Preclinical CRO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

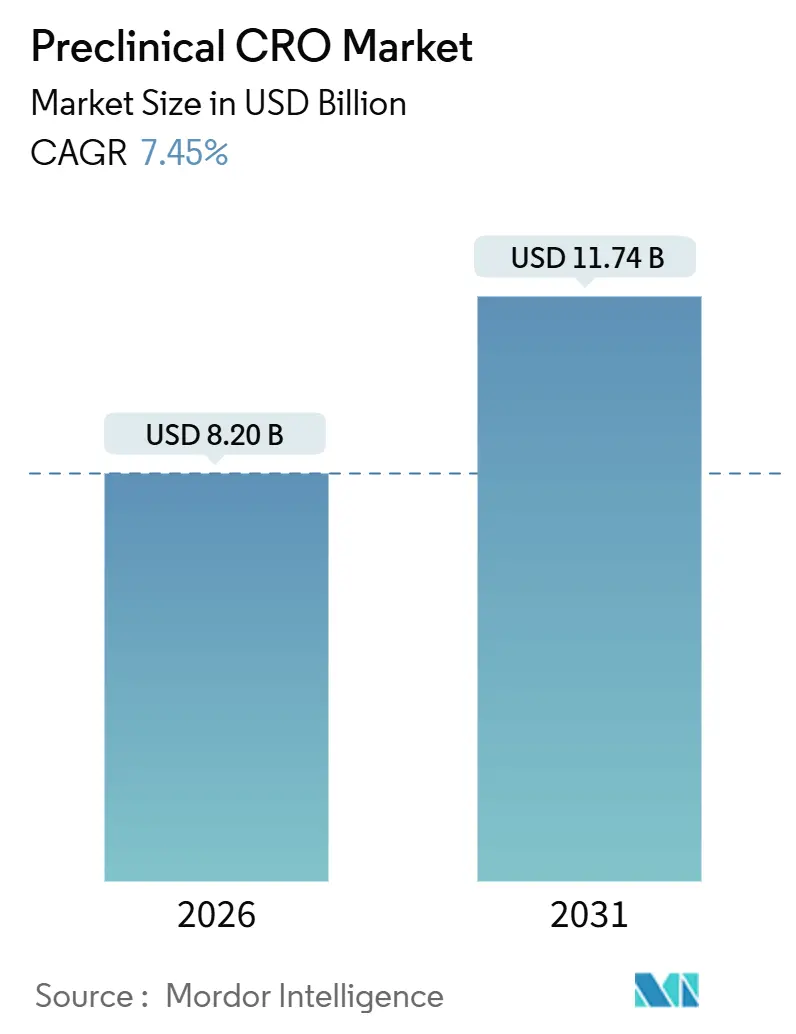

| Market Size (2026) | USD 8.20 Billion |

| Market Size (2031) | USD 11.74 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

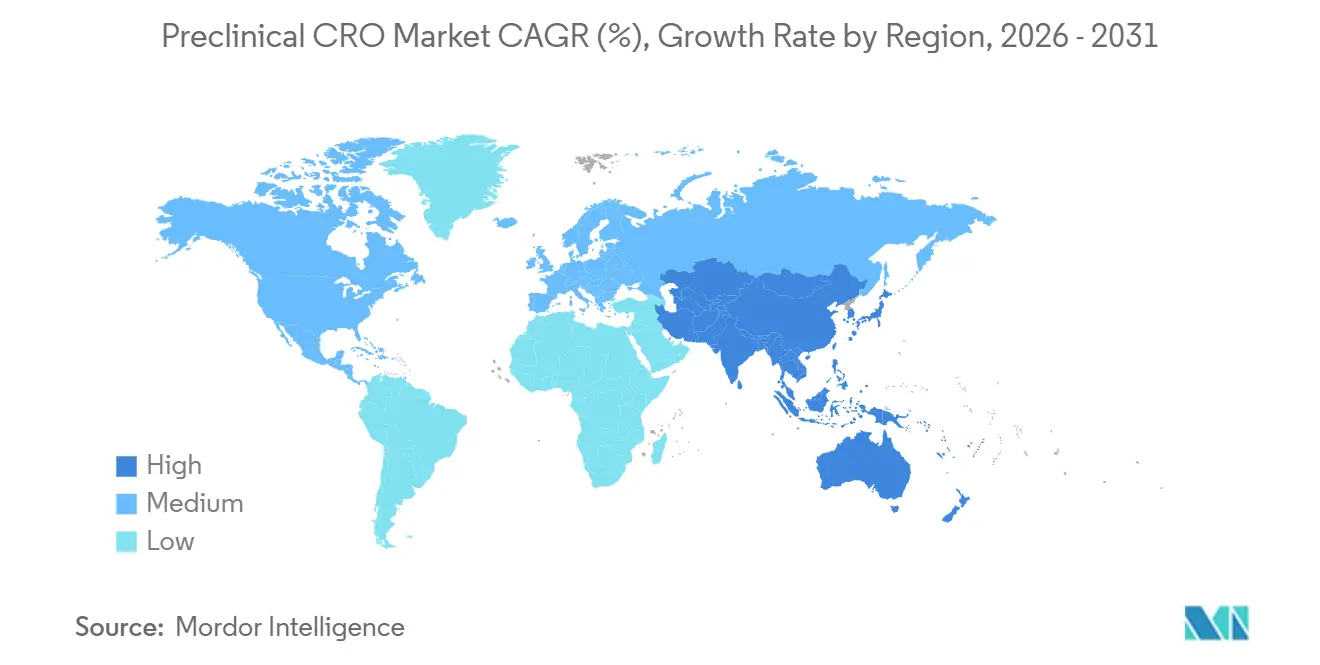

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Preclinical CRO Market Analysis by Mordor Intelligence

The Preclinical CRO Market size is estimated at USD 8.20 billion in 2026, and is expected to reach USD 11.74 billion by 2031, at a CAGR of 7.45% during the forecast period (2026-2031).

The rise of asset-light R&D models, the U.S. FDA Modernization Act 2.0, and accelerating adoption of AI-enabled in-silico platforms are reshaping sponsor strategies and allowing CRO partners to compress timelines and reduce development risk. ICH M3(R2) updates, coupled with cardiovascular liability concerns for novel modalities, continue to elevate the profile of safety pharmacology, while patient-derived organoids are challenging patient-derived xenograft (PDX) dominance by delivering faster, more predictive oncology data. Asia-Pacific enjoys a double-digit tailwind, driven by cost advantages in China and India, whereas North America retains its anchor position due to regulatory proximity, established GLP infrastructure, and rapid study-start capability. Competitive intensity is rising as mid-tier CROs leverage AI-guided study design, while consolidation among top players consolidates GLP capacity and broadens geographic footprints.

Key Report Takeaways

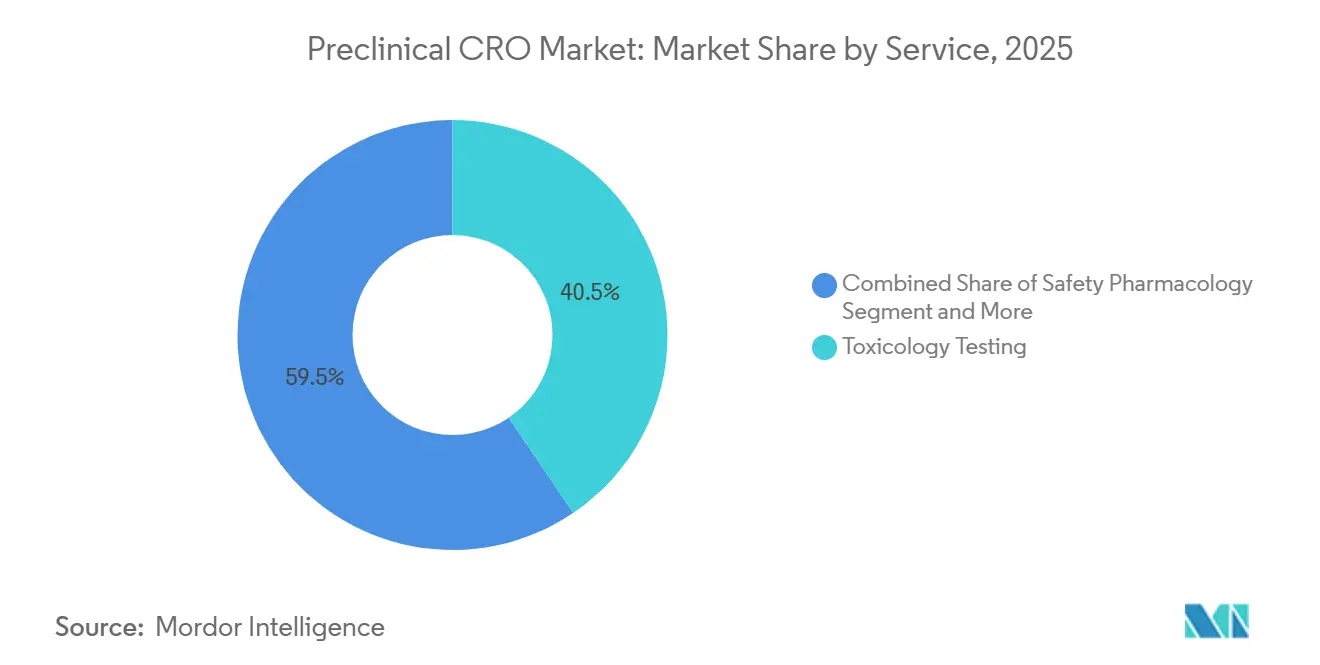

- By service, toxicology commanded a 40.55% preclinical CRO market share in 2025, while safety pharmacology expanded at a 12.25% CAGR through 2031.

- By model type, patient-derived xenografts led with 53.53% revenue share in 2025, but patient-derived organoids are forecast to advance at a 13.85% CAGR to 2031.

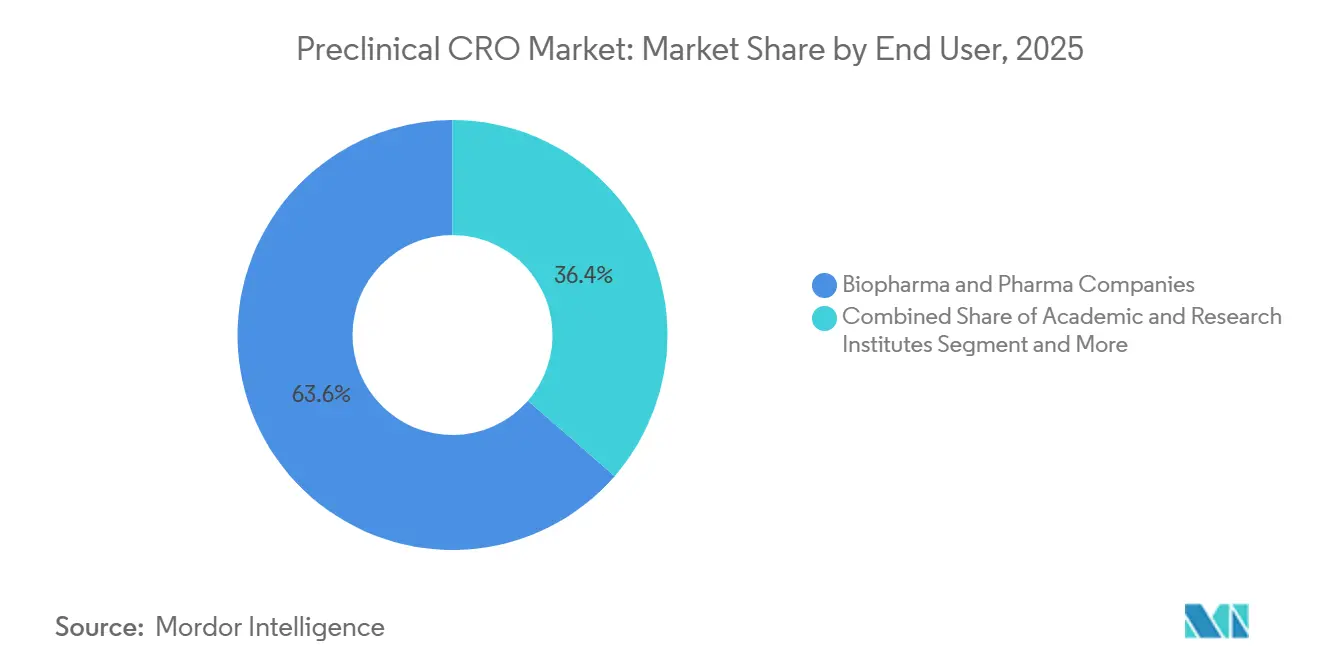

- By end user, biopharma captured 63.63% of 2025 spending, whereas academic and research institutes are growing at an 11.87% CAGR through 2031.

- By geography, North America held 45.13% of 2025 revenue, and Asia-Pacific is poised to grow at a 10.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Preclinical CRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing R&D expenditure in drug discovery | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of preclinical pipelines | +1.5% | Global, APAC spill-over from Western biotech hubs | Long term (≥ 4 years) |

| Cost & time efficiency from outsourcing | +1.3% | North America & EU core, emerging adoption in APAC | Short term (≤ 2 years) |

| Adoption of AI-enabled in-silico models | +1.2% | North America, EU, early gains in China and India | Medium term (2-4 years) |

| Demand for CRO capabilities in advanced therapies | +1.4% | North America & EU dominance, emerging in China and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing R&D Expenditure in Drug Discovery

Pharmaceutical R&D budgets soared in 2025, with Pfizer committing USD 10.7-11.7 billion yet shuttering internal toxicology labs to redirect spending toward digital pathology capabilities[1]Pfizer, “2025 Form 10-K,” pfizer.com. CROs absorbed 35-40% of toxicology workflows as oncology and rare-disease sponsors pursued episodic preclinical packages rather than maintaining fixed in-house capacity. NIH extramural funding reached USD 22.3 billion, with 18% earmarked for IND-enabling research that necessitates GLP-compliant endpoints from external partners. Small biotechs filed 62% of U.S. INDs in 2024, further insulating the preclinical CRO market from downturns in large-pharma pipelines. The resulting demand shift has strengthened CRO bargaining power on pricing and schedule priority.

Expansion of Preclinical Pipelines

More than 8,200 active preclinical programs were in play during 2025, including 1,450 cell and gene therapy candidates, up 22% from 2023. EMA’s revised ATMP guideline now mandates two-species vector shedding studies, effectively doubling workloads for gene-therapy CRO groups. GLP-1 receptor agonists and APOE4-targeted drugs added 340 new pipeline entries, each requiring multi-species toxicology and CNS penetration assays. Chinese sponsors alone initiated 1,100 programs and are partnering with Western CROs to secure dual-market data packages, creating back-to-back study requests for the same compound series. The broadened pipeline has compressed GLP capacity, prompting CROs to fast-track facility expansions.

Cost and Time Efficiency from Outsourcing

Outsourcing a 13-week GLP toxicology study costs USD 450,000-650,000, whereas maintaining a fully accredited vivarium can exceed USD 3-5 million per year, a break-even threshold viable only for sponsors running at least 8-10 studies annually. Virtual biotechs, representing 48% of recent IND submissions, rely exclusively on CRO networks and increasingly prefer integrated “IND-Ready” bundles that consolidate DMPK, toxicology, and bioanalysis under a single contract. CROs have introduced milestone-linked pricing that defers 20-30% of study fees until successful IND acceptance, conserving sponsor liquidity while aligning incentives. Parallel rodent and non-human-primate studies across multi-site facilities now trim IND timelines to 11-12 months, well below legacy in-house cycles.

Adoption of AI-Enabled In-Silico Models

Insilico Medicine’s rentosertib advanced to Phase 2a in 2025 using computational toxicology and organ-on-chip platforms for lead optimization, exemplifying a paradigm where AI guides preclinical decisions. FDA’s 2024 Alternative Methods Roadmap endorses validated QSAR and PBPK models, and Crown Bioscience’s HuPrime AI reduces required PDX cohorts by 60%, saving 40% in direct costs. EMA bioanalytical guidance now permits PBPK simulations in lieu of certain bridging studies, channeling budgets from animal DMPK to computational biology. Sponsors routinely run in-silico screens before committing to GLP studies, concentrating deferred capital on higher-probability assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardization & data interoperability | -0.6% | Global, acute in North America and EU multi-CRO programs | Short term (≤ 2 years) |

| Stringent regulatory & animal-welfare compliance | -0.5% | EU and North America core, emerging in APAC | Medium term (2-4 years) |

| Shortage of skilled in-vivo pharmacology talent | -0.4% | Global, most severe in North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardization and Data Interoperability

SEND validation errors affected 38% of 2024 IND submissions, forcing resubmissions and adding 30-60 days to FDA review times. Proprietary LIMS platforms hinder data merging across CRO partners, imposing 15-20% budget overruns on sponsors who must reconcile histopathology and clinical pathology datasets manually. Only 12 of the top 20 CROs joined Pistoia Alliance’s FAIR Preclinical Data initiative by mid-2026, prolonging metadata fragmentation. Consolidation to preferred-provider panels has therefore intensified as sponsors aim to contain integration overhead.

Stringent Regulatory and Animal-Welfare Compliance

EU Directive 2010/63/EU adds 8-12 weeks to animal-study approvals and lifts per-study administrative costs by 12-15% versus comparable U.S. projects. AAALAC accreditation now incorporates unannounced inspections, raising annual compliance costs to USD 1.2-1.8 million for Western CROs. Talent shortages exacerbate delays; fewer than 50 new board-certified toxicologic pathologists emerge globally each year, falling short of retirements by a 3:2 ratio and forcing outsourcing of histopathology reads. Sponsors often accept higher Western CRO costs to minimize regulatory risk, perpetuating cost differentials with Asia-Pacific providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Toxicology Anchors, Safety Pharmacology Accelerates

Toxicology testing delivered a 40.55% preclinical CRO market share in 2025, reflecting its obligatory role in IND-enabling packages under ICH M3(R2)[2]International Council for Harmonisation, “ICH M3(R2),” ich.org. Repeat-dose studies in two species remain standard, even as organ-on-chip tools displace some exploratory work. Safety pharmacology, however, is racing ahead at a 12.25% CAGR, buoyed by rising cardiovascular liability concerns and a surge in hERG channel and QT interval investigations. The preclinical CRO market size for safety pharmacology is forecast to double by 2031 as more sponsors run conscious telemetered dog studies for kinase inhibitors. Bioanalysis and DMPK remain pivotal for complex modalities such as antibody-drug conjugates, where intact antibody and payload quantification demand specialized LC-MS/MS expertise. Integrated “IND-Ready” bundles continue to gain traction, embedding formulation and DMPK services into fixed-price toxicology packages that simplify procurement for biopharma sponsors.

The rise of organ-on-chip platforms introduces hybrid workflows: sponsors screen multiple leads on microphysiological systems, advance the most promising into GLP studies, and reduce late attrition. The FDA-qualified Liver-Chip now replaces some exploratory hepatotoxicity studies, yet full animal packages remain mandatory for global filings, limiting immediate substitution potential. Genotoxicity work is partially shifting to in-silico QSAR, but regulators still insist on confirmatory Ames and micronucleus tests, preserving a stable revenue floor for wet-lab assays.

By Model Type: PDX Dominates, PDO Disrupts

PDX models produced 53.53% of 2025 model-type revenue, anchored by their high predictive value for targeted oncology therapies. The preclinical CRO market size for PDX studies is projected to climb steadily as immuno-oncology pipelines advance. PDO platforms, expanding at a 13.85% CAGR, can generate efficacy data in eight weeks versus six months for PDX, enabling sponsors to evaluate 3-4 compounds in the time historically needed for one. Cost gaps are narrowing, with PDO assays priced at USD 15,000-25,000 per sample compared to USD 30,000-50,000 for PDX engraftment. Sponsors increasingly triangulate findings by running both models in parallel, enhancing confidence in clinical go-forward decisions.

Growth in AI-guided prediction is strengthening model selection. Platforms such as HuPrime AI predict PDX response based on tumor genomics, reducing the number of animals required and trimming overhead. Regulatory validation of Simcyp PBPK for pediatric dosing further bolsters computational models, although immune-mediated toxicities still necessitate non-human-primate studies, sustaining baseline demand for traditional in-vivo work.

By End User: Biopharma Leads, Academia Gains Velocity

Biopharma sponsors captured 63.63% of 2025 spending, leveraging outsourcing to preserve capital for discovery programs and limit fixed infrastructure[3]Pharmaceutical Research and Manufacturers of America, “2025 Industry Profile,” phrma.org . Academic and research institutes, however, are growing at an 11.87% CAGR on the back of NIH mandates that require GLP toxicology data for IND-enabling grants. The preclinical CRO market size tied to academic users is therefore widening faster than for traditional pharma, aided by turnkey packages that pair study design with regulatory consulting. Public-private consortia, such as BARDA’s USD 450 million pandemic-countermeasure fund, are routing 70% of resources to CROs, spurring demand for accelerated toxicology under compressed timelines.

Virtual biotechs, a subset of the biopharma category, now account for nearly half of U.S. IND submissions. With no internal vivaria, these firms commission soup-to-nuts CRO engagements that include protocol development, dose escalation, safety pharmacology, and SEND submission. Their growth adds structural resilience to the preclinical CRO market, even when big-pharma pipelines cycle down.

Geography Analysis

North America accounted for 45.13% of 2025 revenue, buoyed by FDA proximity, AAALAC-certified infrastructure, and the ability to initiate studies within four to six weeks of contract signature. The region’s dominance is reinforced by rapid ethical review processes compared with Europe, where stricter animal-use audits delay starts. Nonetheless, preclinical CRO market size in Asia-Pacific is forecast to climb at a 10.81% CAGR through 2031, reflecting China’s duty-free import policies and India’s alignment with ICH guidelines. WuXi AppTec expanded its Suzhou campus by 12,000 square meters in 2025, a move that allows more than 600 IND-ready studies annually for a global clientele.

Europe remains indispensable for large-animal cardiovascular pharmacology. Labcorp’s acquisition of a U.K. facility added capacity for conscious telemetered dog studies, which often become rate-limiting for kinase inhibitor programs. South America and the Middle East & Africa sit at earlier adoption stages; however, Brazil’s AAALAC-accredited São Paulo site, opened in 2025, signals nascent regional momentum.

Cross-border demand is reshaping site strategy. Many Western sponsors run exploratory work in Asia-Pacific for cost reasons but conduct pivotal GLP studies in North America or Europe to ease audits. This dual-sourcing model puts pressure on CROs to maintain consistent data standards across regions.

Mordor Intelligence provides coverage of the preclinical cro market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The top players, Charles River Laboratories, Labcorp Drug Development, WuXi AppTec, Eurofins, and others, controlled a significant share of global revenue in 2025, giving the preclinical CRO market a moderate concentration profile. Charles River’s USD 1.9 billion purchase of Explora BioLabs in 2024 added European large-animal surgery capacity, directly contesting Labcorp’s cardiovascular niche. Mid-tier firms differentiate through AI infrastructure; Syngene’s BioInformatics Hub optimizes dose escalation and reduces animal use by 25%, delivering clear 3Rs advantages to risk-averse sponsors.

Organ-on-chip vendors blur the line between technology and service. Emulate Bio’s FDA-qualified Liver-Chip now competes for exploratory hepatotoxicity budgets, creating a disruptive flank that traditional CROs must address. Asia-Pacific players continue to offer 30-40% cost savings, yet only 22 of China’s 80+ CROs hold AAALAC accreditation, limiting access to Western regulatory filings. Preferred-provider panels and rigorous data-quality audits favor incumbents with global GLP footprints, while niche specialists capture price premiums for advanced-therapy assays such as AAV biodistribution and tumorigenicity testing.

Preclinical CRO Industry Leaders

Labcorp Drug Development

Eurofins Scientific

WuXi App Tec

SGS SA

Charles River Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Avance Clinical launched an Early Phase Center of Excellence for biotechs to streamline IND-enabling packages and deliver cost-optimized early-phase studies.

- March 2025: ERBC unified its six preclinical entities under the single brand ERBC, positioning itself as a one-stop preclinical service provider.

Global Preclinical CRO Market Report Scope

As per the scope of this report, preclinical contract research organizations (CROs) specialize in ensuring a seamless procedure with reliable results for each test. Prior to entering clinical trials (or receiving other approvals like 510Ks) or being used for human care, preclinical CROs assist new medical product developers in demonstrating their products' safety and efficacy in live models that the FDA considers as close as possible to the human anatomy.

The preclinical CRO market is segmented by service into toxicology testing, bioanalysis and DMPK studies, safety pharmacology, and other services. By model type, the market is categorized into patient-derived organoid (PDO) models, patient-derived xenograft (PDX) models, and AI-driven or in-silico models. By end user, the market is divided into biopharma and pharmaceutical companies, academic and research institutions, and other users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

| Toxicology Testing |

| Bioanalysis & DMPK Studies |

| Safety Pharmacology |

| Other Services |

| Patient-Derived Organoid (PDO) Models |

| Patient-Derived Xenograft (PDX) Models |

| In-silico / AI-Driven Models |

| Biopharma & Pharma Companies |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Toxicology Testing | |

| Bioanalysis & DMPK Studies | ||

| Safety Pharmacology | ||

| Other Services | ||

| By Model Type | Patient-Derived Organoid (PDO) Models | |

| Patient-Derived Xenograft (PDX) Models | ||

| In-silico / AI-Driven Models | ||

| By End User | Biopharma & Pharma Companies | |

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the preclinical CRO market in 2031?

The preclinical CRO market is forecast to reach USD 11.74 billion by 2031 based on a 7.45% CAGR.

Which service category is growing fastest in outsourced preclinical studies?

Safety pharmacology leads growth, advancing at a 12.25% CAGR due to heightened cardiovascular liability scrutiny.

Why are patient-derived organoids gaining traction over PDX models?

PDOs offer 78% predictive accuracy, deliver results in eight weeks, and cost less than PDX studies, enabling faster go-no-go decisions.

How are regulatory changes influencing CRO demand in Asia-Pacific?

China's duty-free animal import policy and India's ICH alignment cut costs and approval timelines, driving a 10.81% regional CAGR.

What role does AI play in modern preclinical CRO services?

AI improves candidate screening, optimizes dose escalation, reduces animal use, and supports PBPK simulations that regulators increasingly accept.

Page last updated on: