Scaffold Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

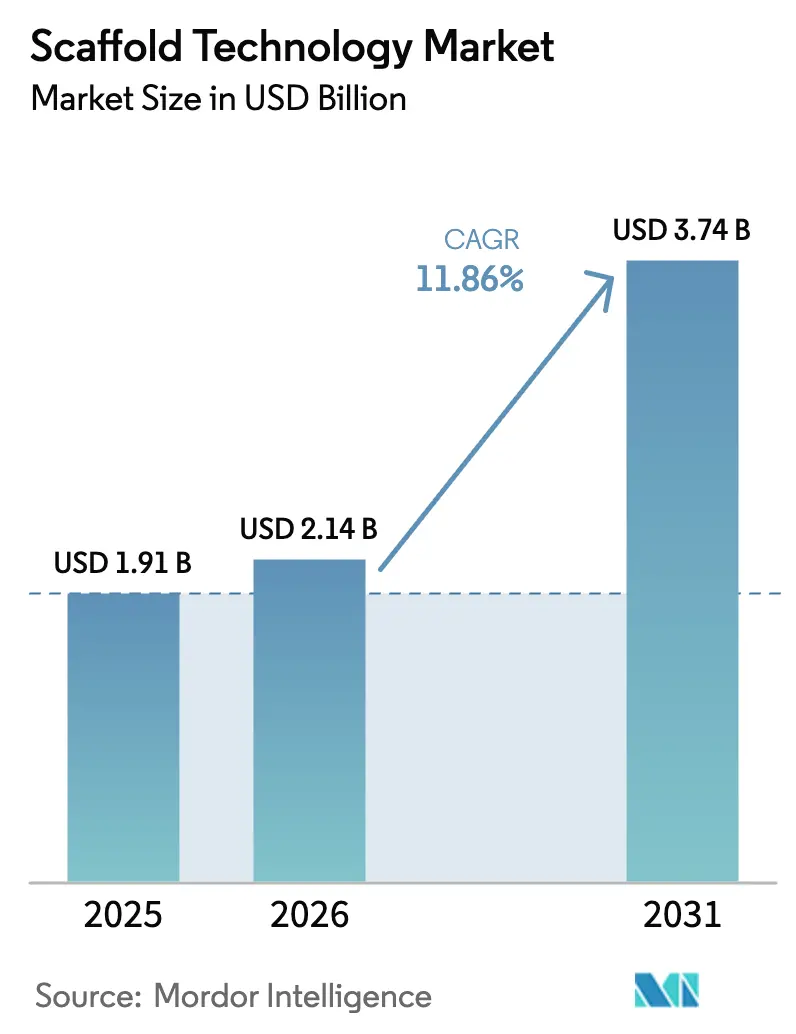

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scaffold Technology Market Analysis by Mordor Intelligence

The Scaffold Technology Market size was valued at USD 1.91 billion in 2025 and estimated to grow from USD 2.14 billion in 2026 to reach USD 3.74 billion by 2031, at a CAGR of 11.86% during the forecast period (2026-2031).

Demand strengthens as three-dimensional cellular models replace two-dimensional cultures, while regulatory bodies approve the first scaffold-based vascular and cell therapies. Hydrogels remain the largest product class, nanofiber scaffolds expand quickest, and orthopedic indications dominate by disease type. Hospitals and diagnostic centers show the fastest end-user uptake, confirming that clinical adoption is accelerating beyond research settings. Geographic performance is led by North America, yet Asia-Pacific records the highest growth on the back of local manufacturing investment, harmonized regulations, and increased funding for regenerative medicine.

Key Report Takeaways

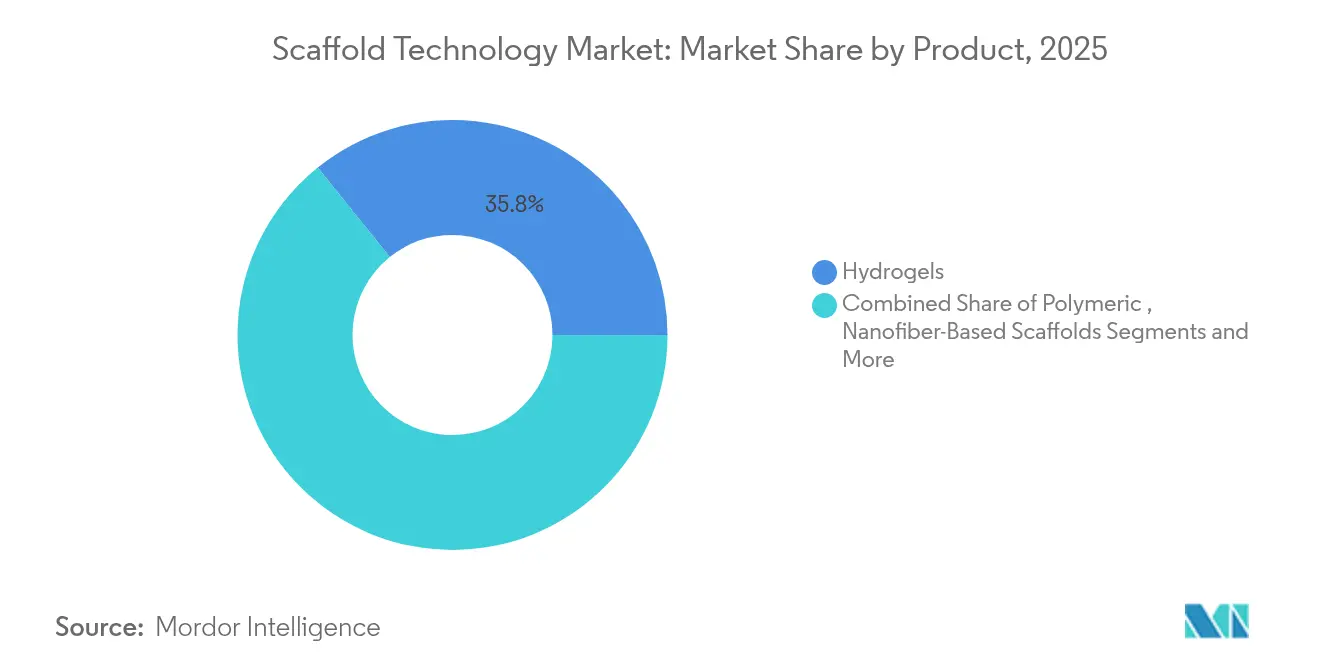

- By product, hydrogels led with 35.78% revenue share in 2025, whereas nanofiber-based scaffolds are projected to surge at a 15.21% CAGR through 2031.

- By disease type, orthopedics held 26.96% of the scaffold technology market share in 2025, while neurology is poised to expand at a 13.62% CAGR to 2031.

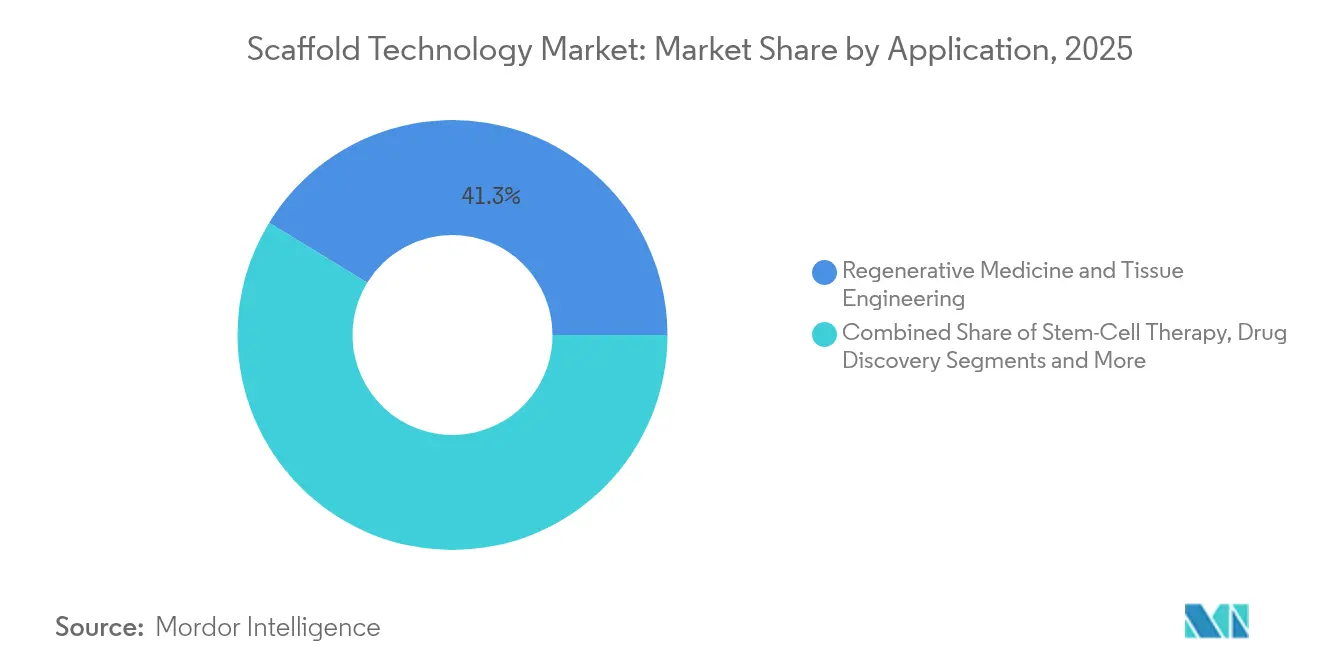

- By application, regenerative medicine and tissue engineering accounted for 41.25% share of the scaffold technology market size in 2025, yet stem cell therapy is expected to rise at a 14.54% CAGR between 2026-2031.

- By end user, biotechnology and pharmaceutical organizations commanded 52.90% share of demand in 2025; hospitals and diagnostic centers record the strongest CAGR at 14.28% through 2031.

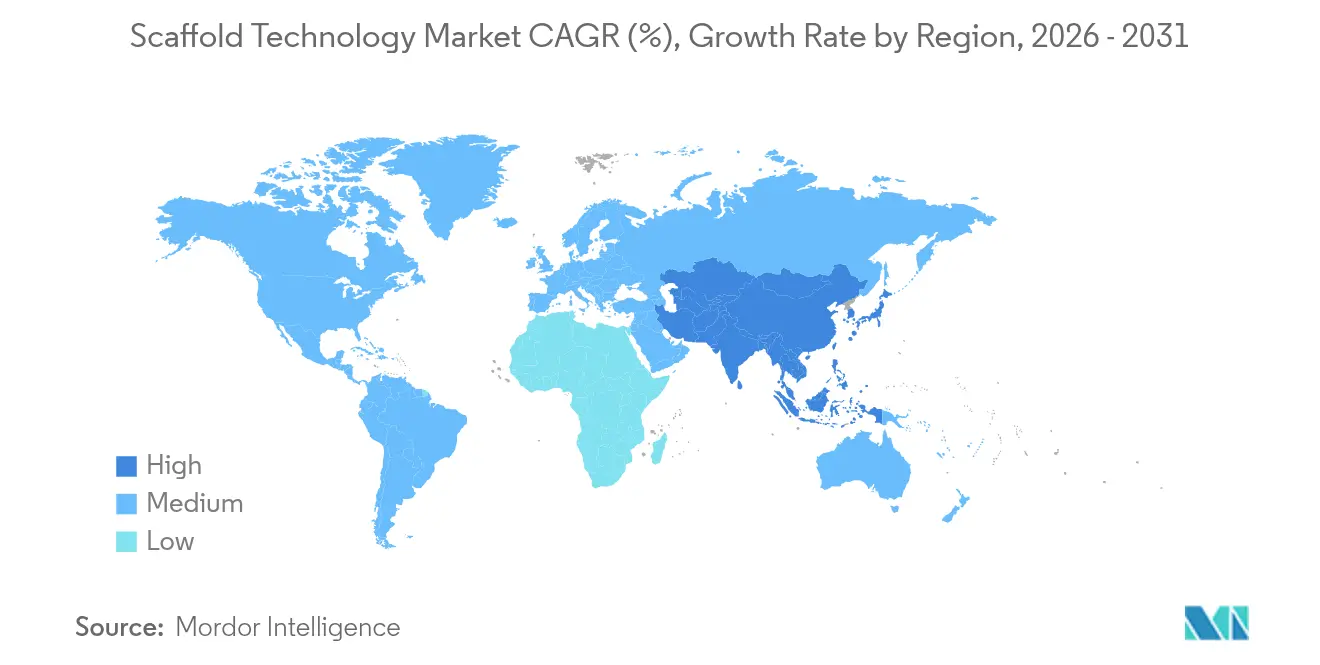

- By geography, North America retained 39.02% market share in 2025 whereas Asia-Pacific is forecast to grow at a 14.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Scaffold Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of 3D cellular models in translational research | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing demand for tissue-engineered grafts for orthopedic and musculoskeletal repair | +1.8% | North America and Asia-Pacific core, spill-over to Europe | Long term (≥ 4 years) |

| Accelerated approvals for regenerative-medicine products by FDA and EMA | +1.5% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shift toward xeno-free, chemically defined scaffold materials | +1.3% | Global | Medium term (2-4 years) |

| Emergence of AI-directed scaffold-design platforms | +1.1% | North America and Europe, technology transfer to Asia-Pacific | Long term (≥ 4 years) |

| Vertical integration by CMOs into scaffold manufacturing for cell-therapy clients | +0.9% | Global, concentrated in bioprocessing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of 3D cellular models in translational research

Pharmaceutical and biotechnology laboratories are replacing two-dimensional cultures with scaffold-based three-dimensional systems because they better replicate human physiology. In March 2025, University of Tokyo scientists showed that placenta-derived IL1α protein accelerated liver organoid growth fivefold, enabling organoids up to 400 µm thick and addressing scalability challenges.[1]Yoshiki Kuse, “Placenta-Derived Factors Contribute to Human iPSC-Liver Organoid Growth,” Nature Communications, nature.comOncology programs now rely on scaffold-embedded tumor organoids that mirror microenvironmental drug resistance patterns, reducing late-stage attrition and sharpening predictive validity.

Growing demand for tissue-engineered grafts for orthopedic applications

An aging population and higher sports injury incidence sustain substantial requirements for bone and soft-tissue reconstruction. Becton Dickinson treated the first patient in its STANCE clinical trial for the fully absorbable P4HB GalaFLEX LITE scaffold in March 2025, extending scaffold use beyond bone repair to breast implant revision. Meanwhile, multiphasic bone-ligament-bone scaffolds incorporating mesoporous hydroxyapatite and deferoxamine demonstrate mechanical strength akin to native ACL tissue while promoting dual therapeutic delivery.

Accelerated regulatory approvals for regenerative-medicine products

Fast-track designations shorten development cycles. The FDA cleared Symvess, the first acellular tissue-engineered vessel, in December 2024, establishing clinical precedent for scaffold-based vascular devices. Ryoncil, an allogeneic mesenchymal stromal cell therapy, also received FDA approval in 2024 for pediatric acute graft-versus-host disease, validating cell-scaffold combination approaches.[2]Office of the Commissioner, “FDA Approves First Acellular Tissue Engineered Vessel to Treat Vascular Trauma in Extremities,” FDA, fda.gov

Shift toward xeno-free, chemically defined scaffold materials

Contamination concerns push developers to abandon animal-derived components. Evonik introduced Vecollan, a non-animal collagen platform, providing consistent quality suitable for medical devices and reducing regulatory risk. Standardized materials support reproducible manufacturing protocols, easing clinical translation.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and validation costs for GMP-grade scaffolds | -1.7% | Global, more acute in emerging markets | Short term (≤ 2 years) |

| Lack of cross-lab reproducibility in complex 3D culture results | -1.2% | Global, hindering multi-site studies | Medium term (2-4 years) |

| Regulatory ambiguity around bio-printed composite scaffolds | -0.9% | North America and Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Limited availability of pharma-grade raw biomaterials | -0.8% | Global, supply chain concentrated regionally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High implementation and validation costs for GMP-grade scaffolds

Transitioning from research-grade to clinical-grade production requires lot-to-lot consistency, full traceability, and validated animal-free processes. Bio-Techne details quality measures that add 18-24 months and sizeable capital to development schedules, challenging smaller firms.

Lack of cross-lab reproducibility in complex 3D culture results

Variable extracellular matrices, culture conditions, and analytics generate inconsistent outcomes. Studies highlight batch-to-batch differences in Matrigel, spurring a shift toward synthetic matrices with adjustable stiffness and ligand density.[3]Kan Li, “Reproducible Extracellular Matrices for Tumor Organoid Culture: Challenges and Opportunities,” Journal of Translational Medicine, translational-medicine.biomedcentral.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Nanofiber Innovation Drives Market Evolution

Hydrogels led the scaffold technology market with 35.78% share in 2025, reflecting strong biocompatibility and adaptable mechanical properties. Polymeric scaffolds occupy substantial share due to fabrication versatility, while micropatterned surface microplates cater to high-throughput drug discovery. Nanofiber-based scaffolds post a 15.21% CAGR to 2031, the fastest among products, because their high surface-area architecture mimics natural extracellular matrices and supports osteogenesis.

Hybrid approaches merge 3D bioprinting with electrospun nanofibers, resulting in multilayer structures that deliver precise geometries and biological cues. Melt electrowriting allows sub-micron control, important for musculoskeletal applications. These advances place nanofibers at the forefront of next-generation solutions while hydrogels continue anchoring mainstream demand.

By Disease Type: Neurology Applications Accelerate Beyond Traditional Orthopedics

Orthopedic indications supplied 26.96% of the scaffold technology market share in 2025, backed by decades of clinical protocols. Cancer studies leverage scaffolds to recreate tumor microenvironments, improving predictive accuracy of therapeutics. Neurology emerges as the quickest-growing area at 13.62% CAGR, propelled by bionic scaffolds that coordinate bioactive factor release and nanomaterials to guide axonal growth.

Customized 3D-printed nerve conduits integrate conductive polymers and growth factors, addressing peripheral nerve injuries where autograft supply is limited. Multiphasic bone-ligament constructs for ACL repair continue to evolve, combining mechanical reinforcement with controlled drug delivery. Together, these innovations support diversified growth beyond established bone repair domains.

By Application: Stem Cell Therapy Drives Next-Generation Growth

Regenerative medicine and tissue engineeri ng retained 41.25% of revenue in 2025 and remain the central application. Drug discovery gains traction as organ-on-chip systems use scaffolds to model tissue-specific pharmacodynamics. Stem cell therapy delivers the highest CAGR at 14.54%, assisted by xeno-free media that boosts derivation efficiency to 46% for extended pluripotent stem cells.

Electrospun meshes coated with biological polymers improve mesenchymal stem cell viability and paracrine secretion, advancing cartilage and cardiac repair trials. Artificial-intelligence platforms now adjust scaffold composition based on cell omics data, accelerating personalized therapy development.

By End User: Hospital Adoption Accelerates Clinical Translation

Biotechnology and pharmaceutical companies captured 52.90% demand in 2025, reflecting high R&D spend and internal pilot manufacturing. Research institutions remain key users for proof-of-concept studies. Hospitals and diagnostic centers post the fastest 14.28% CAGR through 2031, underscoring successful bench-to-bedside transition. Vericel’s NexoBrid approval for pediatric burn care revealed hospital uptake potential across 20 specialized US centers.

Robotic automation clusters now support hospital-based cell therapy suites, reducing labor while maintaining GMP compliance. Contract manufacturers integrate scaffold production to offer turnkey solutions, shrinking supply bottlenecks for clinical programs.

Geography Analysis

North America held 39.02% of the scaffold technology market in 2025, sustained by robust FDA frameworks that fast-track advanced therapies and by a dense network of biotechnology firms. The United States benefits from academic–industry consortia that share GMP facilities, while Canada expands with large-scale CDMO plants such as OmniaBio’s 100,000 ft² site, improving regional supply resilience.

Europe maintains solid growth as cross-border Horizon research grants fund tissue-engineering consortia and the EMA introduces harmonized guidance for combined products. Germany and the Netherlands host additive-manufacturing clusters that emphasize composite scaffold development for musculoskeletal care, aligning with local orthopedic device demand.

Asia-Pacific is the fastest-growing region at a 14.02% CAGR. China scales domestic production under government innovation funds, Japan supports regenerative medicine frameworks that expedite market entry, and India leverages cost-effective manufacturing. Advanced research centers in South Korea and Australia contribute high-value intellectual property and clinical trial data, while regional regulators increasingly align with FDA and EMA criteria, reducing approval uncertainty.

Competitive Landscape

The scaffold technology market demonstrates moderate concentration as leading suppliers combine proprietary materials, automated fabrication, and AI-guided design. Integrated players invest in large-scale research hubs; for instance, Merck KGaA committed EUR 300 million to an advanced center focusing on biotechnological products and mRNA processing. Established contract manufacturers such as Lonza broaden capacity with strategic site acquisitions, securing end-to-end services for biologics and scaffold-based therapies.

Competitive themes include platform modularity, where a base scaffold adapts to multiple indications with minimal re-engineering, and vertical integration, as CMOs embed scaffold lines to control quality and timelines. Start-ups emphasize smart biomaterials such as aloe-vera-derived hydrogels for cultured meat and AI-enabled organoid platforms that integrate predictive modeling.

White-space opportunities persist in standardized protocols that resolve reproducibility gaps and in scalable single-use bioreactors tailored to complex scaffold-cell constructs. As capital intensity and regulatory scrutiny rise, partnerships between material specialists, device makers, and therapeutic developers are expected to increase.

Scaffold Technology Industry Leaders

Thermo Fisher Scientific, Inc.

Merck KGaA

REPROCELL Inc.

Becton, Dickinson, and Company

Corning Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: University of Tokyo researchers reported that placenta-derived IL1α protein enhanced liver organoid growth fivefold, achieving 300–400 µm thickness by replicating hypoxic fetal conditions.

- March 2025: BD began treating patients in the STANCE trial using fully absorbable P4HB GalaFLEX LITE scaffold for breast implant revision surgery.

- December 2024: FDA approved Symvess, the first acellular tissue-engineered vessel for extremity vascular trauma, showing 67% primary patency at 30 days.

- December 2024: FDA approved Ryoncil as the first allogeneic mesenchymal stromal cell therapy for steroid-refractory acute graft-versus-host disease in pediatric patients.

Global Scaffold Technology Market Report Scope

As per the scope of the report, scaffold technology is a critical component of tissue engineering, involving the use of extracellular materials that provide biological, mechanical, and chemical support for tissue formation. Scaffolds serve as templates for new tissue, facilitating cell attachment, growth, and differentiation. They are utilized in various applications, including 3D culture assays that assess cell interactions and migration. Scaffolds can be made from a variety of materials, such as hydrogels, polymers, and metals, and can be designed to be either temporary or permanent. Technology is essential in regenerative medicine and is increasingly applied in drug discovery and development.

The scaffold technology market is segmented by type, disease type, application, end user, and geography. By product, the market is segmented into hydrogels, polymeric scaffolds, micropatterned surface microplates, and nanofiber-based scaffolds. By disease type, the market is segmented into orthopedics, musculoskeletal, cancer, skin and integumentary, dental, cardiology and vascular, neurology, and other disease types. By application, the market is segmented into stem cell therapy, regenerative medicine and tissue engineering, drug discovery, and other applications. By end user, the market is segmented into biotechnology and pharmaceutical organizations, research laboratories and institutes, hospitals and diagnostic centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Report Offers the Value (USD) for the Above Segments.

| Hydrogels |

| Polymeric Scaffolds |

| Micropatterned Surface Microplates |

| Nanofiber-Based Scaffolds |

| Orthopedics |

| Musculoskeletal |

| Cancer |

| Skin & Integumentary |

| Dental |

| Cardiology & Vascular |

| Neurology |

| Other Disease Types |

| Stem-Cell Therapy |

| Regenerative Medicine & Tissue Engineering |

| Drug Discovery |

| Other Applications |

| Biotechnology & Pharmaceutical Organizations |

| Research Laboratories & Institutes |

| Hospitals & Diagnostic Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Hydrogels | |

| Polymeric Scaffolds | ||

| Micropatterned Surface Microplates | ||

| Nanofiber-Based Scaffolds | ||

| By Disease Type | Orthopedics | |

| Musculoskeletal | ||

| Cancer | ||

| Skin & Integumentary | ||

| Dental | ||

| Cardiology & Vascular | ||

| Neurology | ||

| Other Disease Types | ||

| By Application | Stem-Cell Therapy | |

| Regenerative Medicine & Tissue Engineering | ||

| Drug Discovery | ||

| Other Applications | ||

| By End User | Biotechnology & Pharmaceutical Organizations | |

| Research Laboratories & Institutes | ||

| Hospitals & Diagnostic Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the scaffold technology market?

The scaffold technology market was valued at USD 2.14 billion in 2026.

How fast is the scaffold technology market expected to grow?

It is projected to expand at a 11.86% CAGR, reaching USD 3.74 billion by 2031.

Which product segment is growing the fastest?

Nanofiber-based scaffolds are forecast to grow at a 15.21% CAGR through 2031.

Which region will experience the highest growth?

Asia-Pacific is anticipated to register the highest regional CAGR at 14.02% to 2031.

Why are hospitals the fastest-growing end-user group?

Improved reimbursement, greater physician familiarity, and recent FDA approvals are driving hospital adoption at a 14.28% CAGR.

What regulations are shaping market growth?

FDA Regenerative Medicine Advanced Therapy designations and parallel EMA frameworks are accelerating scaffold-based product approvals while highlighting the need for clarity on bio-printed composite constructs.

Page last updated on: