Screen And Script Writing Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

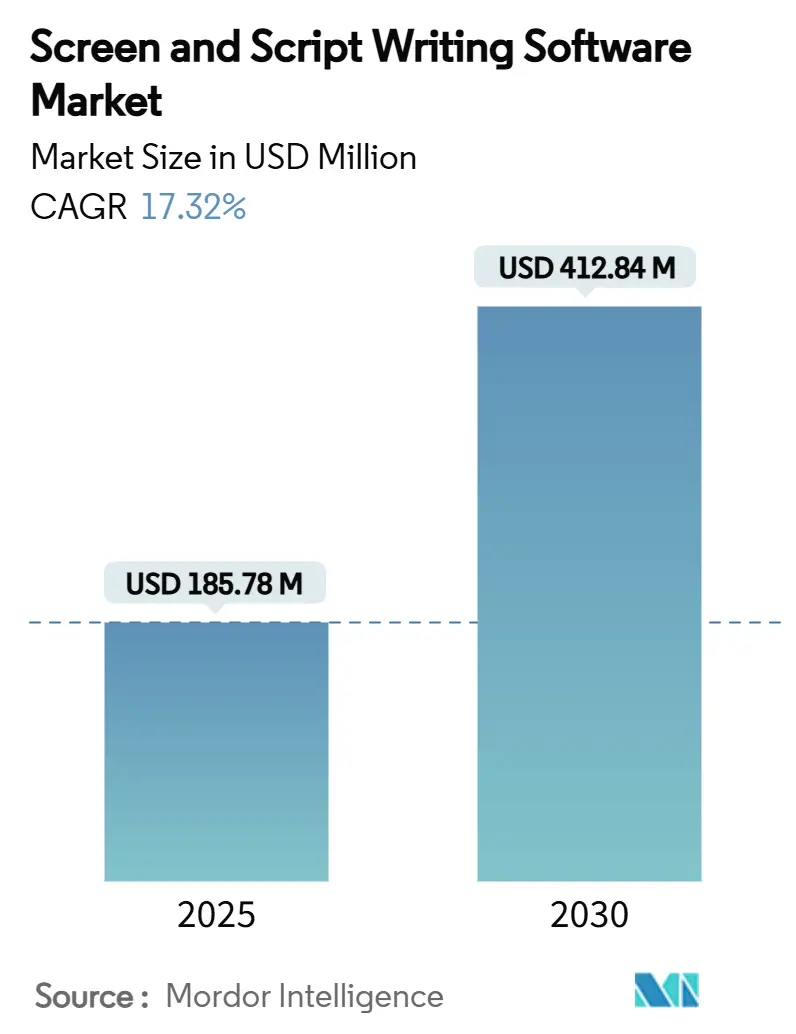

| Market Size (2025) | USD 185.78 Million |

| Market Size (2030) | USD 412.84 Million |

| Growth Rate (2025 - 2030) | 17.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Screen And Script Writing Software Market Analysis by Mordor Intelligence

The screen and script writing software market size stood at USD 185.78 million in 2025 and is forecast to reach USD 412.84 million by 2030, expanding at a CAGR of 17.32%. The growth trajectory reflects rising demand for AI-enhanced collaborative platforms, steady cloud migration, and wider adoption among independent creators. Subscription SaaS continues to anchor vendor revenue even as freemium tiers expand, while regional streaming production hubs in Asia-Pacific accelerate product localization and multilingual workflow demand. Regulatory clarity from the Writers Guild of America (WGA) regarding the acceptable role of AI further strengthens the human-AI collaboration model that underpins new product releases. Competitive intensity remains moderate: legacy desktop leaders still hold meaningful shares but face disruption from browser-native, machine-learning-centric challengers that integrate directly into pre-production and virtual-production pipelines.[1]Writers Guild of America, “Artificial Intelligence,” wga.org

Key Report Takeaways

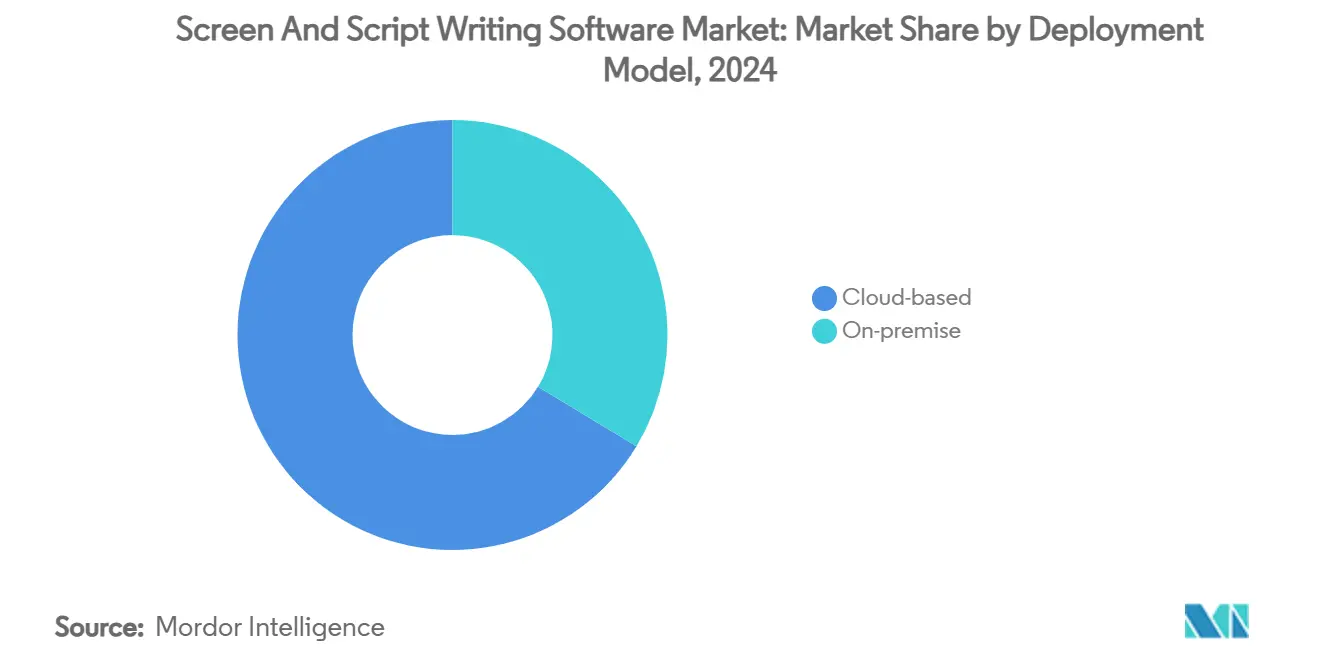

- By deployment model, cloud-based solutions captured 66.34% of screen and script writing software market share in 2024 and are advancing at an 18.23% CAGR through 2030.

- By platform, web-based tools contributed 48.77% to the screen and script writing software market size in 2024 and are projected to grow at 19.01% CAGR to 2030.

- By end user, independent screenwriters are growing at 21.73% CAGR through 2030, outpacing film and TV studios, which retained 39.71% revenue share in 2024.

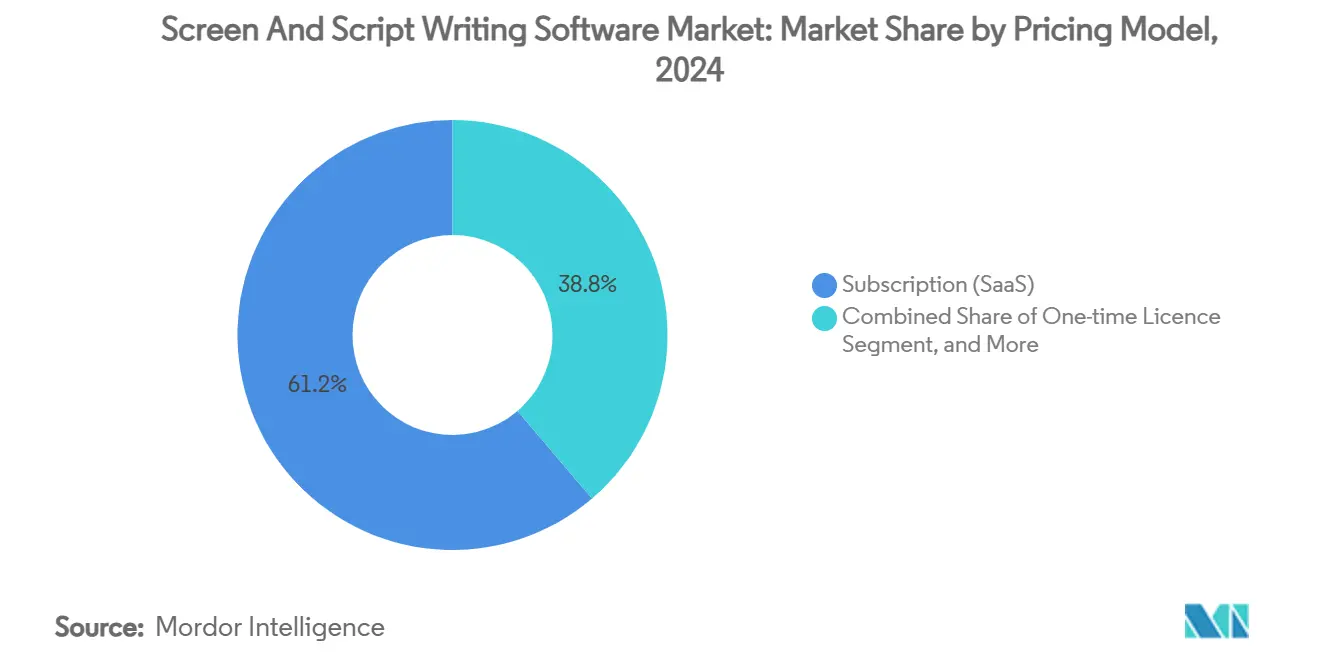

- By pricing model, the subscription tier held 61.24% share of the screen and script writing software market size in 2024, while freemium options are expanding at 19.82% CAGR through 2030.

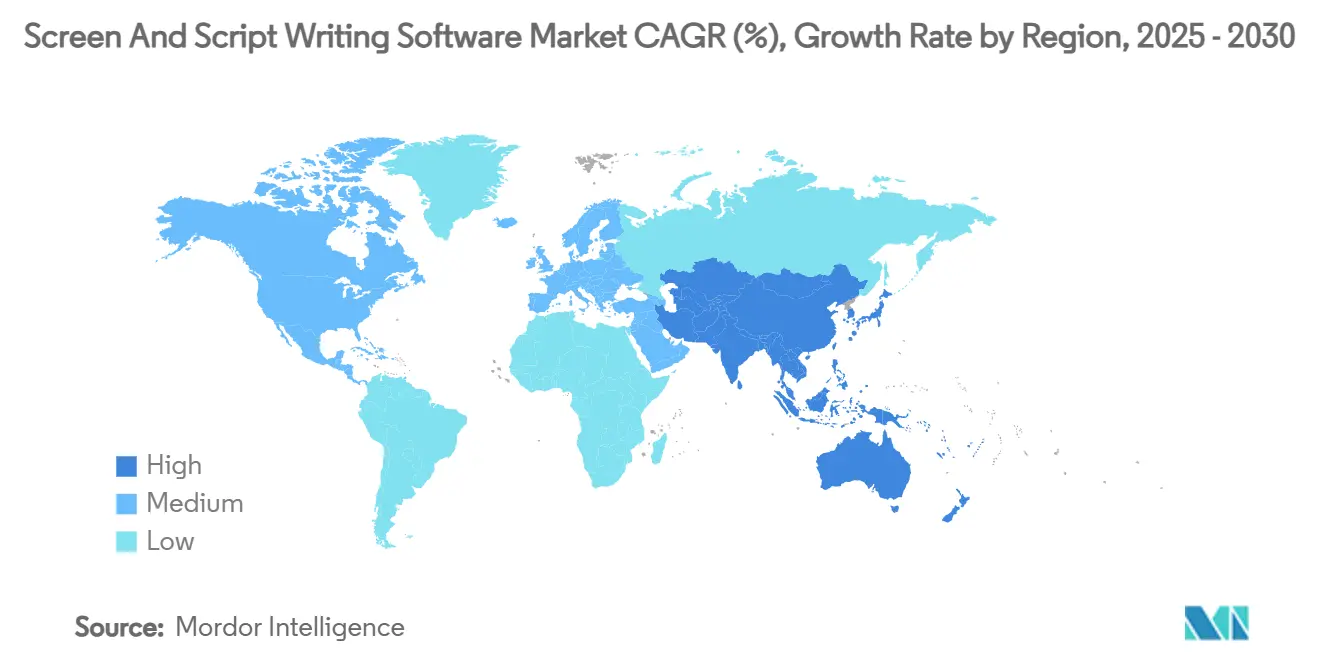

- By geography, Asia-Pacific is forecast to post a 20.81% CAGR between 2025 and 2030, overtaking Europe as the second-largest regional contributor to overall value growth.

Market Trends and Insights

Drivers Impact Analysis of Screen And Script Writing Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for original streaming content | +4.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of cloud-based collaborative platforms | +3.8% | Global, accelerated in North America and Europe | Short term (≤ 2 years) |

| AI-driven writing-assistant and formatting automation | +3.1% | North America and Europe early adoption, Asia-Pacific following | Medium term (2-4 years) |

| Expanding pool of independent creators and micro-studios | +2.9% | Global, with strongest growth in Asia-Pacific and North America | Long term (≥ 4 years) |

| Real-time virtual-production workflow alignment | +1.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Script-as-code metadata and API monetization model | +1.4% | North America and Europe technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Original Streaming Content

The unprecedented content budgets of global streaming services are reshaping script-to-screen workflows. Netflix invested USD 15 billion in 2024, and pilot projects such as “El Eternauta” demonstrated how generative AI compressed visual-effects timelines by a multiple of ten, validating integrated toolchains that connect screenplay development to downstream production tasks.[2]Netflix, “Technology Blog – Generative AI at Work,” netflix.com Studios now require platforms that embed budgeting, scheduling, and localization modules during the writing phase. Regional streaming entrants in India, Korea, and Indonesia accelerate multi-language capabilities, while episodic storytelling norms push vendors to add showrunner dashboards that track season-arc continuity. Predictive analytics that estimate audience affinity scores before green-lighting drafts are emerging as a core differentiator demanded by commissioning teams.

Growing Adoption of Cloud-Based Collaborative Platforms

Real-time, multi-author editing, granular version control, and instant device syncing have become baseline expectations. WriterDuet’s architecture allows concurrent editing without file-locking constraints, illustrating why browser-native approaches now dominate new enterprise rollouts.[3]WriterDuet, “Collaborative Screenwriting Platform,” writerduet.com Cloud deployment also simplifies integration with project-management suites, enabling producers to monitor script progress against budget burn-down charts. Universities increasingly mandate cloud licences because they eliminate computer-lab image management and license-key logistics. The post-pandemic normalization of hybrid work makes low-latency web workflows essential for geographically dispersed teams.

AI-Driven Writing Assistants and Formatting Automation

Machine-learning modules expedite scene slugline generation, dialogue polishing, and automatic compliance checking with studio template standards. NolanAI commercialized these features via annual tiers ranging from USD 480 to USD 1,200, proving that writers will pay premiums for tangible productivity gains. WGA guidelines, however, stipulate that AI-generated text cannot qualify as “literary material.” This ensures human authorship remains central, steering vendors toward co-creation models rather than fully automated drafting. Looking ahead, patent filings by large technology firms suggest AI will soon flag potential IP conflicts and predict regional censorship risks during pre-production.

Expansion of Independent Creators and Micro-Studios

Everyday creators leveraging accessible DSLR and mobile-cinema rigs push demand for professional-grade yet affordable tools. Full Sail University’s production incubator saw enrolment rise in 2025, and its curriculum standardizes Celtx cloud plans for all students, reinforcing early brand loyalty. Crowdfunding campaigns now include line items for cloud-based script tools, and social-media-first formats necessitate modules that output vertical or 15-second scripts compatible with in-app editors. Vendors that combine freemium entry points with AI-powered upsell layers stand to capture this long-tail cohort sustainably.

Restraints Impact Analysis of Screen And Script Writing Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of free / open-source alternatives | -2.7% | Global, with stronger impact in price-sensitive markets | Short term (≤ 2 years) |

| High licence and subscription costs for freelancers | -1.9% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Lack of unified screenplay markup interoperability | -1.4% | Global, with acute impact in collaborative productions | Medium term (2-4 years) |

| Copyright risk in AI-generated story elements | -1.2% | North America and Europe regulatory focus, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Free / Open-Source Alternatives

Community-maintained projects such as Trelby and KIT Scenarist deliver baseline formatting at zero cost, causing budget-sensitive cohorts to postpone paid upgrades. Their GitHub repositories, however, suffer from inconsistent update cadences, prompting professional teams to migrate once feature gaps appear. Commercial vendors counteract the price narrative by bundling encrypted cloud storage, studio-grade security compliance, and 24/7 support—benefits that open-source projects cannot reliably fund.

High Licence and Subscription Costs for Freelancers

Standalone licences such as Final Draft’s USD 249.99 desktop package remain aspirational for early-career writers. While student discounts create temporary relief, the post-graduation jump in pricing often triggers churn toward free web editors. Vendors are increasingly experimenting with usage-based micro-billing that charges only for AI requests or collaboration seats. Such granularity widens addressable demand without diluting perceived product value among enterprise buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Screen And Script Writing Software Market Segment Analysis

By Deployment Model:

Cloud Outpaces On-Premise SolutionsCloud-based offerings contributed 66.34% of 2024 revenue and are forecast to grow at 18.23% CAGR until 2030, reaffirming their pivotal role in the screen and script writing software market. This leadership stems from secure, device-agnostic access that supports distributed writers, showrunners, and executives. The pandemic validated always-on collaboration as a necessity rather than a luxury, positioning vendor-hosted infrastructures as default choices for new studio investments. On-premise installations persist in legacy Hollywood post-houses where air-gapped data policies remain strict, but steady improvements in end-to-end encryption, audit trails, and SSO integrations are reshaping risk calculations in favor of SaaS.

Celtx’s acquisition by Backlight illustrated the premium investors place on holistic, cloud-native ecosystems that merge writing, budgeting, and scheduling into a single workspace. These network effects elevate switching costs and reinforce subscription stickiness. Educational programs also prize cloud deployments, seeing them as equitable access enablers for students using personal laptops or campus media labs. Consequently, the screen and script writing software market size attributable to education licenses is expected to rise proportionally with enrolment growth in film studies programs.

By Platform:

Web-Based Interfaces Narrow the Gap with DesktopDesktop applications maintained 51.23% share in 2024, buoyed by Final Draft’s entrenched usage across union writers. Yet browser-native rivals now log 19.01% CAGR, underscoring a secular shift toward installation-free environments that auto-update silently. Progressive Web App architecture lets writers move from laptop to tablet without version friction, directly addressing long-standing compatibility pain points. Chromebooks’ penetration in K-12 and college cohorts accelerates web preference, because they cannot run conventional desktop binaries.

Mobile/tablet experiences remain a niche but pace-setting frontier for vendors committed to ubiquitous access. As virtual-production teams iterate dialogue on LED stages, real-time script annotations via iPad or foldable phones increasingly influence on-set efficiency. Vendors creating uniform UI languages across desktop, web, and mobile will capture incremental mindshare and minimize user retraining overhead.

By Pricing Model:

Subscriptions Dominate but Freemium AcceleratesSubscription SaaS plans represented 61.24% in 2024 and remain foundational to vendor cash-flow predictability. Continuous delivery of AI models, security patches, and storyboard extensions justify recurring billing for enterprise accounts. Freemium tiers, however, are posting 19.82% CAGR as vendors race to seed creator ecosystems early and monetize later via advanced exports or team-review seats. The screen and script writing software market share derived from one-time licences will further erode unless vendors re-package perpetual packages with optional cloud bolt-ons.

Tiered feature gating is becoming sophisticated: entry levels allow limited script page counts and watermarked PDFs, while premium tiers unlock predictive audience analytics and private-cloud hosting. This stratification ensures price-sensitive users remain engaged and evangelize products without cannibalizing top-line ARPU.

By End User:

Independent Creators Anchor Future Volume GrowthFilm and TV studios retained 39.71% in 2024 thanks to blockbuster production budgets and compliance-driven procurement cycles. Nevertheless, the independent screenwriter cohort is expanding at 21.73% CAGR, propelled by democratized distribution on fast-growing ad-supported video-on-demand (AVOD) platforms. The screen and script writing software market size for this segment is expected to surpass USD 100 million by 2030 as micro-studios internalize writing, financing, and distribution tasks traditionally handled by large studios.

Gaming studios are another high-growth vertical; branching-narrative design tools such as Articy Draft integrate visual flowcharts and real-time game-engine round-trip editing. Ad-agency storyboard units increasingly subscribe to script modules that output both 30-second and 6-second cuts simultaneously, compressing pre-production timetables for digital campaigns.

Geography Analysis

North America Screen And Script Writing Software Market

North America represented 39.64% revenue in 2024, anchored by Los Angeles and New York production ecosystems. The region benefits from early adoption of AI-assisted formatting and mature cloud infrastructure interconnects. Studios routinely integrate script APIs into proprietary budgeting dashboards, setting functional benchmarks later emulated across other regions.

Europe Screen And Script Writing Software Market

Europe’s multilingual landscape creates complexity: vendors must offer one-click switching among Final Draft-style U.S. formats, British standard layouts, and local language character encoding. GDPR compliance also mandates EU-based data residency options. As a result, European customers prefer vendors that provide selectable data-centers within the region, a feature increasingly marketed as a premium add-on.

APAC Screen And Script Writing Software Market

Asia-Pacific is the fastest-growing market at 20.81% CAGR through 2030. Mainland China is moving en masse from pirated legacy binaries toward licensed, cloud-based English-Mandarin dual-language platforms that accelerate cross-border co-production. Korea and Japan channel government grants to local production, which demands integrated subtitle and closed-caption export during the writing stage. India’s booming OTT sector prompts demand for multi-dialect support and episodic tracking to meet regulatory episode-length disclosures.

South America and MEA Screen And Script Writing Software Market

South America and the Middle East & Africa remain nascent but show greenfield potential as local streamers scale original slates. Regional IP funds are increasingly tying financing approval to the use of collaborative cloud scripts that leave auditable revision trails, reassuring investors about story maturity before disbursement.

Competitive Landscape

The market remains moderately fragmented. Final Draft, under Cast & Crew ownership, leverages bundle synergies with payroll and budgeting services, reinforcing its grip on unionized writers. Celtx focuses on indie and education verticals, with Backlight capital injecting resources into roadmap acceleration. WriterDuet anchors its proposition on real-time collaboration features unavailable in legacy tools.

AI-native entrants such as NolanAI and Sudowrite cultivate early adopter communities by inserting GPT-driven scene expansion, sentiment analysis, and tone matching modules. Their advantage lies in serverless, scalable back-ends that iterate faster than monolithic desktop peers. These dynamics are catalyzing a wave of M&A scouting by larger media software consolidators seeking to plug AI and cloud gaps rapidly.

System integrators and cloud hyperscalers demonstrate growing interest: Amazon’s patent filings outline automatic shot-list derivation from screenplay metadata, signaling potential vertical integration toward end-to-end pre-production suites. Boutique vendors in gaming, such as Articy Software, differentiate via branching-narrative visualization essential for interactive media. Competitive success now depends on the depth of platform ecosystems, breadth of third-party plug-ins, and strength of enterprise-grade security certifications.

Screen And Script Writing Software Industry Leaders

Final Draft LLC

Celtx Inc.

StudioBinder Inc.

Adobe Inc.

WriterDuet Inc.

- *Disclaimer: Major Players sorted in no particular order

Screen And Script Writing Software Market Companies Covered in this Report

- Final Draft LLC

- Celtx Inc.

- StudioBinder Inc.

- Adobe Inc.

- WriterDuet Inc.

- Fade In LLC

- Write Brothers Inc. (Movie Magic Screenwriter)

- Arc Studio Labs Inc.

- Scrivener – Literature and Latte Ltd.

- Trelby Project (Open-source)

- KIT Scenarist LLC

- Highland Software LLC

- Contour – Mariner Software Inc.

- Storyist Software LLC

- Quip Story Software Ltd.

- Scrite – SandT Tech Services Pvt Ltd

- Ulysses GmbH

- Final Draft Mobile – Cast and Crew

- Amazon Storywriter (Amazon Studios)

- Microsoft Corp.

Recent Industry Developments in Screen And Script Writing Software Market

- July 2025: Netflix confirmed that generative AI shortened visual-effects delivery on “El Eternauta” by a 10× factor, validating the strategic bet on internal AI pipelines that seamlessly ingest finalized scripts and hand them to real-time rendering engines.

- March 2025: Quote-Unquote Apps released Highland Pro, a multi-device writing suite with automatic formatting, iCloud syncing, and distraction-free modes. The upgrade extends the firm’s freemium ladder, positioning the paid tier as an affordable middle ground between open-source tools and enterprise packages.

- March 2025: Articy released articy:draft X for macOS, extending its interactive narrative platform to creative professionals in Apple-centric workflows. The launch aims to capture storytellers building branching narratives for cross-platform games.

- January 2025: The Writers Guild of America revised its AI policy to ensure transparency whenever AI-generated elements are supplied to writers, solidifying the collaborative framework that software vendors must follow.

Global Screen And Script Writing Software Market Report Scope

Segmentation Overview

| Cloud-based |

| On-premise |

| Desktop |

| Web |

| Mobile / Tablet |

| Subscription (SaaS) |

| One-time Licence |

| Freemium / Ad-supported |

| Film and TV Studios |

| Independent Screenwriters |

| Educational Institutions |

| Gaming Studios |

| Advertising and Marketing Agencies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Deployment Model | Cloud-based | ||

| On-premise | |||

| By Platform | Desktop | ||

| Web | |||

| Mobile / Tablet | |||

| By Pricing Model | Subscription (SaaS) | ||

| One-time Licence | |||

| Freemium / Ad-supported | |||

| By End-user | Film and TV Studios | ||

| Independent Screenwriters | |||

| Educational Institutions | |||

| Gaming Studios | |||

| Advertising and Marketing Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the screen and script writing software space by 2030?

The market is expected to reach USD 412.84 million by 2030, growing at a 17.32% CAGR.

Which region is forecast to expand fastest between 2025 and 2030?

Asia-Pacific is projected to log a 20.81% CAGR owing to surging streaming content production and modernization of local workflows.

Why are cloud-based deployments growing rapidly?

Cloud architectures enable real-time collaboration, seamless device syncing, and integration with budgeting dashboards, leading to an 18.23% CAGR for the segment.

How do AI features influence purchasing decisions?

Writers pay premiums for AI modules that automate formatting, suggest dialogue, and forecast compliance risks, while WGA guidelines preserve human authorship.

What pricing models dominate the market?

Subscription SaaS plans hold 61.24% share, though freemium tiers are expanding quickly as entry points for independent creators.

How are AI writing assistants reshaping creative workflows?

Embedded machine-learning modules automate dialogue polishing, scene sluglines, and compliance checks, allowing writers to redirect time toward narrative development while retaining full authorship under WGA rules.

Page last updated on: