Contract Research Organization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

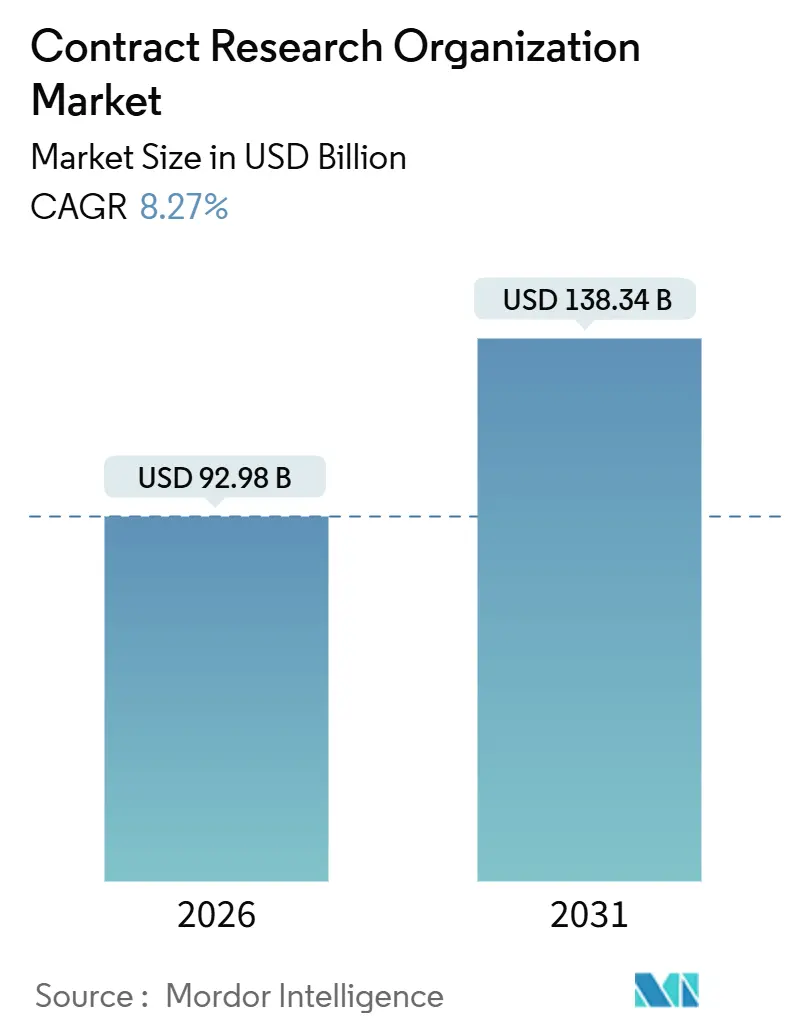

| Market Size (2026) | USD 92.98 Billion |

| Market Size (2031) | USD 138.34 Billion |

| Growth Rate (2026 - 2031) | 8.27% CAGR |

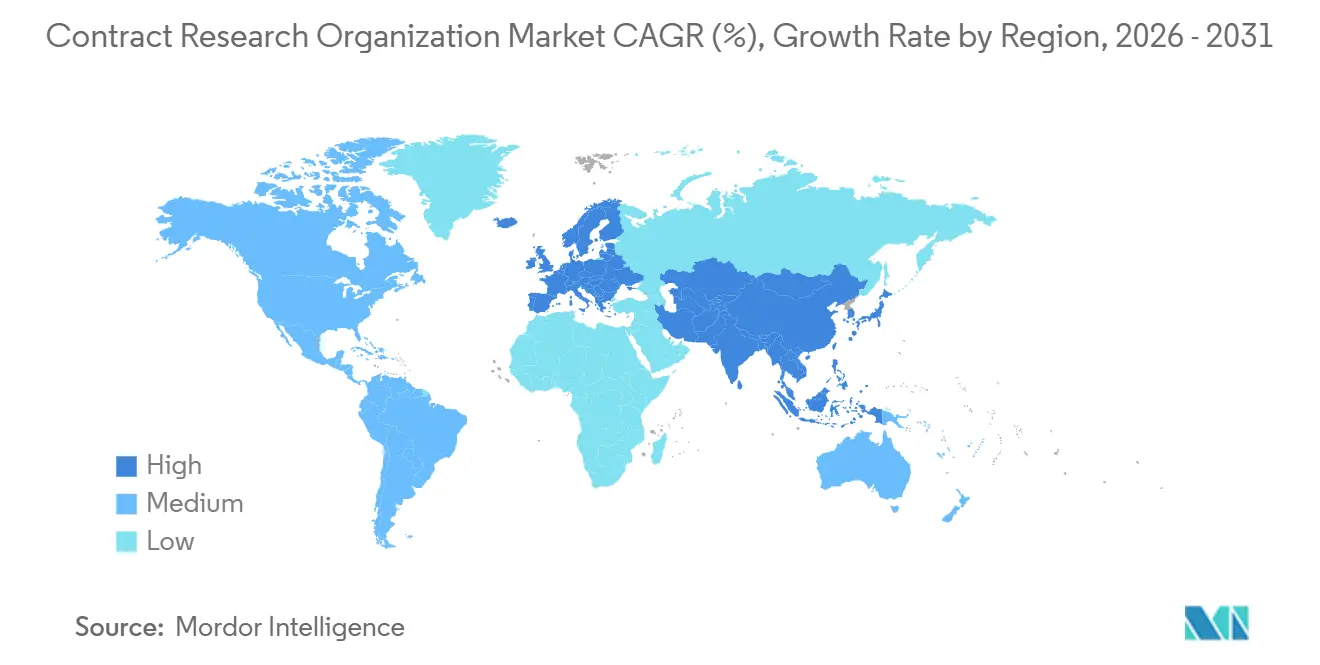

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

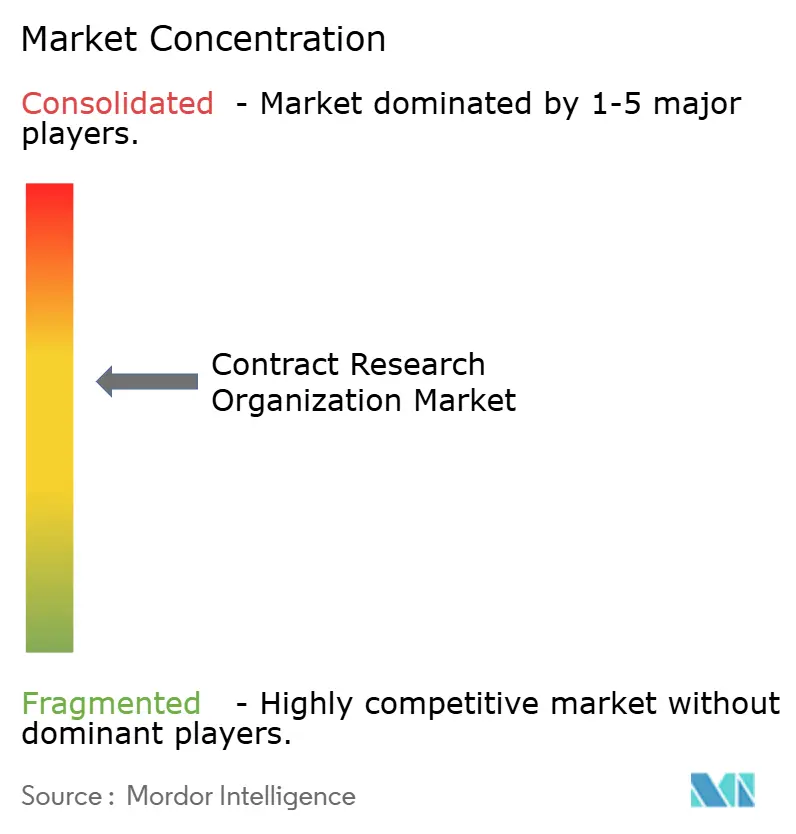

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contract Research Organization Market Analysis by Mordor Intelligence

The Contract Research Organization Market size is estimated at USD 92.98 billion in 2026, and is expected to reach USD 138.34 billion by 2031, at a CAGR of 8.27% during the forecast period (2026-2031).

Revenue expansion is driven by sponsors' increasing need to compress development cycles, secure global patient access, and comply with increasingly complex regulatory pathways. Investment in biologics and cell- and gene-therapies is shifting trial portfolios toward high-complexity protocols that few sponsors can execute in-house. Regulatory agencies continue to award expedited designations, which shorten review times and further encourage the outsourcing of critical functions. Venture capital inflows into early-stage biotechs sustain demand for first-in-human expertise, while technology-enabled site selection tools shorten startup timelines and lower screening failure rates.

Key Report Takeaways

- By service type, clinical research services accounted for 61.45% of the contract research organization market share in 2025; early-phase development services are forecasted to expand at a 10.72% CAGR through 2031.

- By therapeutic area, oncology generated a 21.43% revenue share in 2025; infectious diseases are projected to grow at a 10.81% CAGR through 2031.

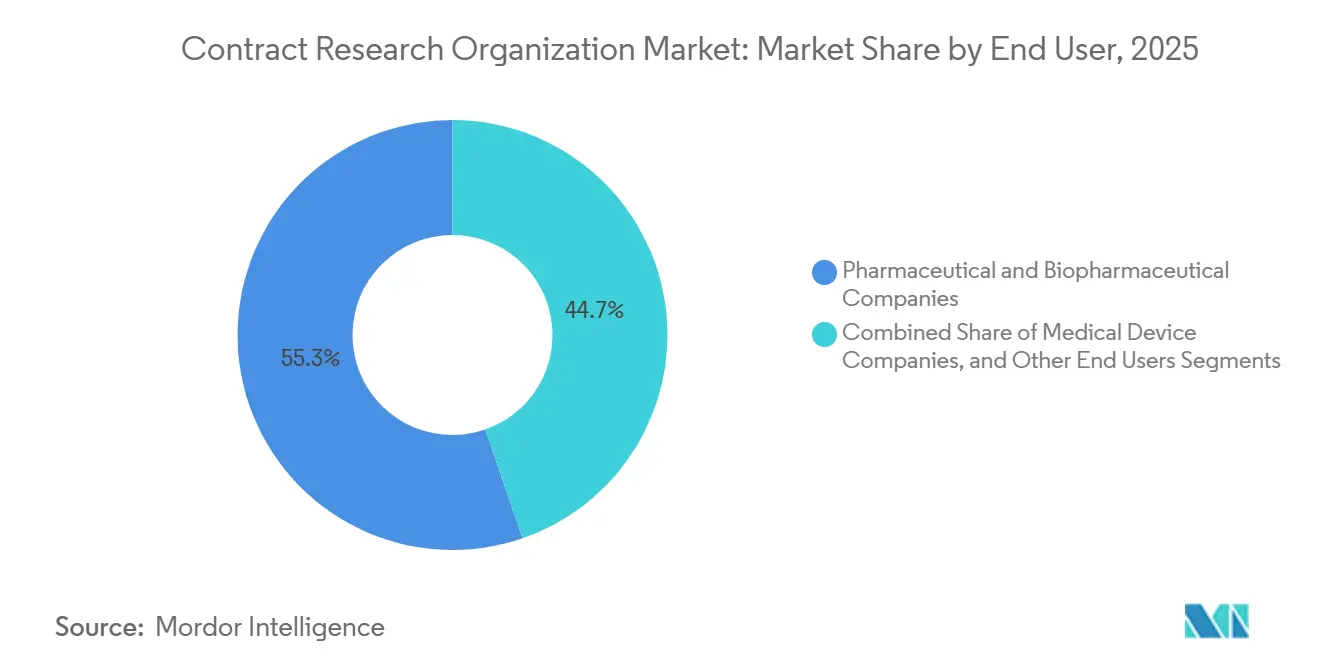

- By end user, pharmaceutical and biopharmaceutical companies accounted for 55.34% spend in 2025; medical device companies are advancing at a 9.58% CAGR to 2031.

- By delivery model, full-service/integrated CROs controlled 62.16% of the contract research organization market share in 2025; functional service provider engagements are increasing at a 10.43% CAGR through 2031.

- By geography, North America led with 38.92% share in 2025; Asia-Pacific is on track for an 11.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Contract Research Organization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume of Biologics and Advanced Therapies Development | +1.8% | North America, Europe, global spill-over | Medium term (2–4 years) |

| Expansion of Emerging Market Patient Pools and Investigator Sites | +1.5% | China, India, South Korea, Latin America, MEA | Long term (≥ 4 years) |

| Accelerated Regulatory Pathways for Orphan and Fast-Track Drugs | +1.2% | Global (FDA, EMA, NMPA) | Short term (≤ 2 years) |

| Growing Venture Capital Funding for Early-Stage Biotech Firms | +1.0% | North America, Europe, Israel, Singapore | Short term (≤ 2 years) |

| Adoption of Decentralized/Hybrid Clinical Trial Architectures | +0.9% | North America, Europe, expanding to APAC and Latin America | Medium term (2–4 years) |

| Integration of Real-World Evidence and Digital Biomarkers to Shorten Timelines | +0.7% | Global (highest acceptance in US and EU) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Biologics and Advanced Therapies Development

Biologics and cell- and gene-therapy pipelines require viral-vector production, ex vivo cell manipulation, and long-term patient monitoring, which most sponsors lack internally. The FDA’s Regenerative Medicine Advanced Therapy designation expedites the qualification of products, rewarding CROs that can manage adaptive designs and decentralized sample logistics[1]U.S. Food and Drug Administration, “Decentralized Clinical Trials for Drugs, Biological Products, and Devices,” fda.gov. New CMC guidelines have reduced IND uncertainties, prompting a reallocation of capital from small-molecule portfolios toward biologics. As biosimilars pressure legacy revenues, sponsors lean on CRO partners to supply the highly specialized infrastructure needed for durable gene-editing trials.

Expansion of Emerging Market Patient Pools and Investigator Sites

China’s multi-regional clinical trial framework now accepts foreign data, accelerating site initiation for multinational programs. India’s Central Drugs Standard Control Organisation has shortened review cycles, drawing oncology and metabolic sponsors seeking treatment-naïve cohorts. Brazil’s ANVISA aligned with ICH E6(R2), reducing administrative friction and promoting Latin American enrollment[2]Agência Nacional de Vigilância Sanitária, “GCP Harmonization Update,” anvisa.gov.br. The demographic breadth in these regions offers rapid accrual and strengthens regulatory submissions through ethnically diverse datasets.

Accelerated Regulatory Pathways for Orphan and Fast-Track Drugs

Fast Track, Breakthrough Therapy, Accelerated Approval, and Priority Review programs enable rolling submissions and the use of surrogate endpoints, thereby compressing timelines that favor nimble CRO execution. The FDA’s orphan drug incentives include tax credits, fee waivers, and seven-year exclusivity, while the EMA’s PRIME scheme offers early scientific advice[3]European Medicines Agency, “PRIME: Priority Medicines,” ema.europa.eu. Harmonization under the ICH enables simultaneous filings, thereby reducing the gap between Phase III readouts and launches.

Growing Venture Capital Funding for Early-Stage Biotech Firms

Series B and C financings fuel asset-light startups that outsource entire clinical portfolios. CROs with first-in-human capabilities capture disproportionate revenue as early success drives follow-on funding. Israel and Singapore attract co-investment, localizing demand for specialized services. Concentration in precision oncology, gene therapy, and rare diseases aligns with investments made by the Biotech CRO industry in niche expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Quality Audits and Compliance Penalties | -0.6% | Global scrutiny, highest in US and EU | Short term (≤ 2 years) |

| High Capital Expenditure for Cutting-Edge Lab Automation | -0.5% | North America, Europe, selective APAC adoption | Medium term (2–4 years) |

| Rising Geopolitical Risks Affecting Cross-Border Trials | -0.4% | US-China, Russia-EU, spill-over to India and Brazil | Long term (≥ 4 years) |

| Scarcity of GMP-Grade Viral Vector Manufacturing Capacity | -0.7% | Global, acute in North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Intensifying Quality Audits and Compliance Penalties

The FDA inspects investigators, IRBs, and sponsors to enforce Good Clinical Practice, pushing CROs to allocate larger budgets to monitoring, electronic audit trails, and third-party verification. The EMA’s Clinical Trials Information System increases transparency, thereby raising the reputational stakes. Smaller providers face margin pressure and consolidation risk as compliance costs climb.

High Capital Expenditure for Cutting-Edge Lab Automation

Robotic sample handling and cloud-based analytics demand significant upfront investments. Sponsors negotiate savings, limiting CRO margin capture. Mid-tier providers form equipment-sharing consortia, while asset-light entrants avoid automation, reinforcing incumbents’ moats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Early-Phase Momentum Outstrips Mature Lines

Early-phase development services, representing the fastest-growing segment of the Contract Research Organization market, are forecast to increase at a 10.72% annual rate through 2031. In value terms, this segment will account for a rising portion of the Contract Research Organization market size as biotech sponsors prioritize rapid proof-of-concept programs. Clinical Research Services remained dominant, with a 61.45% revenue share in 2025; however, heightened procurement scrutiny limits price escalation. Phase I units command premium rates because they have dedicated facilities, experienced medical monitors, and immediate access to academic centers, which mitigate the first-in-human risk. Phase II and Phase III work face commoditization as electronic data capture narrows differentiation. Laboratory Services grow steadily in response to the demand for precision medicine, while Consulting Services retain a niche appeal for complex regulatory strategies.

Sponsors are increasingly deploying biomarker-selected cohorts, which reduces enrollment numbers but increases analytical complexity. Phase IV surveillance expands modestly as agencies request post-approval safety evidence, yet many large sponsors internalize these studies to maintain control over real-world data. Differentiation shifts toward technology platforms, adaptive design expertise, and the seamless integration of decentralized trial components. This bifurcation keeps premium pricing in early-phase activities while mature services compete on operational scale.

By Therapeutic Area: Infectious Diseases Accelerate Beyond Oncology

Oncology generated the most considerable therapeutic-area revenue, at 21.43% in 2025, benefiting from over 1,000 active clinical assets that encompassed immunotherapies, targeted small molecules, and cell therapies. Infectious Diseases, however, exhibits the fastest expansion at 10.81% CAGR through 2031, reflecting pandemic-preparedness investment and mRNA vaccine platforms. Central Nervous System and Immunology each draw sizable spending, aided by the acceptance of digital biomarkers that reduce the need for subjective evaluations. Cardiovascular and Respiratory categories trail as generic erosion shifts R&D funding toward orphan conditions.

Government incentives for antimicrobial development, along with renewed vaccine pipelines, underpin infectious-disease momentum. Oncology’s deceleration represents maturity rather than decline: commercialized checkpoint inhibitors transition activity from late-stage trials to post-marketing commitments. CNS programs still confront high screen-failure rates and lengthy follow-up periods, necessitating collaborations with CROs that include neurology specialists and robust investigator networks. Rare-disease identification remains a bottleneck, granting CROs with proprietary registries a competitive edge.

By End User: Device Manufacturers Drive Outsourcing Growth

Pharmaceutical and biopharmaceutical companies supplied 55.34% of 2025 revenue, yet their proportion is slipping as device firms outsource more complex studies. Medical Device Companies will expand outsourcing at 9.58% CAGR through 2031, buoyed by new AI/ML regulatory guidance that mandates prospective validation and cybersecurity testing. Academic and Government Institutes contribute less revenue but generate high-impact publications, supporting CRO brand visibility.

Device sponsors favor CROs with adaptive-design capabilities and experience navigating breakthrough-device pathways. Venture-backed firms outsource nearly all clinical operations to conserve capital for engineering and regulatory submission fees. Large pharmaceutical companies continue to adopt hybrid models, maintaining strategic oversight while offloading tactical execution. Academic consortia remain price-sensitive, selecting regional partners or fixed-price contracts despite lower margins.

By Delivery Model: Functional Service Providers Capture Flexible Demand

Full-service/integrated providers held 62.16% share in 2025, offering turnkey coverage across protocol design, site activation, monitoring, data management, and submission. Functional Service Provider contracts are on track for a 10.43% CAGR, reflecting sponsors’ preference for modular staff augmentation. Hybrid engagements blend governance from full-service models with selective FSP components, appealing to mid-sized biotechs that demand guidance yet are constrained by budget.

FSP arrangements shorten commitments, letting sponsors redeploy resources as pipelines evolve. Coordination burdens rise, however, as sponsors integrate external staff with internal teams. Full-service models remain favored for global Phase III programs where centralized command reduces execution risk. Technology integration—encompassing eConsent, eSource, and remote monitoring—enables hybrid approaches that optimize both flexibility and strategic oversight.

Geography Analysis

North America contributed 38.92% revenue in 2025, anchored by the United States’ 350,000-site research infrastructure and the FDA’s global regulatory influence. Growth lags the Contract Research Organization market average as sponsors diversify to contain costs and access varied patient pools. Canada and Mexico supply cardiovascular and diabetes cohorts through swift ethics approvals, while U.S. academic centers sustain complex oncology and gene-therapy protocols.

The Asia-Pacific region is poised for an 11.26% CAGR to 2031, the Contract Research Organization market’s fastest regional trajectory, driven by regulatory modernization and vast treatment-naïve populations. China’s streamlined IND reviews and acceptance of foreign data under MRCT promote inclusion in global programs. India accelerates oncology enrollment via shortened review cycles, and Japan’s ICH alignment eases multinational submissions. Australia leverages R&D tax offsets and rapid ethics reviews to attract first-in-human studies. South Korea invests heavily in cell-therapy infrastructure, leading to an increase in advanced-therapy trials.

Europe maintains mature Phase III capacity with harmonized approvals via the EMA’s Clinical Trials Information System. Germany, the United Kingdom, and France remain core hubs, although Brexit now requires parallel UK protocols. Spain and Italy offer relative cost advantages and are capturing incremental respiratory and cardiovascular studies. The Middle East and Africa remain small but are receiving rare-disease and vaccine trials as Gulf states invest in research diversification. Meanwhile, South America, led by Brazil and Argentina, is gaining ground in infectious-disease research amid regulatory harmonization.

Mordor Intelligence provides coverage of the contract research organization market across other key regional markets, including North America and Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The contract research organization market is moderately fragmented, with the top five players accounting for less than 50% combined share, leaving room for specialized boutiques and regional providers. Competition now centers on artificial-intelligence-driven recruitment, real-world evidence generation, and regional expansion into the Asia-Pacific. Sponsors prize technology capabilities that reduce start-up times and uplift data quality. Mid-tier CROs differentiate through therapeutic depth—dedicated oncology or CNS units with proprietary registries—and secure pricing premiums despite smaller footprints.

Technology-enabled newcomers target venture-backed biotechs with asset-light platforms that bundle electronic data capture, telemedicine, and site networks, although their scalability to global Phase III programs remains untested. Heightened quality audits favor incumbents possessing enterprise-level compliance systems.

Geopolitical fragmentation enhances the value of in-country facilities able to navigate data-localization laws. Consolidation is expected as full-service providers acquire niche expertise through mergers, and technology platforms emerge as critical infrastructure for execution.

Contract Research Organization Industry Leaders

ICON plc

Charles River Laboratories

IQVIA Holdings Inc.

Thermo Fisher Scientific Inc. (PPD Inc.)

WuXi AppTec (WuXi Clinical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: WEP Clinical, a full-service contract research organization, completed the acquisition of Siron Clinical, a Netherlands-based European CRO. Siron specializes in flexible, high-quality clinical operations for biotech firms. This move broadens WEP’s global reach and enhances its capacity to provide comprehensive clinical trial solutions across various therapeutic areas.

- December 2025: Avetra, a next-generation Contract Research Organization (CRO), officially launched its operations. It features a modern, site-centric approach to improve collaboration between sponsors, CROs, and investigative sites. With over 350 research-experienced sites nationwide and an in-house central laboratory, Avetra aims to accelerate and streamline clinical trial processes.

- October 2025: Avance Clinical, an Australia-based global CRO specializing in early-phase clinical research, unveiled its new Early Phase Center of Excellence for Biotechs. The center aims to enhance trial design, scientific rigor, and regulatory insight, offering cost-effective solutions for global biotech sponsors. This development expands Avance Clinical’s commitment to delivering innovative and efficient early-phase trials worldwide.

Global Contract Research Organization Market Report Scope

As per the scope of the report, a contract research organization is a company that provides clinical trial services for the pharmaceutical, biotechnology, and medical device industries. CROs range from large, international, full-service organizations to small, niche specialty groups. They can assist their clients in developing a new drug or device from the concept stage to FDA marketing approval, eliminating the need for the drug sponsor to maintain staff for these services.

The contract research organization market is segmented by service type (early-phase development services, clinical research services, laboratory services, consulting services, and data management services), by therapeutic area (oncology, infectious diseases, central nervous system (CNS) disorders, immunological disorders, cardiovascular diseases, respiratory disorders, diabetes, and other therapeutic areas), by end user (pharmaceutical & biopharmaceutical companies, medical device companies, and other end users (academic / government institutes)), by delivery model (full-service / integrated CRO, functional service provider (FSP), and hybrid/modular model), and by geography (North America, Europe, Asia Pacific, South America, and Middle East). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Early-Phase Development Services | |

| Clinical Research Services | Phase I |

| Phase II | |

| Phase III | |

| Phase IV | |

| Laboratory Services | |

| Consulting Services |

| Oncology |

| Infectious Diseases |

| Central Nervous System (CNS) Disorders |

| Immunological Disorders |

| Cardiovascular Diseases |

| Respiratory Disorders |

| Diabetes |

| Other Therapeutic Areas |

| Pharmaceutical & Biopharmaceutical Companies |

| Medical Device Companies |

| Other End Users (Academic / Government Institutes) |

| Full-Service / Integrated CRO |

| Functional Service Provider (FSP) |

| Hybrid / Modular Model |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Service Type | Early-Phase Development Services | |

| Clinical Research Services | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| Laboratory Services | ||

| Consulting Services | ||

| By Therapeutic Area | Oncology | |

| Infectious Diseases | ||

| Central Nervous System (CNS) Disorders | ||

| Immunological Disorders | ||

| Cardiovascular Diseases | ||

| Respiratory Disorders | ||

| Diabetes | ||

| Other Therapeutic Areas | ||

| By End User | Pharmaceutical & Biopharmaceutical Companies | |

| Medical Device Companies | ||

| Other End Users (Academic / Government Institutes) | ||

| By Delivery Model | Full-Service / Integrated CRO | |

| Functional Service Provider (FSP) | ||

| Hybrid / Modular Model | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the Contract Research Organization market?

The Contract Research Organization market size is USD 92.98 billion in 2026.

How fast is the sector growing?

Revenue is forecast to expand at an 8.27% CAGR, reaching USD 138.34 billion by 2031.

Which service line is growing the quickest?

Early-Phase Development Services will rise at a 10.72% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Streamlined approvals in China and India and lower per-patient costs drive an 11.26% CAGR for the region.

How are decentralized trials influencing outsourcing?

Hybrid and remote models improve retention by up to 30% and are boosting demand for CROs with digital capabilities.

What capacity bottleneck restricts gene-therapy studies?

A shortage of GMP-grade viral-vector slots pushes lead times beyond 18 months, delaying early-phase trials.

Page last updated on: