Saudi Arabia Vehicle Reparation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.36 Billion |

| Market Size (2030) | USD 1.82 Billion |

| Growth Rate (2025 - 2030) | 6.38% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Vehicle Reparation Market Analysis by Mordor Intelligence

The Saudi Arabia vehicle reparation market size is valued at USD 1.36 billion in 2025 and is forecast to reach USD 1.82 billion by 2030, translating into a 6.38% CAGR over the period. This expansion stems from Vision 2030’s electrification agenda, the rollout of mandatory periodic technical inspection (PTI), and accelerated mechanical wear in desert operating conditions. Electrified powertrain diagnostics, digital parts procurement, and warranty-linked service packages are reshaping market economics. In parallel, parts localization initiatives—such as the Public Investment Fund (PIF) joint venture with Pirelli—are improving supply security and price stability. Consolidation pressures are rising as OEM-backed networks scale, yet locally owned shops retain strong neighborhood loyalty advantages. Workforce upskilling, grey-market parts enforcement, and subscription mobility trends remain the key strategic variables that will influence operating margins across the forecast horizon.

Key Report Takeaways

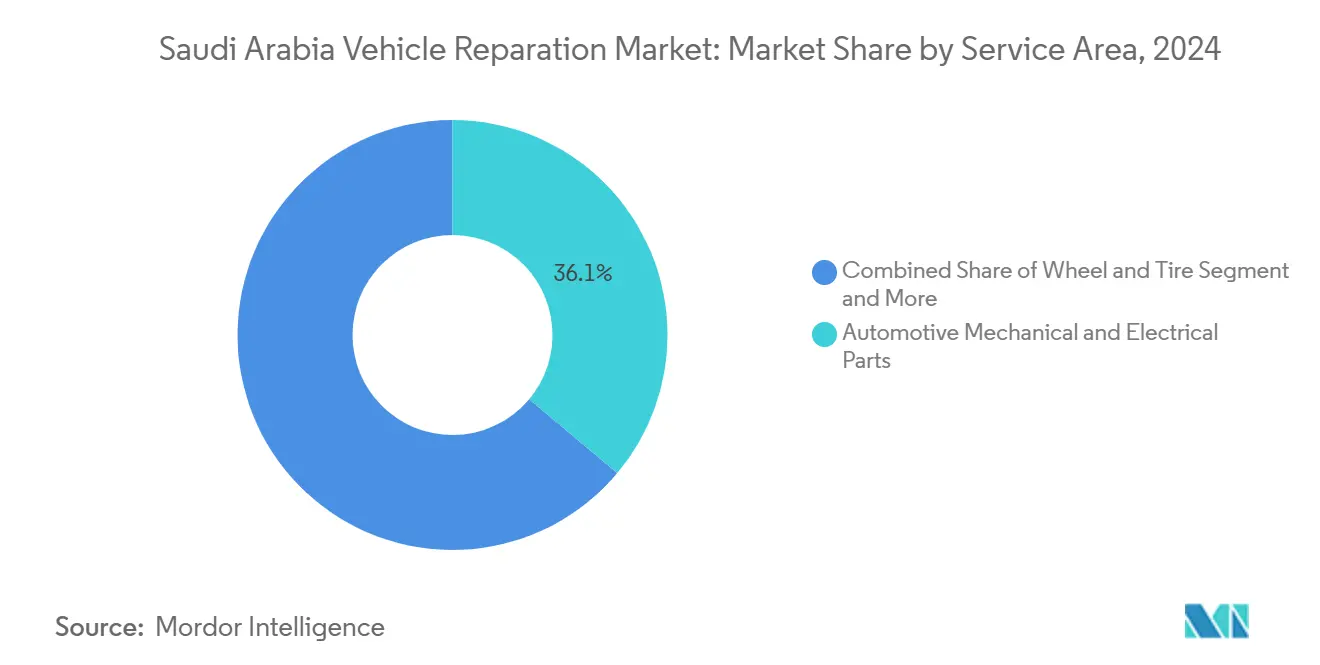

- By service area, electrified powertrains led with 36.07% revenue share in 2024; the same segment is projected to advance at an 18.94% CAGR to 2030.

- By service provider, locally owned repair shops controlled 48.21% of the Saudi Arabian vehicle reparation market share in 2024, while franchise general repairs are expected to grow at 12.38% through 2030.

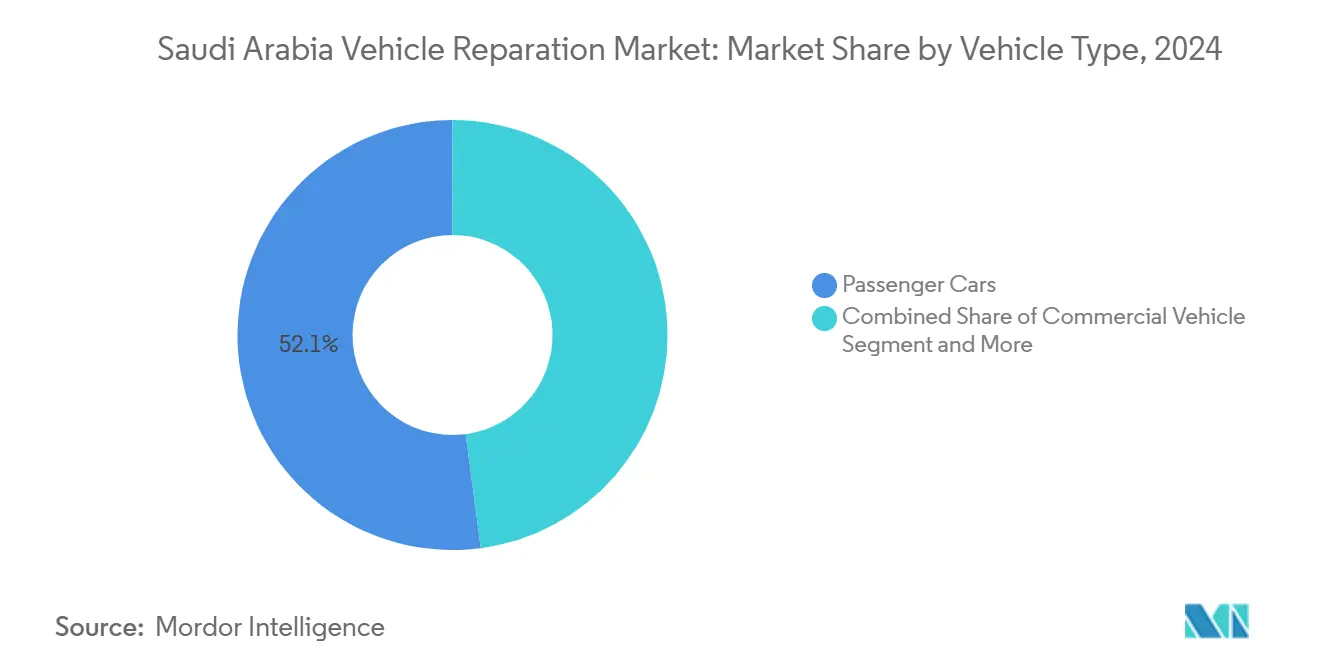

- By vehicle type, electric passenger cars accounted for 52.09% of the Saudi Arabia vehicle reparation market size in 2024 and are set to expand at a 23.11% CAGR through 2030.

- By channel, online accounted for 89.12% of the Saudi Arabian automotive heat shield market size in 2024 and is projected to expand at a 19.52% CAGR through 2030.

- By geography, the Eastern Region captured 32.18% of the Saudi Arabian automotive heat shield market size in 2024 and is forecast to grow at an 11.21% CAGR through 2030.

Saudi Arabia Vehicle Reparation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Average Vehicle Age | +1.8% | National, concentrated in Central and Western regions | Medium term (2-4 years) |

| Mandatory Periodic Technical Inspection (PTI) Roll-Out | +1.2% | National, with early gains in Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| OEM-Backed Extended Warranty Programmes | +0.9% | National, strongest in Eastern and Central regions | Medium term (2-4 years) |

| Growth of Used-Car Trading Platforms | +0.8% | National, with digital penetration highest in major cities | Short term (≤ 2 years) |

| Electrified-Powertrain Service-Tool Localization | +0.7% | Eastern Region core, spill-over to Central and Western | Long term (≥ 4 years) |

| Accelerated Desert-Climate Component Fatigue | +0.6% | National, most severe in Northern and Central regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Average Vehicle Age

Fleet aging dynamics reshape repair demand patterns as Saudi Arabia's vehicle import surge creates a maintenance wave effect. The Kingdom imported over 1 million vehicles in the 15 months to March 2024, valued at SAR 83 billion (USD 22.1 billion), with this influx now entering service-intensive lifecycle phases[1]"Saudi Arabia imports over 1 million vehicles in 15 months," Arab News, arabnews.com.. Professional detailing services alone can increase resale value by 5-15%, while minor body repairs average SAR 300-800 and tire replacement approximately SAR 1,200 per set, indicating substantial aftermarket revenue potential[2]Abdul Rahman, "How to Sell a Car in Saudi Arabia: 2025's Smart Seller's Guide," icartea.com.. The convergence of aging ICE fleets with emerging EV adoption creates a bifurcated service landscape where traditional mechanical expertise must coexist with high-voltage electrical competencies. This trend particularly benefits locally-owned repair shops that can offer cost-effective solutions for older vehicle maintenance while building capabilities for newer technology platforms.

Mandatory Periodic Technical Inspection (PTI) Roll-out

The Saudi Standards, Metrology and Quality Organization (SASO) has digitized vehicle inspection processes through the Vehicle Safety app, creating systematic demand for compliance-driven repairs and component replacements. PTI implementation generates recurring revenue streams for repair providers as vehicle owners must address identified deficiencies to maintain registration validity, with the Ministry of Interior's Absher platform requiring a valid periodic inspection for registration renewal. The regulatory framework creates predictable demand cycles that favor established service providers with certified inspection capabilities and parts inventory management systems. Digital inspection booking and reporting systems reduce administrative friction while increasing transparency, potentially shifting market share toward providers who can demonstrate compliance track records and rapid turnaround times. This regulatory standardization also creates barriers for informal repair operators who lack certification infrastructure, accelerating market consolidation toward compliant service networks.

OEM-backed Extended Warranty Programs

Manufacturer warranty expansion strategies are reshaping competitive dynamics as OEMs leverage service revenue to offset margin pressure from local assembly requirements and import competition. Extended warranty programs create captive service demand while establishing quality benchmarks that independent operators must match to retain market share. The King Salman Automotive Cluster's development will house OEM headquarters and manufacturing facilities for CEER, Lucid, and Hyundai joint ventures, creating integrated service ecosystems that combine manufacturing, parts supply, and warranty fulfillment. This localization trend enables OEMs to offer more competitive warranty terms while building service network density, particularly in the Eastern Region, where automotive industrial activity concentrates. Independent repair providers face pressure to achieve OEM certification standards or risk losing market access as warranty coverage expands across vehicle categories and extends service intervals.

Growth of Used-Car Trading Platforms

Digital marketplaces are transforming vehicle lifecycle management and creating new repair demand patterns as platforms like Syarah, Hatla2ee, and Haraj Motors facilitate rapid vehicle turnover cycles. Hatla2ee's Saudi platform shows substantial inventory depth with Toyota leading at 152 listings, followed by Hyundai at 70 and Mercedes at 41[3],"hatla2ee," ksa.hatla2ee.com. indicating active secondary market circulation. Digital ownership transfer processes are now complete within 48 hours through Absher integration, accelerating vehicle circulation and creating more frequent pre-sale preparation opportunities for repair providers. Platform-driven price transparency and condition assessments incentivize sellers to invest in cosmetic and mechanical improvements, generating consistent demand for minor bodywork, diagnostics, and reconditioning services. The shift toward digital valuation tools and instant quote systems creates market efficiency that rewards repair providers who can deliver rapid, cost-effective improvements that maximize resale values.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Master Technicians | -1.1% | National, most acute in Northern and Southern regions | Medium term (2-4 years) |

| Fragmented Spare-Parts Supply Chain | -0.8% | National, with grey-market concentration in border regions | Short term (≤ 2 years) |

| Growing Popularity of Subscription Mobility | -0.7% | Central and Western regions, urban concentration | Long term (≥ 4 years) |

| Grey-Market Parts Influx from Neighbouring GCC States | -0.6% | Eastern Region and border areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Master Technicians

Workforce development challenges constrain market expansion as the transition toward electrified powertrains requires specialized competencies that existing training infrastructure cannot rapidly supply. The Technical and Vocational Training Corporation (TVTC) provides foundational automotive programs, but EV-specific certifications for high-voltage systems, battery thermal management, and software diagnostics remain limited. Skills Verification Program (SVP) requirements affect foreign technician mobility, potentially reducing the influx of experienced EV specialists from markets with mature electrification programs. Vision 2030's human capability development initiatives emphasize digital automotive technologies and EV maintenance training, but implementation timelines lag behind market demand acceleration. This skills gap particularly affects smaller repair operators who lack resources for specialized training programs, creating competitive advantages for larger service networks with dedicated training capabilities.

Fragmented Spare-Parts Supply Chain

Supply chain fragmentation undermines service quality and creates safety risks as counterfeit components infiltrate repair networks through inadequate verification systems. Saudi Arabia accounts for approximately 3.3% of global counterfeit trade, with car parts representing a commonly counterfeited category that poses significant safety hazards. Saudi Customs destroyed over 2 million counterfeit goods in 2020, including car filters, but enforcement gaps persist, particularly for small-parcel shipments and cross-border component assembly. The OECD's 2025 counterfeit mapping study identifies automotive spare parts as increasingly targeted through online marketplaces and small-parcel postal channels, with average counterfeit part values exceeding USD 300 due to more complex component counterfeiting. Balubaid Group's implementation of integrated ERP systems with real-time inventory visibility and automated quality checks demonstrates how technology solutions can address supply chain integrity challenges, though adoption remains uneven across smaller operators. Regulatory compliance frameworks under ZATCA e-invoicing requirements are improving traceability, but enforcement capacity limitations allow grey-market infiltration to persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Area: Electrified Powertrains Drive Market Evolution

The emergence of automotive mechanical and electrical parts as both the largest segment (36.07% market share in 2024) and fastest-growing category (18.94% CAGR 2025-2030) reflects Saudi Arabia's strategic pivot toward EV manufacturing and adoption under Vision 2030 initiatives. CEER's establishment as the Kingdom's first domestic EV manufacturer, combined with Lucid's local assembly operations in King Abdullah Economic City, creates concentrated demand for specialized diagnostic equipment, battery management systems, and high-voltage safety protocols. Traditional automotive mechanical and electrical parts maintain substantial market presence but face margin pressure as repair complexity shifts toward software-driven diagnostics and thermal management systems.

The PIF and Pirelli's USD 550 million tire manufacturing facility signals supply chain localization efforts that will reshape parts availability and pricing dynamics across service categories. Glass replacement services face disruption from advanced driver assistance systems (ADAS) integration that requires specialized calibration equipment and certified technicians, creating barriers for smaller operators. The "Others" category encompasses emerging service areas, including software updates, over-the-air diagnostics, and cybersecurity maintenance, that traditional segmentation frameworks struggle to capture but represent significant future revenue potential.

By Service Provider: Local Operators Navigate Consolidation Pressures

Locally-owned repair shops command 48.21% market share in 2024 while maintaining 12.38% growth through 2030, demonstrating resilience despite intensifying competition from franchise networks and OEM-backed service expansion. Their competitive advantages center on cost flexibility, geographic proximity, and customer relationship depth, though these benefits face erosion as regulatory compliance requirements favor larger, certified operators with standardized processes and quality systems.

AUTOFIX's expansion as part of Bahwan International Group illustrates how regional conglomerates are consolidating fragmented service markets through multi-brand service offerings and standardized operational systems. The company's presence in Riyadh and Dammam, with expansion plans, demonstrates how successful consolidation strategies combine geographic coverage with service standardization. Petromin's acquisition of SpareIt, an Indian auto-tech platform, signals digital transformation initiatives that enable traditional service providers to compete with technology-driven entrants through enhanced customer engagement and operational efficiency.

By Vehicle Type: Electric Passenger Cars Reshape Service Demand

Passenger cars dominate vehicle type segmentation with 52.09% market share in 2024 and lead growth projections at 23.11% CAGR through 2030, reflecting the Kingdom's accelerated EV adoption strategy and manufacturing localization initiatives. This segment's expansion creates fundamental shifts in service requirements from traditional powertrain maintenance toward battery diagnostics, charging system maintenance, and software update capabilities that require specialized equipment and training.

Busesand coaches are transformed through public transport electrification initiatives in Riyadh and other major cities, creating specialized service demand for fleet operators and municipal authorities. The shift toward electric passenger cars also drives ancillary service opportunities, including home charging installation, battery recycling, and end-of-life vehicle processing,g that traditional repair frameworks do not adequately capture.

By Channel: Digital Transformation Accelerates Market Access

Online channels capture 89.12% market share in 2024 with 19.52% growth through 2030, demonstrating how digital platforms are reshaping customer acquisition, service booking, and parts procurement in a market historically dominated by physical interactions. This digital dominance reflects broader e-commerce adoption patterns and consumer preferences for transparent pricing, service scheduling, and progress tracking that traditional offline channels struggle to match.

Offline channels maintain relevance for complex diagnostics, specialized repairs, and customer segments that prefer direct interaction, but their 10.88% market share reflects declining influence in customer acquisition and transaction processing. Balubaid Group's integration of Odoo ERP systems with Magento e-commerce platforms demonstrates how successful operators bridge online and offline capabilities through unified inventory management, customer relationship systems, and multi-channel order processing.

Geography Analysis

The Eastern Region’s lead is anchored in its dual role as an import gateway and an industrial heartland. King Abdul Aziz Port funnels vehicles to pre-delivery inspection centers, ensuring immediate service demand before units reach showrooms. The King Salman Automotive Cluster will intensify regional specialization by co-locating stamping, assembly, and service-parts warehousing, cutting lead times for warranty repairs. Western Region providers cater to luxury brands whose owners demand OEM stamp-validated work, supporting higher labor rate realization. Central Region workshops benefit from government fleet contracts where preventive maintenance schedules are rigidly enforced, guaranteeing baseline volumes.

Northern Region potential lies in cross-border commerce with Jordan, requiring robust parts logistics to meet quick-turnaround expectations. The Southern Region, characterized by dispersed populations, relies on mobile service vans and hub-and-spoke parts depots to maintain service levels despite lower vehicle density.

Competitive Landscape

More than 650 licensed entities serve the Saudi Arabian vehicle repair market, yet the top five hold under 30% combined revenue, confirming a fragmented structure. Abdul Latif Jameel Motors, Petromin, and Al Jomaih Automotive field nationwide networks, but locally owned shops fill geographic and price niches. Strategic moves center on digitalization, technician upskilling, and vertical integration. AUTOFIX rolled out rapid-service formats in Riyadh malls to capture time-constrained consumers. OEMs increasingly bundle connected-vehicle data subscriptions with maintenance plans, shifting value creation toward software.

White-space opportunities include high-voltage battery refurbishment, ADAS calibration centers, and circular-economy parts recycling. Regulatory focus on counterfeit suppression favors players able to demonstrate parts provenance via blockchain or QR-code systems. Insurers such as Najm funnel collision repairs to certified shops, creating volume pools that non-network garages struggle to access.

Saudi Arabia Vehicle Reparation Industry Leaders

-

Abdul Latif Jameel Motors

-

Petromin

-

Al Jomaih Automotive

-

Al-Jazirah Vehicles Agencies

-

SAMACO Automotive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saudi new light-vehicle sales reached 72,388 units in February 2025, up 14% year-over-year, with cumulative January-February sales of 140,311 units growing 10.9% annually. The sustained vehicle sales growth creates expanding installed base for future maintenance and repair service demand across all vehicle categories.

- September 2024: Merak Capital invested SAR 310.8 million (USD 82.8 million) in SHIFT, a Jeddah-based mobility platform operating across 57 Saudi cities with over 12,000 vehicles. The investment supports technology-driven expansion of car-sharing, chauffeur services, and logistics capabilities that create new maintenance and fleet service demand patterns aligned with Vision 2030 mobility objectives.

Saudi Arabia Vehicle Reparation Market Report Scope

| Automotive Body Parts |

| Automotive Mechanical and Electrical Parts |

| Wheel and Tire |

| Interior Parts |

| Glass |

| Others |

| Automobile Manufacturers |

| Franchise General Repairs |

| Locally-Owned Repair Shops |

| Two-Wheeler |

| Three-Wheeler |

| Passenger Cars |

| Commercial Vehicle |

| Buses and Coaches |

| Offline |

| Online |

| Central Region (Riyadh, Qassim) |

| Western Region (Makkah, Madinah) |

| Eastern Region (Dammam, Khobar) |

| Northern Region (Tabuk, Al-Jouf) |

| Southern Region (Asir, Jazan, Najran) |

| By Service Area | Automotive Body Parts |

| Automotive Mechanical and Electrical Parts | |

| Wheel and Tire | |

| Interior Parts | |

| Glass | |

| Others | |

| By Service Provider | Automobile Manufacturers |

| Franchise General Repairs | |

| Locally-Owned Repair Shops | |

| By Vehicle Type | Two-Wheeler |

| Three-Wheeler | |

| Passenger Cars | |

| Commercial Vehicle | |

| Buses and Coaches | |

| By Channel | Offline |

| Online | |

| By Geography | Central Region (Riyadh, Qassim) |

| Western Region (Makkah, Madinah) | |

| Eastern Region (Dammam, Khobar) | |

| Northern Region (Tabuk, Al-Jouf) | |

| Southern Region (Asir, Jazan, Najran) |

Key Questions Answered in the Report

How large is the Saudi Arabia vehicle reparation market in 2025?

The market stands at USD 1.36 billion in 2025 with a forecast CAGR of 6.38% to 2030.

Which service area generates the most revenue?

Electrified powertrains contribute 36.07% of 2024 revenue and are growing the fastest.

What share do online channels hold?

Digital platforms account for 89.12% of bookings and parts sales in 2024.

Why is the Eastern Region dominant?

Its port infrastructure, industrial fleets, and proximity to emerging OEM plants drive a 32.18% market share.

What is the main restraint facing repair providers?

A shortage of certified master technicians limits capacity, especially for EV systems.

Which vehicle type offers the strongest growth outlook?

Electric passenger cars, expanding at a projected 23.11% CAGR through 2030, will create the highest incremental service demand.

Page last updated on: