Algae Based Coated Paperboard Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

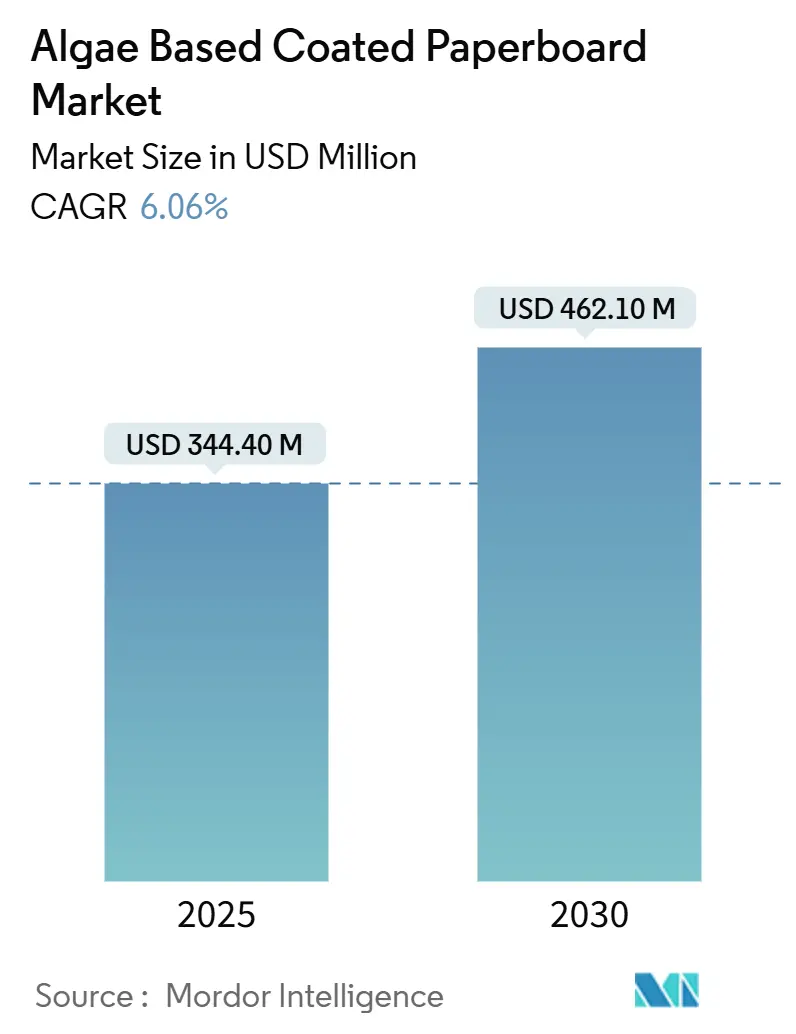

| Market Size (2025) | USD 344.40 Million |

| Market Size (2030) | USD 462.10 Million |

| Growth Rate (2025 - 2030) | 6.06% CAGR |

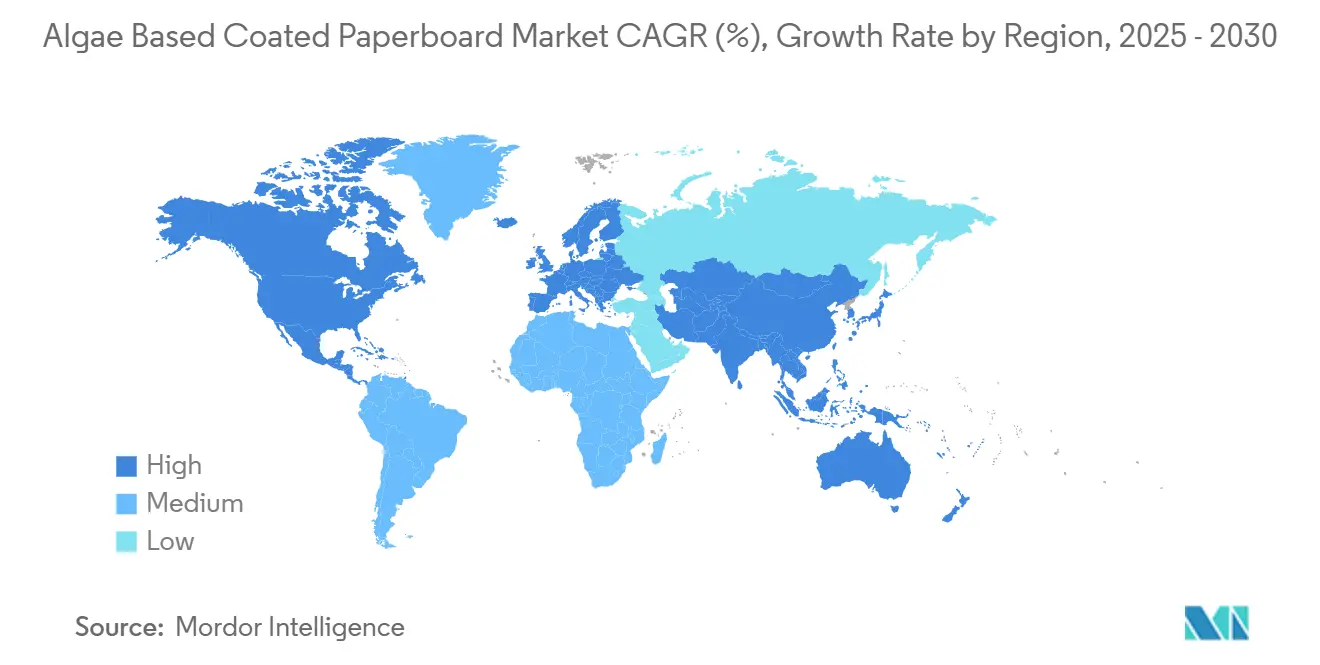

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algae Based Coated Paperboard Market Analysis by Mordor Intelligence

The Algae-Based Coated Paperboard market size is valued at USD 344.1 million in 2025 and is set to reach USD 462.1 million by 2030, advancing at a 6.06% CAGR over the forecast period. Robust growth rests on simultaneous regulatory bans on PFAS, falling seaweed-cultivation costs, and new printing chemistries that let converters switch substrates without capital disruption. Multinational brand owners have widened zero-waste purchasing mandates, converting compliance pressure into an immediate procurement pull for algae-derived barriers. Europe anchors early adoption under the Single-Use Plastics Directive, yet production‐scale advantages in Asia-Pacific are pushing global capacity south-eastward. Competitive intensity remains high because start-ups offer proprietary formulations while incumbents chase vertical integration to secure feedstock and margin insulation.

Key Report Takeaways

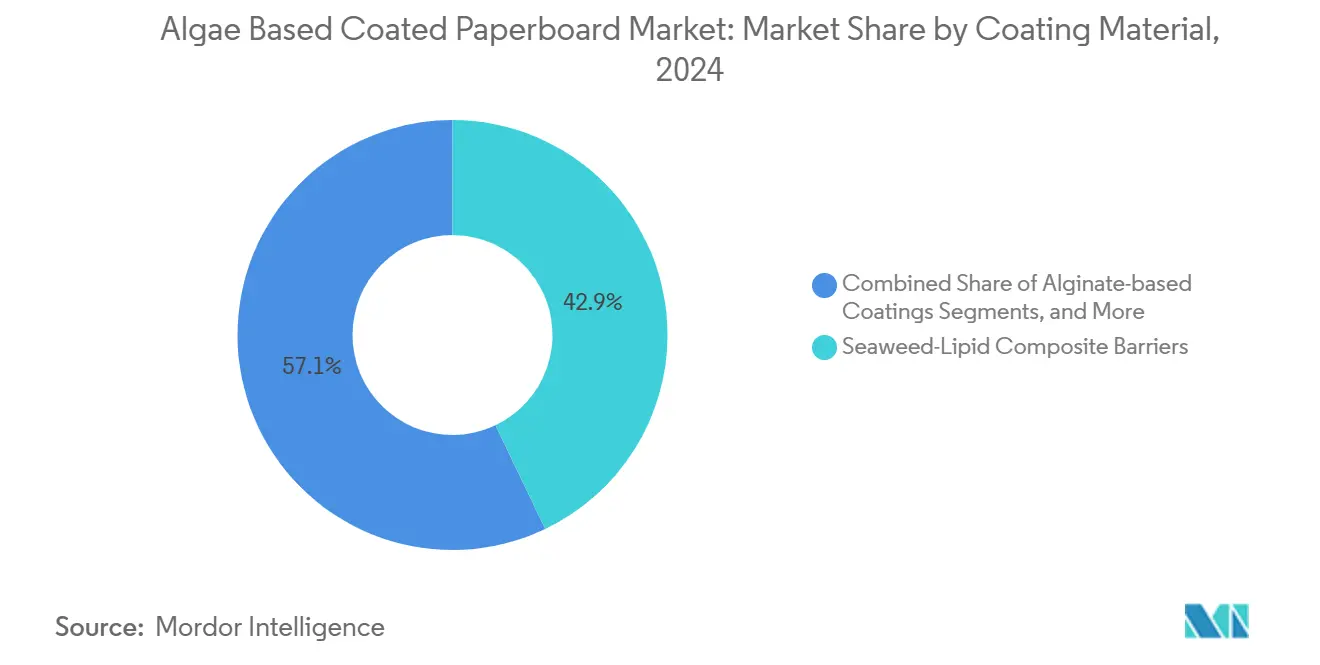

- By coating material, Seaweed-Lipid Composite Barriers led with 42.91% of Algae-Based Coated Paperboard market share in 2024.

- By end-use industry, the Algae-Based Coated Paperboard market size for Personal Care and Cosmetics segment is projected to grow at a 6.81% CAGR between 2025-2030.

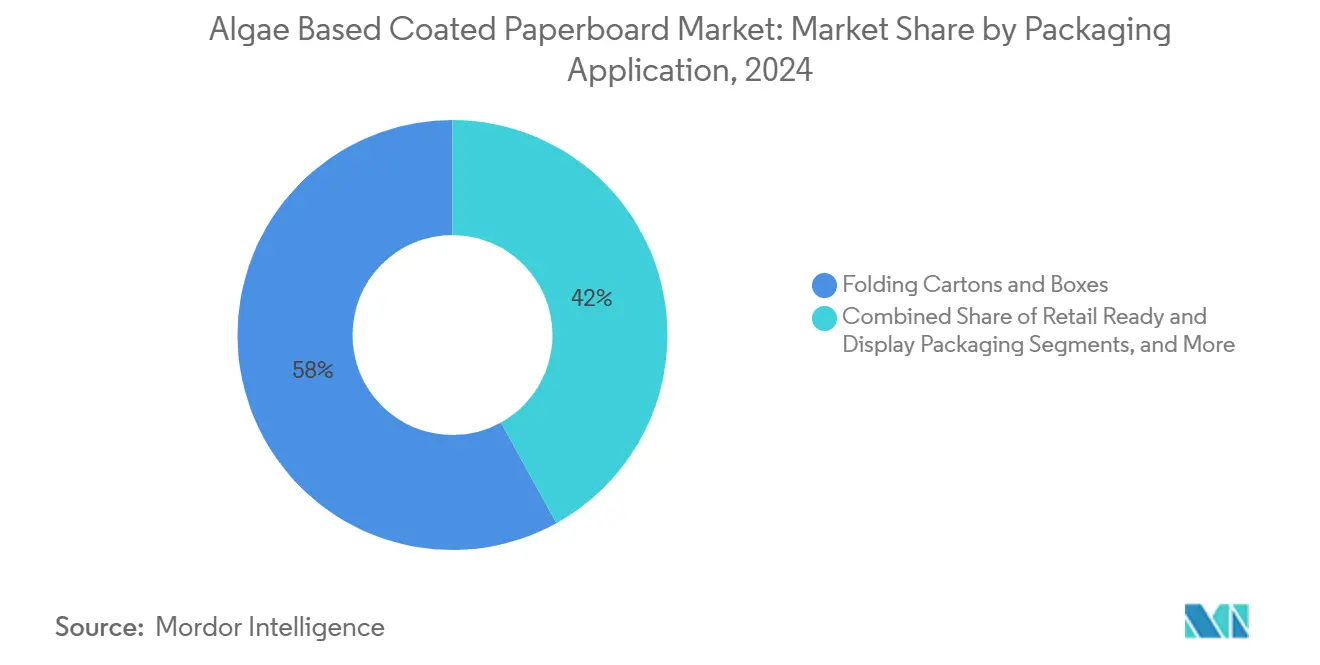

- By packaging application, Folding Cartons and Boxes commanded 58.04% of the Algae-Based Coated Paperboard market share in 2024.

- By geography, the Algae-Based Coated Paperboard market size in for the Asia-Pacific region is projected to grow at a 7.63% CAGR between 2025-2030.

Global Algae Based Coated Paperboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging bans on PFAS and plastic-lined food-service board | + 1.5% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Corporate zero-waste targets accelerating algae-barrier adoption | +1.2% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Cost downs from large-scale seaweed aquaculture | + 0.8% | APAC core, spill-over to global supply chains | Medium term (2-4 years) |

| Emergence of algae-compatible flexo and digital inks | + 0.6% | North America and EU printing hubs | Short term (≤ 2 years) |

| AI-guided formulation improving grease/moisture resistance | + 0.4% | Global R&D centers, early adoption in premium segments | Long term (≥ 4 years) |

| Integration of algae barriers with digital traceability tags | +0.3% | EU and North America, regulatory compliance focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Bans on PFAS and Plastic-Lined Food-Service Board

Regulatory prohibitions hit inflection in 2024 when the FDA barred new PFAS-containing grease-proofing agents and set a phase-out deadline of June 2025, instantly unlocking a USD 118 million replacement pool for the Algae-Based Coated Paperboard market.[2]U.S. Food and Drug Administration, “FDA, Industry Actions End Sales of PFAS Used in US Food Packaging,” fda.gov Washington State’s earlier restriction offered a template now mirrored by California’s AB 347, which caps PFAS at 100 ppm and obliges manufacturer registration. In Europe, paper articles with plastic linings fall under the Single-Use Plastics Directive, making algae-coated substrates the quickest compliant route. [1]Publications Office of the European Union, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” eur-lex.europa.eu This cascade reduces price parity gaps because converters must reformulate regardless, so algae-based alternatives become a default rather than a premium option. Governments worldwide are expected to copy the model, magnifying demand over the forecast horizon.

Corporate Zero-Waste Targets Accelerating Algae-Barrier Adoption

Brand-owner policies now stipulate bio-based substrates as a share of total packaging spend, creating procurement pull-through before mandatory regulations arrive. Stellantis is targeting carbon net-zero by 2038 and is capturing scope-3 emission savings by substituting bio-barriers in component packs. Bayer likewise plans for more than 50% bio-derived sales by 2030, prompting its pharmaceutical vendors to migrate to algae coatings. Such commitments ripple down to tier-1 suppliers that standardize algae specifications across regional plants, multiplying demand even where legislation is less advanced. Because these pledges are public, material changes become a reputational KPI, reinforcing premium pricing resilience.

Cost Downs from Large-Scale Seaweed Aquaculture (2025+)

European and Asian growers are scaling integrated multi-trophic systems co-located with offshore wind parks, a roadmap targeting 8 million tons of seaweed by 2030 that will compress feedstock input costs for the Algae-Based Coated Paperboard market. China’s Jiangsu Province alone harvested 35,936 metric tons of laver in 2023, demonstrating achievable economies of density. US federal research grants have further lowered cultivation capex, anticipating raw material cost parity with synthetic polymers by 2027. Falling feedstock costs enable price-elastic segments such as disposable trays to switch substrates without margin erosion, accelerating volume adoption.

Emergence of Algae-Compatible Flexo and Digital Inks

Until 2024, ink adhesion on hydrophilic alginate surfaces was a principal barrier for high-graphics packaging. Novel waterborne ink systems now use tailored surfactants to anchor pigments without compromising grease performance, allowing converters to keep legacy flexo presses while switching liners. Digital printing variants deliver variable data and embellishments, critical for premium cosmetic cartons. Because print quality is brand-equity sensitive, ink compatibility removes the final technical hurdle inhibiting widespread retail adoption, enlarging the Algae-Based Coated Paperboard market footprint in high-value applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sensitivity of alginate films to relative humidity | -0.7% | Global, particularly humid tropical regions | Short term (≤ 2 years) |

| Seaweed feedstock supply volatility | -0.5% | APAC production regions, global supply chains | Medium term (2-4 years) |

| Limited industrial composting infrastructure | -0.4% | North America and developing markets | Long term (≥ 4 years) |

| Uncertain regulatory harmonisation across export markets | -0.3% | Global trade corridors, export-dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Sensitivity of Alginate Films to Relative Humidity

Above 75% relative humidity, water-vapor transmission through alginate films rises sharply, degrading grease resistance and leading to fiber delamination in refrigerated or tropical environments. Linseed-oil submicron coatings improve hydrophobicity but incur added cost and may slow biodegradation. Converters working in Southeast Asia therefore need controlled-environment storage and rapid-turn logistics, curbing margin gains from algae switches in those climates. The technological gap remains a short-term brake until lipid-alginate composites mature for high-humidity performance.

Seaweed Feedstock Supply Volatility

Extreme weather and warming seas threaten yields in Indonesia, China, and the Philippines, all core cultivation hubs for the Algae-Based Coated Paperboard market. Crop disease flare-ups and export-licence backlogs create price spikes, forcing converters to hold larger inventories that raise working capital. Diversified contracts and near-shore farming pilots in Europe and North America mitigate the risk but elevate landed cost relative to petroleum-based inputs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Material: Lipid Composites Cement Leadership

Seaweed-Lipid Composite Barriers accounted for 42.91% of Algae-Based Coated Paperboard market share in 2024, reflecting their ability to deliver Kit 12 grease scores and water-vapor transmission reductions of up to 44% compared with untreated board. The Algae-Based Coated Paperboard market size for lipid composites is projected to rise in tandem with quick-service packaging volumes as restaurants replace PFAS-lined wraps. Alginate-based Coatings exhibit the highest 7.04% CAGR because they cost 18-20% less per square meter and run on existing curtain coaters with minimal re-tooling.

Ulvan-based and chitosan-enhanced hybrids occupy premium niches where antimicrobial function or mechanical strength override price sensitivity. Researchers have shown that chitosan integration lifts tensile strength by 23%, attracting electronics packagers seeking drop-test compliance. Other experimental blends combining brown and red algae polysaccharides with synthetic bio-esters remain below commercial scale but draw venture investment for high-barrier cosmetic lids. The spectrum of formulations underpins future product-tiering strategies that broaden the Algae-Based Coated Paperboard market beyond food contact into technical packaging.

By End-Use Industry: Food-Service Volume Meets Beauty Margins

Food-Service retained 49.64% share in 2024, anchoring the Algae-Based Coated Paperboard market with predictable menu-item SKUs and uniform pack formats. Regulatory compulsion has accelerated blanket conversions among national QSR chains. The segment is price-elastic, so cost declines in aquaculture drive immediate volume gains. Personal Care and Cosmetics, while smaller, is the fastest climber at 6.81% CAGR. Prestige brands position algae linings as part of clean-beauty narratives to justify 8-12% pack cost premiums.

E-commerce retailers are experimenting with algae-lined mailers that avoid plastic void-fill and improve curbside recyclability scores. Electronics firms leverage algae films’ anti-static properties in protective inserts, linking product safety with eco-friendly branding. Pharmaceutical secondary packs constitute a nascent but strategic niche; alginate’s oxygen barrier slows photo-degradation of light-sensitive drugs, an angle under pilot with two EU-based contract packers. Combined, these dynamics anticipate a more balanced end-use mix by 2030.

By Packaging Application: Beyond the Folding Carton Stronghold

Folding Cartons and Boxes contributed 58.04% of Algae-Based Coated Paperboard market size in 2024, helped by entrenched converting lines that simply swapped coating baths to meet PFAS bans. Protective Inserts and Blister Cards, though only 8.2% of volume, are scaling fastest at 6.57% CAGR as electronics and pharma producers prioritize anti-static and tamper-evident traits. Trays and Clamshells in ready-meal delivery leverage algae coatings for grease and freezer burn resistance, while Cups and Lids benefit from compostability claims that coffee chains advertise on-pack.

Across applications, digital watermark integration drives SKU-level traceability, aligning with EU waste regulations that demand recyclability data disclosure. Retail-ready display packs exploit algae substrates for high-impact graphics and matte aesthetics, echoing luxury sensibilities. The widening spread of technical and aesthetic advantages forecasts rising share for specialty formats beyond traditional cartons over the projection window.

Geography Analysis

Europe commanded 36.51% of 2024 volume, underpinned by the Packaging and Packaging Waste Regulation that obliges recyclability by 2030. Germany and France exhibit the densest converter clusters, benefiting from established collection and composting channels. Italy and Spain integrate Mediterranean seaweed cultivars into regional supply chains, trimming imports and enhancing narrative authenticity of local sourcing.

Asia-Pacific is expanding at a 7.63% CAGR, propelled by China’s concentration of raw material and by government grants that deem algae a strategic replacement for fossil-based plastics. Japan’s precision-fermentation know-how upgrades feedstock purity for cosmetics, while India’s QSR boom feeds carton demand. Indonesia’s cultivation exposure to climate swings encourages diversified farm-site investment, yet cost advantages remain compelling for export.

North America sits between regulation and resource. The FDA phase-out galvanizes demand, but varying state thresholds complicate national rollouts. Canada aligns with US safety standards, smoothing cross-border flows. Mexico’s food-delivery start-ups prefer algae-lined clamshells to satisfy affluent urban consumer expectations. South America and the Middle East and Africa trail in absolute size but are piloting community seaweed farms that may cut import reliance and spark regional growth by late decade.

Competitive Landscape

Competition is fragmented; the top five players hold well below 20% cumulative revenue, giving start-ups room to carve niches. NOTPLA has integrated brown-algae feedstock through UK-based sea farms, pairing coatings with edible sachet spin-offs that cross-pollinate R&D. Sway’s USD 1.5 million Department of Energy grant funds processing of alginate sidestreams from protein extraction, lowering cost bases and bolstering circular-economy credentials . Evoware targets ASEAN markets with single-service sachets pivoting into coated board, exploiting proximity to Indonesian feedstock.

Legacy converters like Nippon Paper are trialing hybrid lines that apply algae dispersions on existing curtain coaters, seeking portfolio greening while using sunk capital. [3]日本製紙株式会社, “Management Briefing,” nipponpapergroup.com Multinationals consider acquisition as a shortcut; at least three due-diligence exercises were reported in 2025 among EU and US majors scouting alginate-coating patents. AI-driven formulation libraries and digital traceability modules are the competitive levers because they embed data services into commodity substrates, delaying price erosion.

White-space exists in medical and security packaging where biodegradability plus tamper-proof coding attract regulatory favor. Protective inserts for batteries and chips illustrate early wins, pairing anti-static performance with compostability. As formulations commoditize, brand equity will shift from barrier performance to sourcing transparency and lifecycle credentials, pressuring late entrants to either vertically integrate or license traceability tech from early movers.

Algae Based Coated Paperboard Industry Leaders

NOTPLA Limited

Kelpi Limited

Sway Innovation Co.

Sappi Limited

Billerud AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Sway and Umaro secured a USD 1.5 million US Department of Energy grant to valorize alginate sidestreams into bioplastic resins.

- September 2024: California’s AB 347 entered force, mandating PFAS thresholds below 100 ppm and manufacturer registration.

- June 2024: Evonik pledged that bio-based products, including algae-derived omega-3s, will exceed 50% of its sales mix by 2030.

- February 2024: The FDA confirmed the complete US phase-out of PFAS grease-proofing agents, opening a USD 118 million compliance market for algae-based coatings.

Global Algae Based Coated Paperboard Market Report Scope

| Alginate-based Coatings |

| Ulvan-based Coatings |

| Chitosan-enhanced Algae Coatings |

| Seaweed-Lipid Composite Barriers |

| Other Coating Material |

| Food-Service (QSR and Catering) |

| Food and Beverage |

| Personal Care and Cosmetics |

| Retail and E-commerce |

| Electronics and Consumer Goods |

| Industrial and Other End-use Industries |

| Folding Cartons and Boxes |

| Trays and Clamshells |

| Cups, Lids, and Cutlery |

| Retail Ready and Display Packaging |

| Protective Inserts and Blister Cards |

| Other Packaging Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Coating Material | Alginate-based Coatings | ||

| Ulvan-based Coatings | |||

| Chitosan-enhanced Algae Coatings | |||

| Seaweed-Lipid Composite Barriers | |||

| Other Coating Material | |||

| By End-Use Industry | Food-Service (QSR and Catering) | ||

| Food and Beverage | |||

| Personal Care and Cosmetics | |||

| Retail and E-commerce | |||

| Electronics and Consumer Goods | |||

| Industrial and Other End-use Industries | |||

| By Packaging Application | Folding Cartons and Boxes | ||

| Trays and Clamshells | |||

| Cups, Lids, and Cutlery | |||

| Retail Ready and Display Packaging | |||

| Protective Inserts and Blister Cards | |||

| Other Packaging Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is revenue expected to grow for algae-coated paperboard between 2025 and 2030?

Revenue is projected to rise from USD 344.1 million in 2025 to USD 462.1 million by 2030 at a 6.06% CAGR.

Which packaging application is gaining share the quickest?

Protective Inserts and Blister Cards top the growth table with a 6.57% CAGR through 2030, driven by electronics and pharmaceutical demand.

Why are Seaweed-Lipid Composite Barriers the leading material choice?

They deliver superior grease and moisture resistance, translating into 42.91% market share in 2024 while supporting regulatory PFAS exits.

What is driving Asia-Pacific to outpace Europe in growth?

Abundant low-cost seaweed cultivation and government sponsorship of bio-based materials push the region to a 7.63% CAGR.

Which regulatory change had the largest immediate market impact?

The FDA’s 2024 PFAS ban for food packaging created a direct USD 118 million replacement opportunity for algae-derived solutions.

How fragmented is the competitive landscape?

The market scores 3 on a 1-10 concentration scale because no single company owns more than a low-double-digit share.

Page last updated on: