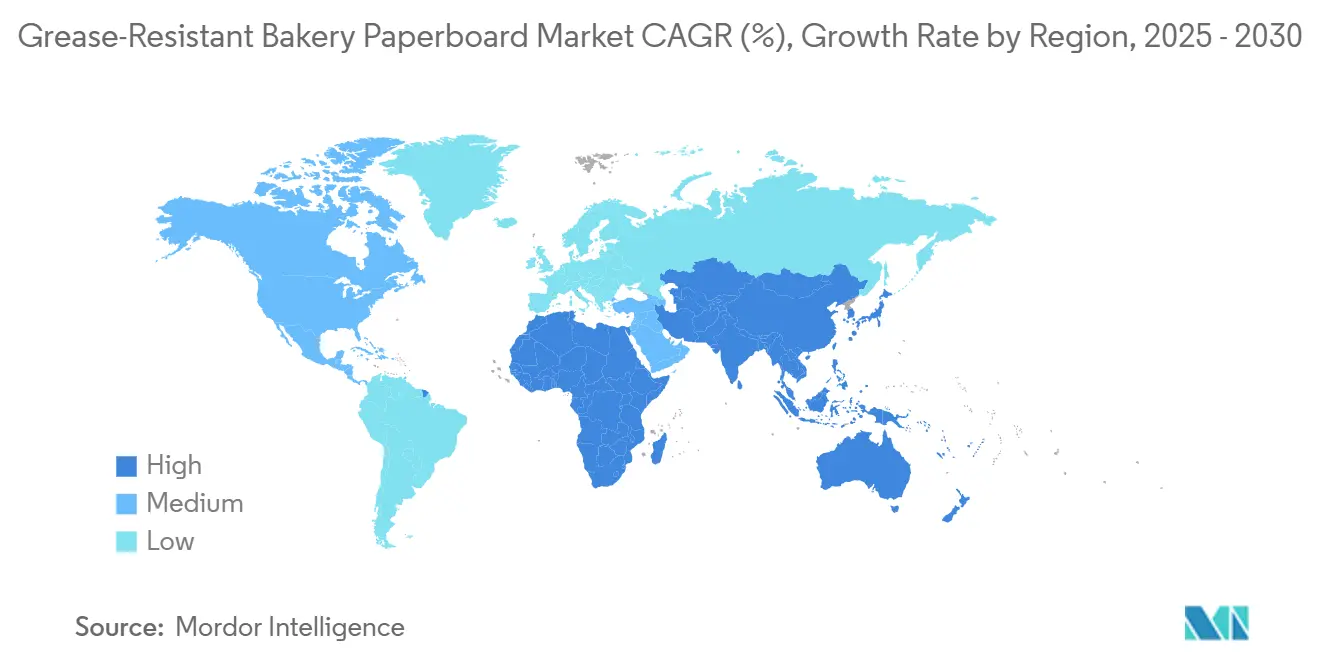

- By geography, North America captured 33.64% of the grease-resistant bakery paperboard market share in 2024.

Global Grease-Resistant Bakery Paperboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of ready-to-eat and delivery bakery formats | +1.8% | Global, early gains in North America and APAC core markets | Medium term (2-4 years) |

| Regulatory shift from plastics to fiber packaging | +1.5% | EU and North America primary, spill-over to APAC | Short term (≤ 2 years) |

| PFAS-free barrier breakthroughs unlock premium contracts | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| E-commerce-driven lightweight parcel standards | +0.9% | Global, urban centers | Short term (≤ 2 years) |

| Advanced calendering cuts board caliper and freight cost | +0.6% | Manufacturing hubs in North America, Europe, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Ready-to-Eat and Delivery Bakery Formats

Grab-and-go bakery consumption is rising sharply as urban dwellers seek convenience, spurring sustained demand for grease barriers that guard visual appeal during last-mile delivery. Quick-service restaurant sales in India are growing at a 13% CAGR, mirroring worldwide momentum for portion-controlled pastries that must endure temperature swings in transit. Improved coatings that resist oil wicking and moisture vapor now allow extended ambient shelf life without secondary plastic wraps. Retail bakery chains are thus switching large-volume SKUs to fiber-based trays with integrated lids to cut plastic tonnage. Converter order books show multi-year supply contracts tied to these format shifts, signaling durable volume pull for the grease-resistant bakery paperboard market.

Regulatory Shift from Plastics to Fiber Packaging

Mandatory recyclability targets under the EU Packaging and Packaging Waste Regulation have accelerated the pivot from multilayer plastic to mono-material fiber constructions. The rule caps allowable PFAS concentrations, pushing converters toward PFAS-free chemistries to keep market access. US brands face parallel deadlines as the FDA invalidated 35 PFAS food-contact notifications effective June 2025, sparking near-term reformulation races.[1]Phys.org, “PFAS could be replaced with safe graphene oxide solution,” phys.orgTier-one bakery producers now embed recyclability scorecards in bid tenders, rewarding suppliers that certify fiber sourcing and barrier compliance. Early movers into bio-based coatings are thus winning price premiums and longer tenures, reinforcing growth for the grease-resistant bakery paperboard market.

PFAS-Free Barrier Breakthroughs Unlock Premium Contracts

Laboratory advances such as Northwestern University’s graphene-oxide coating deliver 30–50% higher oil holdout versus legacy fluorochemicals, closing historical performance gaps for high-fat pastries. Commercial rollout through GO-Eco promises FDA clearance in 2026, and leading converters are already piloting the chemistry on twin-wire board machines in the United States and Finland. Retailers tightly manage brand risk linked to PFAS headlines, so qualified PFAS-free suppliers receive preferred-vendor status and multi-SKU exclusivity. Those awards translate to margin uplift and reinforce the competitive moat for technology leaders in the grease-resistant bakery paperboard market.

E-Commerce-Driven Lightweight Parcel Standards

Online cake and pastry orders must travel farther while staying intact, prompting parcel hubs to set dimensional weight caps. Board caliper reductions of 10–12% achieved via multi-stack calendering hold stiffness while lowering mass, trimming postal fees, and carbon disclosures. Dutch bakery Taartenwinkel adopted a recyclable fiber-based shipper with integrated cold packs, cutting its damage rate to 0.6% and its parcel weight by 180 g per unit. Such gains elevate the adoption of lightweight, grease-resistant bakery paperboard market solutions across digitally native bakeries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating PFAS bans inflate reformulation costs | -1.1% | Global, immediate in EU and North America | Short term (≤ 2 years) |

| Volatility in virgin-fiber pulp pricing | -0.8% | Global, cost-focused segments | Medium term (2-4 years) |

| Ink–oil interaction risks in high-fat pastries | -0.5% | Global, premium bakery applications | Medium term (2-4 years) |

| Converter learning curve for bio-coatings | -0.4% | Manufacturing regions shifting to new tech | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating PFAS Bans Inflate Reformulation Costs

Suppliers must redevelop entire grease barrier portfolios on compressed lead times after the US and EU bans invalidate legacy fluorochemicals. Reformulation budgets now include pilot-line trials, analytical validation, and downstream customer requalification tests, lifting cost-per-ton of coated board in 2025 by 7–9% compared with 2023 levels. Smaller converters face liquidity strain and may exit premium bakery segments, potentially consolidating demand within top-tier players in the grease-resistant bakery paperboard market.

Volatility in Virgin-Fiber Pulp Pricing

Futures contracts for Northern Bleached Softwood Kraft pulp swung 18% inside 2024, complicating fixed-price quoting cycles. Energy-intensive pulp mills in Canada and Scandinavia pass through higher electricity tariffs, raising delivered fiber costs for board makers. Converters attempt to hedge with recycled fiber blends, yet stringent odor and migration limits for bakery applications cap substitution rates. Such cost turbulence temporarily compresses margins across the grease-resistant bakery paperboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unbleached Grades Capture Sustainability Momentum

Bleached board continues to command the largest slice of the grease-resistant bakery paperboard market, holding a 63.23% share in 2024, thanks to bright surfaces that elevate brand graphics. Its dominance is evident across premium cake cartons where shelf appeal drives unit economics. However, unbleached variants are logging a 6.84% CAGR, outpacing market average as bakery chains adopt natural-brown aesthetics to signal eco-credentials. The grease-resistant bakery paperboard market size for unbleached grades is projected to widen even further as coating advances temper historical performance gaps. Vertical integration between Nordic pulp suppliers and European converters has ensured a steady fiber supply, reinforcing cost advantages for unbleached offerings. North American quick-service restaurants are piloting Kraft-Tone burger bun sleeves, validating this growth trajectory. Sustained capex in online color management systems will allow unbleached substrates to win placements once reserved for bleached rivals.

Second-tier applications, such as in-store bakery liners, also lean toward unbleached stock because visual requirements are modest. Asian bakeries increasingly position Kraft cartons as premium minimalism, supporting higher price points while shrinking total coating load. Exports of kraft-tone cupcake carriers from China climbed 14% in 2024, showing that mills can achieve acceptable brightness without chlorine bleaching. Given the regulatory tailwind, the grease-resistant bakery paperboard market is likely to witness convergence of performance standards between bleached and unbleached over the forecast window.

By Coating Type: Bio-Based Alternatives Accelerate Commercial Adoption

PFAS-free synthetic systems, principally PVOH, acrylic, and silicone, controlled a 37.92% share of the grease-resistant bakery paperboard market in 2024, furnishing drop-in performance at existing blade coaters. These chemistries carry robust regulatory dossiers and have been scaled on four-meter machines across Europe and North America. Yet bio-based or wax coatings are clocking a 7.13% CAGR, the fastest within coating segments, as retailers ratchet up plastics elimination targets. Early wax iterations struggled with heat sealability, but new hybrid recipes incorporating starch and shellac display oil kit values above 11 and acceptable heat-seal windows. The grease-resistant bakery paperboard market size for bio-coated board remains modest yet expanding, spurred by bakery chains offering compostable takeaway packaging. Synthetic suppliers respond by bundling water-resistance boosters, blurring performance distinctions, and granting end users broader menu compatibility.

Regulatory spotlights on chemical recycling favor bio-systems that require no special post-consumer handling, attracting venture funding into pilot lines in Sweden and Canada. Technology alliances between board mills and bio-resin companies have shortened qualification cycles, suggesting that bio-coatings could close the share gap faster than earlier projections. Converter uptime still hinges on mastering viscosity drift and dryer loads, but those hurdles are shrinking with each commercial run.

By Packaging Type: Boxes and Containers Retain Dual Leadership

Boxes and rigid containers accounted for 56.87% of 2024 revenue and are set to grow at 6.41% annually, illustrating their alignment with mechanized filling lines and e-commerce dimension standards. Many delivery platforms specify right-angle edges for robotic picking, favoring corrugated style board that blends grease barrier with crush strength. The grease-resistant bakery paperboard market size attributed to boxes is therefore scaling with every incremental meal-delivery transaction. Liners and wraps maintain relevance for in-store bakery counters, but they are losing share as retailers opt for lidded clamshells that curb cross-contamination. Bags and pouches fill niche roles for bread rolls or long baguettes, yet their thinner walls complicate barrier application and reduce graphics real estate.

Automation upgrades across Asian converter plants are tilting investments toward die-cut boxes that run at 300 units per minute, versus manual fold wraps at 90 units. Freight optimizations further reward rectangular formats, cementing box dominance. Performance demands for deep-freeze cheesecakes have also steered toward lined rigid trays compatible with secondary corrugate shippers, reinforcing the segment’s growth.

By Application: Cakes and Pastries Remain the Value Anchor

Cakes and pastries drew 32.27% of 2024 demand, benefiting from high-fat contents that require premium grease barriers to avoid panel staining. Graphics-heavy cake boxes amplify brand equity and justify upscale substrates, ensuring stable volume pull for bleached boards. Cookie and biscuit SKUs are scaling quickly at a 5.83% CAGR amid portion control trends, moderate fat content, and higher snack frequency across emerging economies. The grease-resistant bakery paperboard market share linked to cookies is thus widening faster than historical averages. Meanwhile, bread and rolls stick to commodity performance thresholds, dampening differentiated board demand. Specialty ethnic bakery products, though small in tonnage, spur custom dimensions and multi-layer barriers, adding complexity but limited scale effect.

Mill R&D pipelines increasingly target the oil-migration profiles of laminated puff pastries, hinting that successful proof-of-concepts could elevate overall adoption within this application cluster. Retail in-store bakeries remain a parallel engine, upgrading package aesthetics to mimic premium patisserie standards, thereby sustaining demand for higher-caliper grease-resistant bakery paperboard market solutions.

Geography Analysis

North America held 33.64% of 2024 revenue, underpinned by integrated pulp supply and early PFAS compliance strategies. Regional mills enjoy a stable offtake contracts from national bakery chains, and recent asset purchases, including Suzano’s acquisition of two US board mills adding 420,000 tons, signal long-term commitment. Demand is reinforced by consolidated grocery networks that roll out uniform packaging specs across thousands of stores, reducing onboarding friction for novel barrier films.

Europe follows with steady growth as policymakers enforce circularity mandates that privilege fiber substrates. High consumer awareness of sustainability accelerates the adoption of unbleached kraft cartons, particularly in the Nordic and DACH regions. Stora Enso’s EUR 1 billion upgrading of its Oulu line will supply up to 750,000 tons of premium barrier board by 2027. These investments indicate that Europe will remain a technology test bed for bio-coatings and closed-loop recovery schemes, steering global adoption curves for the grease-resistant bakery paperboard market.

Asia-Pacific is the fastest-expanding region at 7.51% CAGR, propelled by soaring discretionary income, westernized diets, and double-digit e-commerce penetration. China’s bakery retail sales are on track to reach USD 53 billion in 2025, underpinning large-volume requirement for branded cake cartons.[2]U.S. Department of Agriculture, “China’s Rising Bakery Sector,” fas.usda.gov India’s Food Safety and Standards regulations, last updated in 2024, embed fiber safety specifications that facilitate adoption. Japanese premium convenience stores continue to demand ultra-bright board with flawless print, offering margin-rich niches for high-performance suppliers. Supply is periodically constrained when typhoons or energy shocks hit local pulp mills, but diversified import channels cushion disruptions.

Long-term, regional consumption profiles are converging around digital ordering and sustainable messaging, indicating that performance benchmarks set in North America and Europe will quickly migrate to Asia-Pacific. Consequently, mills in Indonesia and Vietnam are evaluating twin-blade coaters to capture emerging demand, cementing the region’s status as volume growth engine for the grease-resistant bakery paperboard market.

Competitive Landscape

The grease-resistant bakery paperboard market displays moderate concentration. The top five global players command roughly 55–60% of coated board output, creating room for mid-size regional converters that specialize in quick-turn orders. Competitive focus has shifted from pure scale to technology differentiation, especially around PFAS-free barriers. Smurfit WestRock’s creation through the Smurfit Kappa-WestRock merger established a USD 34 billion packaging titan that combines kraftliner depth with proprietary acrylic barriers, challenging incumbents on three continents.[3]WestRock, “Smurfit Kappa and WestRock Announce Transaction,” westrock.com

Strategic acquisitions continue: International Paper’s USD 7.2 billion bid for DS Smith extends its grease-resistant portfolio into Europe, enhancing access to brand-owner specification hubs. Private-equity-backed entrants are investing in niche bio-coating plants able to run shorter job lengths, appealing to artisan bakeries seeking customized graphics. Capital intensity remains high, and barriers to entry are rising as end-users impose multi-year greener-chemistry commitments.

Innovation pipelines show intensive collaboration with chemical suppliers. Converters run joint audits with retailers to certify end-of-life recovery, thereby embedding themselves deeper into customer value chains. Pricing remains rational due to long contract cycles; however, spot markets can swing when pulp volatility spikes. Overall, the grease-resistant bakery paperboard market gravitates toward technology-driven differentiation more than commodity price wars.

Grease-Resistant Bakery Paperboard Industry Leaders

Smurfit WestRock PLC

International Paper Company

Stora Enso Oyj

Mondi PLC

Graphic Packaging Holding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Northwestern University and GO-Eco unveiled a graphene-oxide paperboard coating offering 30–50% higher grease resistance.

- April 2025: Stora Enso reported Q1 2025 revenue of EUR 2,362 million and confirmed ramp-up of its EUR 1 billion Oulu barrier board line.

- January 2025: The FDA ruled 35 PFAS food-contact notifications ineffective, finalizing the PFAS phase-out in US food packaging by Jun 30, 2025.

- January 2025: The European Council adopted Regulation 2025/40, setting PFAS limits of 25 ppb for individual PFAS and 250 ppb for totals, effective Aug 2026.

Global Grease-Resistant Bakery Paperboard Market Report Scope

| Bleached |

| Unbleached |

| PFAS Fluorochemical |

| PFAS-Free Synthetic (PVOH/Acrylic/Silicone) |

| Bio-based/Wax |

| Hybrid Multi-layer |

| Boxes and Containers |

| Wraps and Liners |

| Bags and Pouches |

| Bread and Rolls |

| Cakes and Pastries |

| Cookies and Biscuits |

| Other Bakery Products |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Bleached | ||

| Unbleached | |||

| By Coating Type | PFAS Fluorochemical | ||

| PFAS-Free Synthetic (PVOH/Acrylic/Silicone) | |||

| Bio-based/Wax | |||

| Hybrid Multi-layer | |||

| By Packaging Type | Boxes and Containers | ||

| Wraps and Liners | |||

| Bags and Pouches | |||

| By Application | Bread and Rolls | ||

| Cakes and Pastries | |||

| Cookies and Biscuits | |||

| Other Bakery Products | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the grease-resistant bakery paperboard market in 2025?

It stands at USD 623.1 million and is projected to reach USD 813.4 million by 2030 at a 5.47% CAGR.

What segment leads in product type?

Bleached board retains 63.23% share, though unbleached is expanding faster at 6.84% CAGR.

Which coating technology is growing fastest?

Bio-based or wax coatings are set to grow at 7.13% CAGR as brands phase out PFAS.

Which region is expanding most rapidly?

Asia-Pacific is forecast for a 7.51% CAGR driven by rising bakery consumption in China and India.

How are suppliers responding to PFAS bans?

Leading mills are investing in PFAS-free synthetics and bio-based barriers, upgrading calendering, and pursuing joint R&D with chemical firms.

What is the market outlook for e-commerce bakery packaging?

Boxes and containers fitted to parcel standards are projected to grow at 6.41% CAGR, leveraging lightweight board and robust grease barriers.

Page last updated on: